- Healthcare IT

- Picture Archiving and Communication System Market

Picture Archiving and Communication System Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Picture Archiving and Communication System Market by Component (Workstations and Archives, Imaging Modalities, Secured Network), Deployment Mode (Web-Based, Cloud-Based, On-premise), Application (Cardiology, Oncology, Orthopedics, Dental, Others), End-user (Hospitals, Imaging Centers, Diagnostic Centers, Dental Practices, Others), and Regional Analysis from 2025 to 2032

Picture Archiving and Communication System Market Share and Trends Analysis

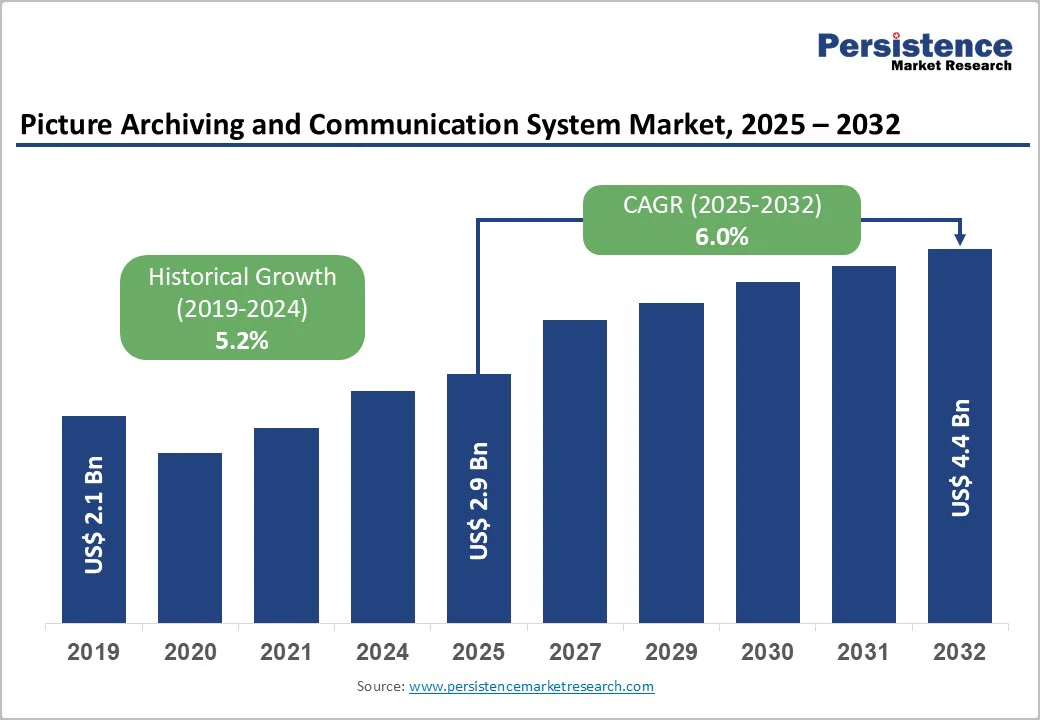

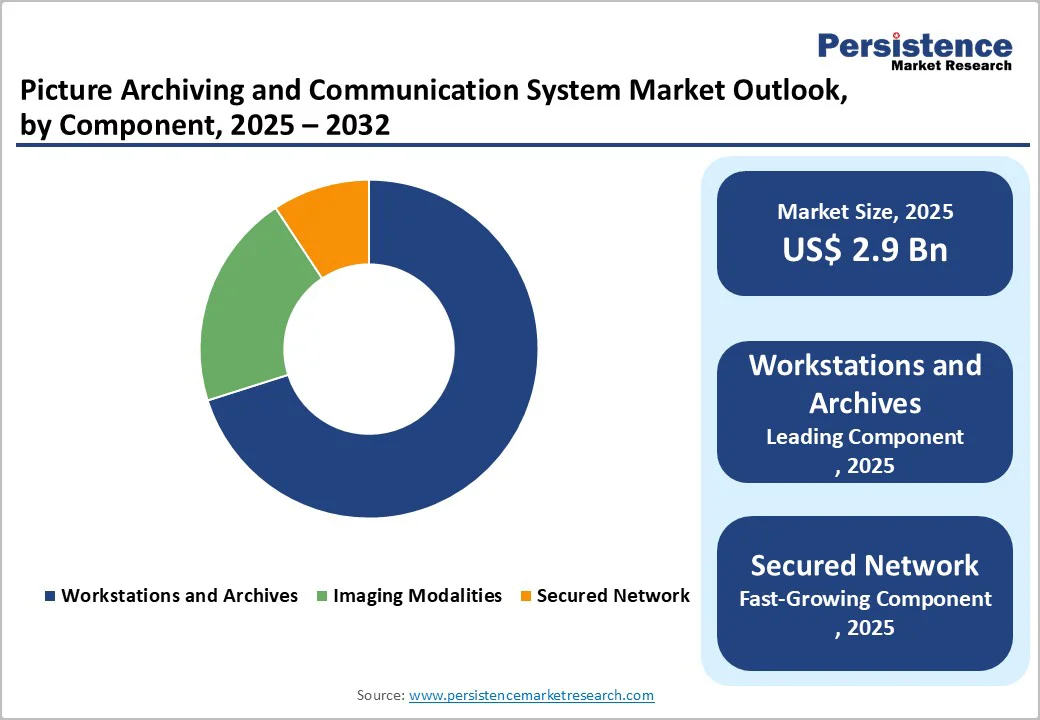

The global picture archiving and communication system market size is valued at US$2.9 billion in 2025 and is projected to reach US$4.4 billion by 2032, growing at a CAGR of 6.0% from 2025 to 2032.

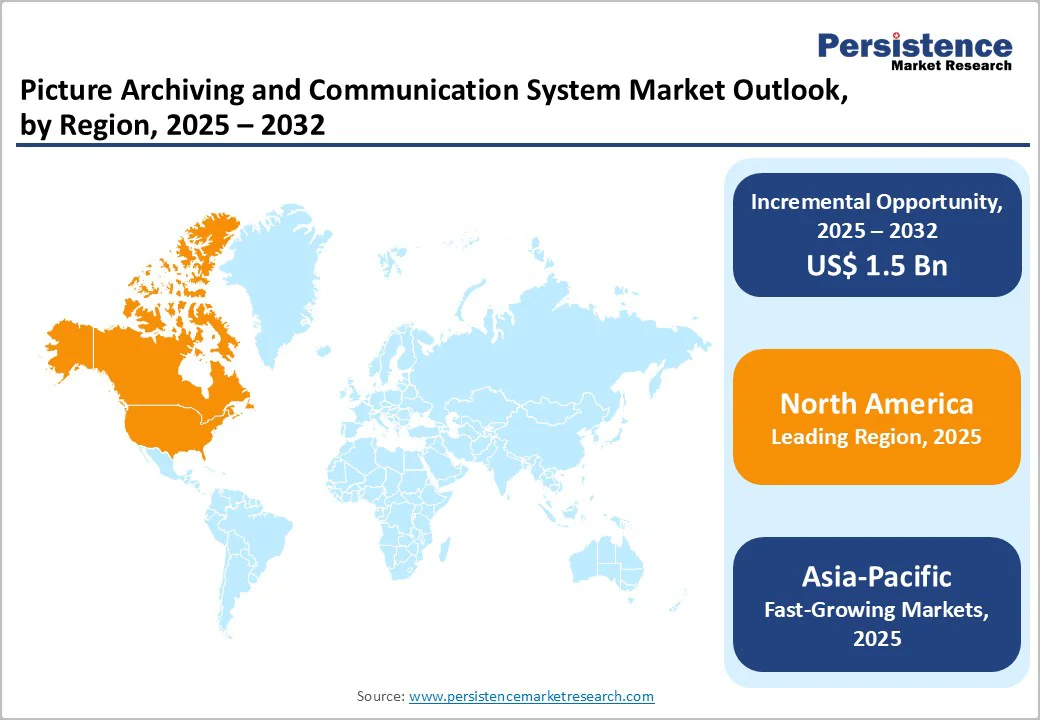

The global market is growing steadily, fueled by demand for precise imaging, improved workflow, and enhanced patient safety. North America leads with advanced infrastructure and strong regulations. At the same time, Asia Pacific shows the fastest growth, driven by rising hospital expansion, increasing surgical volumes, and the adoption of advanced imaging and PACS technologies.

Key Industry Highlights:

- Dominant Segment: Workstations & Archives dominate with 70.1% market share, driven by growing imaging data volumes, the need for centralized storage, secure access, and advanced diagnostic workflows. The increasing adoption of enterprise imaging, cloud-based archives, and AI-assisted image analysis further strengthens the segment's global leadership.

- Dominant Region: North America leads with 38.9% share, supported by advanced healthcare infrastructure, high PACS adoption, and strong regulatory frameworks. Asia Pacific holds 22.3% and grows fastest, driven by hospital expansion, rising imaging procedures, and increasing cloud-based and web-based PACS deployment.

- Growth Indicator: Growth is propelled by rising demand for digital imaging, the need for efficient storage and retrieval, integration with EMR/EHR systems, the adoption of cloud and AI solutions, and regulatory support for secure medical data management.

- Market Opportunity: Opportunities include cloud-based PACS, AI-driven diagnostics, vendor-neutral archives, web-enabled access for tele-radiology, cost-efficient solutions for emerging markets, and partnerships with academic hospitals and imaging centers. Increasing demand for interoperability and scalable storage enhances long-term growth potential.

| Key Insights | Details |

|---|---|

| Picture Archiving and Communication System Market Size (2025E) | US$2.9 Bn |

| Market Value Forecast (2032F) | US$4.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.2% |

Market Dynamics

Driver - Rise in Digital Imaging Demand

Rising demand for digital imaging is a major driver for the picture archiving and communication system (PACS) market. Globally, over 1.2 billion imaging procedures were carried out in 2020, reflecting the rapid growth of diagnostic imaging. In Taiwan, the use of CT scans increased more than threefold from 2000 to 2017, while MRI usage surged almost fourfold, demonstrating the growing reliance on advanced imaging modalities.

In the United States, over 80 million CT scans are performed annually, highlighting the heavy use of ionizing imaging techniques. This surge in imaging procedures generates massive volumes of high-resolution digital data, necessitating efficient storage, retrieval, and management solutions.

Hospitals, diagnostic centers, and imaging facilities increasingly rely on PACS to ensure seamless integration with electronic medical records, quick clinician access, and secure long-term archiving. As digital imaging continues to expand, PACS adoption is expected to rise correspondingly, supporting improved workflow, diagnostic accuracy, and patient care efficiency.

Restraints - Maintenance & Operational Costs

Maintenance and operational costs are a significant restraint for the picture archiving and communication system market. Hospitals and diagnostic centers incur substantial recurring expenses for software updates, hardware support, license renewals, and secure data storage. In some cases, annual PACS maintenance can reach approximately US $229,000, accounting for 10-15% of the system’s initial capital cost.

Additionally, healthcare facilities often allocate 10-18% of the purchase price annually to service contracts to ensure system reliability and uptime. Infrastructure requirements for disaster recovery, secure networking, and long-term archival storage of high-resolution imaging data further compound these costs.

For smaller hospitals and clinics, such recurring expenditures can strain budgets and limit new PACS deployments. Even for larger institutions, high operational costs may reduce the overall return on investment. Consequently, maintenance and operational expenses remain a key barrier to widespread adoption of PACS systems, particularly in resource-constrained settings.

Opportunity - Adoption of Vendor-Neutral Archives (VNA)

Adoption of vendor-neutral archives (VNA) offers a powerful opportunity in the PACS market by enabling true interoperability across disparate imaging systems. As imaging volumes soar, hospitals struggle with multiple proprietary PACS silos; VNAs solve this by centralizing storage in a standard DICOM-compliant format, allowing unified access.

According to GE Healthcare, this creates “one central place to store images and one interface to access them.” The need is critical: as imaging data floods healthcare systems, legacy PACS installations are strained by fragmented archives.

VNAs also improve operational efficiency and reduce long-term costs by eliminating vendor lock-in and simplifying data access. This flexibility supports cloud or hybrid deployments and future AI-driven analytics, making VNA adoption a scalable, future-proof strategy for enterprise imaging.

Category-wise Analysis

By Component Insights

Workstations and archives account for 70.1% of the global market in 2025, driven by the rapid growth of medical imaging data and the need for efficient storage and access. Large hospitals process tens of petabytes of imaging data annually, with a single CT scan generating 1-5 GB and advanced MRI or 3D imaging producing even larger files.

Digital medical images now constitute approximately 70% of all clinical data, creating high demand for secure, long-term archives. Workstations enable clinicians to quickly access and analyze high-resolution images, supporting timely diagnosis and treatment decisions.

The combination of large data volumes, strict retention requirements, and the need for fast, reliable access makes the Workstations & archives component the backbone of PACS systems, driving its dominant market share.

By Deployment Type Insights

Cloud-based PACS dominates the market due to the growing shift of healthcare organizations toward scalable, internet-hosted storage solutions. Approximately 70% of hospitals and imaging centers now utilize cloud computing for data storage and IT workloads, enabling them to manage massive imaging volumes without investing heavily in local hardware.

Cloud deployment reduces infrastructure costs, supports disaster recovery, and allows secure multi-site access and remote collaboration. With imaging data growing exponentially, including high-resolution CT, MRI, and 3D scans, cloud PACS offers the flexibility to store and retrieve images efficiently.

It also facilitates integration with AI tools and advanced analytics, improving workflow and diagnostic accuracy. These advantages make cloud-based deployment the preferred choice over on-premise and web-based PACS systems.

Regional Insights

North America Picture Archiving and Communication System Market Trends

North America dominates the picture archiving and communication system market with a 38.9% share in 2025, due to high imaging volumes and advanced digital health infrastructure. In the U.S., approximately 93 million CT scans are performed annually, among the highest globally, driving demand for efficient storage and retrieval systems.

Most hospitals have achieved advanced IT maturity, integrating PACS with electronic medical records and enterprise health systems, ensuring seamless workflow and interoperability. The region also benefits from strong regulatory support, reimbursement frameworks, and significant investment in healthcare IT.

Additionally, initiatives supporting medical imaging data sharing and analytics enhance the adoption of enterprise-grade PACS solutions. These factors collectively make North America the largest PACS market, with hospitals and diagnostic centers prioritizing robust, secure, and scalable imaging management systems to handle growing data volumes.

Europe Picture Archiving and Communication System Market Trends

Europe is an important region in the PACS market due to its advanced imaging infrastructure and strong digital-health initiatives. The area has approximately 25 CT scanners and 16 MRI units per million inhabitants, reflecting high imaging capacity and clinical demand. Large-scale programs, such as cancer imaging initiatives covering over 100,000 cases across multiple tumor types, drive the need for centralized, interoperable imaging archives.

Widespread adoption of teleradiology enables remote diagnostics, secure image sharing, and cross-border collaboration among healthcare providers. Additionally, government support for digital health, regulatory frameworks, and investment in hospital IT systems further encourage PACS adoption.

These factors collectively make Europe a mature and strategically significant market, with high demand for efficient, scalable, and integrated imaging management solutions.

Asia Pacific Picture Archiving and Communication System Market Trends

Asia Pacific is the fastest-growing region in the PACS market because of its rapidly expanding healthcare infrastructure, surging imaging volumes, and strong public-sector digitization. Hospital capacity remains low, just 2.6 beds per 1,000 population in many Asian countries, prompting rapid investment in hospital construction.

At the same time, China and India are scaling up advanced imaging: China is expanding adoption of CT and MRI across secondary and tertiary hospitals, while India’s public-private hospital chains are aggressively adding beds. Cloud-based PACS adoption is particularly strong, supported by growing health-IT budgets, government digitization programs, and AI-enabled imaging systems.

This combination of rising demand, technology leapfrogging, and infrastructure expansion fuels rapid PACS uptake across the Asia Pacific.

Competitive Landscape

Leading PACS providers focus on high-performance workstations, secure archives, and seamless interoperability. They invest in scalable storage, cloud-based solutions, and AI-enabled analytics for efficient image management.

Strategic partnerships with hospitals and IT vendors enhance deployment and support, while R&D emphasizes workflow efficiency, data security, and diagnostic accuracy, driving adoption, improving patient care, and meeting growing global imaging demands.

Key Industry Developments:

- In May 2025, GE HealthCare announced new PACS integrations designed to enhance imaging workflows and improve interoperability across healthcare systems. The update enabled seamless connection between PACS and electronic medical records, advanced analytics, and AI-assisted diagnostic tools.

- In December 2024, Siemens Healthineers and RadNet’s wholly owned subsidiary, DeepHealth, announced a collaboration to enhance ultrasound workflows using AI-powered SmartTechnology™. The partnership aimed to integrate advanced artificial intelligence into RadNet’s ultrasound imaging processes to improve diagnostic accuracy, efficiency, and consistency.

- In November 2024, GE HealthCare and RadNet forged a collaboration to transform imaging systems and accelerate AI adoption through SmartTechnology™. The partnership aimed to integrate advanced artificial intelligence into RadNet’s imaging network to enhance diagnostic accuracy, workflow efficiency, and patient care.

Companies Covered in Picture Archiving and Communication System Market

- GE Healthcare

- Siemens Healthineers

- Agfa-Gevaert Group

- Carestream Health

- Koninklijke Philips N.V.-(Philips Healthcare)

- FUJIFILM Medical Systems

- INFINITT Healthcare Co. Ltd.

- Merge Healthcare Solutions Inc. (an IBM company)

- Mckesson Corp

- Sectra AB

- Others

Frequently Asked Questions

The global picture archiving and communication system market is projected to be valued at US$ 2.9 Bn in 2025.

Rising digital imaging demand, AI integration, cloud adoption, EMR/EHR interoperability, and regulatory support drive the global PACS market.

The global picture archiving and communication system market is poised to witness a CAGR of 6.0% between 2025 and 2032.

Opportunities include AI-driven diagnostics, cloud-based PACS, vendor-neutral archives, tele-radiology, advanced visualization, and cost-effective solutions for emerging markets.

GE Healthcare, Siemens Healthineers, Agfa-Gevaert Group, Carestream Health, Koninklijke Philips N.V.- (Philips Healthcare), FUJIFILM Medical Systems.