- Marine

- Offshore Support Vessel Services Market

Offshore Support Vessel Services Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Offshore Support Vessel Services Market by Product (Platform Supply Vessel (PSV), Multirole field & ROV Supply Vessel (MRSV), Offshore Subsea Construction Vessel (OSCV), Anchor Handling Tig Supply Vessel (AHTS), Emergency Response and Rescue Vessel (ERRSV), Chase & Seismic Vessel, Standby Crew Vessels and Others), Application, End-user, and Regional Analysis for 2025 - 2032

Offshore Support Vessel Services Market Size and Trends Analysis

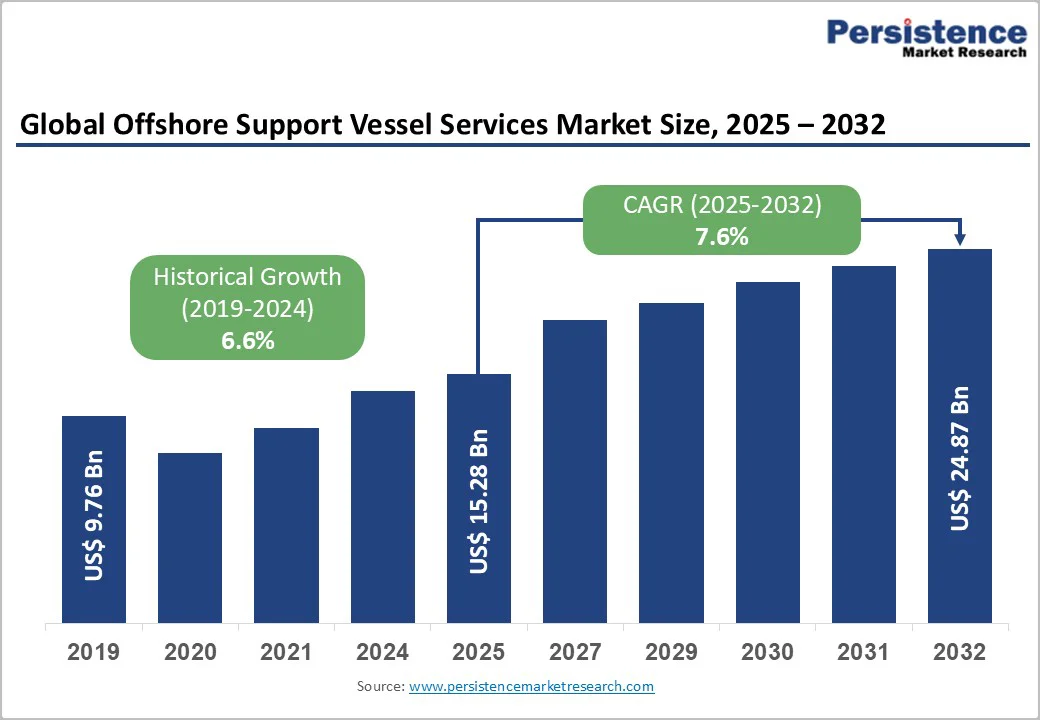

The global offshore support vessel services market size is valued at US$15.28 billion in 2025 and is projected to reach US$24.87 billion, growing at a CAGR of 7.6% between 2025 and 2032.

The market's expansion is fundamentally driven by deepwater and ultra-deepwater oil and gas exploration, particularly in the Gulf of Mexico, the North Sea, and Asia-Pacific, as well as by substantial government investments in offshore wind energy infrastructure.

Key Industry Highlights:

- Vessel Type Leadership: Platform Supply Vessels (PSVs) dominate the market with an estimated 60% share (US$1.93 billion), driven by their essential role in transporting equipment, cargo, and personnel to offshore platforms. Anchor Handling Tug Supply (AHTS) Vessels represent the fastest-growing segment, supported by increasing deepwater exploration activities and demand for high-performance positioning and towing capabilities in challenging marine environments.

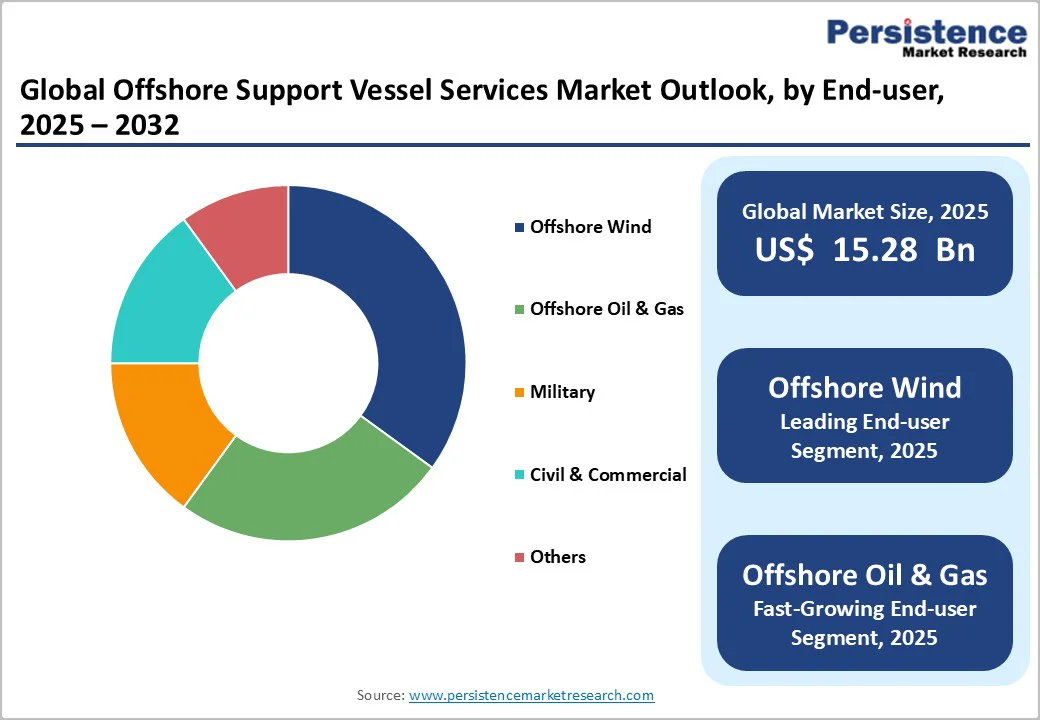

- End-User Market Dynamics: The Offshore Wind Oil & Gas sector maintains established market leadership through sustained exploration, drilling, and production operations, while the Offshore Oil & Gas segment emerges as the fastest-growing category, projected to expand its share by 32.2%, fueled by global energy transition efforts and large-scale offshore wind farm installations.

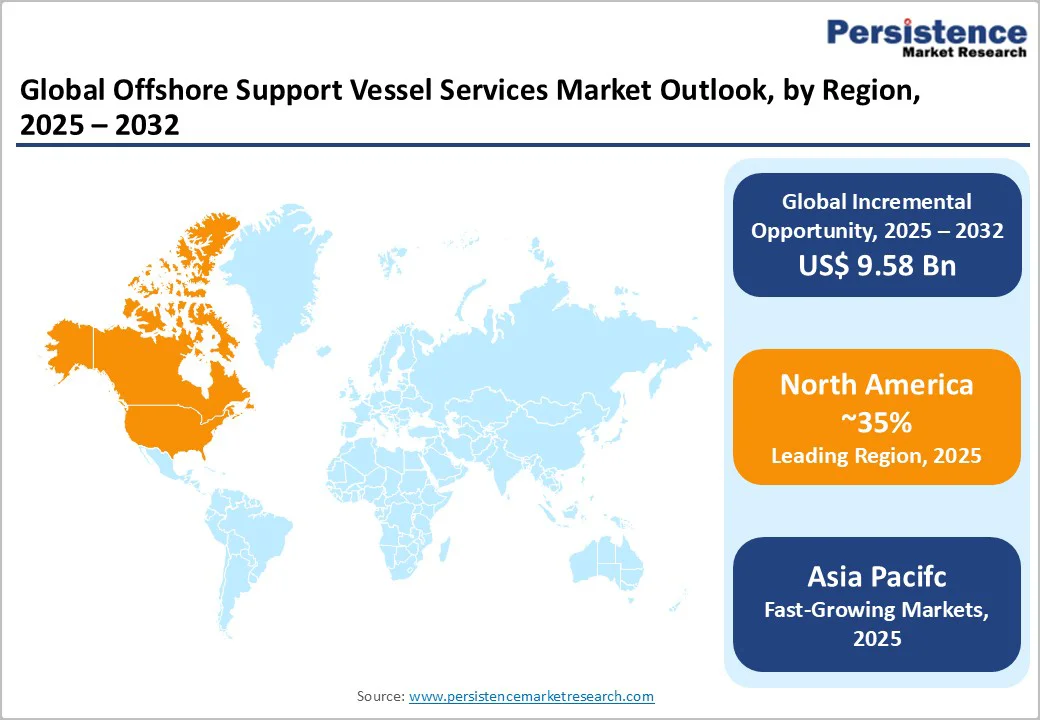

- Regional Growth Patterns: North America leads the market with a 35% share, driven by steady offshore oil production and Gulf of Mexico operations. Asia-Pacific is set to record the fastest growth at 7.5% CAGR, propelled by China’s deepwater exploration investments and India’s offshore field development initiatives, alongside regional policy support for renewable energy deployment.

- Technology Evolution: The industry is witnessing a shift toward hybrid-electric propulsion systems, dynamic positioning (DP) integration, and autonomous navigation technologies that enhance efficiency and safety. Compliance with IMO 2020 sulfur cap and EPA Tier 4 emission standards is accelerating fleet modernization and investments in cleaner propulsion solutions.

- Strategic Market Developments: Leading players such as Tidewater Inc. and Edison Chouest Offshore are expanding their fleets with dual-fuel, hybrid, and renewable-energy-capable vessels, signaling a strategic move toward sustainable offshore operations. Regional operators are aligning with the offshore wind transition, balancing new energy opportunities with the continued reliability of oil and gas services.

| Key Insights | Details |

|---|---|

| Offshore Support Vessel Services Market Size (2025E) | US$15.28 Bn |

| Market Value Forecast (2032F) | US$24.87 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.6% |

Market Dynamics

Expansion of Offshore Renewable Energy Infrastructure and Wind Farm Development

The offshore support vessel services market is experiencing substantial growth, driven by global offshore wind energy capacity targets, establishing significant infrastructure investment requirements. Europe targets 120 GW of installed offshore wind capacity by 2030 and 300 GW by 2050, requiring specialized vessels for turbine installation, maintenance, and cable-laying operations.

The United States Department of Energy aims to achieve 30 GW of offshore wind capacity by 2030, with states like New Jersey and New York leading the pipeline. Approximately 18% of the global OSV fleet is currently dedicated to offshore wind support, a proportion that is expanding rapidly as renewable energy projects accelerate globally.

The North Sea and Baltic Sea regions represent primary hubs for offshore wind development, driving substantial demand for Service Operation Vessels (SOVs) and crew transfer vessels capable of offshore accommodation and advanced positioning. This renewable energy transition creates significant market opportunities for specialized OSV operators possessing advanced vessel capabilities.

Increasing Deepwater and Ultra-Deepwater Oil and Gas Exploration

Global offshore oil and gas exploration expansion, particularly in ultra-deepwater environments, continues to generate substantial demand for advanced support vessels despite energy transition pressures.

India's oil minister announced potential investments of $100 billion in oil and gas exploration during the Urja Varta conference in July 2024, emphasizing plans to increase sedimentary basin exploration from 10% to 16% by year-end 2024. The Gulf of Mexico remains a critical production hub, with expectations of 2.3 million barrels per day in 2024, a 13% increase from 2022.

The United States Energy Information Administration predicts continued expansion of offshore oil and gas output, sustaining demand for traditional platform supply vessels and anchor-handling tug supply vessels.

China's offshore oil and gas operations in the South China Sea, combined with the discovery of 100+ million ton oil reserves in the Pearl River Delta, create substantial OSV deployment requirements. These deepwater activities require specialized, high-specification vessels equipped with advanced technology, sustaining premium pricing and stable cash flows for operators.

Restraints - Volatile Commodity Prices and Economic Uncertainties

Fluctuating oil and natural gas prices create demand volatility and limit capital investment in offshore exploration and production, thereby constraining OSV deployment requirements. High operational costs, including fuel expenses, crew management, and maintenance, compound profitability pressures during commodity price downturns.

Uncertain economic conditions reduce corporate investment in deepwater exploration projects, directly limiting OSV utilization rates and revenue generation capacity. These cyclical market dynamics create risk factors restraining long-term growth projections and financial stability for OSV operators.

Stringent Environmental Regulations and Compliance Costs

Increasingly stringent environmental regulations requiring emissions reduction, , and pollution control impose substantial compliance costs on OSV operators.

Vessel retrofitting to meet modern environmental standards requires significant capital investments, and some older vessels may face economically unviable upgrade requirements. Global sustainability imperatives and regulatory pressures restrict operations in certain environmentally sensitive waterways, limiting service deployment opportunities.

Opportunity - Specialized Vessel Development for Emerging Applications

Offshore subsea cable installation, particularly for renewable energy transmission, represents an emerging market opportunity distinct from traditional oil and gas and wind farm support applications. Dynamic positioning vessels with specialized cable-laying equipment represent an underserved market segment with substantial growth potential.

Offshore aquaculture infrastructure development and deepwater mining exploration activities create emerging vessel application opportunities requiring specialized support services. Companies developing versatile, adaptable OSV platforms capable of supporting diverse offshore activities position themselves for sustained revenue growth across multiple market segments.

Digital Transformation and Autonomous Vessel Technology Integration

Advancing automation, digitalization, and autonomous operational systems represent substantial market opportunities for OSV operators investing in cutting-edge technologies. Remote operations and AI-driven optimization systems reduce crew requirements while enhancing safety and operational efficiency, creating premium service value propositions.

Integration of advanced data management systems, predictive maintenance algorithms, and real-time operational monitoring enables predictive servicing and reduced downtime. Companies leveraging digital transformation and autonomous technologies establish competitive differentiation, particularly in price-sensitive markets where operational efficiency determines contract awards.

Category-wise Analysis

Vessel Type Insights

Platform Supply Vessels (PSVs) dominate the offshore support vessel services market with a 60% share (US$1.93 billion in 2025), serving as the backbone of offshore logistics. Their large cargo capacity and versatility make them essential for transporting supplies, equipment, and personnel across oil, gas, and offshore wind operations.

Technological advancements such as enhanced dynamic positioning and automated cargo handling continue to strengthen their market leadership. Meanwhile, Anchor Handling Tug Supply (AHTS) vessels represent the fastest-growing category, driven by rising deepwater and ultra-deepwater exploration.

Equipped for anchor handling, towing, firefighting, and emergency response, these high-capability vessels meet the increasing demand for reliable, multifunctional support in complex offshore and renewable energy installations.

Application Insights

Logistics and cargo management services dominate the offshore support vessel (OSV) services market, serving as the foundation for all offshore operations. These services encompass supply delivery, equipment transport, waste removal, and personnel logistics, ensuring the uninterrupted operation of offshore platforms. Their universal applicability across oil, gas, and renewable operations ensures stable revenue generation and consistent demand for OSV operators.

In contrast, offshore installation support services represent the fastest-growing application segment, driven by rapid offshore wind farm construction, subsea cable installation, and deepwater infrastructure expansion. Specialized OSVs equipped with dynamic positioning, heavy-lift systems, and construction support equipment are vital for turbine installation, foundation placement, and cable laying.

End-User Insights

The offshore oil and gas segment remains the largest end-user of offshore support vessel (OSV) services, driven by ongoing exploration and production activities across regions such as the Gulf of Mexico, the North Sea, and the South China Sea. Continuous development of deepwater and ultra-deepwater projects ensures stable, long-term contracts for OSV operators supporting logistics, maintenance, and rig operations in mature and new fields.

The offshore wind segment is the fastest-growing end-user category, projected to expand its market share by 32.2%, fueled by global renewable energy targets and large-scale infrastructure investments. Europe’s 120 GW offshore wind target by 2030 and the U.S. pipeline for 30 GW of capacity are driving demand for specialized service operation vessels (SOVs) for installation, maintenance, and crew transfer, reflecting strong energy transition momentum worldwide.

Regional Market Insights

North America Offshore Support Vessel Services Market Trends

North America accounts for 30-35% of the global offshore support vessel (OSV) services market, with the United States leading regional demand. Valued at USD 2.43 billion in 2022, the U.S. market is projected to grow at a 7.7% CAGR through 2030, supported by strong offshore oil and gas activity in the Gulf of Mexico, which hosts 55% of the national OSV fleet and 218 marine service facilities.

The region benefits from mature infrastructure, advanced maritime logistics, and favorable regulatory frameworks.

The U.S. offshore wind sector, targeting 30 GW capacity by 2030, is driving new OSV deployment for installation, maintenance, and logistics. Northeast coastal states lead development with programs targeting over 112 GW of capacity by 2050, creating premium opportunities for specialized wind-support vessels. U.S.

Europe Offshore Support Vessel Services Market Trends

Renewable Energy Leadership and North Sea Operations

Europe accounts for 20-25% of the global offshore support vessel (OSV) services market, driven by offshore wind expansion and North Sea oil and gas activities. The regional market is projected to reach EUR 11.90 billion by 2033, growing at a 5.68% CAGR.

Norway leads with the most advanced offshore fleet, supported by strong maritime infrastructure and sustained oil and gas production. The UK, Germany, and Denmark are driving rapid offshore wind development, creating rising demand for specialized OSVs for installation and maintenance.

The European Union’s regulatory frameworks, focused on environmental protection, safety, and emissions reduction, encourage fleet modernization and the adoption of hybrid-electric vessels. Mature operational hubs in the North and Baltic Seas ensure reliable infrastructure to support complex offshore projects.

Asia Pacific Offshore Support Vessel Services Market Trends

Rapid Market Expansion and Regional Leadership

Asia-Pacific is the fastest-growing region in the offshore support vessel (OSV) market, projected to capture 25% of global share and expand from USD 4.73 billion in 2024 to USD 9.75 billion by 2034 at a 7.5% CAGR. China drives regional demand through large-scale oil and gas exploration in the South China Sea and rapid offshore wind farm development. At the same time, India demonstrates strong potential with expanding ONGC offshore activities and fleet modernization.

The construction of 514 GW of new oil and gas capacity across Asia-Pacific fuels long-term demand for advanced OSVs supporting deepwater and ultra-deepwater operations. Additionally, Australia’s offshore energy diversification and growing renewable energy transition initiatives create broad service opportunities across exploration, installation, and maintenance.

Competitive Landscape

The global offshore support vessel services market exhibits moderate concentration with major international operators controlling substantial market shares through established fleets and global operational networks. Leading companies including Tidewater Inc., Edison Chouest Offshore, Hornbeck Offshore Services, and regional specialists command significant market positions.

The market structure supports both large-scale multinational operators with diversified global fleets and specialized regional providers focusing on specific geographic markets or vessel types. Technological capabilities, regulatory expertise, and vessel fleet sophistication represent critical competitive differentiators enabling premium service positioning and contract acquisition

Key Industry Developments

- In July 2024, Maersk Supply Service spun off a new entity called Maersk Offshore Wind, dedicated to installation services in the offshore wind sector. This venture is based on its innovative “Maersk WIV” (wind installation vessel) concept, designed to reduce turbine installation time by approximately 30%.

- In February 2023, Damen Shipyards Group modified its FLOW-SV vessel idea that can fast-track the expansion of vessel concept that can accelerate the development of this maritime segment. The Damen FLOW-SV is mainly designed for installation of ground attacks for offshore-turbine floaters.

Companies Covered in Offshore Support Vessel Services Market

- BOURBON Corporation

- A.P. Møller - Mærsk A/S

- Falcon Energy Group

- Delta marine Industries Inc

- Swire Pacific Limited

- Edison ChouestOffshore

- Greatship (India) Limited

- Vallianz Holdings. Limited

- Bumi Armada Berhad

- SolstadFarstad ASA

- Seacor Holdings Inc.

- GulfMarkOffshore, Inc

- Others Key Players

Frequently Asked Questions

The Offshore Support Vessel Services market is estimated to be valued at US$ 15.28 Nn in 2025.

The key demand driver for the Offshore Support Vessel (OSV) Services Market is the growing offshore exploration and production (E&P) activities across the oil & gas and renewable energy sectors, particularly offshore wind.

In 2025, the North America region will dominate the market with an exceeding 30% revenue share in the global Offshore Support Vessel Services market.

Among the Vessel Type, Platform Supply Vessel (PSV) holds the highest preference, capturing beyond 60.4% of the market revenue share in 2025, surpassing other Vessel.

The key players in Offshore Support Vessel Services are BOURBON Corporation, A.P. Møller - Mærsk A/S, Falcon Energy Group and Delta marine Industries Inc.