- Automation & Robotics

- Palletizing Robots Market

Palletizing Robots Market Size, Share, and Growth Forecast, 2026 – 2033

Palletizing Robots Market by Robot Type (Articulated Robots, Cobots, SCARA, Others), Application (Cases and Boxes Palletizing, Others), End-user (Discrete Manufacturing, Chemicals & Materials, Others), and Regional Analysis for 2026 – 2033

Palletizing Robots Market Size and Trends Analysis

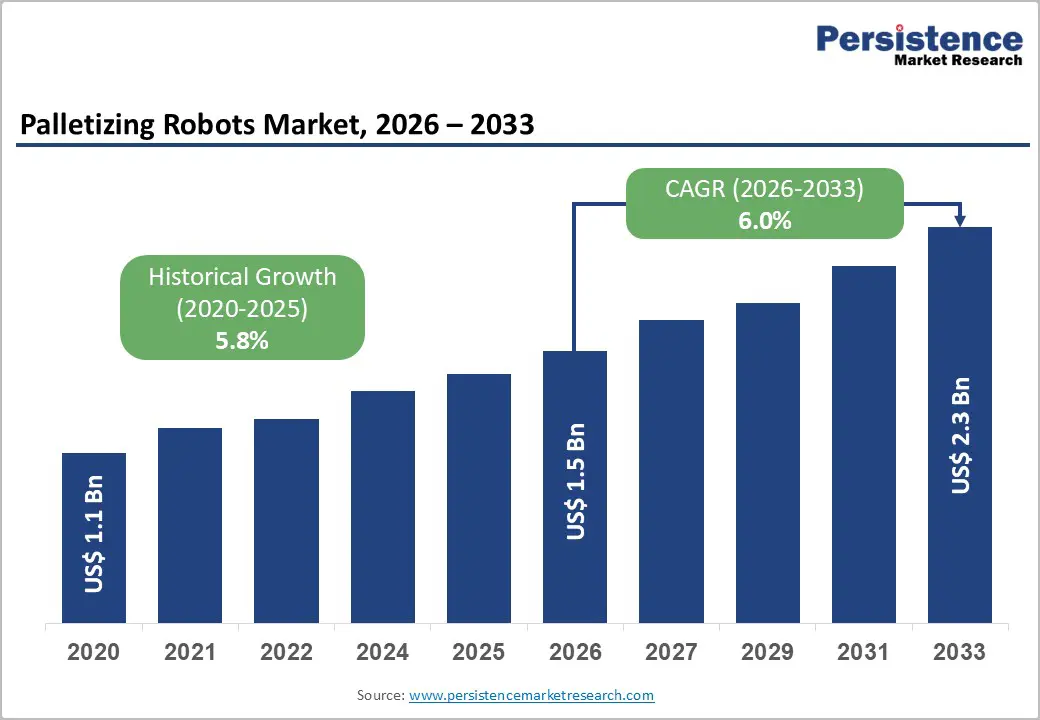

The global palletizing robots market size is likely to be valued at US$1.5 billion in 2026 and is expected to reach US$2.3 billion by 2033, growing at a CAGR of 6.0% during the forecast period from 2026 to 2033, driven by the increasing adoption of industrial automation across manufacturing and logistics environments. The growing need for efficient end-of-line packaging operations, combined with ongoing labor shortages and rising operational costs, is encouraging companies to deploy robotic palletizing systems that enhance productivity, consistency, and workplace safety. Rapid growth in e-commerce and organized retail is also driving demand for high-speed palletizing solutions capable of handling diverse product formats and mixed-SKU orders. Industries such as food and beverage, consumer goods, pharmaceuticals, and chemicals are also increasingly integrating flexible robotic systems to manage high-volume packaging and distribution processes. Advancements in robotic technologies, including improved sensors, vision systems, and collaborative capabilities, are enabling easier integration of palletizing robots within modern production lines and automated warehouses.

Key Industry Highlights:

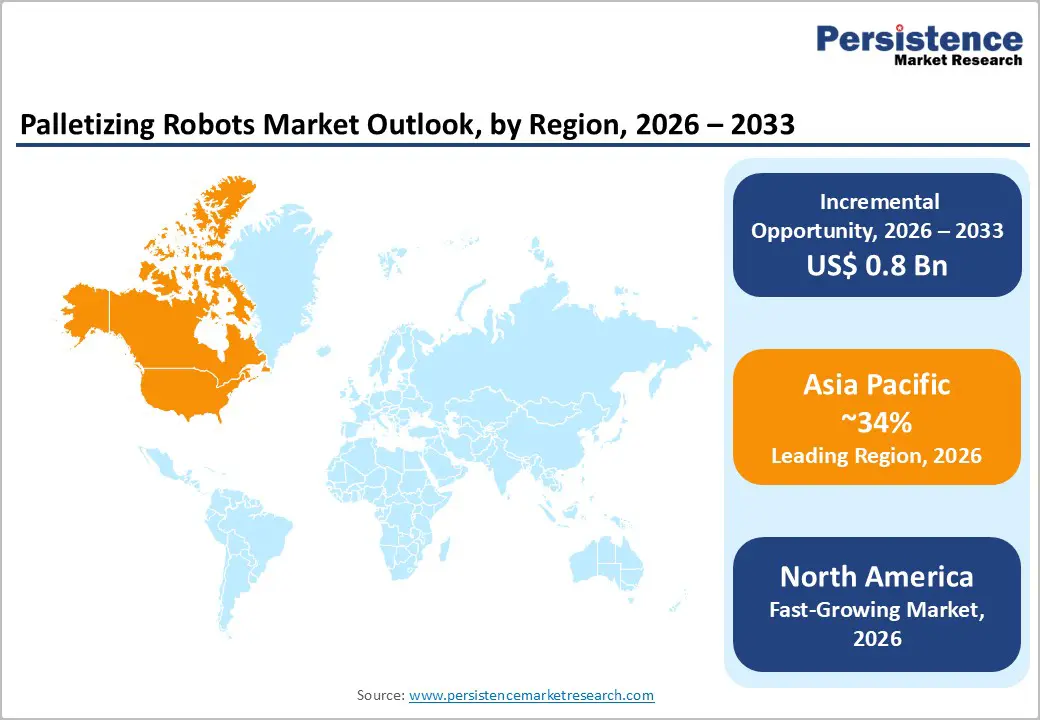

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 34% in 2026, driven by strong manufacturing capacity, expanding e-commerce logistics, and increasing adoption of automation across China, India, and ASEAN countries.

- Fastest-growing Region: North America is likely to be the fastest-growing region, supported by rapid advanced warehouse automation, strong e-commerce distribution networks, and increasing adoption of robotic palletizing systems across logistics and manufacturing sectors.

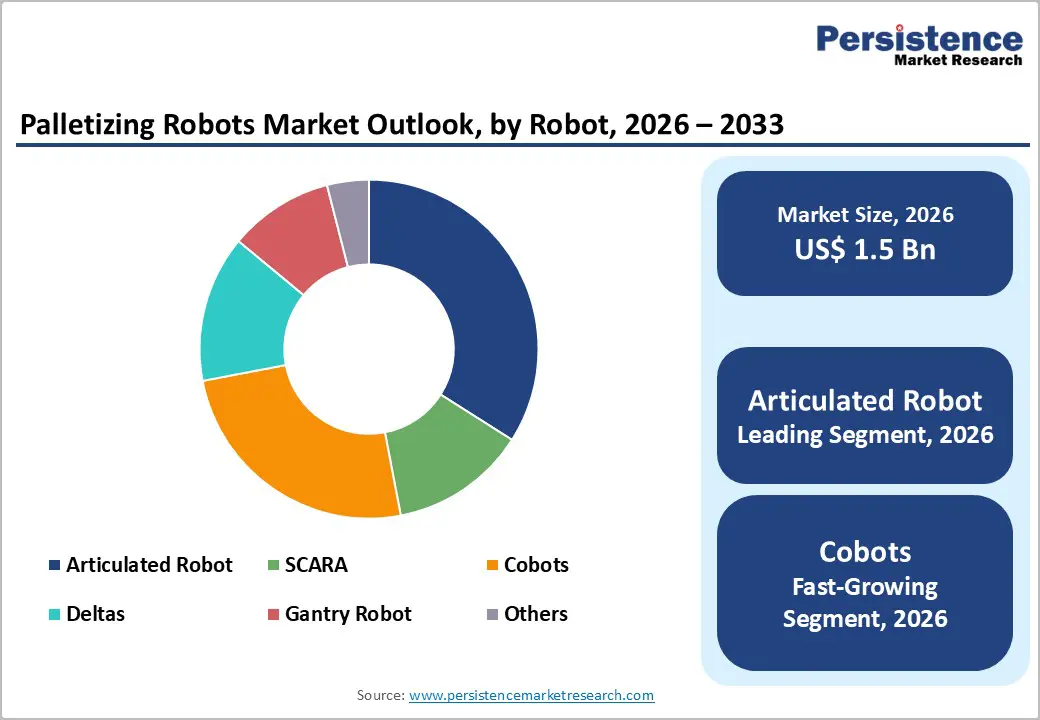

- Leading Robot Type: Articulated robots are projected to represent the leading robot type in 2026, accounting for 48% of the revenue share, driven by their multi-axis flexibility and ability to manage complex palletizing operations across industries.

- Leading Application: The cases and boxes palletizing segment is anticipated to be the leading application, accounting for over 33% of the revenue share in 2026, supported by its widespread use in high-volume packaging across food, consumer goods, and pharmaceutical industries.

| Key Insights | Details |

|---|---|

|

Palletizing Robots Market Size (2026E) |

US$1.5 Bn |

|

Market Value Forecast (2033F) |

US$2.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis- Labor Shortages and Demographic Shifts Drive Adoption

Aging workforces in industrial economies and declining availability of manual labor for physically demanding warehouse tasks are pushing companies to automate end-of-line packaging operations. Palletizing activities traditionally require repetitive lifting and continuous handling of heavy cartons or sacks, making them difficult to staff consistently. Robotic palletizing systems provide a reliable alternative by maintaining consistent throughput while reducing dependence on manual workers. Industries such as food and beverage, consumer goods, and logistics distribution centers increasingly deploy articulated robots and collaborative systems to ensure operational continuity and improve workplace safety.

Demographic shifts are also contributing to long-term structural changes in labor availability, particularly in developed economies where younger workers are less inclined toward physically intensive warehouse jobs. This has encouraged manufacturers and logistics operators to invest in automated palletizing solutions capable of operating continuously with minimal supervision. Robotic palletizing cells improve productivity by reducing downtime, eliminating human fatigue, and enabling consistent stacking accuracy. Automation allows companies to reassign available workers to higher-value operational roles such as quality control, supervision, and process management.

E-Commerce and Supply-Chain Complexity Accelerate Demand

The rapid expansion of e-commerce has dramatically increased the complexity of modern supply chains, creating strong demand for automated palletizing solutions. Online retail requires warehouses and distribution centers to process large volumes of mixed products with varying sizes, weights, and packaging formats. Manual palletizing struggles to maintain the speed and accuracy required for such dynamic order fulfillment environments. Robotic palletizing systems equipped with advanced grippers and programmable stacking patterns allow facilities to manage high product variety while maintaining consistent throughput. As retailers expand omnichannel logistics operations, palletizing robots are increasingly deployed to streamline packaging, sorting, and shipping workflows within automated warehouses.

Supply chains are also becoming more geographically distributed and time-sensitive, requiring faster handling of goods from production facilities to distribution hubs. Automated palletizing systems help companies maintain operational efficiency by enabling high-speed stacking, reducing handling errors, and improving load stability during transport. Robotic systems integrate with warehouse management and conveyor systems, creating seamless material-handling workflows that support continuous operations. Industries including consumer packaged goods, pharmaceuticals, and electronics rely on palletizing robots to manage increasing shipment volumes while maintaining product safety and consistency. As supply chain complexity continues to rise, automation plays a critical role in ensuring reliable distribution performance.

Barrier Analysis - Integration Complexity with Legacy Systems Poses Structural Challenges

Despite strong adoption trends, integration complexity with legacy manufacturing infrastructure remains a key restraint for the palletizing robots market. Many production facilities still operate older conveyor systems, packaging equipment, and control software that were not designed to support robotic automation. Integrating modern palletizing robots into these environments often requires extensive system redesign, additional hardware interfaces, and customized programming. Such modifications can increase project timelines and implementation costs, particularly for small and medium-sized facilities with limited automation expertise. Companies delay or scale back automation investments when faced with operational disruptions during the integration process.

Legacy infrastructure also limits the ability to achieve full operational efficiency from robotic palletizing systems. Older equipment lacks standardized communication protocols or real-time data connectivity needed for seamless automation workflows. This can create bottlenecks where robotic systems operate faster than upstream or downstream processes, reducing overall productivity gains. Workforce training and maintenance requirements increase when integrating new robotics technologies into existing facilities. Companies must often rely on specialized system integrators to manage deployment and ensure compatibility across production lines. These technical and operational challenges continue to slow adoption in facilities that rely heavily on older manufacturing infrastructure.

Product Variability and Irregular Packaging Constrain Performance

Product variability and irregular packaging formats present operational challenges for palletizing robots in many industries. Items such as flexible bags, irregularly shaped packages, or unstable bundles require precise handling to ensure stable pallet loads. Traditional robotic palletizing systems are optimized for uniform cartons or rigid boxes, making it more difficult to manage products with inconsistent dimensions or weight distribution. When packaging varies significantly, robots require specialized grippers, vision systems, or additional programming to maintain stacking accuracy. Without these adaptations, robotic palletizing operations may experience reduced efficiency or increased risk of product damage during automated handling processes.

Industries such as agriculture, chemicals, and bulk materials frequently rely on flexible packaging formats that are more difficult to automate compared to rigid containers. Variations in bag shape, filling levels, and surface friction can affect how items are gripped and stacked during palletizing operations. This complexity limits the speed of robotic handling or requires advanced sensors and adaptive algorithms to maintain stability. Facilities that handle diverse product lines often need multiple robotic configurations or customized end-effectors to support different packaging types. These technical requirements increase implementation complexity and can slow broader adoption of palletizing robots in highly variable packaging environments.

Opportunity Analysis - AI and Vision-Guided Convergence Unlocks Flexible Palletizing

Vision-guided systems enable robots to identify product orientation, size variations, and positioning on conveyors in real time. This allows robotic palletizers to adapt dynamically to different packaging formats without extensive reprogramming. AI-driven algorithms can optimize stacking patterns, improve object detection accuracy, and reduce handling errors during high-speed operations. These capabilities expand the range of products that can be automated, including irregular packages and mixed-SKU orders. Manufacturers and logistics operators can deploy palletizing robots in more complex packaging environments.

The integration of AI-enabled robotics also supports the development of smarter and more connected production lines. Vision-guided palletizing systems can communicate with warehouse management and packaging systems to coordinate product flow and stacking configurations automatically. This improves operational flexibility while enabling facilities to respond quickly to changing order requirements. AI technologies allow predictive adjustments that maintain consistent load stability and minimize downtime caused by misaligned products. As robotics hardware becomes more affordable and software capabilities continue to advance, AI-driven palletizing solutions are expected to expand across industries seeking adaptable automation for high-mix production and distribution operations.

Cobots for SMEs and Human-Robot Collaboration

Collaborative robots, or cobots, represent a major growth opportunity within the palletizing robots market, particularly for small and medium-sized enterprises. Unlike traditional industrial robots that require safety cages and complex installations, cobots are designed to operate safely alongside human workers using integrated sensors and force-limiting technologies. Their simplified programming and modular design allow companies with limited automation experience to deploy palletizing solutions more easily. Cobots are especially useful in facilities handling moderate production volumes where flexible automation is preferred over large robotic systems. This accessibility enables smaller manufacturers and packaging operations to improve efficiency without extensive infrastructure upgrades.

Human-robot collaboration is transforming how palletizing tasks are performed in modern manufacturing environments. Cobots can assist workers by handling repetitive lifting and stacking operations while humans manage quality checks, adjustments, and supervision. This hybrid approach improves workplace ergonomics and reduces injury risks associated with manual palletizing. Cobots allow rapid redeployment across different packaging lines, making them suitable for facilities producing multiple product types. Their scalability and lower implementation complexity make collaborative palletizing solutions attractive for businesses seeking gradual automation adoption.

Category-wise Analysis

Robot Type Insights

Articulated robots are expected to lead the palletizing robots market, accounting for approximately 48% of revenue in 2026, driven by their exceptional flexibility and capability to perform complex palletizing tasks across diverse industrial environments. These robots feature multiple rotating joints that allow a wide range of motion, enabling them to handle heavy payloads and manage intricate stacking patterns with high precision. For example, FANUC provides articulated palletizing robots widely used in beverage bottling plants, where they efficiently stack cartons and cases at the end of automated packaging lines.

Cobots (collaborative robots) are likely to represent the fastest-growing segment, supported by their ability to safely operate alongside human workers and their simplified programming requirements. Unlike traditional industrial robots that require extensive safety barriers and specialized programming, cobots are designed with built-in sensors and force-limiting features that allow safe human-robot interaction. Collaborative palletizing robots support improved workplace ergonomics by taking over repetitive lifting tasks while employees focus on supervision and quality control. For example, KUKA Robotics Corporation offers collaborative robotic solutions used in packaging facilities where workers and robots share palletizing tasks efficiently.

Application Insights

The cases and boxes palletizing segment is projected to lead the market, capturing around 33% of the revenue share in 2026, supported by its widespread use in industries that rely on standardized packaging formats. Corrugated cartons and rigid cases are commonly used in sectors such as food and beverage, pharmaceuticals, and consumer packaged goods because they offer structural stability and ease of stacking during transportation and storage. For example, Kawasaki Robotics supplies robotic palletizing systems used in beverage and packaged food facilities where robots rapidly stack cartons onto pallets for streamlined distribution and logistics operations.

Bags and sacks palletizing is likely to be the fastest-growing application, driven by increasing automation demand in industries handling bulk and flexible packaging formats. Sectors such as agriculture, chemicals, fertilizers, and construction materials frequently use sacks to package powdered or granular products. Flexible packaging can be difficult to handle manually due to irregular shapes and shifting weight distribution. Trade in bulk materials expands, and sustainability initiatives encourage the use of recyclable sack packaging; automation solutions for bag palletizing are becoming more attractive. For example, Yaskawa America, Inc. offers robotic palletizing systems designed for handling industrial sacks in chemical and agricultural processing plants, enabling consistent stacking and improved material-handling efficiency.

Regional Insights

North America Palletizing Robots Market Trends

North America is likely to be the fastest-growing region in palletizing robots, driven by increasing automation across manufacturing plants, logistics hubs, and e-commerce fulfillment centers. Companies in the U.S. and Canada are investing heavily in robotic palletizing systems to address labor shortages, rising wages, and the need for consistent high-speed packaging operations. Food and beverage manufacturers, consumer packaged goods producers, and pharmaceutical companies are among the largest adopters of robotic palletizers because they require reliable and hygienic end-of-line handling solutions.

Businesses are increasingly deploying automated systems that combine palletizing robots with AI-driven inventory management, conveyor networks, and warehouse management software to improve productivity and accuracy. These technologies allow facilities to process large volumes of goods while minimizing manual handling and operational errors. E-commerce growth has particularly accelerated this trend, as retailers and logistics providers seek scalable automation capable of managing high-volume order fulfillment. For example, Symbotic, a U.S.-based warehouse automation company, develops AI-powered robotic systems used by major retail and grocery operators to automate storage, picking, and palletizing workflows within distribution centers.

Europe Palletizing Robots Market Trends

Europe is likely to be a significant market for palletizing robots in 2026, due to increased automation investments to improve productivity, workplace safety, and supply-chain efficiency. Countries such as Germany, Italy, France, and the U.K. are leading adoption due to their strong industrial bases and advanced manufacturing ecosystems. Food and beverage processing, pharmaceuticals, and consumer goods packaging are among the key industries deploying palletizing robots to streamline end-of-line packaging operations. Strict workplace safety regulations and high labor costs are also accelerating the shift from manual pallet handling to automated robotic systems.

Many European manufacturers are integrating palletizing robots with digital control systems, data analytics, and AI-enabled optimization tools to improve stacking accuracy and reduce downtime. For example, KUKA AG, headquartered in Germany, develops advanced robotic palletizing solutions widely used in food processing and industrial packaging plants across Europe. These robotic systems enable manufacturers to automate high-volume packaging tasks while maintaining consistent quality and operational efficiency. Germany remains a key hub for robotic innovation due to strong manufacturing capabilities and government-supported industry programs that encourage automation adoption across factories and logistics networks.

Asia Pacific Palletizing Robots Market Trends

The Asia Pacific region is anticipated to be the leading region, accounting for a market share of 34% in 2026, driven by strong manufacturing activity, increasing automation investments, and the growth of large-scale logistics infrastructure across countries such as China and India. The region leads the adoption of palletizing robots as manufacturers modernize production lines to improve productivity and reduce dependence on manual labor. Rapid industrialization and government initiatives supporting smart factories are accelerating the deployment of robotic palletizing systems in sectors including electronics, consumer goods, food processing, and pharmaceuticals. Warehousing automation linked to expanding e-commerce networks is also creating strong demand for robotic end-of-line solutions capable of handling high product volumes and mixed packaging formats.

Manufacturers are increasingly adopting intelligent palletizing systems equipped with machine vision, AI-based motion control, and flexible grippers to handle different product formats and packaging types. These technologies improve operational efficiency while reducing product handling errors and downtime in large factories and distribution facilities. For example, Mitsubishi Electric provides industrial robotic solutions widely used in Asian packaging and manufacturing plants for automated palletizing operations. The company’s robotic systems support high-speed product handling and are commonly deployed in electronics and consumer goods manufacturing facilities.

Competitive Landscape

The global palletizing robots market exhibits a moderately fragmented structure, driven by the presence of multiple international robotics manufacturers and specialized automation providers focusing on material-handling solutions for packaging, warehousing, and logistics operations. Growing demand for automated end-of-line systems across food & beverage, pharmaceuticals, and e-commerce fulfillment centers has intensified competition among vendors offering high-speed robotic palletizers, flexible grippers, and vision-guided stacking technologies.

With key leaders including FANUC, ABB, KUKA, Yaskawa Electric Corporation, and Kawasaki Heavy Industries, the competitive landscape is shaped by companies that combine advanced robotics engineering with strong distribution networks and system-integration capabilities. These players compete through continuous product innovation, strategic partnerships with automation integrators, expansion of service networks, and development of flexible palletizing solutions capable of handling mixed-product loads.

Key Industry Developments:

- In February 2026, Kawasaki Heavy Industries launched the CP110L high-speed palletizing robot, designed with a compact structure and enhanced handling capacity to support automated palletizing in logistics and manufacturing environments with limited installation space.

- In January 2026, Universal Robots and Robotiq, in collaboration with Siemens, unveiled a next-generation robotic palletizing solution at the Consumer Electronics Show 2026, integrating the UR20 collaborative robot with Robotiq’s PAL Ready palletizing cell and Siemens’ digital-twin software to enhance automated palletizing efficiency in manufacturing and logistics operations.

- In January 2025, KUKA introduced the KR FORTEC PA and KR FORTEC ultra PA heavy-duty palletizing robot families, designed to improve efficiency in industrial palletizing with high payload capacity, modular design, and lower operating costs for logistics, manufacturing, and packaging applications.

Companies Covered in Palletizing Robots Market

- FANUC

- Kuka Robotics Corporation

- Kawasaki Robotics

- Yaskawa America, Inc.

- MMCI Robotics

- MHI

- RMH Systems

Frequently Asked Questions

The global palletizing robots market is projected to reach US$1.5 billion in 2026.

The palletizing robots market is driven by increasing industrial automation, labor shortages in manufacturing and logistics, and rising demand for efficient high-speed packaging and warehouse operations.

The palletizing robots market is expected to grow at a CAGR of 6.0% from 2026 to 2033.

Key opportunities in the palletizing robots market arise from the growing adoption of AI-enabled vision systems, the expansion of collaborative robots for SMEs, and increasing automation in e-commerce warehouses and smart manufacturing facilities.

FANUC, KUKA Robotics Corporation, Kawasaki Robotics, Yaskawa America, Inc, and MMCI Robotics are the leading players.