- Plastics, Polymers & Resins

- Polysilicon Market

Polysilicon Market Size, Share, Trends, and Growth Forecast, 2025 - 2032

Polysilicon Market By Purity Level (Solar Grade, Electronic Grade), Application (Solar PV, Electronics), and Regional Analysis for 2025 - 2032

Polysilicon Market Share and Trends Analysis

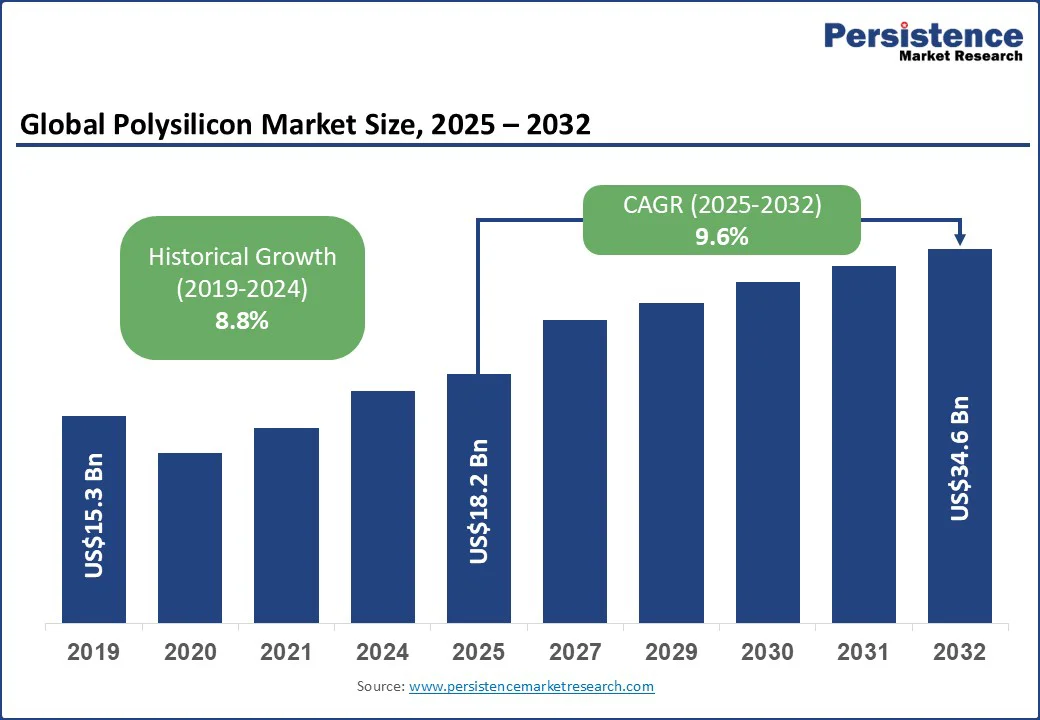

The global polysilicon market size is likely to be valued at US$18.2 Bn in 2025 and is expected to reach US$34.6 Bn by 2032, growing at a CAGR of 9.6% during the forecast period from 2025 to 2032.

Key Industry Highlights

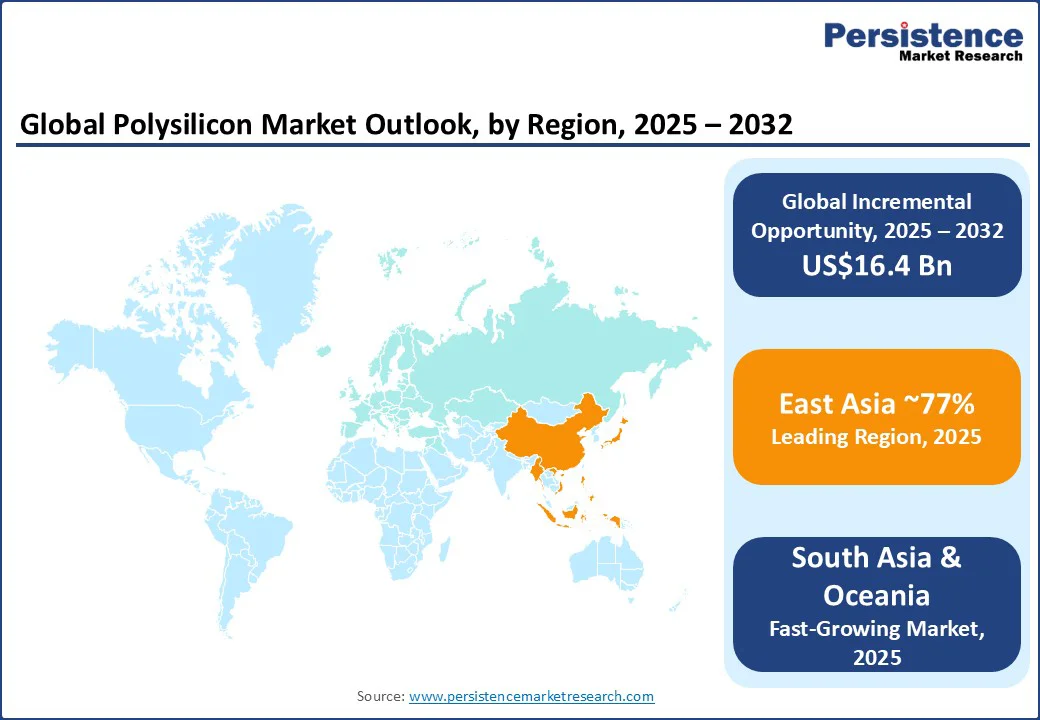

- Leading Region: East Asia is anticipated to dominate with around 77% of the market share in 2025, led by China’s 93% global production capacity and strong policy support.

- Fastest-growing Region: South Asia& Oceania is anticipated to grow at the fastest CAGR, driven by booming solar PV adoption and semiconductor demand, supported by government initiatives such as Production-Linked Incentive (PLI) schemes aimed at boosting domestic manufacturing capabilities.

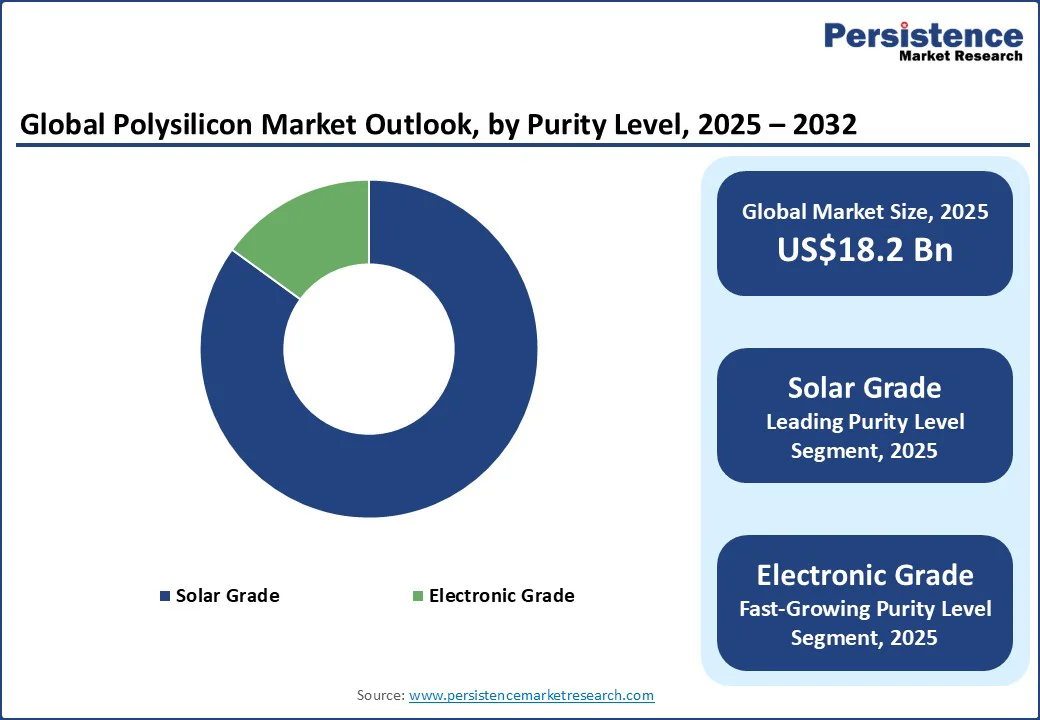

- Dominant Purity Level: The solar grade segment, categorized by purity level, is projected to account for approximately 85% of the market share, driven by surging demand for renewable energy and the rapid expansion of photovoltaic installations across the globe.

- Leading Application Type: The electronics segment is anticipated to hold around 13% of the market share, driven by the demand for high-purity silicon in semiconductors, integrated circuits, and advanced microchips.

- Low-carbon, traceable silicon is emerging as a premium growth avenue, reinforced by U.S. IRA credits and EU import bans on forced-labor-linked materials.

- Advanced reactor technologies and process optimization are redefining production pathways, with FBR delivering up to 30% efficiency gains compared to Siemens reactors.

| Global Market Attribute | Details |

|---|---|

| Market Size (2024A) | US$16.6 Bn |

| Estimated Market Size (2025E) | US$18.2 Bn |

| Projected Market Value (2032F) | US$34.6 Bn |

| Value CAGR (2025 to 2032) | 9.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 8.8% |

Polysilicon remains a critical material for solar photovoltaic (PV) modules and semiconductor wafers, supporting a wide range of industries, including renewable energy, electric vehicles (EVs), artificial intelligence (AI), and high-performance consumer electronics.

Market expansion is supported by countries such as China, the U.S., Germany, South Korea, and India, which are advancing clean energy targets and developing local manufacturing hubs to enhance supply chain resilience.

Market Factors- Growth, Barrier, Opportunity, and Trend Analysis

Solar Cell Efficiency Leap and Localized Supply Chains Fuel Polysilicon Expansion

The global energy transition is accelerating, and solar PV has become the centerpiece of clean power growth. The push toward advanced solar technologies such as Tunnel Oxide Passivated Contact (TOPCon) and Heterojunction Technology (HJT) requires ultra-high-purity feedstock, directly tying the evolution of PV efficiency to the raw material ecosystem.

This connection is driving strong growth in the polysilicon market, as the industry transitions from legacy p-type solar cells to more advanced n-type architectures, which require cleaner and more consistent input materials.

According to the International Energy Agency Photovoltaic Power Systems Programme, more than 1.6 TW of solar capacity was operational at the start of 2024, generating over 2,135 TWh of power, or 8.3% of the global electricity demand.

The IEA also highlights that TOPCon’s share surged from 10% in 2022 to 30% in 2023, and hit 50% in 2024, with n-type capacity expected to reach nearly 69% by the end of 2024. This technological shift demands feedstock with far tighter impurity specifications, linking solar efficiency gains directly to the material supply chain.

The U.S. Department of Energy highlights that the Inflation Reduction Act’s 45X Production Tax Credit and 48C Investment Tax Credit are channeling billions into domestic solar manufacturing, including the integration of upstream materials.

In India, the Ministry of New and Renewable Energy is executing INR 24,000 crore (US$2.89 Bn) Production Linked Incentive (PLI) scheme to build a giga-scale capacity in high-efficiency solar PV modules, reducing import dependence and creating a stronger ecosystem for renewable energy manufacturing. These policy frameworks, combined with technology-driven demand, reinforce a sustained growth path for the market.

Energy-Heavy Production and Cyclical Price Crashes Challenge Industry Stability

High-purity silicon production is the foundation of the solar PV supply chain; however, its exceptionally high energy requirements can hinder industry growth, especially during periods of market downturn. The chemical vapor deposition process consumes massive amounts of electricity, driving production costs higher and exposing producers to sharp cyclic downturns in solar raw material pricing.

When solar PV raw material costs rise above the average selling prices of wafers, downstream manufacturers gain leverage. At the same time, upstream producers are often forced to reduce output, creating supply chain imbalances that ripple through global photovoltaic markets.

The challenge is evident across key producing regions. In China, utilization rates have declined as producers adjust to periods of overcapacity. At the same time, in the U.S., REC Silicon’s closure of its Moses Lake facility underscores how tariff barriers, quality control issues, and high electricity consumption amplify risks when global prices fall. Even established leaders such as Wacker Chemie have reported weaker solar-grade sales, reinforcing the pervasive impact of cyclical pricing and energy-intensive production.

Unless the industry accelerates efficiency improvements, adopts advanced n-type wafer technologies, and enhances the digital optimization of high-purity silicon manufacturing, producers of solar PV raw materials will remain vulnerable to recurring boom-and-bust cycles. This restraint highlights how energy-heavy production and price volatility continue to limit stable, long-term growth in the global solar materials market.

Low-Carbon, Traceable Polysilicon Emerges as the Premium Growth Avenue

The clean energy transition is reshaping procurement priorities, opening a premium growth path for low-carbon and traceable silicon materials. Regulatory frameworks such as the U.S. Uyghur Forced Labor Prevention Act (UFLPA) now demand strict verification of supply chains.

According to the U.S. Department of Homeland Security, numerous shipments have already been stopped at ports due to traceability concerns. This demonstrates that verified, low-carbon, and ethically sourced materials are no longer optional. They are essential for participation in solar and semiconductor supply chains.

Sustainability and energy efficiency have become commercial differentiators. REC Silicon reports that its Fluidized Bed Reactor (FBR) technology significantly reduces energy use compared to conventional Siemens methods, enabling one of the smallest carbon footprints in the market. Powered by hydroelectric energy at its Moses Lake facility, REC has already secured premium pricing for its granular product.

Financial and policy levers are accelerating this momentum. Europe’s import ban on forced-labor-linked products will make verified, traceable materials the standard across PV modules, wafers, and semiconductor-grade inputs.

The International Labour Organization continues to highlight forced labor as a systemic global risk, meaning buyers must invest in transparent sourcing or risk exclusion from major markets. This convergence of clean energy incentives, strict labor compliance, and sustainability mandates positions low-carbon, traceable silicon as the premium growth avenue in both photovoltaic and electronic-grade applications.

Trend - Advanced Reactor Technologies and Carbon-Intensive Process Optimization Redefine Industry Pathways

Traditional Siemens reactors, while reliable, have been energy-intensive and costly, prompting a global shift toward next-generation alternatives such as fluidized bed reactors (FBRs) and upgraded metallurgical-grade (UMG) processes.

These advancements reduce electricity consumption per kilogram of output and bring operational scalability that supports growing solar PV and semiconductor demand. According to the International Energy Agency (IEA), solar PV capacity is projected to expand by more than 280 GW annually through 2030, intensifying the need for cost-efficient and cleaner raw material supply chains.

Producers such as GCL-Poly and OCI have already invested in FBR technology, demonstrating efficiency gains of up to 30% compared to traditional methods. Companies are exploring hybrid production models that integrate UMG with chemical vapor deposition (CVD), cutting down carbon footprints while maintaining quality standards demanded by solar module makers and semiconductor fabs.

This trend signals a decisive pivot in the market, where sustainability and competitiveness now converge. With governments tightening carbon regulations and investors scrutinizing energy intensity, producers that embrace process optimization and deploy advanced reactors are set to lead the next growth wave.

The pathway redefines not only production costs but also the positioning of the industry in the global renewable energy transition, making technological innovation the cornerstone of future market leadership.

Category-wise Analysis

Purity Level Insights

The solar grade segment is anticipated to account for approximately 85% share, fueled by unprecedented demand for renewable energy and the rapid scaling of photovoltaic installations worldwide. The purity requirements for solar-grade silicon are less stringent than electronic-grade, enabling cost optimization and higher production efficiency.

Benefiting from supportive policies, the cost of electricity generated from solar panels has significantly declined over the past decade, making solar one of the most affordable and scalable renewable technologies.

According to the International Energy Agency (IEA), global solar PV generation rose by 320 TWh in 2023 alone, up 25% from 2022, driving the need for a high-volume supply of solar-grade material to meet expanding project pipelines.

Continuous technological progress in reactor designs, supply-chain optimization, and large-scale production is further reinforcing the dominance of solar-grade purity levels in the market. Between 2018 and 2023, global solar capacity tripled, and projections show it could account for nearly 80% of renewable growth by 2030.

Major markets such as China, the European Union, the U.S., and India are accelerating deployment through ambitious policies such as the Inflation Reduction Act (US), REPowerEU Plan (EU), and China’s 14th Five-Year Renewable Energy Plan. These developments ensure that solar grade remains the primary driver of demand for high-purity silicon, securing its overwhelming share while setting the stage for even stronger growth through the next decade.

Application Insights

The electronics segment is projected to account for a 13% share in 2025, driven by the demand for high-purity silicon in semiconductors, integrated circuits, and advanced microchips. It serves as a critical feedstock for consumer, automotive, and AI-driven electronics, supporting devices with higher performance and lower power consumption.

Strong industry momentum is evident, as according to the Semiconductor Industry Association (SIA), global semiconductor sales reached $627.6 billion in 2024, up 19.1% y-o-y, with monthly sales in early 2025 hitting record highs despite short-term fluctuations. Continuous innovation and the need for ultra-pure materials position it as a cornerstone of technological advancement and market scalability, cementing the segment as a long-term growth driver.

Regional Insights

Europe Polysilicon Market Trends

Europe is anticipated to account for an 11% share in 2025 driven by strong renewable energy targets, government-backed clean energy policies, and strategic initiatives to localize supply chains. The region aligns its production with broader energy transition and decarbonization goals, particularly through solar PV expansion under the REPowerEU Plan and the Green Deal Industrial Plan.

Germany serves as an anchor of Europe’s polysilicon market, with Wacker Chemie operating one of the largest solar-grade silicon production facilities. Despite a smaller capacity compared to East Asia, Europe’s high-purity manufacturing remains a critical pillar of clean technology, solar PV deployment, and semiconductor-grade material supply, poised for stable growth as energy markets normalize.

East Asia Polysilicon Market Trends

East Asia has become the undisputed global powerhouse in solar-grade materials, with demand and production capacity reaching unprecedented levels. Policy support, industrial scale, and cost advantages have turned East Asia into the largest hub for solar energy and advanced electronics supply chains. China leads this growth, reinforcing East Asia’s role as both the largest producer and a key demand center for the global renewable energy transition.

Competitive Landscape

The global polysilicon market is largely oligopolistic, dominated by a few major manufacturers controlling significant production capacity. Leading players such as Tongwei Co., Ltd., GCL Technology Holdings Ltd., Daqo New Energy Corp., Xinte Energy Co., Ltd., and Wacker Chemie AG drive the market through high-purity polysilicon production, serving both solar-grade and semiconductor-grade applications.

Manufacturing remains capital-intensive, with facilities taking up to five years to become fully operational, emphasizing the significance of established producers such as Wacker Chemie, Hemlock Semiconductor, OCI, and GCL Technology. These companies leverage large-scale manufacturing, advanced production technologies, and strategic positioning to maintain leadership while ensuring consistent supply to global photovoltaic and electronics supply chains.

Trade policies, tariffs, and regional incentives also influence market dynamics. Initiatives such as the U.S. Inflation Reduction Act (IRA), Europe’s REPowerEU, and India’s Production-Linked Incentive (PLI) scheme are reshaping competitive advantages. Despite pricing pressures, ongoing strategic investments, technological innovation, and focus on high-purity production continue to drive growth in renewable energy, semiconductor, and advanced electronics markets.

Industry Developments:

- In February 2025, Tongwei Co., Ltd. launched a granular polysilicon production project through its subsidiary, Yongxiang New Energy Co., as part of the “Yongxiang New Energy Phase II Technological Transformation Project.” The project includes a 10,000 MT/year pilot line, utilizing silane-based fluidized bed technology to diversify the company’s product range and enhance competitiveness in the solar PV market.

- In April 2025, Tongwei announced plans to introduce strategic investors into its wholly owned polysilicon unit, Sichuan Yongxiang Co., via a CNY 10 Bn (US$1.37 Bn) investment, supporting debt repayment and working capital while retaining majority ownership.

Companies Covered in Polysilicon Market

- Tongwei Co., Ltd.

- GCL Technology Holdings Ltd.

- Daqo New Energy Corp.

- Xinte Energy Co., Ltd.

- Wacker Chemie AG

- Asia Silicon (Qinghai) Co., Ltd.

- Xinjiang East Hope New Energy Co., Ltd.

- OCI Company Ltd./OCI Holdings Co., Ltd.

- Hemlock Semiconductor Operations LLC

- Shaanxi Non-Ferrous Tianhong REC Silicon Mat. Co., Ltd.

Frequently Asked Questions

The polysilicon market is projected to be valued at US$18.2 Bn in 2025.

Solar grade is expected to hold an 85% market share in 2025, driven by global PV expansion, supportive policies, and cost-efficient production technologies.

The polysilicon market is poised to witness a CAGR of 9.6% from 2025 to 2032.

Growth in the polysilicon market is driven by the global energy transition, rising adoption of advanced n-type solar technologies such as TOPCon and HJT, and supportive policies accelerating high-purity solar PV manufacturing.

The key opportunity in the polysilicon market lies in low-carbon, traceable, and ethically sourced silicon, meeting the rising demand for sustainable, compliant, and high-purity materials in photovoltaic and electronics applications.

Key players in the polysilicon market include Tongwei Co., Ltd., GCL Technology Holdings Ltd., Daqo New Energy Corp., Xinte Energy Co., Ltd., and Wacker Chemie AG.