- Processed Food

- Packaged Fruit Snacks Market

Packaged Fruit Snacks Market Size, Share, and Growth Forecast, 2025 - 2032

Packaged Fruit Snacks Market by Product Type (Dried Fruit Snacks, Fruit Bars & Cups, Frozen Fruit Snacks, Fruit Leather), Packaging (Single Serve Packs, Bulk Packaging, Pouches, Cups & Jars, Resealable Bags, Others), Ingredient (Organic, Non-organic, Natural Sweeteners, Sugar Free, Additive Free), Distribution Channel, and Regional Analysis for 2025 - 2032

Packaged Fruit Snacks Market Size and Trend Analysis

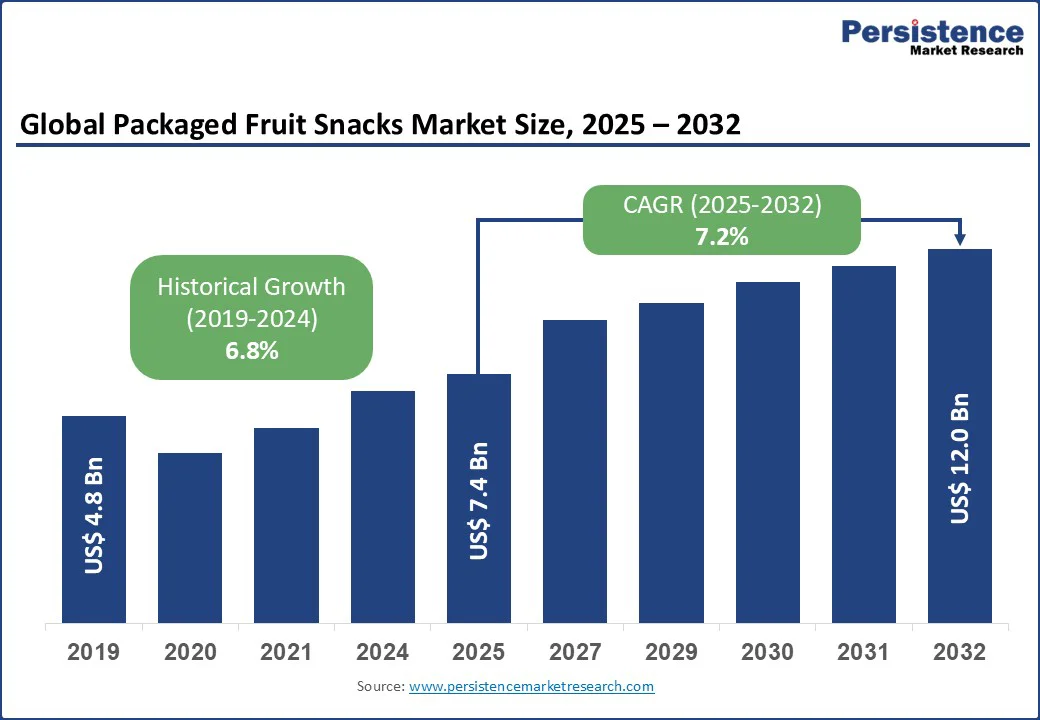

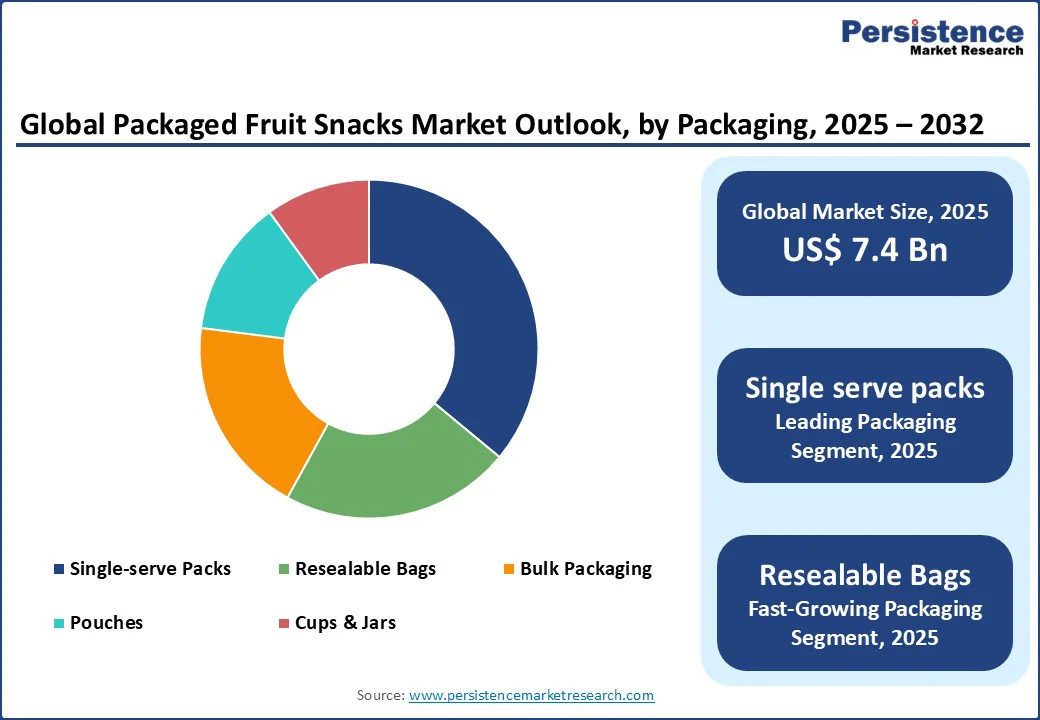

The global packaged fruit snacks market size is likely to be valued at US$7.4 bn in 2025 and is estimated to reach US$12.0 bn by 2032, growing at a CAGR of 7.2% during the forecast period from 2025 to 2032.

The growth is driven by rising health consciousness and demand for convenient, nutrient-rich snacks.

Consumers increasingly prefer organic, sugar-free, and additive-free fruit snacks. Busy lifestyles and on-the-go consumption further boost adoption, while innovation in functional ingredients, portion-controlled packaging, and sustainable solutions strengthens market expansion globally.

Key Industry Highlights

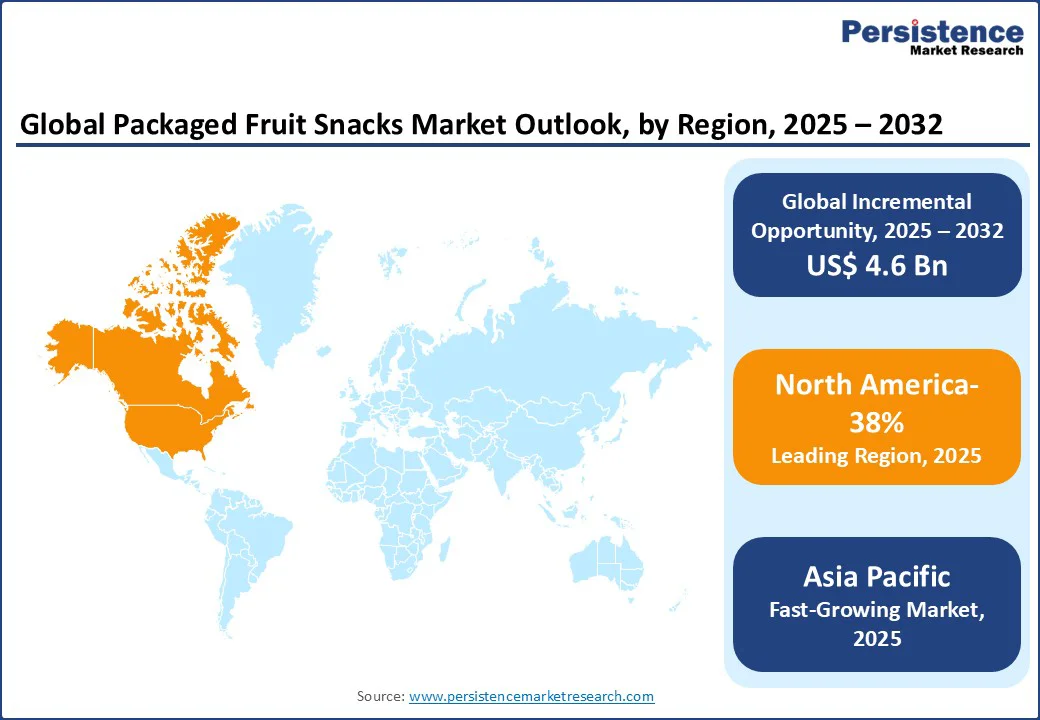

- Leading Region: North America accounted for 38% of the global packaged fruit snacks market in 2025, supported by strong demand for organic, sugar-free, and additive-free snack varieties.

- Fastest-Growing Region: Asia Pacific is projected to register the highest CAGR, driven by rising health awareness, urbanization, and rapid retail expansion in markets such as India and China.

- Dominant Product Type: Dried fruit snacks held nearly 52% share, benefiting from extended shelf life, portability, and strong consumer acceptance as a natural snacking option.

- Leading Ingredient: Organic ingredients represented around 40% of the market, reflecting consumer preference for clean-label, sustainable, and pesticide-free products.

- Leading Distribution Channel: Supermarkets and hypermarkets captured 45% of sales, owing to their wide product assortment, visibility for new launches, and convenience for bulk shopping.

- Key Developments: In November 2024, Welch’s launched the FruitSide™ Assistance campaign with zero-sugar fruit bites, while in June 2025, David Beckham co-founded BEEUP, a honey-based fruit snack brand debuting at Target and online

|

Global Market Attribute |

Key Insights |

|

Packaged Fruit Snacks Market Size (2025E) |

US$7.4 Bn |

|

Market Value Forecast (2032F) |

US$12.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.8% |

Market Dynamics

Driver: Rising Health Consciousness and Demand for Convenient Snacks

Rising health consciousness is a key driver of the packaged fruit snacks market, as consumers increasingly focus on nutrition, balanced diets, and preventive wellness. With greater awareness of obesity, diabetes, and heart health risks, buyers are shifting toward snacks that provide natural vitamins, minerals, and fiber without excess sugar or artificial additives.

Packaged fruit snacks such as dried fruits, fruit bars, and fruit purées align with this demand, offering nutrient-dense options that support healthier lifestyles. Their convenience and portion-controlled packaging make them highly appealing for busy individuals who want quick, on-the-go choices that do not compromise health.

Government initiatives further reinforce this trend. For instance, the U.S. Department of Agriculture promotes “smart snacks” in schools by encouraging the inclusion of single-serve packaged fruit such as sliced apples, blueberries, and fresh-cut peaches. These initiatives highlight how packaged fruit snacks meet both health and convenience needs. By combining nutritional value with portability, this segment continues to grow as a preferred alternative to traditional, calorie-dense snack foods.

Restraint: High Costs of Organic and Premium Products

The high costs associated with organic and premium packaged fruit snacks act as a major restraint on market growth. Organic fruit snacks are produced using certified farming methods, free from synthetic pesticides and chemical additives, which increases cultivation, processing, and certification expenses.

Similarly, premium offerings often involve innovative packaging, exotic fruit varieties, or value-added features such as non-GMO or gluten-free claims. These factors push production costs significantly higher compared to conventional snacks, making them less accessible to price-sensitive consumers, particularly in emerging economies.

While health-conscious buyers in developed markets may be willing to pay extra for organic and premium fruit snacks, affordability remains a challenge for wider adoption. The price gap between conventional and organic products limits penetration in mass retail channels, slowing overall demand growth. This restraint creates a market imbalance where consumer awareness of healthier options is rising, but actual purchase decisions are restricted by cost barriers, impacting volume sales and broader market expansion.

Opportunity: Innovation in Functional Ingredients and Emerging Markets

Innovation in functional ingredients presents a strong growth opportunity in the packaged fruit snacks market. Consumers are increasingly seeking snacks that deliver added health benefits beyond basic nutrition. Incorporating functional ingredients such as probiotics, plant proteins, antioxidants, omega-3 fatty acids, and superfruits enhances the value proposition of fruit snacks.

These innovations allow manufacturers to position products as not only convenient and tasty but also supportive of digestive health, immunity, and energy needs. The growing interest in clean-label and fortified snacks is encouraging brands to expand their product portfolios with premium, multifunctional fruit snack offerings.

At the same time, emerging markets are becoming key growth frontiers for the packaged fruit snacks industry. Rising disposable incomes, rapid urbanization, and increasing health awareness in regions such as the Asia Pacific, Latin America, and the Middle East are driving demand for convenient, nutrient-rich snack options. Expanding retail networks and e-commerce penetration further amplify accessibility. Together, functional ingredient innovation and emerging market expansion create significant opportunities for long-term growth.

Category-wise Insights

Product Type Insights

Among the product types, dried fruit snacks account for the largest share of the packaged fruit snacks market, representing close to 52% of global sales. Their dominance is driven by longer shelf life, convenience, and versatility across consumer groups. Products such as raisins, cranberries, apricots, and mango slices are perceived as clean-label, nutrient-rich alternatives to confectionery, making them highly popular in both developed and emerging markets.

Easy availability in supermarkets, convenience stores, and online platforms further boosts their consumption. With health-conscious buyers seeking natural, minimally processed options, dried fruit snacks remain the backbone of the category and continue to secure the highest revenue contribution

Fruit bars and cups are the fastest-growing segment. Their success stems from portion-controlled packaging, added functional ingredients, and a strong appeal to millennials, working professionals, and school-age children. Fortified fruit bars with proteins, fibers, or superfruit blends are gaining rapid traction, while fruit cups are increasingly adopted for lunchboxes and quick snacking. This adaptability and innovation potential are expected to make fruit bars and cups the leading growth driver, recording the highest CAGR among all product types

Packaging Insights

In the packaged fruit snacks market, single-serve packs dominate with an estimated 36% share of global sales. Their popularity is fueled by strong demand for portion-controlled, on-the-go snacking among children, office workers, and health-conscious buyers.

Single-serve packaging ensures freshness, convenience, and portability, making it especially suitable for school programs, travel, and vending machine distribution. As parents and busy consumers look for ready-to-eat, pre-measured fruit snacks, this packaging format continues to lead the market. Its wide availability across supermarkets, convenience stores, and e-commerce channels further strengthens its position as the most preferred packaging type.

Beyond single-serve formats, resealable bags are emerging as one of the fastest-growing packaging solutions. These bags address consumer concerns about food preservation and waste reduction by allowing snacks to stay fresh even after opening.

They are particularly favored for family-sized purchases and bulk buying. Lightweight pouches and eco-friendly designs also support sustainability goals, further boosting demand. Together, resealable bags and innovative pouches complement single-serve packs, ensuring that packaging remains a key differentiator, driving consumer appeal and long-term growth.

Ingredient Insights

By ingredient type, the organic segment dominates the packaged fruit snacks market, contributing roughly 40% of global revenue. Growing health consciousness and rising demand for clean-label products have fueled the preference for organic fruit snacks, which are free from synthetic pesticides and chemicals.

Consumers view them as safer, healthier alternatives that align with sustainable farming practices and eco-friendly choices. This segment is particularly strong in developed markets, where buyers are willing to pay a premium for organic certification and transparency in sourcing.

Alongside organic, the sugar-free and additive-free categories are among the fastest-growing segments, propelled by increasing awareness of diabetes, obesity, and lifestyle-related health concerns. Fruit snacks formulated with natural sweeteners such as stevia or monk fruit are gaining traction, as they offer indulgence without excess calories.

These innovations cater to health-conscious millennials, parents seeking better options for children, and consumers prioritizing wellness. As demand for functional, guilt-free snacking rises, sugar-free and additive-free formulations are expected to record the highest CAGR.

Distribution Channel Insights

In the packaged fruit snacks market, hypermarkets and supermarkets dominate distribution, accounting for around 45% of total sales. These large retail outlets offer wide product assortments, attractive discounts, and strong brand visibility, making them the primary choice for consumers.

Shoppers often prefer purchasing packaged fruit snacks during routine grocery trips, and the availability of private-label products further strengthens this channel. Supermarkets also serve as a launch platform for new snack varieties, giving consumers access to innovative dried fruits, bars, and fruit cups under one roof. Their established presence in both developed and emerging regions ensures consistent demand through this channel.

Meanwhile, online retail is the fastest-growing distribution channel, driven by the rise of e-commerce platforms, home delivery services, and digital promotions. Consumers increasingly turn to online stores for bulk purchases, subscription snack boxes, and niche organic or premium fruit snacks not always available offline.

Convenience stores also remain important for impulse and on-the-go purchases, while specialty stores cater to buyers seeking premium or organic options. Together, these channels create a balanced ecosystem, but e-commerce is expected to record the highest CAGR due to shifting consumer shopping habits.

Regional Insights

North America Packaged Fruit Snacks Market Trends

North America leads the packaged fruit snacks market, holding nearly 38% of global share. Strong consumer demand for healthy, convenient, and clean-label snacks drives this dominance, supported by high awareness of nutrition and preventive wellness.

The presence of leading brands, advanced retail infrastructure, and growing adoption of organic and sugar-free options further strengthen the region’s position. Additionally, the popularity of portion-controlled packs and functional fruit bars makes North America the most influential market for driving innovation and long-term growth.

Europe Packaged Fruit Snacks Market Trends

Europe holds a significant share of the packaged fruit snacks market, driven by strong consumer preference for organic, additive-free, and sustainably sourced products. High health awareness, strict food regulations, and demand for clean-label snacks support market expansion in the region.

Retailers and specialty stores play a key role in promoting premium fruit bars, dried fruits, and functional snack varieties. With the rising adoption of plant-based and sugar-free options, Europe remains a crucial market contributing consistently to overall industry growth.

Asia Pacific Packaged Fruit Snacks Market Trends

Asia Pacific is the fastest-growing region in the packaged fruit snacks market, supported by rapid urbanization, rising disposable incomes, and shifting dietary habits. Increasing health awareness is driving demand for convenient, nutrient-rich snacks among young consumers and working professionals.

Expanding supermarket chains, strong e-commerce penetration, and government initiatives promoting healthy eating further accelerate growth. With growing preference for organic, sugar-free, and functional fruit snacks, the Asia Pacific is expected to record the highest CAGR, emerging as a key engine of market expansion.

Competitive Landscape

The global packaged fruit snacks market is highly competitive, driven by continuous innovation in flavors, functional ingredients, and eco-friendly packaging. Companies emphasize clean-label, sugar-free, and organic formulations to align with evolving consumer trends. Regional manufacturers are also expanding through online platforms, targeting health-conscious buyers and niche product categories for differentiation.

Key Developments

- November 2024: Welch’s Fruit Snacks launched the FruitSide™ Assistance campaign, promoting zero-sugar fruit bites and travel-friendly kits to support holiday journeys, strengthening consumer engagement and brand visibility.

- June 2025: David Beckham co-founded BEEUP, a honey-based fruit snack brand offering gluten-free, naturally sweetened packs. Positioned as a healthy energy snack, the line debuted at Target and online platforms, appealing to health-conscious families.

- June 2025: Welch’s introduced Juicefuls Fusions, a dual-flavor fruit gummy with a chewy outer layer and juicy center. Fortified with vitamins A, C, and E, the product was launched across leading retail and e-commerce channels, targeting the growing demand for functional, indulgent fruit snacks.

Companies Covered in Packaged Fruit Snacks Market

- General Mills

- Kellogg

- Sun Opta

- Sunkist Growers

- Welch’s

- Flaper

- Bare Foods

- Crispy Green

- Crunchies Natural Food

- Mount Franklin Foods

- Nourish Snacks

- Nutty Goodness

- Paradise Fruits

- Peeled Snacks

- Tropical Foods

- WhiteWave Foods

- Others

Frequently Asked Questions

The packaged fruit snacks market is projected to reach US$7.4 Bn in 2025, driven by demand for healthy and convenient snacks.

Rising health consciousness, demand for organic and additive-free products, and convenient packaging fuel market growth.

The market will grow from US$7.4 Bn in 2025 to US$12.0 Bn by 2032, with a CAGR of 7.2%.

Innovations in functional ingredients and expansion in emerging markets drive growth opportunities.

Leading players include General Mills, Kellogg, SunOpta, Sunkist Growers, Welch’s, and Bare Foods.