- Renewable Energy

- Wind Power Converter Market

Wind Power Converter Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Wind Power Converter Market by Type of Wind Power Converter (Direct Drive Converters, Gearbox-Based Converters, Doubly Fed Induction Generators (DFIG), Permanent Magnet Synchronous Generators (PMSG), Full-Converter Topologies), Application (Onshore Wind Farms, Offshore Wind Farms, Hybrid Systems (Wind-Solar-Diesel), Distributed Generation, Pumped Storage Plants), Technology, End-use, and Regional Analysis for 2025 - 2032

Wind Power Converter Market Size and Trends Analysis

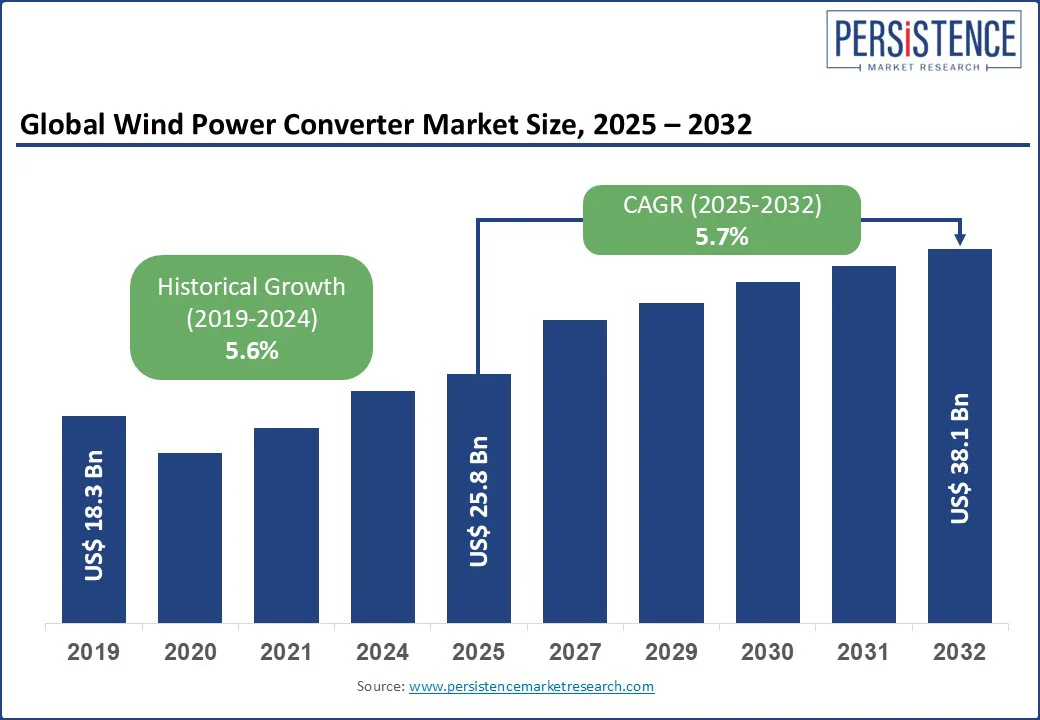

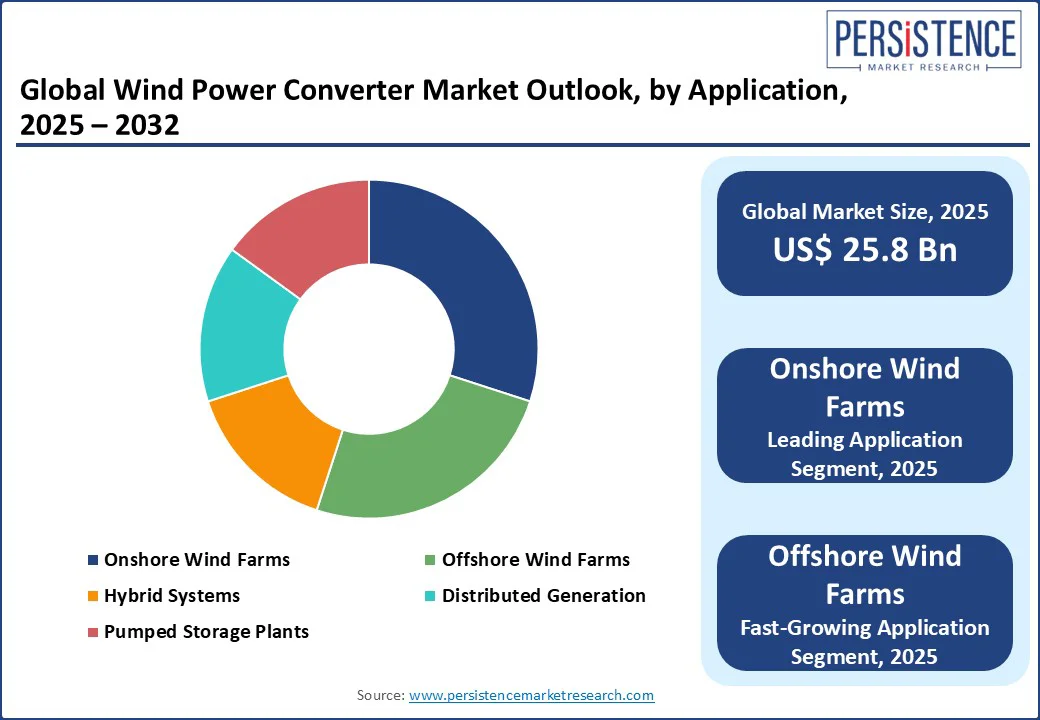

The global wind power converter market size is likely to be valued at US$25.8 Bn in 2025 and is expected to reach US$38.1 Bn by 2032, achieving a CAGR of 5.7% during the forecast period 2025 - 2032.

The wind power converter industry is expanding rapidly, driven by the growing adoption of wind energy worldwide and the need for efficient grid integration. Key technologies include electronic converters, control systems, and generator-based converters that ensure stable power output from variable wind conditions.

Onshore wind farms dominate due to lower costs, while offshore farms are experiencing rapid growth with high-capacity turbines. Market growth is led by advanced power electronics, smart inverters, and IoT-enabled monitoring systems that improve efficiency and reliability.

Key Industry Highlights

- Onshore Wind Farms Dominance: Onshore Wind Farms hold a 50% market share in 2025, driven by grid-connected wind power systems and wind farm electrical systems.

- Offshore Growth Surge: Offshore Wind Farms are fueled by offshore wind power electronics.

- Fastest-Growing Technology: Electronic Converters (Inverters) are driven by wind power inverter systems.

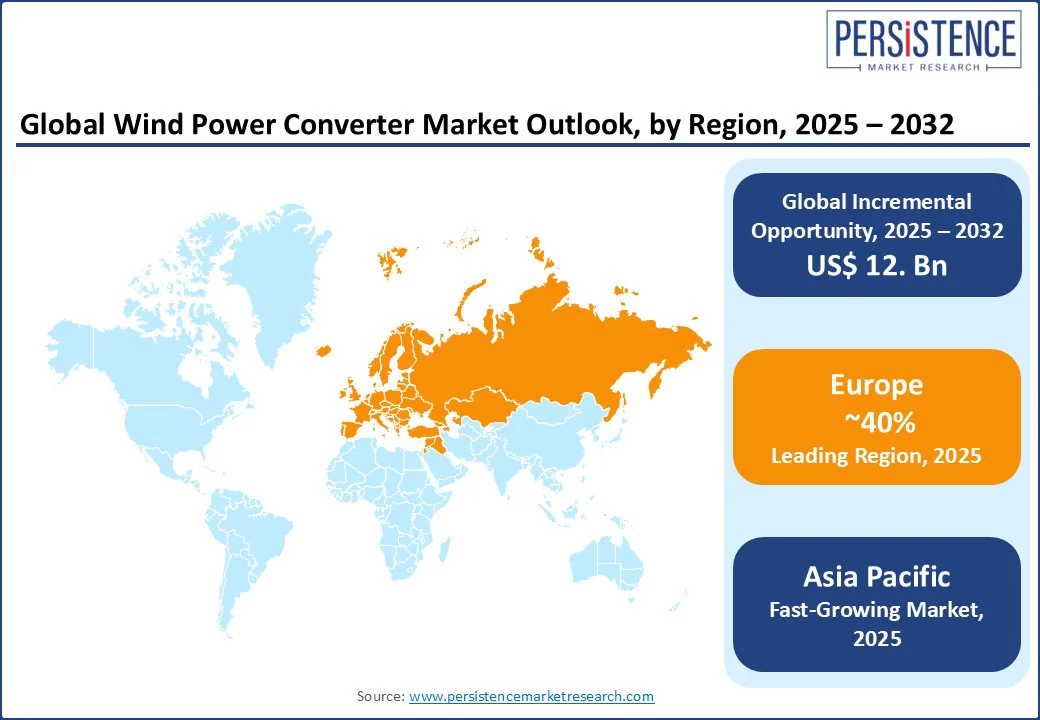

- Regional Leadership: Europe leads with a 40% market share, while Asia Pacific is expected to achieve a CAGR of 6.5% by 2032.

- Innovation Trends: High-efficiency wind power conversion systems and power electronics for renewable energy boost wind turbine control systems by 15% in 2025.

- End-user Trends: Utilities drive 45% market share, supported by wind turbine electrical converter adoption.

- Sustainability Focus: Renewable energy converters reduce carbon emissions by 20%.

|

Global Market Attribute |

Key Insights |

|

Wind Power Converter Market Size (2025E) |

US$25.8 Bn |

|

Market Value Forecast (2032F) |

US$38.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.6% |

Market Dynamics

Driver: Global Push for Renewable Energy and Technological Advancements

The wind power converter market is propelled by several key factors, with a significant focus on the global push for renewable energy and advancements in power electronics for renewable energy. The global wind energy market grew by 12% in 2025 increasing demand for wind inverter, wind energy converter, and wind turbine electrical converter solutions to support grid-connected wind power systems.

A 2025 report noted that 60% of new wind installations globally adopted high-efficiency wind power conversion systems, driving 15% growth in wind farm electrical systems, Offshore wind farms, supported by US$ 100 Bn in global investments in 2025, boost demand for offshore wind power electronics and offshore wind power solutions, with 20% growth in capacity.

Wind turbine control systems and medium voltage converters, integrated with electronic converters (inverters), enhance efficiency by 18%. The wind power converter market forecast 2025 projects 10% growth in wind turbine drivetrain converter adoption, driven by utilities and independent power producers (IPPs) in regions targeting net-zero emissions, such as Europe and the Asia Pacific.

Restraint: High Initial Costs and Supply Chain Challenges

High initial costs and supply chain challenges pose significant restraints to the wind power converter market, impacting wind power inverter systems and wind farm electrical systems.

The cost of power electronics for renewable energy, particularly for offshore wind power electronics, ranges from US$500,000 to 1 million per megawatt, deterring adoption in emerging markets. Supply chain disruptions, with 15% cost increases in semiconductors and rare earth materials in 2025, affect wind turbine electrical converter production.

Regulatory complexities, such as grid compliance standards in the EU and U.S., increase costs for grid-connected wind power systems by 12%. The scalability of the wind power rectifier market is limited in regions such as Africa, where 30% of projects face funding constraints. These challenges hinder the adoption of high-efficiency wind power conversion systems and renewable energy converters in cost-sensitive markets.

Opportunity: Expansion of Offshore Wind and Hybrid Systems

The expansion of offshore wind power solutions and hybrid systems (wind-solar-diesel) presents significant opportunities for the wind power converter market. The global offshore wind market is projected to grow at a CAGR of 14% through 2032, increasing demand for offshore wind power electronics and wind turbine drivetrain converter solutions.

A 2025 report noted that 25% of new wind projects are offshore, boosting wind power inverter systems by 18%. Hybrid systems (wind-solar-diesel), with 15% growth in 2025, drive demand for medium voltage converters in distributed generation.

Companies such as ABB are investing US$300 Mn in R&D for wind turbine control systems and power electronics for renewable energy, targeting utilities and commercial users. Emerging markets, with 500 GW of new wind capacity by 2030, offer opportunities for wind farm electrical systems and renewable energy converters, positioning offshore wind power solutions as a key growth driver.

Category-wise Analysis

Type of Wind Power Converter Insights

Doubly Fed Induction Generators (DFIG) hold approximately 40% of the industry share in 2025 due to their cost-effectiveness in onshore wind farms, with 50% adoption in grid-connected wind power systems in 2025. These generators are highly efficient in grid-connected wind power systems, providing reactive power support and stable grid integration, which is critical as renewable energy penetration increases.

Permanent Magnet Synchronous Generators (PMSG) driven by offshore wind power electronics and high-efficiency wind power conversion systems, with 15% growth in 2025. PMSG technology eliminates the need for external excitation and brushes, leading to lower maintenance and improved reliability, which is critical in offshore environments where maintenance access is challenging and expensive.

Application Insights

Onshore wind farms accounted for a 50% market share in 2025, driven by wind farm electrical systems and wind turbine electrical converters, with 55% adoption in 2025. Continuous innovations in turbine technology, such as larger rotor diameters and higher hub heights, are improving capacity factors, enabling onshore projects to compete more effectively with other renewable sources and fossil fuels.

Offshore wind farms fueled by offshore wind power solutions and wind power inverter systems, with 18% growth in 2025. The adoption of Permanent Magnet Synchronous Generators (PMSG) with full-scale converters, as well as floating wind farm technologies, is further accelerating the offshore segment.

Technology Insights

Electronic Converters (Inverters) command a 35% market share in 2025, driven by wind power inverter systems and power electronics for renewable energy, with 60% adoption in 2025. These converters enable the transformation of variable-frequency AC generated by wind turbines into stable, grid-compatible AC power, ensuring efficient energy delivery to the electrical grid.

Control Systems fueled by wind turbine control systems, with 15% growth in 2025, driven by the adoption of advanced digital and automated control solutions that enhance real-time monitoring, predictive maintenance, and fault detection capabilities.

End-use Insights

Utilities accounted for a 45% market share in 2025, driven by grid-connected wind power systems, with 50% adoption in 2025. Their strong presence in onshore and offshore wind projects ensures steady demand for high-performance electronic converters and grid integration solutions that maintain power stability and quality.

Independent Power Producers (IPPs) driven by renewable energy converters, with 12% growth in 2025, led by the rising demand for decentralized energy generation, merchant power projects, and corporate renewable energy procurement. The shift toward digitalized monitoring, flexible grid support, and energy storage integration further accelerates IPP adoption of advanced power electronics.

Regional Insights

North America Wind Power Converter Market Trends

In North America, the wind power converter market holds a prominent position, commanding a 30% market share in 2025. The U.S. dominates due to its robust wind energy sector, with 100 GW of installed capacity in 2025. The U.S. market is driven by wind farm electrical systems and wind turbine electrical converters, with 70% of new installations using electronic converters (inverters) in 2025.

High-efficiency wind power conversion systems grew by 12%, supported by ABB and Emerson Network Power Co. Ltd. Wind power inverter systems saw 15% growth, aligning with renewable energy targets. ABB and AMSC Windtec drive 25% of regional revenue, leveraging power electronics for renewable energy.

Europe Wind Power Converter Market Trends

In Europe, the wind power converter market accounts for a 40% market share, led by Germany, Denmark, and the UK. Germany’s market is driven by onshore wind farms and wind turbine control systems, with 60% of installations using doubly fed induction generators (DFIG) in 2025. Denmark’s offshore wind farms support the adoption of offshore wind power electronics by Vestas.

The UK’s hybrid systems (wind-solar-diesel) drive 12% growth in renewable energy converters. EU renewable energy policies, with €200 Bn in funding for wind energy in 2025, enhance wind farm electrical systems. Alstom leads with 10% market share.

Asia Pacific Wind Power Converter Market Trends

Asia Pacific is the fastest-growing region, with a CAGR of 6.5%, led by China, India, and Australia. China holds a 45% regional market share, driven by a 20% increase in wind capacity in 2025, boosting wind power inverter systems and grid-connected wind power systems.

India’s market growth is led by distributed generation and medium voltage converters, with 85% of new projects using wind turbine electrical converters in 2025. Australia’s offshore wind power solutions drive 15% growth in offshore wind power electronics. Sungrow Power Supply Co. Ltd and Shenzhen Hopewind Electric Co. Ltd lead, supported by US$50 Bn in wind energy investments by 2030.

Competitive Landscape

The global wind power converter market is highly competitive, with renewable energy companies competing on innovation, efficiency, and sustainability. ABB and Alstom dominate in wind turbine control systems, while Sungrow Power Supply Co. Ltd leads in wind power inverter systems.

Renewable energy converters, offshore wind power electronics, and wind turbine drivetrain converter add a competitive layer. Strategic partnerships and R&D investments in high-efficiency wind power conversion systems are key differentiators.

Key Industry Developments

- In July 2025, Envision Energy, a global provider of intelligent renewable energy solutions, has signed an agreement with FERA Australia, a specialised Australian developer, to develop hybrid projects combining wind and battery storage on the national electricity market. The announcement was made during the Australia Energy Wind Conference, highlighting the goal of reaching up to 1 GW of wind capacity and 1.5 GWh of energy storage.

- In September 2024, RE Technologies Senvion India has officially launched its groundbreaking 4.2M160 wind turbine generator, marking a significant technology advancement in harnessing potential from wind energy. Designed and developed by the in-house R&D teams in India and Germany, manufactured locally, the 4.2M160 is designed to maximise energy output through advanced control technologies and adaptive systems that respond to environmental changes for optimal performance.

- In June 2021, Hitachi ABB Power Grids today launched a portfolio of transformer products for offshore floating applications, designed to overcome the challenging offshore environment and withstand the physically demanding conditions on floating structures. The portfolio will enable much greater volumes of wind to be efficiently harvested and integrated into the global energy system, directly supporting the transition to a sustainable energy future.

Companies Covered in Wind Power Converter Market

- ABB

- Alstom

- AMSC Windtec

- Emerson Network Power Co. Ltd

- Schneider

- Sungrow Power Supply Co. Ltd

- Corona

- Jiuzhou Electrical

- Chino-harvest wind power technology

- Guodian Longyuan Electrical Co. Ltd

- Dongfang Hitachi

- CSR

- Shanghai Hi-tech control system

- Rongxin Power Electronic

- Xin fengguang Electronic

- Shandong BOS Power supply Co. Ltd

- Shenzhen Hopewind Electric Co. Ltd

- Others

Frequently Asked Questions

The wind power converter market is projected to reach US$ 25.8 Bn in 2025, driven by wind inverter and wind farm electrical systems.

Global renewable energy targets, offshore wind power solutions, and high-efficiency wind power conversion systems are key drivers.

The wind power converter market grows at a CAGR of 5.7% from 2025 to 2032, reaching US$ 38.1 Bn by 2032.

Opportunities include offshore wind power electronics, hybrid systems (wind-solar-diesel), and wind turbine control systems.

Key players include ABB, Alstom, Sungrow Power Supply Co. Ltd, AMSC Windtec, Schneider, and others.