- Nutraceuticals & Functional Foods

- Nutraceuticals Market

Nutraceuticals Market Size, Share, Trends, and Growth Forecast 2025 - 2032

Nutraceuticals Market by Product Type (Dietary Supplements including Vitamins, Minerals, Botanicals, Amino acids; Functional Foods including Fortified cereals, Dairy products, Snacks; Functional Beverages including Energy drinks, Fortified juices, Probiotic beverages; Others), Form, Distribution Channel, by Regional Analysis, 2025 - 2032

Nutraceuticals Market Size and Trend Analysis

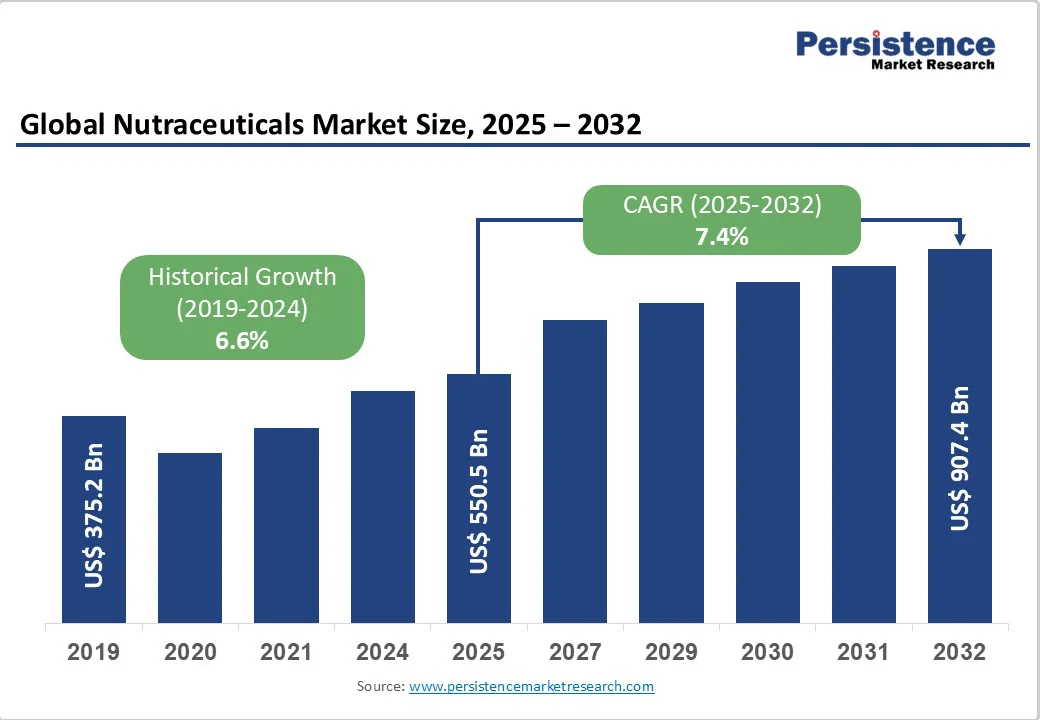

The global nutraceuticals market size is likely to value at US$ 550.5 billion in 2025 and is projected to reach US$ 907.4 billion by 2032, growing at a CAGR of 7.4% between 2025 and 2032.

The rise in health consciousness among consumers, high prevalence of lifestyle-related diseases, and growing demand for preventive healthcare solutions.

The market expansion is further supported by aging populations seeking functional products, enhanced distribution channels including e-commerce platforms, and innovative product formulations that address specific health needs across diverse consumer segments.

Key Market Highlights:

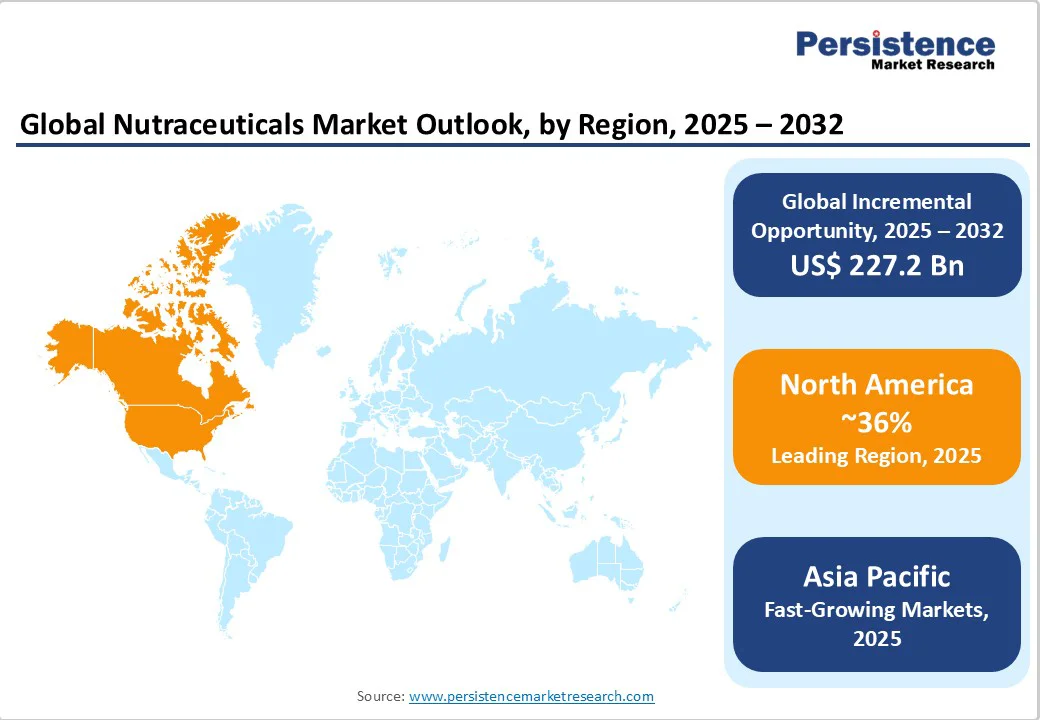

- Leading Region: North America dominates the global nutraceuticals market with 36% revenue share, driven by established regulatory frameworks, high consumer awareness, and robust healthcare professional endorsement across diverse product categories.

- Fastest-Growing Region: Asia Pacific emerges as the fastest-growing region with 7.9% CAGR through 2030, fueled by rapid economic development, urbanization, and government initiatives promoting preventive healthcare solutions.

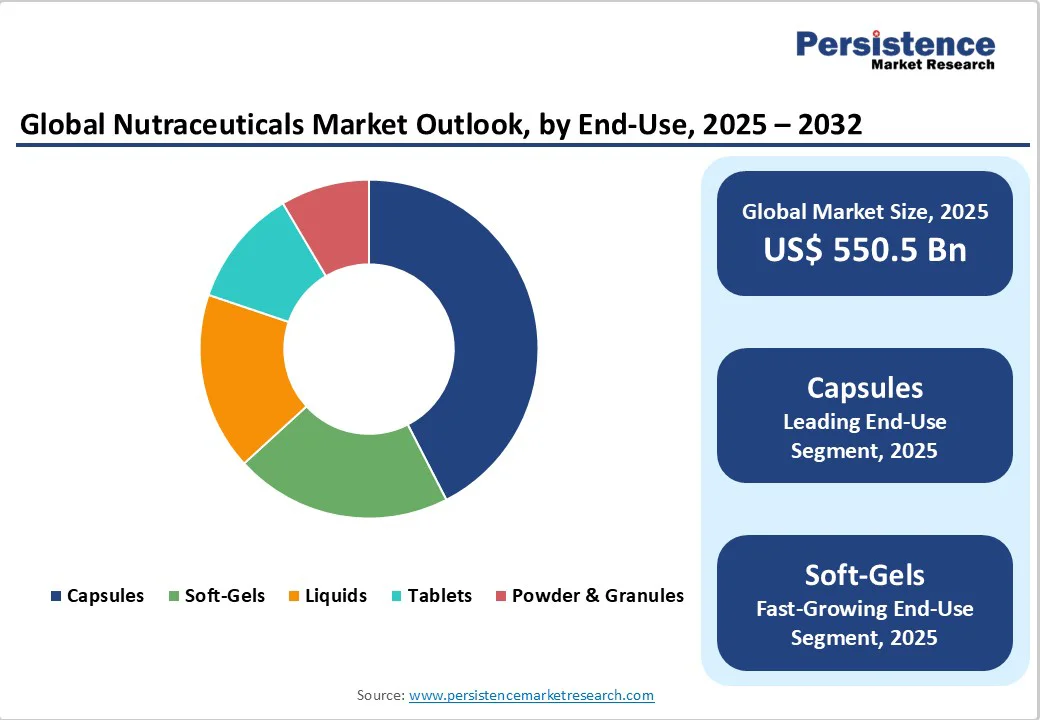

- Leading Product Type Segment: Dietary Supplements represent the dominant product segment with 65% market share, supported by comprehensive scientific validation, regulatory clarity, and established consumer acceptance across global markets.

- Fastest-Growing Form Segment: Capsules constitute the fastest-growing form segment at 6.3% CAGR, driven by superior bioavailability, precise dosing capabilities, and technological innovations in sustained-release formulations for enhanced efficacy.

- Key Market Opportunity: Personalized nutrition presents the most significant market opportunity, projected to reach US$ 64.6 Bn by 2030 through genomics integration, AI-driven recommendations, and subscription-based delivery models.

| Key Insights | Details |

|---|---|

| Nutraceuticals Market Size (2025E) | US$ 550.5 Bn |

| Market Value Forecast (2032F) | US$ 907.4 Bn |

| Projected Growth CAGR(2025 - 2032) | 7.4% |

| Historical Market Growth (2019-2024) | 6.6% |

Market Dynamics

Driver - Rising Health Consciousness and Preventive Healthcare Adoption

The increasing focus on preventive healthcare is a major factor driving the nutraceuticals market. Consumers are shifting from treatment-based approaches to proactive wellness, seeking functional foods and dietary supplements to maintain long-term health. Rising healthcare costs have further motivated individuals to adopt cost-effective preventive solutions.

This trend is particularly strong among millennials and Generation Z, who are willing to invest in products supporting immunity and overall well-being. Events like the COVID-19 pandemic amplified demand for immune-boosting nutraceuticals. Additionally, government initiatives such as updated dietary guidelines and enhanced regulatory frameworks have strengthened consumer trust in these products, fueling consistent market growth across all demographic segments.

Demographic Transition and Aging Population Dynamics

The global demographic shift toward an aging population is emerging as a powerful growth driver for the nutraceuticals market. Individuals aged 65 and above are increasingly prioritizing products that support cognitive function, bone density, cardiovascular health, and overall vitality. This demographic is projected to reach 1.6 Bn by 2050, creating a massive consumer base with distinct nutritional needs and a preference for age-specific formulations.

In addition to rising health needs, older consumers possess higher disposable income and demonstrate strong brand loyalty. Their consistent investment in supplements, combined with a focus on preventive health and longevity, provides nutraceutical manufacturers with a sustained and lucrative revenue opportunity. Markets targeting age-focused products are therefore witnessing accelerated adoption and innovation.

Restraint - Regulatory Complexity and Compliance Challenges

The nutraceuticals industry faces significant challenges due to complex and varying regulatory frameworks across regions. Authorities such as the EFSA require rigorous pre-market safety assessments for novel ingredients, with approval processes taking 18-24 months and costing manufacturers up to US$ 2 Mn. Similarly, the FDA enforces strict cGMP standards under 21 CFR Part 111, demanding extensive documentation and quality control systems that particularly strain smaller manufacturers.

These regulatory inconsistencies force companies to maintain separate formulations, labeling, and marketing strategies for different regions, increasing operational costs and delaying market entry. The compliance burden limits scalability for emerging brands and slows innovation, making regulatory navigation a key constraint for the global nutraceuticals market.

Market Fragmentation and Intense Price Competition

The nutraceuticals market is highly fragmented, with thousands of players competing across multiple product categories. This intense competition exerts significant price pressure, compressing profit margins, particularly for generic dietary supplements, which have seen 15-20% margin reductions in recent years.

The rise of private-label products from major retailers has further intensified competition, offering comparable nutraceuticals at 30-40% lower prices. Combined with a low entry barrier for basic supplement manufacturing, market oversaturation makes differentiation challenging. Companies are often forced to compete on price rather than innovation or quality, limiting sustainable revenue growth and creating a highly competitive operating environment.

Opportunities - Personalized Nutrition and Technology Integration

The convergence of genomics, artificial intelligence, and consumer health data is creating significant opportunities for nutraceutical companies. Personalized nutrition solutions, tailored to individual metabolic profiles and health goals, are gaining traction as consumers increasingly seek precision-based wellness products. Advances in biomarker testing and AI-driven analytics enable the development of supplements that deliver measurable health outcomes, commanding premium pricing.

Companies such as Ritual and Care/of have proven the commercial viability of subscription-based personalized supplements, achieving retention rates above 85% compared to 45% for traditional retailers. Early adopters investing in wearable integration, genetic testing insights, and lifestyle data are establishing sustainable competitive advantages while raising entry barriers for conventional players.

Emerging Markets Expansion and Digital Commerce Penetration

Rapid economic growth in Asia-Pacific, Latin America, and Middle East & Africa offers immense potential for nutraceutical market expansion. These regions, representing 60% of the global population but only 35% of current consumption, are witnessing rising health awareness, disposable incomes, and urbanization.

The proliferation of e-commerce has democratized access, enabling SMEs to reach consumers directly while reducing distribution costs by 25-30%. Cross-border regulations, mobile payment adoption, and social commerce platforms like WeChat and Instagram allow targeted marketing and seamless transactions. These factors collectively create opportunities for premium nutraceutical products and measurable growth in emerging markets.

Category-wise Insights

Product Type Analysis

Dietary supplements dominate the nutraceutical market with approximately 65% share, driven by versatility, convenience, and strong consumer trust. Vitamins, minerals, and botanical extracts address specific health deficiencies and wellness goals.

Multivitamins account for the largest portion of intake, and products like Vitamin D grew in 2024 due to rising awareness of immune support and bone health. Regulatory clarity under frameworks such as the FDA’s DSHEA ensures safe manufacturing, labeling, and marketing, reinforcing consumer confidence.

Functional foods and beverages are the fastest-growing product segment, fueled by rising health consciousness and demand for convenient nutrition. Fortified foods, probiotic beverages, and energy drinks are increasingly popular for immunity, gut health, and energy support. Innovations in flavor, personalized formulations, and subscription-based delivery models have broadened appeal and improved retention, making this segment a rapidly expanding opportunity for manufacturers.

Form Analysis

Capsules lead the form segment with roughly 42% share due to precise dosing, superior bioavailability, and convenience. Soft-gels enhance the absorption of omega-3 fatty acids, fat-soluble vitamins, and herbal extracts. Manufacturing efficiencies, enteric coatings, and vegetarian alternatives further enhance their appeal, while automated encapsulation reduces production costs and ensures consistent quality.

Soft-gels and powdered supplements are the fastest-growing format, projected at 6.7% CAGR. Soft-gels improve nutrient absorption, while powders cater to sports nutrition, weight management, and functional formulations. Flavor masking, delayed-release technology, and enhanced bioavailability attract younger, health-conscious consumers, driving rapid adoption and growth in this segment.

Distribution Channels Analysis

Offline channels hold a leading position with around 58% share, supported by consumer trust, in-store consultation, and immediate product access. Pharmacies and specialty nutrition retailers provide knowledgeable staff, loyalty programs, and wide product selections, creating confidence and supporting sustained adoption.

Online channels are the fastest-growing distribution segment, powered by e-commerce penetration, mobile payments, and social commerce. Direct-to-consumer models reduce distribution costs and broaden reach, while subscription services, personalized recommendations, and targeted marketing accelerate adoption, particularly in emerging markets, making online the most dynamic channel in nutraceuticals.

Regional Insights

North America Nutraceuticals Market Trends

North America maintains its position as the largest nutraceuticals market, accounting for approximately 36% of global revenue, driven by high consumer health awareness, robust regulatory frameworks, and advanced research infrastructure supporting product innovation.

The United States leads regional growth with the FDA's comprehensive regulatory structure under 21 CFR Part 111 ensuring product quality and safety standards that build consumer confidence. The region benefits from strong healthcare professional endorsement, with 68% of physicians regularly recommending supplements to patients according to the Council for Responsible Nutrition.

Canada's Natural and Non-prescription Health Products Directorate has streamlined approval processes for natural health products, facilitating market entry for innovative formulations while maintaining safety standards. The region demonstrates sophisticated consumer behavior with increasing demand for evidence-based products, clean-label formulations, and sustainable packaging solutions.

E-commerce penetration has reached 45% of supplement sales, accelerated by COVID-19 impacts and enhanced by subscription-based delivery models that improve customer lifetime value. Major retailers including Amazon, iHerb, and Vitacost have invested heavily in fulfillment infrastructure, reducing delivery times to 24-48 hours in metropolitan areas.

Europe Nutraceuticals Market Trends

Europe's nutraceuticals market demonstrates strong growth momentum driven by harmonized European Food Safety Authority (EFSA) regulations that facilitate cross-border trade while maintaining stringent safety standards across 27 member nations. Germany leads regional consumption with supplement usage rates reaching 62% of the adult population, supported by the country's strong tradition in natural medicine and phytotherapy.

France's pharmaceutical distribution model through pharmacies has driven premium positioning for nutraceutical products, with average selling prices 25% higher than other European markets. The United Kingdom's post-Brexit regulatory framework has created opportunities for regulatory divergence, potentially accelerating approval processes for certain categories.

Sustainability concerns drive significant market dynamics, with 73% of European consumers prioritizing environmentally responsible packaging and sourcing practices. The region's aging demographic creates sustained demand for cognitive health and bone health products, with Germany, Italy, and France showing the highest per-capita consumption of senior-focused formulations.

Asia Pacific Nutraceuticals Market Trends

Asia Pacific represents the fastest-growing nutraceuticals market globally, projected to expand at 7.9% CAGR through 2030, driven by rapid economic development, urbanization, and evolving dietary patterns across diverse consumer segments.

China dominates regional market dynamics with 37.9% market share, supported by government initiatives promoting the integration of Traditional Chinese Medicine with modern nutraceutical science. The country's National Health Commission has prioritized preventive healthcare through its Healthy China 2030 initiative, creating favorable regulatory environments for functional food development.

India emerges as the region's growth powerhouse with 11.6% CAGR projected through 2033, driven by FSSAI regulatory modernization and expanding middle-class purchasing power. The country's rich Ayurvedic heritage provides competitive advantages in botanical and herbal formulations, with companies like Dabur and Himalaya successfully combining traditional knowledge with modern manufacturing standards.

Japan's sophisticated market demonstrates high acceptance of functional foods through the FOSHU (Foods for Specified Health Uses) regulatory framework, enabling premium positioning for scientifically validated products. E-commerce penetration has accelerated dramatically, with platforms such as Tmall, JD.com, and Amazon India capturing 35% of supplement sales through targeted digital marketing and rapid delivery capabilities.

Competitive Landscape

The nutraceuticals market is highly fragmented, comprising numerous multinational corporations alongside thousands of specialized regional players. Large, established companies leverage extensive distribution networks, regulatory expertise, and strong research and development capabilities to maintain leadership in traditional segments.

Strategic acquisitions are commonly used to rapidly expand product portfolios and gain local market expertise, strengthening their position across multiple categories.

Mid-tier and smaller players differentiate through specialization in niche segments such as sports nutrition, cognitive health, or plant-based formulations. Direct-to-consumer brands focus on innovative delivery systems, personalized nutrition, and digital-first marketing. Adoption of advanced technologies, including AI-driven product development and precision manufacturing, has become a key factor for competitive advantage.

Key Market Developments

- In September 2024, Nestlé Health Science announced the launch of its personalized nutrition platform, integrating genetic testing with AI-driven supplement recommendations. The platform targets growing consumer demand for customized wellness solutions across North American and European markets, enabling precision nutrition, improved health outcomes, and enhanced engagement through personalized product offerings.

- In August 2024, ADM Company completed the acquisition of a specialized probiotic manufacturer to strengthen its functional beverage capabilities. The move expands ADM’s presence in the rapidly growing gut health segment, valued at US$ 15.2 Bn globally, and enhances its portfolio of probiotic solutions while addressing increasing consumer interest in digestive health and wellness-focused products.

- In July 2024, Royal DSM N.V. unveiled a breakthrough microencapsulation technology for omega-3 fatty acids. This innovation improves stability, enhances bioavailability, and reduces fishy taste issues, significantly increasing consumer compliance. The technology targets supplement and functional food applications, addressing longstanding challenges in delivering effective and palatable omega-3 formulations.

Companies Covered in Nutraceuticals Market

- Nestlé Health Science

- Glanbia plc

- Amway Corporation

- Bayer AG

- Herbalife Nutrition Ltd.

- Archer Daniels Midland Company

- Royal DSM N.V.

- NOW Foods

- Ritual

- Pharmavite LLC

- Nature's Way

- Thorne Research

- Nordic Naturals

- New Chapter

- Gaia Herbs

- Abbott Laboratories

- PepsiCo Inc.

- Danone S.A.

- General Mills Inc.

- BASF SE

Frequently Asked Questions

The global nutraceuticals market is projected to reach US$ 907.4 Bn by 2032, growing from US$ 550.5 Bn in 2025 at a CAGR of 7.4% during the forecast period.

The nutraceuticals market is primarily driven by rising health consciousness, aging population demographics, increasing prevalence of lifestyle-related diseases, and growing consumer preference for preventive healthcare solutions over treatment-based approaches.

Dietary Supplements dominate the market with approximately 65% market share, driven by their versatility, convenience, scientific validation, and established consumer acceptance across global markets.

North America leads the global nutraceuticals market with 36% revenue share, supported by established regulatory frameworks, high consumer awareness, and robust healthcare professional endorsement.

Personalized nutrition presents the most significant opportunity, projected to reach US$ 64.6 Bn by 2030, driven by advances in genomics, AI-driven recommendations, and consumer acceptance of customized health solutions.

Leading companies include Nestlé Health Science, Glanbia plc, Amway Corporation, Bayer AG, Herbalife Nutrition Ltd., Archer Daniels Midland Company, Royal DSM N.V., and other established multinational corporations with strong research capabilities and global distribution networks.