- Nutraceuticals & Functional Foods

- Psychedelic Mushrooms Market

Psychedelic Mushrooms Market Size, Share, and Growth Forecast, 2026 - 2033

Psychedelic Mushrooms Market by Product Type (Psilocybe, Gymnopilus, Panaeolus), Application (De-addiction, Anxiety Relief, Depression Relief, Recreational), Form (Fresh, Dried, Processed), and Regional Analysis for 2026-2033

Psychedelic Mushrooms Market Share and Trends Analysis

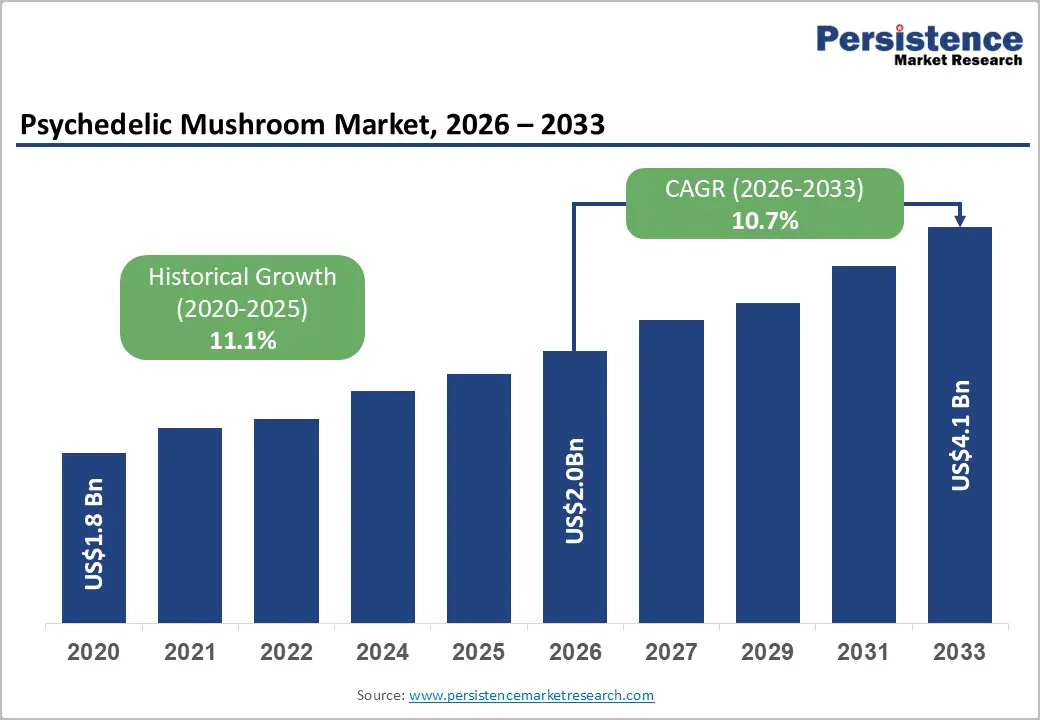

The global psychedelic mushrooms market size is likely to be valued at US$ 1.8 billion in 2026, and is projected to reach US$ 3.0 billion by 2033, growing at a CAGR of 6.0% during the forecast period 2026−2033. This growth trajectory is reflecting increasing recognition of the therapeutic potential of psychedelic compounds, particularly psilocybin, within regulated medical research and treatment settings.

Market momentum is building as healthcare stakeholders are actively reassessing conventional approaches to mental health management, especially for conditions with limited response to standard pharmacological therapies.

Expansion is being driven by progressive regulatory reforms in select jurisdictions, alongside rising clinical trial activity that is demonstrating efficacy in treatment-resistant depression and post-traumatic stress disorder (PTSD). Medical and research institutions are increasingly validating safety protocols, dosing frameworks, and controlled treatment environments, thereby strengthening confidence among clinicians and policymakers.

Acceptance within the medical community continues to improve as peer-reviewed evidence expands and treatment outcomes become more measurable. As a result, psychedelic mushrooms are likely to be increasingly positioned as a complementary neuropsychiatric intervention, rather than a replacement therapy, shaping a cautious but structured pathway toward broader clinical integration.

Key Industry Highlights

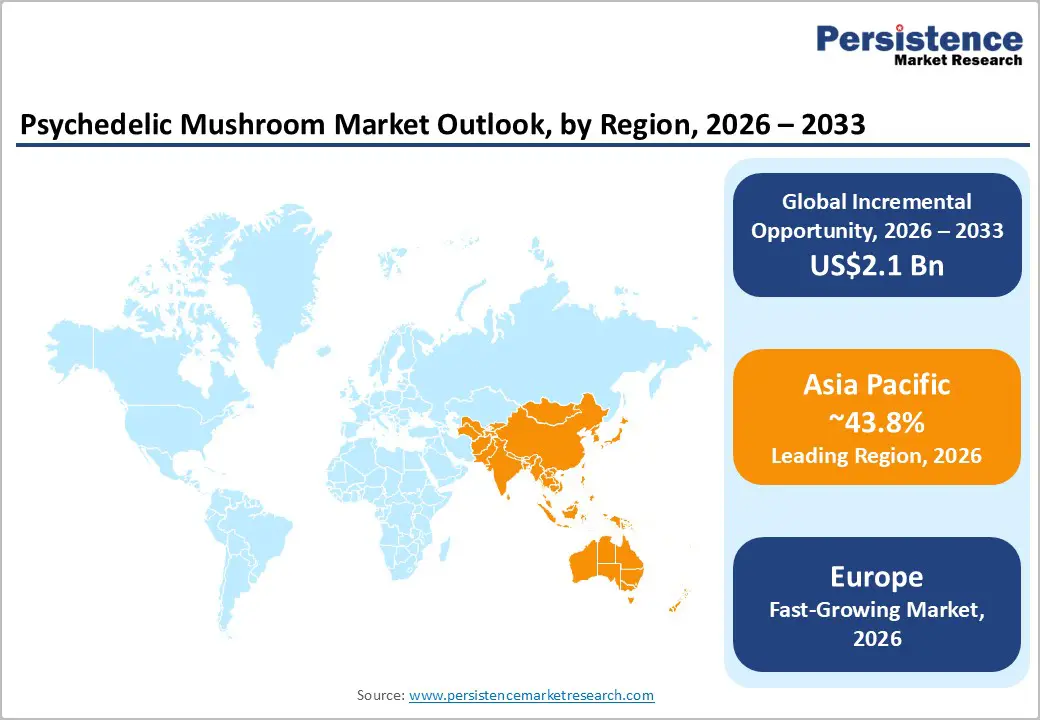

- Dominant Region: North America is expected to account for approximately 55% of the market in 2026, supported by the implementation of some of the most progressive regulatory frameworks worldwide.

- Fastest-growing Market: The Asia-Pacific market is set to be the fastest-growing through 2033, driven by increasing mental health awareness among urban populations.

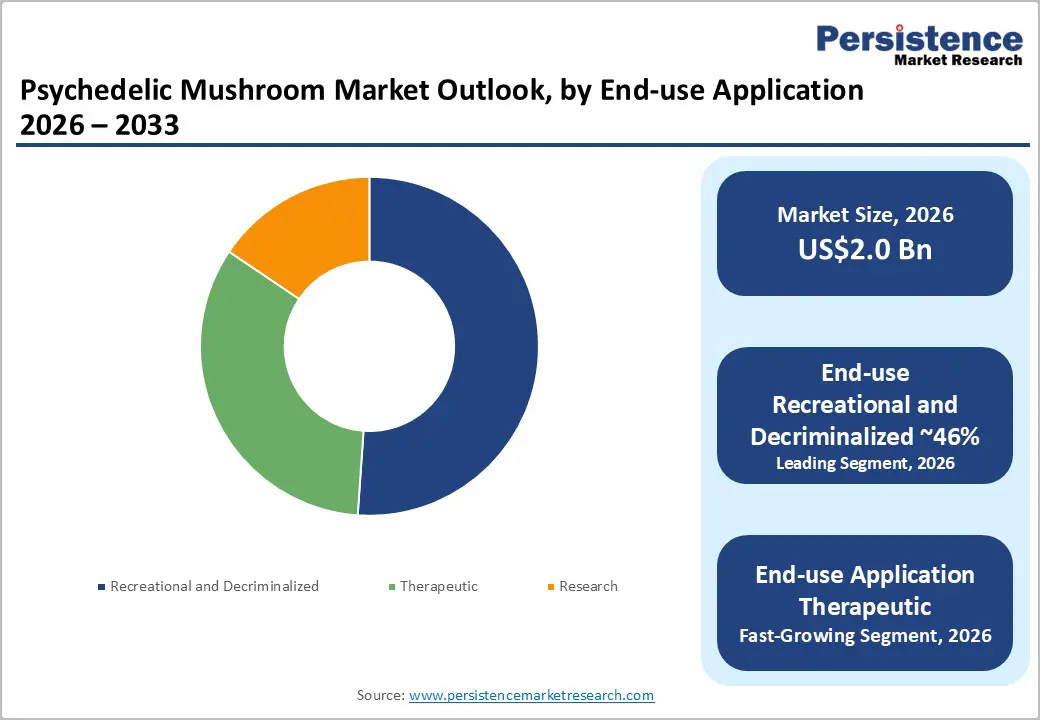

- Leading & Fastest-growing Applications: Depression relief is projected to account for the largest share at about 45% in 2026, while anxiety relief is expected to be the fastest-growing segment over the 2026-2033 forecast period.

- Form Dominance: The fresh segment is expected to account for approximately 44% of revenue in 2026, while the processed segment is projected to be the fastest-growing during the 2026-2033 forecast period.

- December 2025: Czech Republic lawmakers approved psilocybin (magic mushroom) use from 2026 for psychiatrists/psychotherapists treating severe depression, including cancer-related cases, when standard treatments fail.

| Key Insights | Details |

|---|---|

| Psychedelic Mushrooms Market Size (2026E) | US$ 55.2 Bn |

| Market Value Forecast (2033F) | US$ 70.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 2.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Mental Health Crisis and Treatment Gap

The global mental health burden serves as a primary catalyst for the psychedelic mushrooms market growth. Depression affects millions worldwide, and conventional antidepressants fail to help a substantial portion of patients. The COVID-19 pandemic worsened these challenges significantly. Clinical trials in leading medical journals reveal psilocybin's rapid antidepressant effects.

Healthcare providers are increasingly interested in such alternatives due to their potential for treating treatment-resistant cases. Payers increasingly consider novel therapeutic options to address persistent care gaps.

This unmet medical need creates strong demand for innovative solutions. Psilocybin demonstrates sustained benefits in specific patient groups, unlike traditional treatments. Providers seek therapies with faster onset and longer-lasting results. Health systems face pressure to adopt effective modalities amid rising demand. Organizations that prioritize patient outcomes gain a competitive advantage.

Early movers in this space build trust with regulators and clinicians alike. Strategic focus on evidence-based applications ensures sustainable market positioning. Leaders must balance innovation with rigorous safety protocols to capture long-term value.

Regulatory Complexity and Legal Fragmentation

Regulatory heterogeneity poses a major constraint despite reforms in certain regions. Psychedelic mushrooms retain Schedule I status under the United Nations Convention on Psychotropic Substances (UN-CPS). Most countries maintain federal prohibitions on cultivation, manufacturing, and clinical use.

These restrictions create operational hurdles for producers and healthcare providers alike. Legal gaps between national and local rules in places such as the United States and Canada increase compliance demands. Investors face heightened uncertainty as a result.

Standardized quality frameworks remain absent across jurisdictions. Good manufacturing practice (GMP) guidelines and pharmacopoeia standards stay underdeveloped for this category. Large-scale production faces significant barriers in the absence of these protocols. International trade rules further restrict cross-border supply chains.

Companies operate within fragmented geographic zones as a consequence. Economies of scale prove elusive under current conditions. Organizations prioritize compliance infrastructure early. They establish modular operations adaptable to evolving regulations. Such preparation positions firms to capture value when standardization emerges. Patient safety demands rigorous quality controls regardless of market access constraints.

Technology Integration and Novel Delivery Systems

Technological innovation creates significant opportunities for market differentiation and enhanced patient outcomes. Synthetic psilocybin production removes agricultural inconsistencies and achieves pharmaceutical-grade consistency. Clinical applications command premium pricing through such standardization.

Companies develop nanotechnology-based delivery systems to improve bioavailability and enable precise dosing. These advancements address key limitations in traditional administration methods. Forward-thinking firms invest in proprietary formulations to strengthen competitive positioning.

Digital therapeutics platforms integrate virtual reality, biometric monitoring, and artificial intelligence (AI)-guided sessions. Developers solve scalability issues found in conventional psychedelic-assisted therapy. Extended-release preparations and microdosing protocols aim to elicit sub-hallucinogenic effects to expand patient access. These solutions extend beyond intensive clinical environments. The convergence of psychedelic treatments with digital health systems unlocks new market potential.

Organizations that lead in platform integration gain a first-mover advantage. Strategic partnerships with technology providers accelerate commercialization timelines. Leaders balance the pace of innovation with regulatory alignment to maximize long-term value.

Category-wise Analysis

Product Type Insights

Psilocybe is slated to maintain a dominant position in the market with an estimated 2026 share exceeding 67%, driven by its high psilocybin potency, extensive clinical research backing, and widespread consumer familiarity across therapeutic and recreational markets. This variety accounts for the majority of global demand due to its consistent psychoactive effects and well-established cultivation practices that ensure reliable yield and quality control.

Suppliers prioritize Psilocybe for its versatility in both fresh and processed forms, from whole mushrooms for immediate therapeutic use to standardized extracts for pharmaceutical applications. These attributes position Psilocybe as the cornerstone of commercial operations, enabling producers to meet diverse market needs while maintaining compliance with emerging regulatory standards in jurisdictions where psilocybin mushrooms are legalized.

Panaeolus is likely to be the fastest-growing segment during the 2026-2033 forecast period, boosted by rising interest in its diverse psilocybin profiles and niche therapeutic applications that distinguish it from traditional varieties.

Emerging research highlights Panaeolus's unique alkaloid composition, which shows particular promise for anxiety management and de-addiction treatments, attracting innovation-focused producers seeking differentiation. As legalized regions expand market access, cultivators accelerate adoption by diversifying beyond Psilocybe dominance to meet evolving clinical demands.

Application Insights

Depression relief is projected command around 45% of the psychedelic mushrooms market revenue share in 2026, supported by robust clinical evidence demonstrating psilocybin's efficacy in treatment-resistant depression cases where conventional therapies fail. Providers favor this application for its rapid symptom reduction, often within hours rather than weeks, positioning it as the primary therapeutic use amid escalating global mental health crises.

Regulatory approvals, such as Breakthrough Therapy Designations and state-level legalization, further solidify its market position by creating clear reimbursement pathways and clinical integration protocols.

Anxiety relief is expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by expanding clinical trials targeting PTSD and generalized anxiety disorders, where traditional treatments show limited success.

Microdosing protocols significantly broaden accessibility beyond intensive clinical settings, appealing to wellness consumers seeking subtle cognitive and emotional benefits without full psychedelic experiences. Legalization trends amplify demand in outpatient practices and self-care contexts, enabling scalable delivery through integrated mental health platforms.

Form Insights

Fresh psychedelic mushrooms are poised to lead with an approximate 44% market share in 2026, due to consumer preference for its purity, potency preservation, and minimal processing required for both therapeutic and experiential applications.

Buyers value the mushrooms' natural state, which maintains biochemical integrity essential for clinical research, immediate therapeutic administration, and authentic recreational experiences.

This form eliminates extraction risks and delivers the highest bioactive compound concentration without degradation from drying or processing. Regulated markets support premium pricing for fresh/whole products through quality assurance certifications and transparent supply chains.

Processed mushrooms is anticipated to be the fastest-growing segment during the 2026-2033 forecast period. Accelerating market expansion through standardization is essential for pharmaceutical integration and microdosing product development.

Advances in extraction technologies enable the production of scalable, shelf-stable options that meet good manufacturing practice (GMP) standards, addressing critical barriers to institutional adoption. These forms target hospitals, clinics, and global distributors seeking consistent potency, extended shelf life, and regulatory compliance.

Processed products eliminate variability inherent in fresh mushrooms, ensuring precise dosing for clinical trials and outpatient prescriptions.

Regional Insights

North America Psychedelic Mushrooms Market Trends

North America is set to dominate with approximately 55% of the psychedelic mushrooms market share in 2026. The region hosts the most advanced regulatory frameworks worldwide. States such as Oregon operate established psilocybin service centers.

Colorado implements regulated market structures through progressive legislation. Canada maintains accessible pathways via its Special Access Program. The United States drives the majority of regional activity through state-level innovation.

These developments create diverse business models for cultivation, therapy delivery, and research applications. Healthcare providers gain practical experience with supervised administration protocols.

Growth stems from multiple strategic advantages. Regulatory agencies grant Breakthrough Therapy Designations that accelerate clinical pathways. Leading research institutions conduct extensive trials on mental health applications.

Venture capital supports biotechnology innovation and infrastructure development. The competitive landscape blends pharmaceutical giants with specialized psychedelic firms and service providers. Organizations pursue vertical integration across the supply chain. Investment focuses on clinical development, digital platforms, and cultivation technology.

Leaders navigate federal restrictions through state-level compliance strategies. Early market participants establish defensible positions as standardization emerges.

Europe Psychedelic Mushrooms Market Trends

Europe is expected to maintain a strong position in the global market for psychedelic mushrooms from 2026 to 2033. Germany leads regional activity through its advanced pharmaceutical ecosystem and progressive mental health policies. The United Kingdom contributes significantly via research leadership at institutions and established innovation clusters.

France and Spain show growing momentum, with expanding clinical trial activity and policy reform discussions. These countries create diverse market entry points across the region. Healthcare systems integrate psychedelic research into existing mental health frameworks effectively.

This unified approach offers efficiency gains over fragmented national processes. Leading pharmaceutical companies initiate psychedelic research programs.

Regulatory harmonization drives strategic advantages. The European Medicines Agency (EMA) streamlines market access across 27 member states after marketing authorization. Specialized biotechnology firms develop clinical pipelines.

Academic centers conduct investigator-initiated trials. Compassionate use provisions enable early patient access in countries such as Germany, the Netherlands, and Switzerland. Investment targets pharmaceutical-grade manufacturing and clinical research networks.

Universal healthcare integration accelerates therapeutic adoption. Organizations leverage Europe's regulatory expertise to establish scalable commercialization pathways.

Asia Pacific Psychedelic Mushrooms Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for psychedelic mushrooms through 2033. Australia leads development through the Therapeutic Goods Administration's (TGA) authorization of psilocybin therapy for treatment-resistant depression.

Specialized clinics establish operations alongside practitioner training programs and pharmaceutical supply chains. Japan advances through pharmaceutical company research partnerships. India contributes cultural acceptance rooted in traditional practices.

These nations create foundational market infrastructure across diverse regulatory environments. Urban populations recognize rising mental health challenges linked to modernization pressures.

Governments invest in mental health systems to address concerns about workplace productivity. Middle-class consumers gain access to premium therapeutic options. ASEAN countries such as Thailand pursue drug policy reforms while leveraging medical tourism infrastructure.

Manufacturing advantages include expertise in botanical extraction and proximity to pharmaceutical ingredient production centers. Western biotechnology firms form research partnerships with local manufacturers. Investment targets clinical trial networks and specialized treatment facilities.

Organizations tailor clinical evidence to regional populations for optimal adoption. Market leaders prioritize policy advocacy alongside localized commercialization strategies to capture long-term demographic-driven demand.

Competitive Landscape

The global psychedelic mushrooms market is exhibiting a moderately fragmented competitive structure, led by companies such as Compass Pathways, Mind Medicine, Cybin Inc., ATAI Life Sciences, and Numinus Wellness, which collectively are accounting for approximately 25% to 30% of total market share.

This distribution is reflecting an evolving ecosystem where no single participant is achieving dominance, largely due to regulatory complexity, long development timelines, and varied commercialization pathways. As a result, competitive intensity is remaining high, while barriers to entry are favoring well-capitalized players with strong scientific, regulatory, and clinical capabilities.

Competitive strategies are diverging clearly across the value chain as companies are aligning business models with regulatory exposure and target end users. Pharmaceutical-focused players are prioritizing intellectual property protection and clinical trial leadership to secure long-term therapeutic positioning and regulatory exclusivity.

Vertically integrated operators in jurisdictions with legalized access are concentrating on controlling market entry points and building brand equity through cultivation, formulation, and clinical delivery. Technology-driven platforms are differentiating through digital therapeutic tools and scalable treatment models, enabling broader reach beyond physical clinics. Together, these approaches are addressing distinct patient populations, reimbursement pathways, and revenue structures, shaping a diversified and adaptive competitive landscape.

Key Industry Developments

- In December 2025, St. Joseph's Healthcare Hamilton launched the Centre for Innovation and Psychedelics in late 2025 to advance research on psychedelics such as psilocybin (from magic mushrooms), LSD, MDMA, and ketamine for treating treatment-resistant depression, chronic pain, migraines, and anxiety, including ongoing trials for cannabis addiction and pain management.

- In July 2025, Emory researchers found psilocin (from psilocybin in psychedelic mushrooms) extended human skin/lung cell lifespan by over 50% and boosted aged mice survival by 30% with healthier fur and hair regrowth. The study shows psilocybin reduces oxidative stress, improves DNA repair, and preserves telomeres, targeting aging hallmarks even when started late in life.

- In June 2025, New Zealand became the latest country to approve psilocybin, the psychoactive compound in "magic mushrooms", for therapeutic use against treatment-resistant depression, with Dr. Cameron Lacey, a University of Otago psychiatrist and the nation's only authorized prescriber, administering the first doses under strict clinical protocols.

Companies Covered in Psychedelic Mushrooms Market

- Compass Pathways

- MindMed

- Cybin Inc.

- ATAI Life Sciences

- Numinus Wellness

- Field Trip Health

- Small Pharma

- PharmaTher Holdings

- Revive Therapeutics

- Awakn Life Sciences

- Entheon Biomedical

- Mydecine Innovations Group

- Novamind

- Havn Life Sciences

- Algernon Pharmaceuticals

Frequently Asked Questions

The global psychedelic mushrooms market is projected to reach US$ 1.8 billion in 2026.

The market is poised to witness a CAGR of 5.7% from 2026 to 2033.

Expansion of psychedelic-assisted therapies in healthcare, product innovation (microdosing, extracts), and evolving regulations in Asia Pacific amid growing legalization and wellness demand.

Compass Pathways, Mind Medicine, Cybin Inc., ATAI Life Sciences and Numinus Wellness are some of the key players in the market.