- Biotechnology

- Perfusion Bioreactors Market

Perfusion Bioreactors Market Size, Share, and Growth Forecast, 2025 - 2032

Perfusion Bioreactors Market By Product Type (Stirred-Tank, Hollow Fiber, Others), Application (Monoclonal Antibodies (mAb), Others), End-user (Biopharmaceutical Companies, Biotechnology Firms, Contract Manufacturing Organizations (CMOs), Others), and Regional Analysis for 2025 - 2032

Perfusion Bioreactors Market Share and Trends Analysis

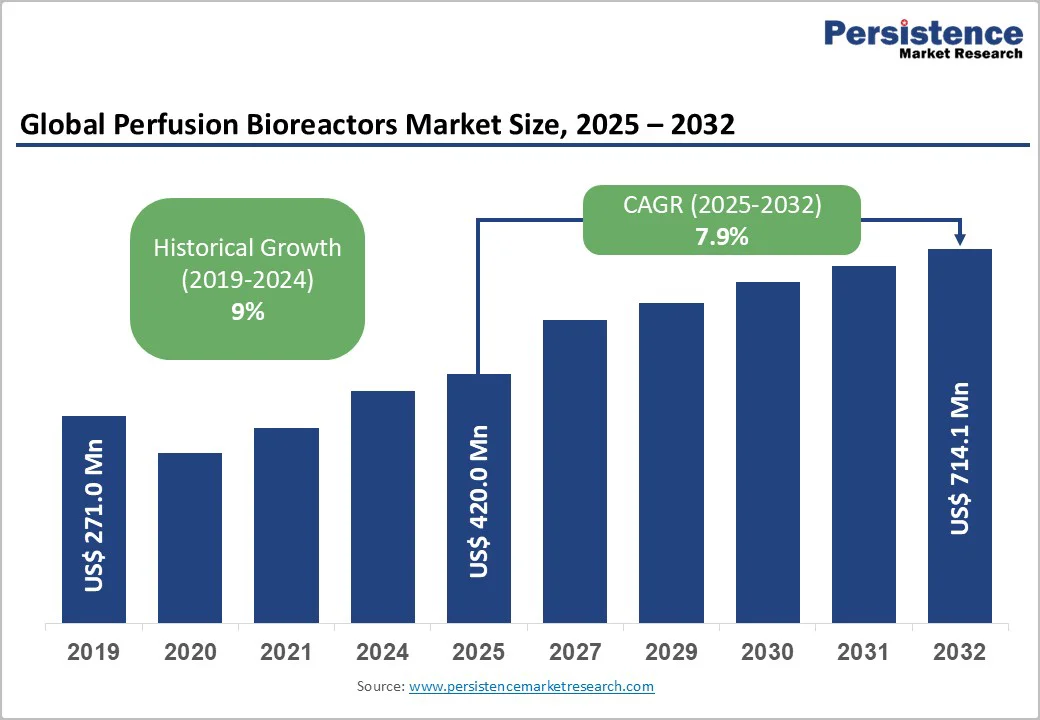

The global perfusion bioreactors market size is likely to be valued at US$420.0 Million in 2025, and is estimated to reach US$714.1 Million by 2032, growing at a CAGR of 7.9% during the forecast period 2025−2032, driven by increasing applications across monoclonal antibody production, cell therapy, and vaccine manufacturing.

Key growth drivers include the adoption of continuous manufacturing, technological advances, and the rising demand for high-density cell cultures. Innovations in single-use systems and AI-driven bioprocess control boost efficiency, while biopharma companies, CMOs, and research institutions increasingly deploy perfusion bioreactors to support next-generation therapies.

Key Industry Highlights

- Dominant Product Types: Stirred-tank bioreactors dominate with 40% market share in 2025, while single-use systems are set to be the fastest-growing through 2032, due to their flexibility and contamination control capabilities.

- Dominant Applications: Monoclonal antibody (mAb) manufacturing comprises nearly 54% of demand in 2025, whereas cell therapy retains the fastest growth from 2025 to 2032.

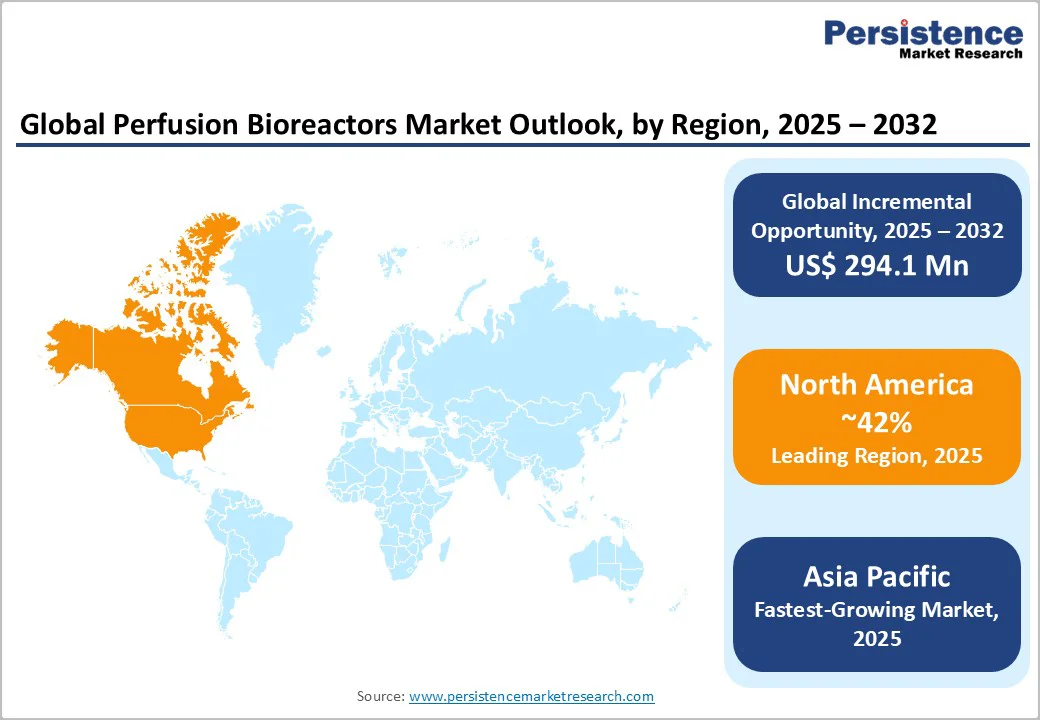

- Leading Regional Markets: North America holds the largest market share at 42% in 2025, backed by regulatory and innovation advantages, with Asia Pacific experiencing the fastest regional expansion.

- Major Trend: Supply chain resilience improvements and environmental sustainability pressures are proving critical in shaping future market dynamics.

- Competitive Environment: The competitive landscape is rapidly evolving with industry consolidations, product innovations, strategic alliances, and targeted capacity expansions by top players.

- February 2025: Sunflower Therapeutics announced the commercial launch of its Daisy Petal perfusion bioreactor system in Asia, aiming to enhance cell therapy manufacturing capabilities in the region.

| Key Insights | Details |

|---|---|

|

Perfusion Bioreactors Market Size (2025E) |

US$420.0 Mn |

|

Market Value Forecast (2032F) |

US$714.1 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

7.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9% |

Market Factors: Growth, Barriers, and Opportunity Analysis

Growing Adoption of Continuous Manufacturing to Aid Market Expansion

Continuous manufacturing is fundamentally reshaping bioprocessing by enabling an uninterrupted, intensified production workflow that delivers more consistent product quality, higher productivity, and reduced operational costs. Unlike traditional batch processes, continuous bioprocessing maintains a steady state, minimizing downtime and product degradation, which enhances product purity and reduces risks associated with batch variability. The approach also significantly reduces facility footprint requirements and resource consumption through smaller equipment and streamlined workflows. Its modular and scalable designs allow manufacturers to quickly adapt to changing demand, improving agility and supply chain resilience.

Regulatory agencies such as the U.S. Food and Drug Administration (FDA) and European Medicines Agency (EMA) are increasingly recognizing these benefits and are providing guidance supportive of continuous approaches, encouraging industry adoption. However, despite its clear advantages, the transition from established fed-batch platforms remains cautious due to required process development efforts, technology transfer complexities, and the need for sophisticated real-time monitoring and control systems. Yet, continuous manufacturing is widely viewed as a necessary evolution to meet rising global biopharmaceutical demand with improved efficiency, quality consistency, and cost-effectiveness.

Capital Intensity and Operational Complications of Bioreactors to Subdue Market Prospects

High capital requirements and operational complexities remain key challenges limiting the widespread adoption of perfusion bioreactors, especially among mid-sized biopharma companies and academic institutions. The comprehensive system setup, including essential ancillary equipment, utilities, and meeting regulatory compliance, demands substantial upfront investment and extends validation timelines, which together create significant financial and operational barriers. Adding to this is the limited availability of professionals with specialized expertise in perfusion processes, which further slows deployment and increases technical risk during scaling and process transfer, further discouraging smaller organizations.

Environmental concerns are also impacting market growth, as single-use perfusion systems generate considerable plastic waste, prompting regulatory scrutiny and driving interest toward hybrid or reusable systems with improved sustainability profiles. Supply chain dependencies on a small number of key suppliers and fluctuations in raw material costs contribute to pricing pressures and supply uncertainties. These combined factors restrict market expansion and emphasize the urgent need within the industry for more affordable, modular, and sustainable perfusion solutions, alongside focused efforts to develop skilled workforce capabilities and strengthen supply chain resilience.

Integration of Industry 4.0 & AI Enables High-Margin Software Ecosystems

The integration of artificial intelligence (AI), machine learning (ML), and real-time analytics with perfusion bioreactor technology is driving unprecedented changes in the market. AI-enabled systems enhance autonomous process control by optimizing parameters such as nutrient feeding, waste removal, pH, and oxygen levels, which improves productivity, product quality, and process consistency. This technological advancement lowers operational complexity and allows manufacturers to achieve higher yields with greater robustness.

Regulatory approvals in key regions have facilitated adoption by reducing compliance barriers and empowering early adopters with competitive advantages. Concurrently, emerging economies of Asia Pacific, notably China and India, are becoming important growth engines for perfusion bioreactors, stimulated by supportive government policies, investments in biotechnology infrastructure, and expanding cell therapy and vaccine production capabilities. Southeast Asian countries, including Thailand, Vietnam, and Singapore, are also establishing local manufacturing hubs, diversifying the global supply chain, and diminishing reliance on Western manufacturers. This geographic diversification is opening new opportunities for both manufacturers and service providers seeking to capitalize on expanding regional demand and localized production strategies.

Category-wise Analysis

Product Type Insights

Stirred-tank perfusion bioreactors remain the dominant product type in 2025, accounting for roughly 40% of the market. Their leadership is anchored in operational scalability, robust regulatory acceptance, and widespread industry familiarity. The technology supports volumetric scalability from laboratory (1–10 liters) to commercial scales (up to 2,000 liters), allowing consistency in hydrodynamic and oxygen transfer environments. This segment primarily services large-scale monoclonal antibody, recombinant protein, and vaccine manufacturing sectors. Amidst growing environmental and cost pressures, hybrid configurations integrating modular single-use perfusion cassettes are gaining traction within this segment. The future growth of this segment is likely to be driven by expansions in manufacturing hubs in developing economies and incremental technology enhancements such as Industry 4.0-enabled sensor integration.

The single-use perfusion segment is the fastest-growing through 2032, powered by its flexibility, contamination control, and lower capital requirements. The adoption of these bioreactors is especially pronounced among mid-sized biopharmaceutical companies, emerging biotech ventures, and specialized cell therapy manufacturers prioritizing speed and compliance over scale. On the other hand, hollow fiber perfusion bioreactors are gaining strong traction in three-dimensional cell culture and tissue engineering applications, with growth catalyzed by regenerative medicine advances. Their closed, high-surface-area membrane designs allow for efficient nutrient and oxygen exchange, supporting cell densities exceeding those achievable in stirred-tank systems.

Application Insights

Monoclonal antibody (mAb) production dominates, accounting for roughly 54% of the market share in 2025. The mAb market, being one of the largest and fastest-growing biologics sectors, dictates bioprocessing infrastructure requirements. Perfusion systems improve volumetric productivity and higher cell densities, enabling manufacturers to scale efficiently while maintaining quality. This segment also benefits from established regulatory pathways and high commercial therapeutic volumes. Monoclonal antibodies represent a key revenue driver for CMOs, which offer perfusion capacity to emerging biopharma companies.

Cell and gene therapy represent the fastest-growing application, powered by the urgent need for high-density, consistent cell expansion in autologous and allogeneic therapies. Perfusion culture delivers a higher viable cell count and improved cell uniformity compared to fed-batch, critical for therapeutic efficacy. A growing number of gene therapy trials and companies have incorporated perfusion systems for clinical and commercial manufacturing, particularly in CAR-T, TCR, NK-cell, and stem cell therapies. Regulatory approvals have accelerated manufacturing scale-up. The segment also benefits from growing academic and hospital cell therapy production centers adopting perfusion technologies.

End-user Insights

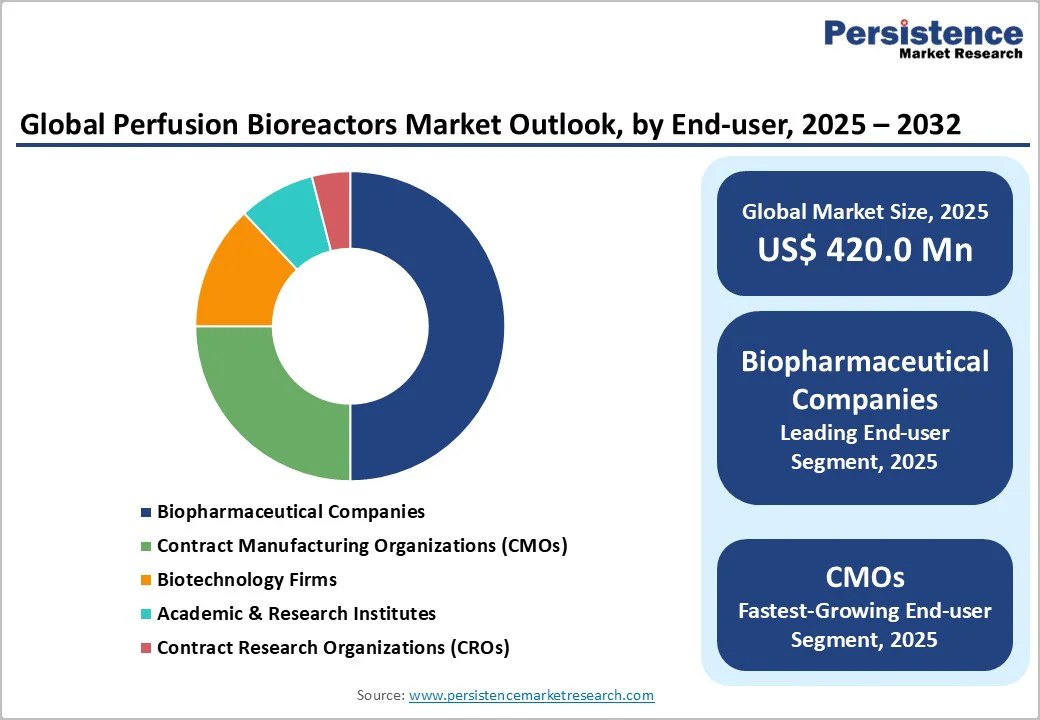

Biopharmaceutical companies lead the market in the deployment of perfusion bioreactors, primarily for commercial therapeutic manufacturing. These companies leverage economies of scale, have established regulatory pathways, and possess capital resources for infrastructure investments. Large pharmaceutical firms such as Roche, Eli Lilly, and Novo Nordisk dominate, with more than half of commercial-scale perfusion bioreactors operated by companies with annual biopharma revenues exceeding US$2 billion. Their manufacturing emphasis is on monoclonal antibodies and recombinant proteins, with nascent but growing interest in cell therapies. Biopharma companies are likely to experience moderate growth from 2025 to 2032, reflective of the maturity in their preferred modalities and regions.

CMOs and cell therapy manufacturing specialists are the fastest-growing end-users for perfusion bioreactors. CMOs provide flexible manufacturing capacity for smaller biotechs lacking in-house facilities. Major providers such as WuXi Biologics, Lonza AG, Samsung Bioepis, and Rentschler Biopharma heavily invest in perfusion infrastructure to service growing client demand. CMOs are expanding geographically into Asia Pacific and emerging regions, reinforcing their role in global perfusion capacity expansion. Cell therapy specialists, including emerging companies and academic spin-offs, require perfusion systems optimized for personalized therapies. This segment also stands to gain from favorable regulations and funding support.

Regional Insights

North America Perfusion Bioreactors Market Trends

North America holds the leading position with approximately 42% of the market share in 2025. The U.S. dominates the region market, accounting for nearly 90% of demand and benefiting from a mature pharmaceutical industry, concentrated biotech ecosystems such as those in San Francisco and Boston, and regulatory leadership. The FDA’s proactive stance on continuous manufacturing, AI-enabled process control, and single-use system guidance fosters a highly innovative environment. Venture capital investments exceeding billions over the last few years have supported infrastructure and technology adoption. CMOs in the U.S. have also been expanding perfusion capacity aggressively. Growth is strongest in cell and gene therapy manufacturing, while traditional monoclonal antibody manufacturing is expected to expand steadily through 2032. Emerging hubs in Texas and North Carolina diversify the geographic footprint, with new installations favoring modular and single-use technologies.

Europe Perfusion Bioreactors Market Trends

The Europe perfusion bioreactors market benefits from clusters in Germany with 38% share, the U.K. with 22%, and France with 15%. Established pharmaceutical manufacturers, specialized bioreactor suppliers, and a coordinated regulatory environment underpin regional market growth. The EMA’s harmonized framework supports continuous manufacturing adoption and AI-enabled processes, complemented by the European Union (EU) Horizon Europe funding. Sustainability directives have encouraged the adoption of hybrid and reusable systems, differentiating Europe’s consumption patterns. Robust progress is evident in cell and gene therapies and vaccine manufacturing, with emerging Eastern European clusters offering additional potential. Regulatory emphasis on environmental metrics has moderated the penetration of single-use perfusion bioreactors in Europe compared to North America.

Asia Pacific Perfusion Bioreactors Market Trends

Asia Pacific is poised to be the fastest-growing regional market for perfusion bioreactors, powered by China and India, with Japan and South Korea presenting mature but steady growth. China’s 14th Five-Year Plan allocates over US$3 Billion to biopharma development. Increasing domestic innovation, regulatory facilitation by the National Medical Products Administration (NMPA), and a growing pipeline of cell and gene therapies drive expansion.

India benefits from the Production-Linked Incentive scheme, supporting US$1 Billion worth of investments in developing manufacturing infrastructure. Southeast Asian countries are also developing manufacturing hubs with regulatory incentives and CMO investments. This regional growth is characterized by rapid infrastructure buildout, increasing adoption of modular and single-use systems, and dynamic pipeline diversification.

Competitive Landscape

The global perfusion bioreactors market is shaped by established life-science leaders and innovative niche entrants, serving next-generation biologics, cell, and gene therapy manufacturing. The market is moderately consolidated, with key players such as Merck, Sartorius, Pall, and Cytiva leveraging acquisitions, product innovation, and global expansion in single-use, modular, and digitally integrated systems.

Strategic collaborations enhance end-to-end solutions combining cell retention, real-time analytics, and AI-driven process control. Emerging firms in microfluidics and smart sensors target niche applications, particularly cell therapy. Market dynamics are influenced by regulatory harmonization, cost pressures, sustainability mandates, and R&D-driven capacity upgrades.

Key Industry Developments

- In September 2025, Distek expanded its BIOne Single-Use Bioreactor (SUB) line with new models compatible with perfusion technologies, such as Repligen's XCell® and KrosFlo® TFDF® systems. The new bioreactors come in 2L, 5L, and 10L working volumes, designed for process development, scale-up, and small-scale production. They support applications including recombinant proteins, monoclonal antibodies, and cell therapies.

- In March 2025, Los Alamos researchers developed a 3D-printed perfusion bioreactor that enhances stem cell growth by improving nutrient delivery and mimicking physiological conditions, boosting viability and proliferation, and addressing limitations of traditional bioreactors for regenerative medicine applications.

- In March 2025, STEER World and Gericke partnered to create a fully integrated continuous granulation system for pharmaceutical OSD manufacturing. The solution ensures consistent granule quality, minimizes manual intervention, lowers analytics costs, and reduces operational footprint. It merges Gericke’s system integration expertise with STEER World’s patented Integraal™ technology.

Companies Covered in Perfusion Bioreactors Market

- Merck KGaA

- Sartorius AG

- Pall Corporation

- Cytiva

- Bionet Co., Ltd.

- FiberCell Systems

- WuXi Biologics

- Lonza AG

- Rentschler Biopharma

- Xpect Biotech

- Viscient Biosciences

- ABEC

- Eppendorf

- Meissner Filtration Products

- GE Healthcare Life Sciences

Frequently Asked Questions

The global perfusion bioreactors market is projected to reach US$420.0 Million in 2025.

The growing adoption of continuous manufacturing processes, technological advancements, and rising demand for high-density cell cultures are driving the perfusion bioreactors market.

The perfusion bioreactors market is poised to witness a CAGR of 7.9% from 2025 to 2032.

Innovations in single-use systems and AI-enabled bioprocess control, and increasing integration of perfusion bioreactors to meet the dynamic demands of next-generation therapies by biopharmaceutical companies, CMOs, and research institutions are key market opportunities.

Merck KGaA, Sartorius AG, Pall Corporation, and Cytiva are some of the key players in the perfusion bioreactors market.