- Biotechnology

- Oligonucleotide Synthesis Market

Oligonucleotide Synthesis Market Size, Share, and Growth Forecast, 2025 - 2032

Oligonucleotide Synthesis Market By Product (Oligonucleotides, Reagents & Consumables, Equipment/Synthesizers), Oligonucleotide Type (Custom Oligonucleotides, Predesigned Oligonucleotides), Application, End-user, and Regional Analysis for 2025 - 2032

Oligonucleotide Synthesis Market Size and Trends Analysis

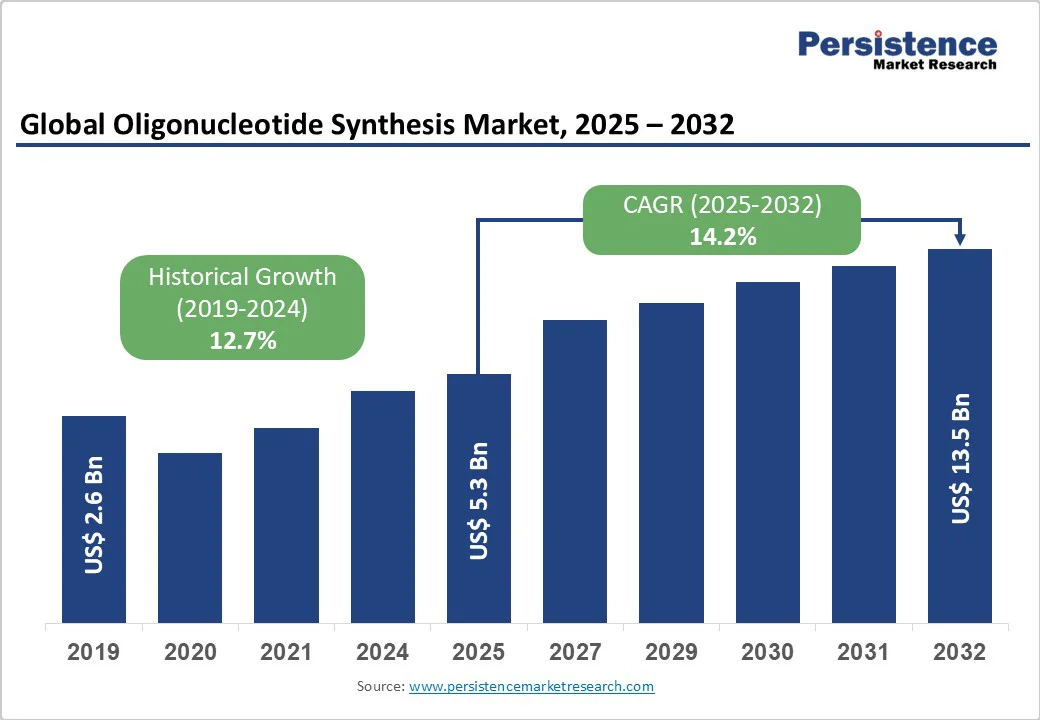

The global oligonucleotide synthesis market size is likely to be valued at US$5.3 Billion in 2025 and is expected to reach US$13.5 Billion by 2032, growing at a CAGR of 14.2% during the forecast period from 2025 to 2032, driven by its applications across research, diagnostics, forensics, and therapeutics. In medicine, antisense oligonucleotides (ASOs), typically 20–30 nucleotides in length, facilitate gene silencing by targeting and inhibiting specific RNA sequences, thereby preventing the production of harmful or overactive proteins. The rising interest in synthetic nucleotides is fueling the development of DNA- and RNA-based vaccines, highlighting their growing significance in next-generation therapeutic strategies.

Key Industry Highlights

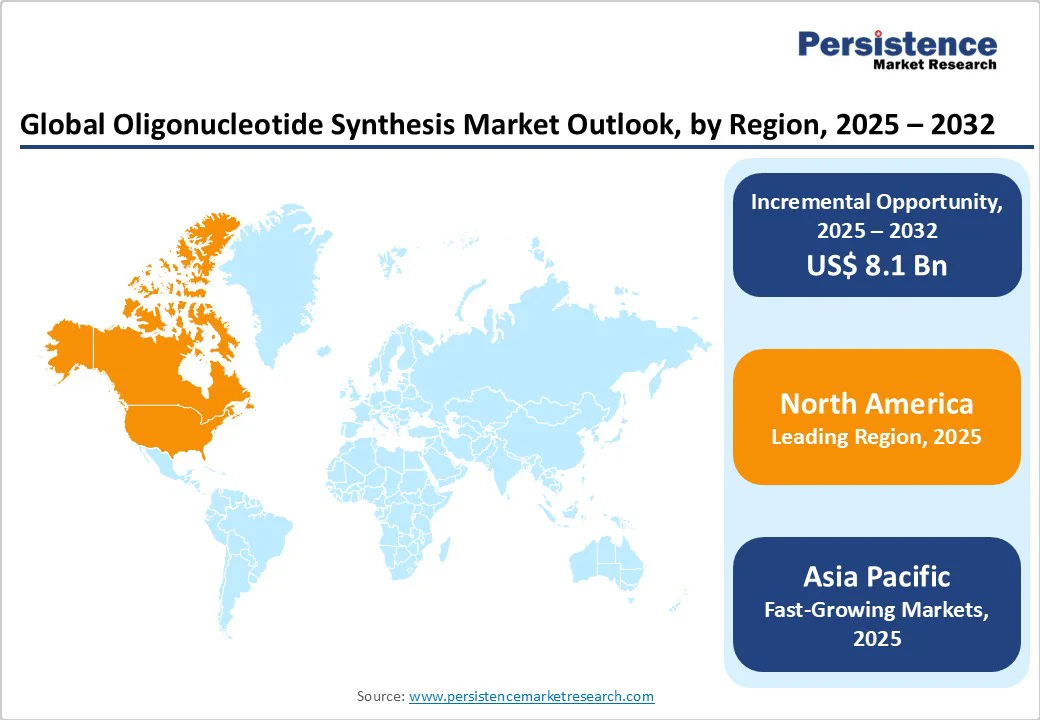

- Leading Region: North America is projected to lead the global market with over 40% value share in 2025, driven by high demand for therapeutic oligos, established GMP manufacturing facilities, and strong regulatory support for clinical development and commercialization.

- Fastest-growing Region: Asia Pacific is the fastest-growing market, fueled by expanding contract research and manufacturing organizations (CRDOs/CDMOs), increasing investment in oligonucleotide R&D, and rising adoption of RNA- and DNA-based therapeutics.

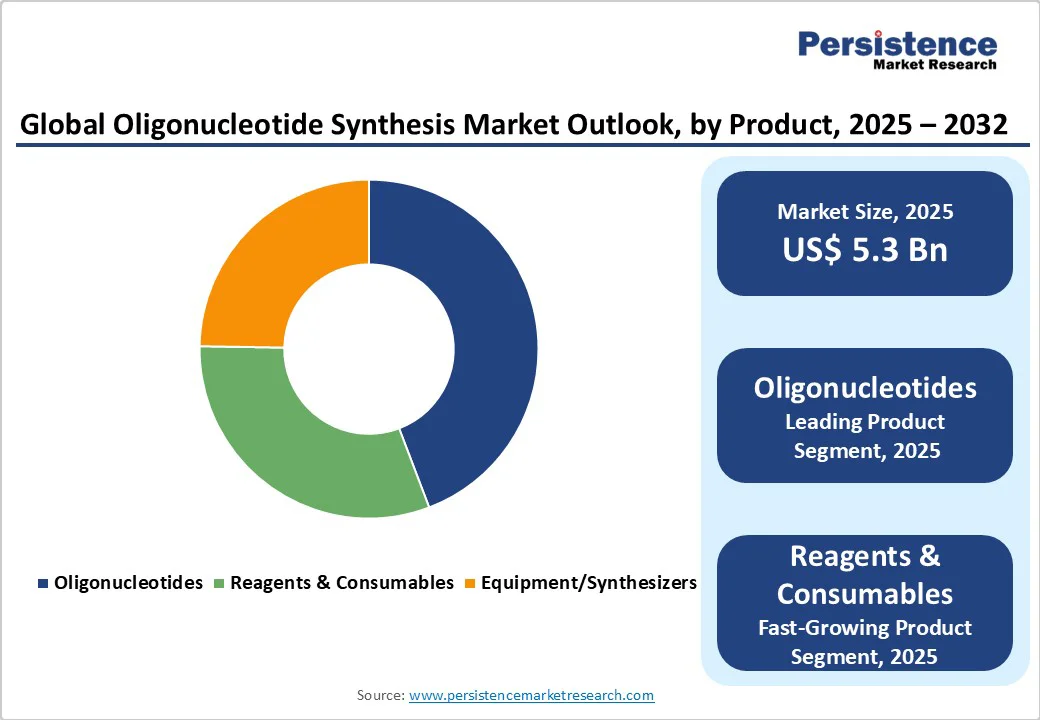

- Leading Product: Oligonucleotides are the primary revenue-generating segment, encompassing custom- and therapeutic-grade oligos for research, diagnostics, and therapeutic applications.

- Leading Oligonucleotide Type: Custom-synthesized oligonucleotides dominate due to widespread use in research, diagnostics, and therapeutics.

- Opportunities: Companies are scaling production, employing flexible synthesis capacities, and leveraging dedicated R&D labs to enhance next-generation oligonucleotide synthesis and process efficiency.

| Key Insights | Details |

|---|---|

|

Oligonucleotide Synthesis Market Size (2025E) |

US$5.3 Bn |

|

Market Value Forecast (2032F) |

US$13.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

14.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

12.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expanding Therapeutic Pipelines, Regulatory Approvals, and Investments

The market is witnessing strong momentum, driven by the expanding pipeline of therapeutic candidates, increasing regulatory approvals, and rising investments in next-generation platforms. 20 oligonucleotide-based drugs have received global approvals as of March 2025, with several others in clinical and preclinical development, highlighting the therapeutic promise of the modality.

Recent financing rounds underscore investor confidence, such as AusperBio, which secured US$73 Million in Series B funding (December 2024) to advance its lead antisense oligonucleotide AHB-137 for chronic hepatitis B, supporting both China-based and global Phase 2 studies alongside commercial-scale manufacturing and pipeline expansion.

Judo Bio emerged in October 2024 with US$100 Million in seed and Series A funding to progress kidney-targeted oligonucleotide medicines, leveraging its STRIKE (Selectively Targeting RNA Into Kidney) platform to overcome delivery challenges. These developments, coupled with innovative applications in molecular diagnostics, DNA data storage, and programmable biological systems, position oligonucleotide synthesis as a cornerstone of modern biotechnology growth.

Technological, Process, and Cost Challenges

Despite its transformative potential, the market faces significant restraints linked to technological, process, and cost-related challenges. The industry standard, phosphoramidite-based solid-phase synthesis, while efficient for short sequences, struggles with declining yields for longer constructs, high error rates, and dependence on toxic solvents.

Typical siRNA (small interfering RNA) production, for instance, requires over 160 steps, consumes nearly five tons of raw material per kilogram of API (active pharmaceutical ingredient), and still delivers only ~90% purity, driving API costs above US$1 Million/kg.

Alternative approaches, such as enzymatic synthesis, promise higher selectivity but remain limited by template dependence, incompatibility with chemically modified nucleotides, and high error rates, as seen in a recent study reporting 9.9% deletions of nucleotides. Solution-phase and array-based methods face purification, yield, and scalability issues. These barriers, coupled with challenges in purification, stability, and delivery of antisense oligonucleotides, hinder large-scale commercialization and limit adoption beyond rare disease applications, restraining broader market expansion.

Automation, Scalability, and Expanding Therapeutic Applications

The market presents strong opportunities, underpinned by automation, digital integration, and expanding therapeutic demand. Automated synthesis platforms equipped with inline process analytical technologies (PAT) ensure reproducibility, mitigate manual risks, and enable consistent control over critical process parameters. This shift supports large-scale manufacturing by enhancing efficiency, reducing errors, and creating structured datasets that accelerate regulatory compliance and process optimization.

Advances in reactor design, solid-phase supports, and hybrid batch–solution workflows are also streamlining scalability and improving yields. Beyond technology, the rising adoption of oligonucleotides in PCR (polymerase chain reaction), sequencing, gene editing, vaccines, and targeted therapies is creating substantial commercial opportunities.

Antisense oligonucleotides, RNA therapeutics, and siRNAs are moving from rare disease applications toward broader indications, driving the need for higher-volume, cost-effective production. Together, automation-driven precision, process scalability, and growing therapeutic pipelines position oligonucleotide synthesis as a critical growth frontier in modern biotechnology.

Category-wise Analysis

Product Insights

Oligonucleotides are expected to retain the prominent share of the market in 2025, accounting for 45.7%. Their dominance is driven by widespread adoption across therapeutics, diagnostics, and research applications. These short DNA or RNA sequences are critical in gene expression modulation, RNA interference, and molecular diagnostics. The increasing prevalence of genetic disorders, demand for regenerative medicine, and advancements in nucleic acid technologies are fueling consistent growth, making oligonucleotides an essential component of modern biomedical research and drug development.

Oligonucleotide Type Insights

Custom oligonucleotides are projected to remain the leading segment, capturing 58.2% of the global market in 2025. Tailored to specific research and therapeutic needs, these sequences enable precision applications such as gene editing, molecular diagnostics, and RNA therapeutics.

Rising demand for personalized medicine, increasing biotechnology R&D, and the expansion of academic and industrial collaborations are key factors supporting this growth. The flexibility, accuracy, and high-quality synthesis offered by custom oligonucleotides make them indispensable for advanced biomedical and pharmaceutical applications.

Application Insights

Therapeutic oligonucleotides are expected to maintain a leading share of 42.8% in 2025. These drugs modulate gene expression to treat previously untreatable diseases, with the first FDA-approved oligonucleotide therapy emerging in 2017. By 2020, ten more oligonucleotide-based drugs gained regulatory approval, reaching 20 by March 2024, and numerous candidates are in the pipeline.

Growing clinical acceptance, expanding indications across rare and genetic disorders, and advancements in delivery mechanisms are driving adoption. Increasing investments in oligonucleotide therapeutics further support robust growth and market leadership within the market.

Regional Insights

North America Oligonucleotide Synthesis Market Trends

North America represents the prominent regional opportunity for the market, projected to capture 42.1% of the global share by 2025. The region benefits from strong regulatory support, advanced R&D infrastructure, and pioneering initiatives in personalized medicine. A key example is the N=1 Collaborative (N1C), which unites academia, industry, patients, and regulators to accelerate customized gene-targeting therapies. Initially focused on antisense oligonucleotides (ASOs) for ultra-rare neurodegenerative diseases, N1C is shaping frameworks that could extend to broader therapeutic modalities.

The U.S. is also leading in individualized ASO (antisense oligonucleotide) treatments, with most clinical programs currently active there. The U.S. Food and Drug Administration’s (FDA) clear regulatory pathway, including investigational new drug (IND) applications and draft guidance for noncommercial ASO development, further supports rapid innovation. These efforts not only strengthen North America’s dominance in rare disease therapeutics but also provide critical insights into dosing, safety, and efficacy, ultimately positioning the region as a hub for the next-generation oligonucleotide-based therapies and large-scale synthesis demand.

Europe Oligonucleotide Synthesis Market Trends

Europe stands as a pivotal region in the global market, expected to capture nearly 28.8% of the global share by 2025. The region is strongly positioned due to its collaborative research culture, advanced funding frameworks, and emphasis on translational science. A key initiative is ON-TRACT (OligoNucleotide Technologies for Rapid Advancement of Cancer Therapies), which brings together 10 academic groups, 4 companies, 1 hospital, and 1 non-profit to accelerate oligonucleotide-based treatments for lung cancer, B-cell malignancies, and chronic inflammation. By integrating medicinal chemistry, biology, and advanced delivery platforms, the consortium seeks to overcome barriers such as poor stability, inefficient delivery, and off-target effects to enable safer and more effective oligonucleotide therapies.

Europe also leads in academically driven precision medicine initiatives, such as the 1 Mutation 1 Medicine (1M1M) platform, which fosters regulatory dialogue to advance antisense oligonucleotide (ASO) treatments for rare diseases. Coupled with the continent’s strong focus on sustainability, ethical testing, and frameworks for interdisciplinary innovation, Europe is building a fertile ecosystem for oligonucleotide therapies that will drive demand for scalable synthesis technologies and broaden therapeutic applications.

Asia Pacific Oligonucleotide Synthesis Market Trends

The Asia Pacific market is witnessing rapid growth with a CAGR of 17.8%, driven by investments in advanced manufacturing, expanding R&D capabilities, and increasing adoption of nucleic acid therapeutics. In April 2024, Asahi Kasei Bioprocess (AKB) and Axolabs announced a strategic partnership to establish a 59,000 sq. ft. cGMP oligonucleotide manufacturing facility, aiming to accelerate the development and commercialization of oligo-based therapies. In 2024, Biolytic Lab Performance joined the International Gene Synthesis Consortium (IGSC), reinforcing its commitment to ethical and safe practices in synthetic biology.

More recently, in August 2025, Hongene Biotech Corporation, a CDMO specializing in nucleic acid therapeutics, entered a non-exclusive licensing agreement with UMass Chan Medical School to produce extended nucleic acid (exNA) monomers and exNA-modified oligonucleotides for research, enhancing RNA interference (RNAi), ASO, and CRISPR (Clustered Regularly Interspaced Short Palindromic Repeats) applications. These initiatives demonstrate Asia Pacific’s emergence as a hub for high-quality, scalable oligonucleotide manufacturing, innovative RNA chemistry, and advanced therapeutic development, positioning the region as a key driver of growth in the global market.

Competitive Landscape

The global oligonucleotide synthesis market is competitive and evolving, with key players expanding manufacturing capacities, investing in automated and high-throughput platforms, pursuing strategic partnerships, and acquiring specialized biotech firms to enhance capabilities across therapeutic, diagnostic, and research applications worldwide.

Key Industry Developments

- In May 2025, Oligo Factory launched low-scale oligo synthesis, expanding support for therapeutic and diagnostic development, including discovery, preclinical, and toxicology studies, and will showcase its FactorTx™ portfolio at TIDES USA, May 19–22 in San Diego.

- In December 2024, Codexis completed construction of its ECO Synthesis Innovation Lab to produce GLP-grade oligonucleotides for preclinical studies, with the facility opening in 2025 to advance enzymatic oligonucleotide manufacturing.

- In October 2024, Synoligo Biotechnologies expanded with a new 5,000 sq. ft. high-throughput oligonucleotide synthesis facility, boosting service capacity for therapeutic and diagnostic applications and supporting rapid growth since its founding in 2022.

- In June 2024, GSK acquired San Diego-based Elsie Biotechnologies for up to $50 million to integrate oligonucleotide discovery, synthesis, and delivery technologies, strengthening its therapeutic platform and accelerating pipeline development.

Companies Covered in Oligonucleotide Synthesis Market

- Integrated DNA Technologies, Inc.

- GenScript Biotech Corporation

- Eurofins Scientific SE

- Bioneer Corporation

- Kaneka Corporation (Eurogentec)

- Biolegio B.V.

- Eton Bioscience, Inc.

- IBA GmbH

- Quintara Biosciences

- LGC Biosearch Technologies

- Thermo Fisher Scientific, Inc.

- TriLink BioTechnologies, LLC

- TAG Copenhagen A/S

- PolyGen GmbH

- General Electric Co.

- BioAutomation

- Biolytic Lab Performance Inc.

- Others.

Frequently Asked Questions

The oligonucleotide synthesis market size is projected to be valued at US$5.3 Billion in 2025.

The rising demand for oligonucleotide-based therapeutics, diagnostics, and gene-editing applications, coupled with increasing R&D investments and technological advancements, drives market growth.

The oligonucleotide synthesis market is poised to witness a CAGR of 14.2% between 2025 and 2032.

Expansion of automated synthesis, scalable manufacturing, and personalized medicine initiatives presents significant growth opportunities worldwide.

Major players in the oligonucleotide synthesis market include Merck KGaA, FUJIFILM Wako Pure Chemical Corporation, Thermo Fisher Scientific, Inc., Syngene International Limited, and DH Life Sciences, LLC.