- LED & Lighting (Optoelectronics)

- Packaged LED Market

Packaged LED Market Size, Share, and Growth Forecast 2025 - 2032

Packaged LED Market by Packaging Type (Surface Mount Device, Chip On Board (COB), Others), Power Range (Mid-Power LEDs 0.5 W–1 W, Low-Power LEDs 0.3 W–0.5 W, Others), Application (General Lighting, Backlighting, Others), and Regional Analysis for 2025 - 2032

Packaged LED Market Size and Trend Analysis

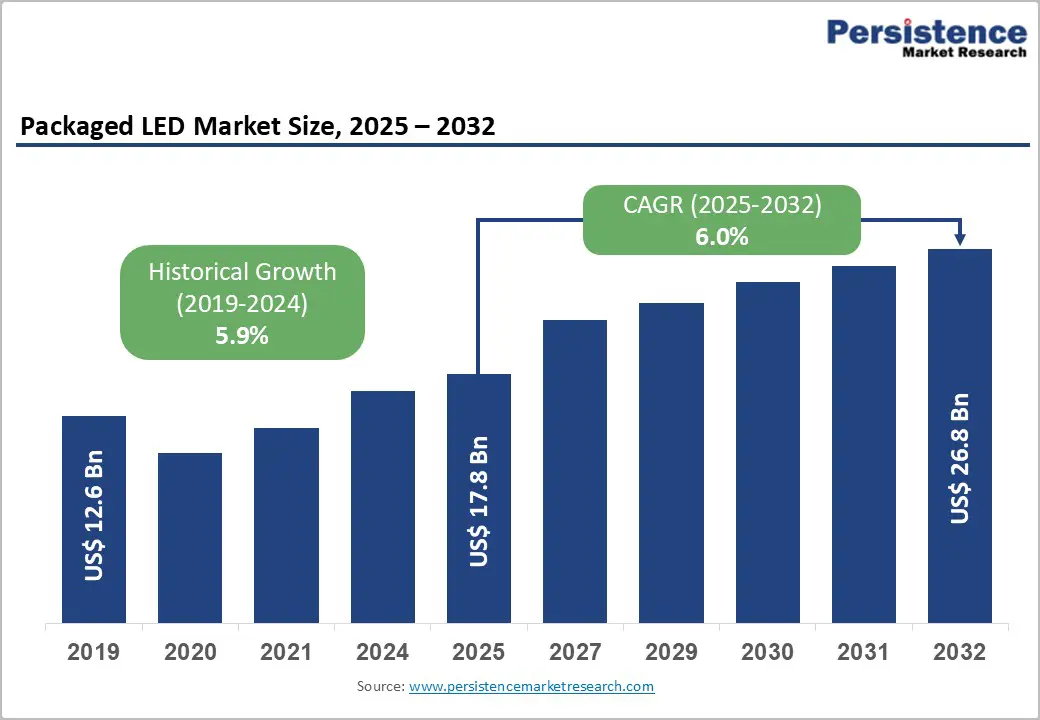

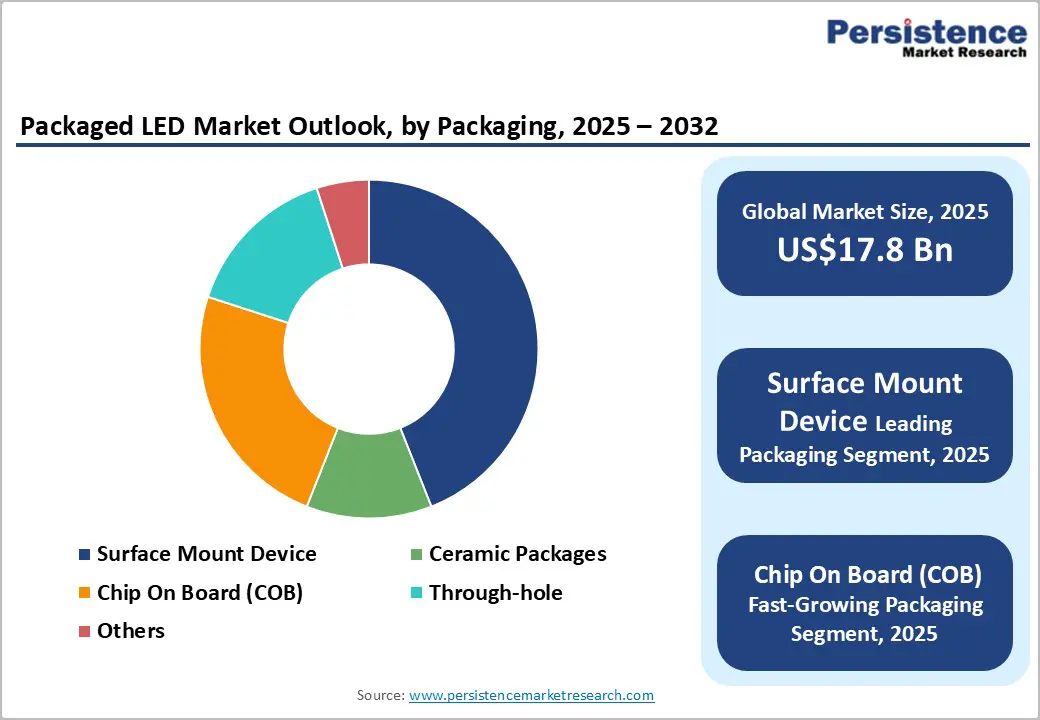

The global packaged LED market size is likely to be valued at US$17.8 billion in 2025 and is expected to reach US$26.8 billion by 2032, growing at a CAGR of 6.0% during the forecast period from 2025 and 2032, driven by rising demand for energy-efficient lighting, rapid advancements in miniaturized and high-density packaging technologies such as CSP and COB, and expanding adoption across smart lighting, automotive illumination, mini-LED displays, and industrial applications.

Supportive government regulations, increasing smart city investments, and growing penetration of LEDs in electric vehicles (EVs) and advanced display systems further reinforce long-term market momentum.

Key Industry Highlights:

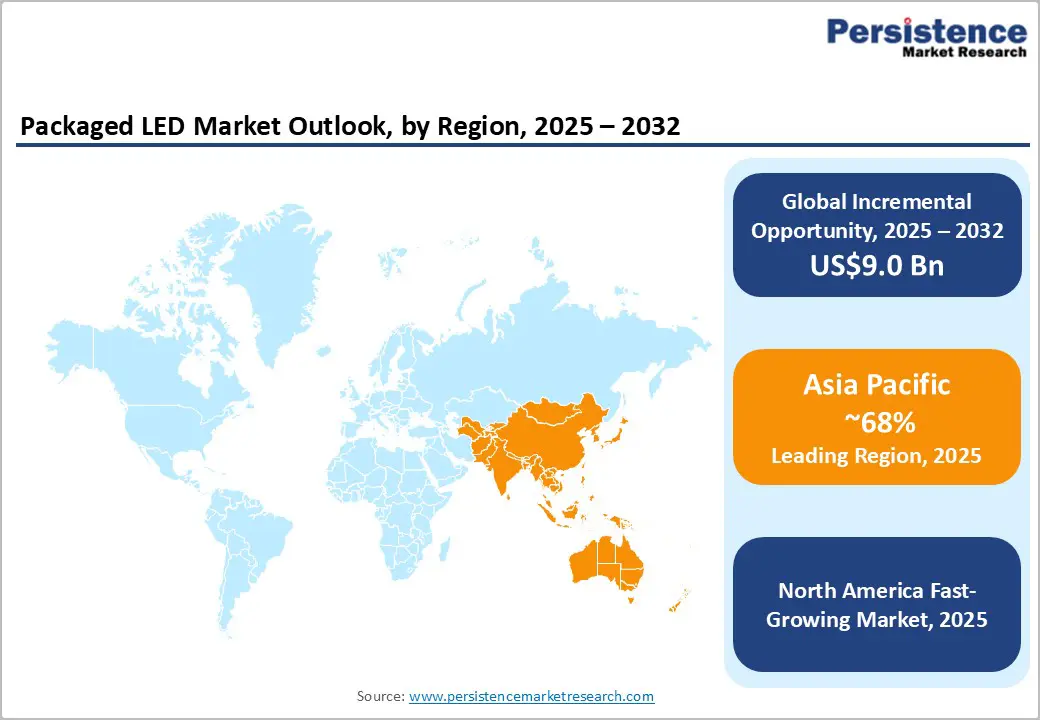

- Leading Region: Asia Pacific leads the market with around 68% share, driven by urbanization, manufacturing cost advantages, supportive energy-efficient policies, heavy investments across the electronics value chain, and strong clusters of vertically integrated, globally integrated OEM-ODM manufacturers.

- Fastest-Growing Region: North America is the fastest-growing region, driven by energy-efficient lighting regulations, strong R&D and smart-city investments, and a competitive landscape dominated by advanced technology providers and strategic partnerships.

- Leading Packaging Type: The surface-mount device (SMD) segment leads the packaging type segment, accounting for 50% of revenue, driven by its widespread use in displays, consumer electronics, and general lighting.

- Leading Power Range Type: Mid-power LEDs (0.5–1 W) lead the market with over 45% revenue share, driven by their cost-effectiveness and suitability for mainstream residential and commercial lighting.

- Leading Application Type: General lighting is the leading segment in the market with about 38% share, driven by regulatory support and broad adoption across developed and emerging regions.

| Key Insights | Details |

|---|---|

|

Packaged LED Market Size (2025E) |

US$17.8 Bn |

|

Market Value Forecast (2032F) |

US$26.8 Bn |

|

Projected Growth CAGR (2025-2032) |

6.0% |

|

Historical Market Growth (2019-2024) |

5.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Technology Advancements and Miniaturization

Technological advancements and ongoing miniaturization are driving market growth by enabling manufacturers to achieve higher performance, better thermal management, and greater design flexibility. Innovations such as chip-scale packages (CSP), flip-chip architectures, and advanced phosphor materials have improved lumen output, color stability, and energy efficiency. Developments in wafer-level packaging and substrate materials are reducing package sizes while enhancing reliability and lifespan, supporting higher current densities and more effective heat dissipation, making LEDs suitable for demanding industrial and automotive applications.

Miniaturization is also transforming end-user markets by enabling slimmer, lighter, and more energy-efficient devices. In displays, mini-LED and micro-LED technologies leverage ultra-small packaged LEDs to deliver exceptional brightness and contrast for TVs, laptops, and smartphones. In the automotive sector, compact, high-output modules support adaptive headlights, advanced interior lighting, and driver-assistance systems. Miniaturized LEDs are increasingly used in wearable electronics, medical devices, and sensing applications, where space efficiency and precise lighting are critical. These trends are expanding the addressable market for advanced packaged LED solutions.

Intense Pricing Pressure and Market Saturation

Intense pricing pressure and rising market saturation continue to challenge the packaged LED industry, especially as competition intensifies across major manufacturing hubs in the Asia Pacific. Rapid expansion of production capacity, particularly in China, has led to oversupply in recent years, driving down average selling prices for mid- and low-power LEDs. This has compressed profit margins and limited pricing flexibility, forcing many manufacturers to compete primarily on cost rather than technological differentiation. Smaller and mid-sized companies are particularly affected, struggling to maintain profitability while keeping pace with large-scale producers.

Market saturation further exacerbates these challenges, especially in mature applications such as general lighting, where LED adoption is already high in North America, Europe, and parts of Asia. The long lifespan of LEDs has lowered replacement demand, slowing volume growth in conventional lighting segments. This environment makes market entry more difficult for new players and intensifies commoditization, making products less distinguishable by performance alone. Many manufacturers are shifting focus toward higher-value segments, including automotive lighting, specialty LEDs, and smart lighting solutions, to counter growth limitations caused by saturation.

Smart Lighting and IoT Integration

Smart lighting and IoT integration represent a major growth opportunity for the market, as buildings, cities, and industrial facilities increasingly adopt connected illumination systems. The shift toward intelligent lighting, enabled by sensors, wireless connectivity, and automated controls, is driving demand for advanced LED packages with higher efficiency, better thermal management, and seamless integration with digital platforms. Government-led smart city initiatives and energy-efficiency regulations are further boosting adoption, particularly in street lighting, commercial buildings, and public infrastructure.

IoT-enabled LEDs are also creating opportunities in residential automation, retail spaces, warehouses, and industrial facilities. Features such as occupancy sensing, daylight harvesting, color tuning, and remote monitoring rely on compact, durable LED packages integrated with control electronics and communication modules. The growing use of AI-driven building management and predictive maintenance systems is increasing demand for LEDs capable of real-time data exchange and precise light control. These developments are expanding the role of packaged LEDs beyond basic illumination, positioning them as key components in connected and intelligent environments.

Category-wise Analysis

Packaging Type Insights

Surface-Mount Device (SMD) LEDs lead the market, accounting for approximately 50% of the revenue share in 2025. Their dominance stems from versatility, cost-effectiveness, and compatibility with high-volume manufacturing. SMD LEDs are widely used in displays, consumer electronics, residential lighting, and commercial illumination due to their compact size, efficient heat dissipation, and stable performance. For example, Samsung deploys SMD LEDs in high-resolution TVs, while Nichia uses them in residential panel lights. Growth in LED retrofits, displays, and energy-efficient lighting continues to reinforce SMD’s leading position, making it the preferred choice for mainstream applications.

Chip-On-Board (COB) LEDs represent the fastest-growing product type, driven by demand for high-density, high-output modules. COB packaging is increasingly used in industrial lighting, automotive headlights, and high-lumen applications, thanks to superior thermal management and uniform light output. For instance, Cree’s COB modules power warehouse high-bays, and Dialight integrates COB LEDs into industrial floodlights. Chip-Scale Package (CSP) technology is also advancing rapidly, finding applications in automotive signaling, mini-LED backlighting, and compact devices due to its small footprint and high power efficiency.

Power Range Type Insights

Mid-power LEDs (0.5–1 W) lead the market, capturing over 45% of the revenue share in 2025, owing to their optimal balance of cost, brightness, and efficiency for mainstream residential and commercial lighting. They are widely used in retrofit downlights, panel lighting, and general illumination, offering strong performance without the higher heat output or complexity of more powerful LEDs. For example, Cree’s mid-power LEDs are commonly deployed in residential downlight retrofits. Their widespread adoption is further supported by energy-efficiency regulations and the growing economic benefits of LED upgrades in commercial buildings.

High-power LEDs (1 W and above) represent the fastest-growing segment, driven by rising demand in automotive, industrial, and outdoor applications. In automotive lighting, these LEDs power adaptive headlights, signal lights, and high-beam modules, benefiting from higher luminous flux and robust thermal performance. For instance, Osram’s high-power LEDs are used in EV headlamps, while Lumileds’ modules are integrated into automotive DRLs. Industrial and outdoor applications, such as street lighting, floodlights, and high-bay fixtures, are also increasingly adopting high-power LEDs to achieve brighter illumination and longer lifespans.

Application Type Insights

General lighting is the leading application segment, accounting for 38% of the revenue share in 2025, driven by strict energy-efficiency regulations, large-scale retrofit initiatives, and widespread adoption of LED solutions across both mature and emerging markets. Residential, commercial, and industrial facilities are increasingly replacing legacy lighting with LED systems to reduce energy use and operational costs. For example, Philips’ LED panel lights are widely deployed in offices and commercial buildings. Continued improvements in brightness, thermal management, and declining LED prices further reinforce general lighting as a primary market driver.

Automotive lighting is the fastest-growing application segment, fueled by the expansion of advanced driver-assistance systems (ADAS) and the transition to LED-based headlamps, DRLs, and interior ambient lighting. Miniaturization and high-power efficiency are also driving adoption in EVs; for instance, Lumileds’ modules are used for interior cabin lighting. Digital signage and display applications, including mini-LED and outdoor advertising panels, are growing rapidly due to smart city initiatives, the increasing adoption of large-format displays, and rising demand for high-brightness, durable lighting solutions.

Regional Insights

North America Packaged LED Market Trends

North America is the fastest-growing region, driven by the rapid adoption of advanced lighting technologies and strong energy-efficiency policies. Growth is supported by accelerated LED retrofit programs, stricter building codes, and widespread replacement of legacy halogen and fluorescent systems in commercial, residential, and industrial environments. Increased investments in manufacturing and R&D are further establishing the region as an innovation hub. Partnerships between lighting OEMs and technology companies are enhancing smart lighting solutions, while government incentives for energy-efficient upgrades continue to drive adoption across both public and private sectors.

The region’s expansion is also fueled by strong uptake of smart lighting, connected controls, and IoT-enabled luminaires, particularly in corporate campuses, warehouses, smart homes, and municipal infrastructure. Automotive LED packages, especially for EVs, are seeing double-digit growth, supported by advanced headlamp technologies and stricter safety regulations. Rising demand for high-brightness LEDs in digital signage, outdoor displays, sports arenas, and entertainment venues further sustains momentum. The increasing adoption of AI-driven building management and predictive maintenance systems is creating added demand for high-performance LED packages.

Europe Packaged LED Market Trends

Europe continues to be a key market for packaged LEDs, driven by stringent energy-efficiency regulations, sustainability mandates, and widespread adoption across residential, commercial, and industrial sectors. EU directives such as Eco-design and RoHS are accelerating the transition from legacy lighting to advanced LED packages, supporting strong demand for SMD, COB, and CSP technologies. The region also benefits from robust automotive manufacturing, particularly in Germany and Eastern Europe, which is driving rapid adoption of advanced LED lighting. Government-led retrofit programs and incentives for energy-efficient lighting upgrades are further boosting demand in commercial and public infrastructure, while ongoing R&D investments enhance LED performance and reliability across applications.

Europe’s packaged LED market is also shaped by growing demand for miniaturized, high-density LED solutions, expanding smart city projects, and wider deployment of digital signage and architectural lighting. Emerging applications in UV-LED, medical lighting, and horticulture are supporting diversification across the value chain. Despite pricing pressure from low-cost Asian competitors, European manufacturers are emphasizing innovation, quality, and sustainable materials to maintain leadership and comply with tightening regulations. The adoption of connected lighting systems and IoT-enabled solutions in urban infrastructure, along with advanced display applications, is driving growth in high-brightness and specialized LED packages.

Asia Pacific Packaged LED Market Trends

Asia Pacific leads the global packaged LED market, accounting for 68% market share, supported by its strong manufacturing base and significant investments in urbanization and smart-city lighting initiatives. Home to major LED producers such as China, Japan, South Korea, and Taiwan, the region benefits from large-scale production, cost advantages, and robust government support for energy-efficient lighting. For instance, Samsung Electronics in South Korea and Nichia in Japan are heavily investing in high-density SMD and CSP LED packages.

The region is experiencing rapid growth across general lighting as well as advanced applications, including mini-LED displays, automotive lighting, and industrial illumination. Adoption of smart lighting is particularly strong, driven by government energy-efficiency mandates and infrastructure development in countries such as China and India. At the same time, pricing pressure and intense competition are challenges for manufacturers, prompting them to focus on innovation, improved thermal management, and sustainable materials to differentiate their products.

Competitive Landscape

The global packaged LED market exhibits a moderately fragmented structure, driven by a mix of large, well-capitalized incumbents and numerous regional specialists serving niche applications. Market share is led by a few tech-strong firms, while numerous regional OSATs and specialists maintain competitive pricing and localized supply. With key leaders including Nichia, ams-OSRAM, Samsung Electronics, Lumileds, and Seoul Semiconductor, these firms combine deep IP, global sales channels, and broad product portfolios that span SMD, COB, CSP, and specialty UV/IR packages.

These players compete through rapid product innovation, scale manufacturing, and ecosystem partnerships: they invest heavily in R&D for higher-efficacy dies, advanced phosphors, wafer-level and flip-chip packaging, and thermal management to win automotive, display, and industrial contracts. At the same time, margin pressure from APAC volume producers forces differentiation via value-added services.

Key Industry Developments:

- In May 2025, Luminus Devices launched the CFT-50X Series, a high-performance LED product line for medical, life sciences, and industrial applications. The series features 10 SKUs spanning UVA (405 nm) to Red (638 nm), tailored for medical endoscopy, fluorescence microscopy, biophotonic research, and machine vision. Designed for long-term reliability exceeding 10 years, the LEDs offer wide wavelength selection, optimized coupling for fiber optics, high-drive-current operation, and robust thermal management with automotive-grade connectors.

- In January 2025, Hisense unveiled its first consumer-ready MicroLED TV, the 136MX, at CES in Las Vegas. Featuring a high-density array of over 24.88 million microscopic LEDs, each pixel acts as its own light source with independent red, green, and blue LEDs, eliminating the need for a traditional backlight. The self-emissive design delivers near-infinite contrast, deep blacks, high brightness, and precise colors, offering long-lasting, burn-in-free performance ideal for home theaters and bright living spaces.

Companies Covered in Packaged LED Market

- Nichia Corporation

- OSRAM Opto Semiconductors

- Lumileds Holding B.V.

- Signify Holding

- Samsung Electronics

- Seoul Semiconductor Co. Ltd.

- Cree LED (Smart Global Holdings)

- Lextar Electronics Corporation

- Bolb Inc.

Frequently Asked Questions

The global packaged LED market is valued at US$17.8 billion in 2025 and expected to reach US$26.8 billion by 2032, reflecting robust growth.

Key demand drivers for the packaged LED market include government regulations promoting energy-efficient lighting, advancements in miniaturization that enable new automotive and display applications, and the growing adoption of smart, connected, and IoT-enabled lighting systems.

General lighting is the dominant application segment in the packaged LED market, accounting for approximately 38% of revenue, fueled by supportive regulations and widespread adoption across both developed and emerging markets.

Asia Pacific dominates, capturing over 68% driven by urbanization, manufacturing cost advantages, supportive energy-efficient policies, heavy investments across the electronics value chain, and strong clusters of vertically integrated, globally integrated OEM-ODM manufacturers.

A major growth opportunity in the market lies in the integration of smart lighting and IoT-enabled controls within buildings and infrastructure, driven by urban modernization initiatives and significant investment in connected lighting solutions.