- Semiconductor Materials & Components

- Quantum Sensors Market

Quantum Sensors Market Size, Share, and Growth Forecast 2026 - 2033

Quantum Sensors by Sensor Type (Atomic Clocks, Magnetic Sensors, PAR Sensors, Gravity Sensors, Gyroscopes, Imaging & LiDAR Sensors, Temperature Sensors, Others), by Industry (Defense & Aerospace, Oil & Gas, Mining, IT and Telecommunication, Medical and Healthcare, Transportation & Automotive, Others), by Regional Analysis, 2026 - 2033

Quantum Sensors Market Size and Trend Analysis

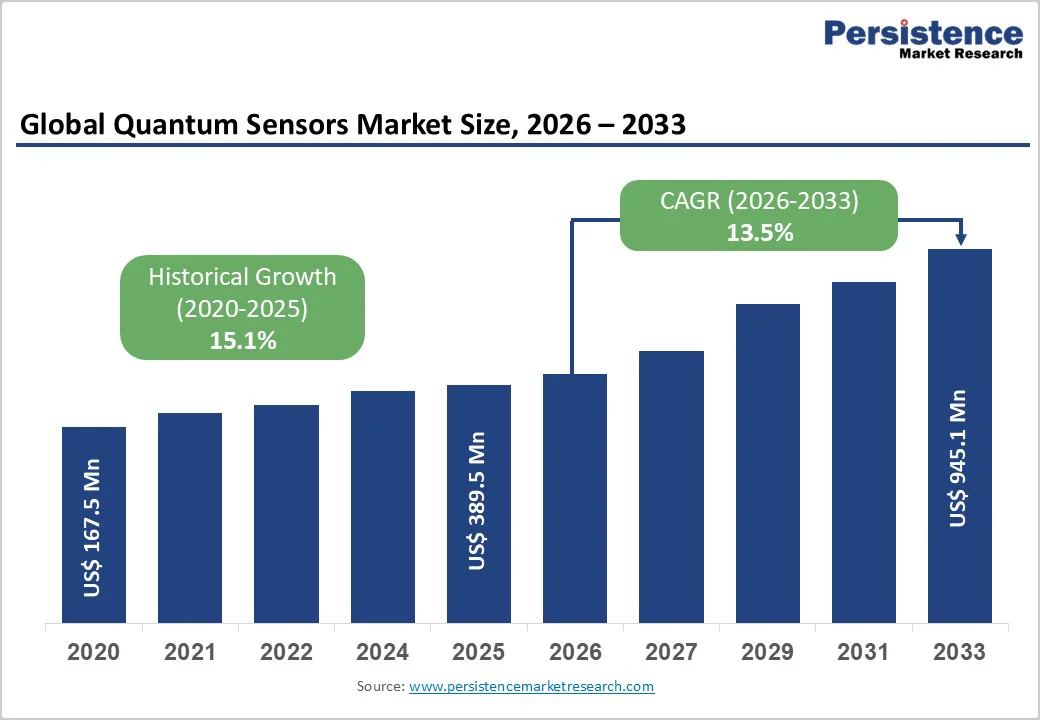

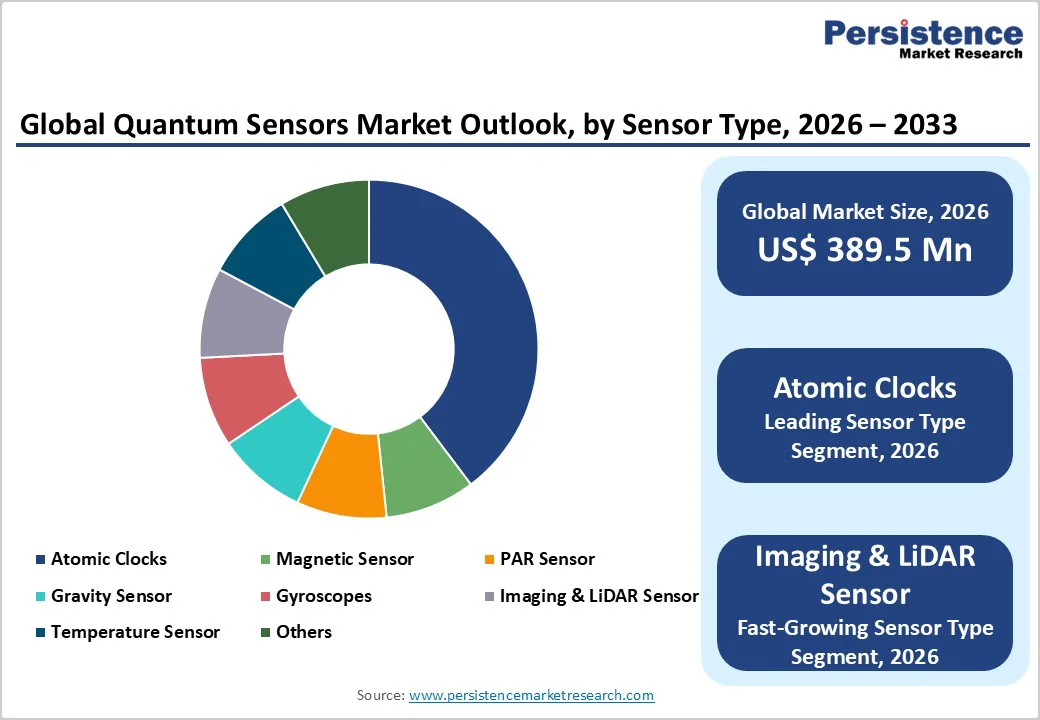

The global quantum sensors market size is projected to be approximately US$389.5 million in 2026 and is projected to reach US$945.1 million by 2033, growing at a CAGR of 13.5% during the forecast period from 2026 to 2033.

Quantum sensors mark a major leap in precision measurement, using quantum mechanics to detect physical changes with exceptionally high sensitivity and accuracy. Market growth is driven by defense and aerospace applications requiring GPS-independent navigation, healthcare adoption of quantum-enhanced imaging for earlier disease detection, and rising industrial demand in oil and gas, mining, and autonomous systems, where conventional sensors no longer meet required precision levels.

Key Market Highlights

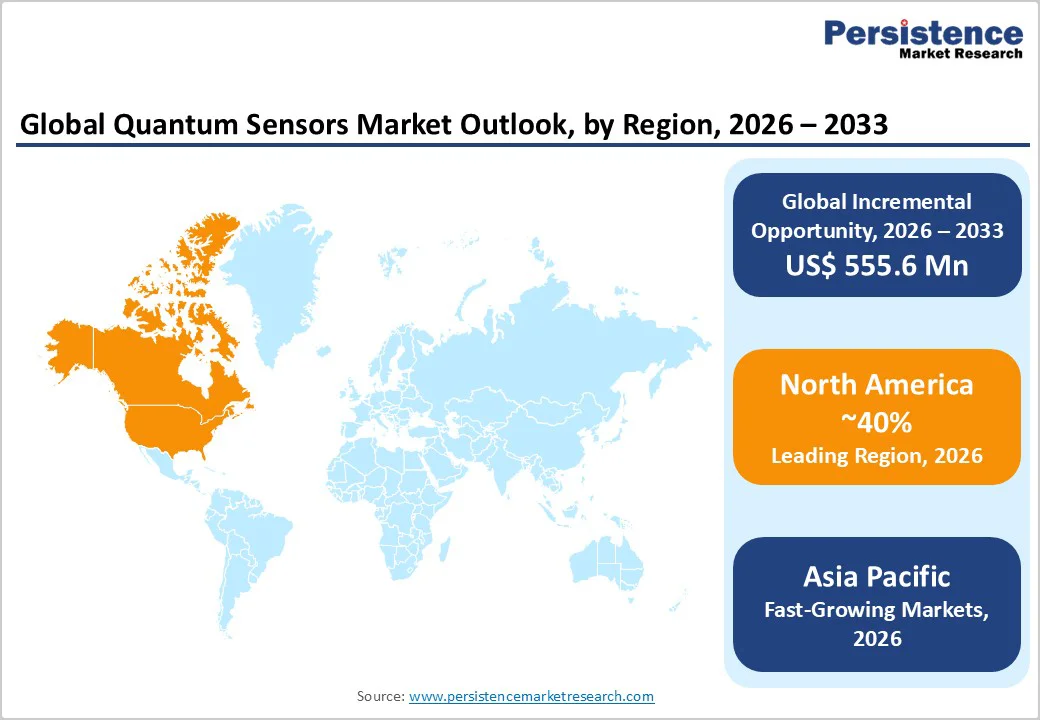

- Leading Region: North America holds about 40% market share in 2025, supported by strong U.S. defense funding and a mature quantum technology ecosystem enabling rapid development and commercialization of advanced quantum sensors.

- Fastest Growing Region: Asia Pacific is expected to achieve a 24.7% CAGR through 2032, driven by major national quantum missions in China, Japan, and India dominates in semiconductor and rare-earth materials manufacturing.

- Dominant Sensor Type Segment: Atomic clocks hold roughly 42% market share in 2025 due to long-term technology maturity, established manufacturing capabilities, and consistent procurement from defense, GPS, and telecom synchronization systems.

- Fastest Growing Sensor Type Segment: Imaging and LiDAR quantum sensors grow at 20% CAGR through 2032, fueled by rising adoption in autonomous mobility, subsurface geophysical mapping, and high-precision medical imaging applications.

- Key Market Opportunity: AI-enabled and edge-integrated quantum sensing creates multi-billion-dollar opportunities by enabling real-time analysis, predictive maintenance, and hybrid quantum-classical architectures that simplify deployment and expand commercial viability.

| Key Insights | Details |

|---|---|

|

Quantum Sensors Market Size (2026E) |

US$389.5 million |

|

Market Value Forecast (2033F) |

US$945.1 million |

|

Projected Growth CAGR (2026-2033) |

13.5% |

|

Historical Market Growth (2020-2025) |

15.1% |

Market Dynamics

Drivers - Rise in Defense and Aerospace Sector Investments

The defense sector represents the primary catalyst for quantum sensors market expansion, with DARPA, the U.S. Department of Defense, and international defense agencies investing unprecedented capital in quantum-enabled navigation and positioning systems. Q-CTRL received US$24.4 million in DARPA contracts to develop next-generation quantum navigation sensors capable of operating in GPS-denied environments, achieving up to 111-fold higher positioning accuracy than conventional inertial navigation systems.

The geopolitical imperative for technology sovereignty and the vulnerability of GPS infrastructure to jamming and spoofing have catalyzed the adoption of quantum sensors across military platforms—aircraft, submarines, and ground vehicles. Quantum magnetometers and atomic gyroscopes address critical capability gaps in contested electromagnetic environments, with government-funded research demonstrating operational viability across airborne, maritime, and ground-based defense platforms. This sector concentration ensures sustained funding pipelines through the forecast period, with procurement cycles extending from prototype demonstration through field validation to operational deployment.

Healthcare Diagnostics and Medical Imaging Revolution

The healthcare sector is the fastest-growing application segment, with a projected CAGR exceeding 20% through 2033, driven by quantum sensing’s revolutionary impact on diagnostic imaging precision. Quantum-enhanced MRI systems utilizing quantum coherence and entanglement principles generate diagnostic images with 10- 20x superior resolution compared to classical systems, enabling detection of pathological conditions at molecular and cellular scales. MIT researchers and the Quantum Economic Development Consortium document that quantum magnetometers can detect cardiac arrhythmias, neurological abnormalities indicative of Alzheimer’s disease, and early-stage malignant tumors with measurement sensitivity previously impossible through conventional technologies.

The healthcare quantum sensing market reflects institutional adoption by leading medical research centers, academic medical centers, and progressive healthcare systems investing in next-generation diagnostic capabilities. Quantum sensors for fetal monitoring, subcellular imaging, and molecular-level disease biomarker detection represent high-impact use cases that align with global healthcare system priorities for precision medicine and early intervention protocols.

Restraints - High Capital Investment and Complex Operational Requirements

The quantum sensors market faces formidable barriers stemming from prohibitive deployment costs and technical complexity, which limit commercialization velocity and market penetration. Cryogenic cooling systems for quantum sensors require continuous maintenance, with cold-atom systems demanding operating temperatures near absolute zero, necessitating sophisticated vacuum chambers, laser systems, and specialized electronics infrastructure. Operational complexity demands highly trained quantum physics specialists for installation, calibration, maintenance, and real-time data processing, creating human capital constraints that limit scalability in non-research institutional environments.

Technical sensitivity to environmental perturbations such as vibrations, electromagnetic interference, and temperature fluctuations requires deployment in controlled settings with specialized isolation infrastructure or extensive field ruggedization modifications. These barriers collectively constrain quantum sensors' adoption in cost-conscious industrial segments and emerging market geographies where infrastructure maturity remains nascent, effectively limiting near-term commercialization to defense, aerospace, healthcare research, and government scientific institutions with substantial R&D budgets.

Technology Transfer Complexity and Standardization Barriers

The transition from laboratory prototypes to scalable industrial manufacturing faces critical obstacles in standardization and knowledge transfer, extending commercialization timelines and slowing market growth. Quantum sensor technologies typically comprise integrated systems that combine multiple components, such as laser systems, vacuum chambers, optical modulators, cryogenic apparatus, signal-processing electronics, and specialized software—rather than discrete components suitable for conventional supply chain integration.

Lack of industry-wide standards for sensor calibration, performance metrics validation, and interoperability protocols impedes integration into existing operational workflows and procurement frameworks. The Quantum Economic Development Consortium and technology transfer analyses note that traditional licensing models prove ineffective for quantum sensor IP commercialization, requiring instead hands-on startup development, customer co-creation partnerships, and iterative prototype refinement through field trials.

Opportunities - Integration of Artificial Intelligence and Edge Computing for Real-Time Data Processing

Emerging opportunities leverage AI and machine learning algorithms to unlock the full analytical potential of quantum sensors, transforming raw sensor data into actionable intelligence at the point of deployment. Quantum sensors generate massive, high-dimensional datasets exceeding the processing capacity of traditional analytical frameworks, yet contain subtle signal patterns imperceptible to conventional analysis. Q-CTRL’s proprietary AI-powered software ruggedization technology, demonstrated through DARPA-funded projects, demonstrates that algorithmic optimization can enhance quantum sensor resilience to environmental noise and platform vibrations, increasing field-deployment viability and reducing infrastructure-isolation requirements.

Generative AI algorithms capable of real-time processing of sensor data, anomaly detection, and predictive maintenance represent a multi-billion-dollar opportunity for systems integrators and software platforms supporting quantum sensors deployed in autonomous systems, healthcare diagnostics, and precision manufacturing applications.

Hybrid quantum-classical sensor systems—combining quantum sensors’ drift-free, high-sensitivity measurements with classical sensors’ continuous high-frequency sampling—require sophisticated AI-driven sensor fusion architectures that reconcile heterogeneous data streams. Medical imaging equipment using quantum-enhanced MRI systems can deploy deep learning diagnostic support algorithms that extract diagnostic information from quantum sensor data, achieving accuracy surpassing that of human radiologists.

Commercial Quantum Communication and Secure Telecommunications Infrastructure Development

Quantum key distribution (QKD) systems and secure quantum communication networks represent a multi-billion-dollar near-term opportunity, with government and financial institutions deploying quantum sensors to validate communication security and ensure network integrity.

European Quantum Communication Infrastructure (EuroQCI) and China’s national quantum communication backbone investments create derived demand for quantum sensors supporting network security verification, eavesdropping detection, and quantum signal characterization. The shift toward quantum-safe cryptography standards by government cybersecurity agencies and financial institutions obligates investments in infrastructure modernization, in which quantum sensors validate secure communication channel integrity and detect quantum hacking attempts.

Telecommunications companies in North America and Europe require precision timing sensors, atomic frequency references, and quantum-enhanced synchronization technologies that quantum sensor manufacturers supply through specialized product lines. Quantum sensor-enabled telecom infrastructure supporting next-generation 5G and anticipated 6G communication systems demands precise frequency stability, phase coherence maintenance, and synchronization precision—capabilities quantum clocks and atomic frequency standards provide. Integration of quantum sensors into commercial telecom networks creates sustained revenue streams through equipment sales, upgrade cycles, and managed services supporting network reliability and performance validation.

Category-wise Analysis

Sensor Type Insights

Atomic clocks maintain clear leadership within the sensor type category, accounting for approximately 42% market share in 2025, supported by their maturity and unmatched timing precision. These systems rely on quantum transitions in rare earth elements such as cesium, rubidium, or ytterbium atoms to achieve long-term stability far superior to quartz oscillators, making them indispensable for satellite-based timing architectures. GPS constellations depend entirely on atomic clock accuracy, with each satellite housing multiple redundant units, creating recurring procurement cycles that reinforce sustained market dominance. Continued advances in optical lattice clocks provide multi-decade innovation potential by enabling higher sensitivity for scientific measurement and future space-based quantum missions.

Industry Insights

The defense and aerospace segment holds the dominant position with 45% market share in 2025, reflecting national security priorities and long-term government investment in quantum-enabled navigation, sensing, and communication. Quantum inertial systems enhance guidance accuracy in GPS-denied environments, while quantum magnetometers and gravimeters support submarine detection, underground structure mapping, and advanced surveillance capabilities. Large-scale programs such as DARPA’s RoQS initiative accelerate performance validation and operational deployment, strengthening procurement visibility. Aerospace applications—including satellite timing, deep-space navigation, and gravitational mapping—reinforce stable demand. High strategic relevance, protected budgets, and mission-critical performance requirements ensure this segment’s continued dominance through the next decade.

Healthcare emerges as the fastest-expanding end-use category, projected to grow at 20% CAGR through 2033, driven by rapid progress in quantum-enabled diagnostic technologies. Quantum magnetometers facilitate ultra-sensitive cardiac field detection, enabling identification of arrhythmias earlier than conventional ECG Devices. Quantum-enhanced MRI platforms offer superior resolution and earlier detection of neurological disorders, supporting improved clinical outcomes. The quantum sensing in the medical imaging segment is growing rapidly at a 20% CAGR, reflecting accelerating adoption. Applications such as fetal magnetocardiography further expand clinical relevance, supported by strong research activity in major medical centers.

Regional Insights

North America Quantum Sensors Market Trends

North America maintains the largest 40% share of the quantum sensors market, supported by substantial federal funding, strong research institutions, and a mature innovation ecosystem. Agencies such as DARPA, the National Science Foundation, the Department of Energy, and the U.S. Army collectively sustain multibillion-dollar quantum R&D pipelines, with quantum sensing positioned as a priority area for defense, aerospace, and advanced navigation applications. Regional manufacturing strength is reinforced by established defense contractors, specialized sensor developers, and dense startup clusters across California, Colorado, and the Northeast, which accelerate technology transfer and prototype-to-deployment cycles.

Regulatory structures, including export control regimes, further incentivize domestic production and supply chain localization, helping maintain North America’s competitive lead. In parallel, Canada contributes strong photonics and atomic physics capabilities, supported by research centers in Ontario and Quebec. Growing healthcare experimentation with quantum-enhanced imaging and diagnostics—particularly across U.S. medical research hubs—provides additional early validation opportunities and attracts venture funding for clinical-oriented quantum sensing innovations.

Europe Quantum Sensors Market Trends

Europe accounts for roughly one-quarter of global quantum sensor activity, underpinned by sustained public investment and a strong scientific base. Germany leads the regional landscape through multibillion-euro funding commitments and industrial programs emphasizing metrology, automation, and geophysical sensing applications. Broader European Union initiatives, including the Quantum Flagship and EuroQCI infrastructure rollout, reinforce demand for advanced timing, navigation, and network-security sensors supporting secure communication frameworks.

France and the United Kingdom complement this momentum with targeted national strategies that advance quantum timing systems, gravimetry platforms, and healthcare-oriented sensing technologies. Europe’s research institutions maintain global leadership in atom interferometry and optical clock development, enabling a reliable pipeline of breakthroughs transitioning into commercial solutions. Specialized companies and technical institutes also supply high-precision optical timing systems for telecom and industrial users, demonstrating strong technology maturity in select segments. Overall, Europe’s combination of coordinated public funding, academic excellence, and industrial engagement positions the region as a robust and steadily advancing quantum sensing market.

Asia Pacific Quantum Sensors Market Trends

Asia Pacific represents the fastest-growing quantum sensors market, expanding rapidly due to large-scale national investments and strong regional manufacturing capabilities. China anchors regional momentum with multibillion-dollar government programs supporting quantum sensing for defense, satellite navigation, seismic monitoring, and industrial automation. Japan’s Moonshot Program and advanced semiconductor ecosystem enable progress in quantum-enhanced imaging, optical sensing modules, and precision engineering applications. India’s National Quantum Mission accelerates development across sensing, materials research, and subsystem prototyping while fostering a growing startup ecosystem.

Across the region, semiconductor fabrication strengths in Taiwan, South Korea, and Japan support scalable production of vapor cells, diamond-defect materials, and quantum-ready photonic components, positioning the Asia Pacific as an emerging hardware manufacturing hub. Australia contributes through applied research partnerships linking quantum sensing startups with mining, defense, and environmental monitoring sectors. Additionally, Southeast Asian nations continue expanding research capabilities, creating a collaborative regional ecosystem that supports rapid commercialization and adoption of next-generation quantum sensing technologies.

Competitive Landscape

Entry barriers stay relatively high due to complex R&D requirements, long validation cycles, and regulatory restrictions on cross-border technology transfer, reinforcing a competitive environment centered on innovation rather than scale. Business strategies emphasize vertical specialization, with firms prioritizing miniaturization, ruggedization, AI-enabled performance enhancements, and manufacturability improvements to move quantum sensors from laboratory settings toward commercial deployment. Continued government funding and university commercialization programs support steady new entrant activity, further sustaining a fragmented but rapidly evolving competitive landscape.

Key Market Developments:

- September 2025: Q-CTRL received two DARPA RoQS program contracts worth US$24.4 million to develop advanced quantum navigation sensors for military use following successful early-stage field demonstrations.

- June 2025: CSEM and QDI Systems developed the first quantum-dot CMOS sensor that directly converts X-rays into electronic signals, enabling miniaturized, lower-cost imaging for medical and industrial applications.

- March 2025: Fermilab and partner universities began the US$71 million DOE-funded Quandarum project to advance silicon-spin-qubit quantum sensors for dark-matter searches and next-generation fundamental physics experiments.

Companies Covered in Quantum Sensors Market

- Microsemi Corp.

- Muquans SAS

- Robert Bosch GmbH

- Spectrum Technologies Inc.

- Thomas Industrial Network Inc.

- Oscilloquartz S.A. (ADVA Optical Networking)

- Supracon AG

- M Squared Lasers Limited

- GWR Instruments, Inc.

- Cryogenic Limited

- AOSense, Inc.

- Wooptix

- Biospherical Instruments Inc.

- LI-COR, Inc.

- Q-CTRL

- Honeywell International Inc.

- Lockheed Martin Corporation

- Vector Atomic

- Infleqtion

- Delta g

Frequently Asked Questions

The quantum sensors market will grow from US$ 389.5 million in 2026 to US$ 945.1 million by 2033 at a CAGR of 13.5%.

Demand is driven by government R&D investments, defense needs for precise navigation and secure operations, and healthcare adoption of quantum-enhanced imaging.

Atomic clocks lead the market with about 42% share due to their maturity and ultra-high accuracy.

North America leads with around 40% share, supported by strong defense funding, advanced research institutions, and a robust quantum technology ecosystem.

AI-integrated quantum sensing and quantum medical imaging systems offer major growth opportunities worth over US$ 2.5 billion combined.