- Medical Devices

- Muscle Stimulation Devices Market

Muscle Stimulation Devices Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Muscle Stimulation Devices Market by Product Type (Neuromuscular Electric Stimulator (NMES), Transcutaneous Electric Nerve Stimulator (TENS), Interferential (IF), Burst Mode Alternating Current), by Application (Pain Management, Neurological & Movement Disorder Management, Musculoskeletal Disorder Management), End-user (Hospitals, Physiotherapy Clinics, Sports Clinics, Home Care Settings), by Regional Analysis 2026 - 2033

Muscle Stimulation Devices Market Share and Trends

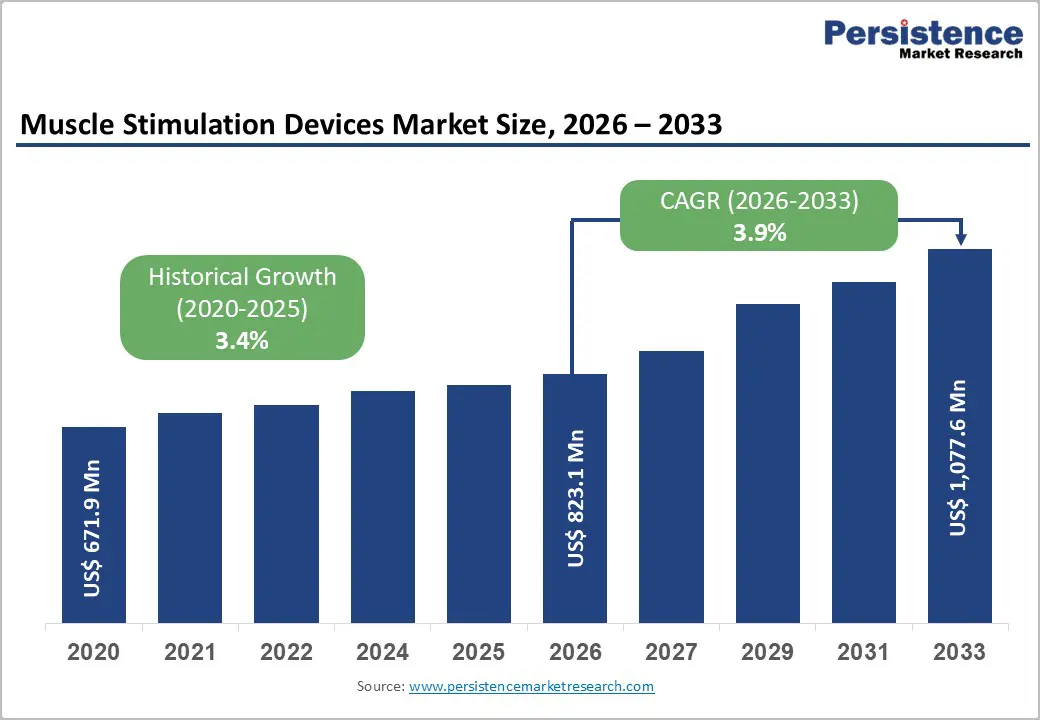

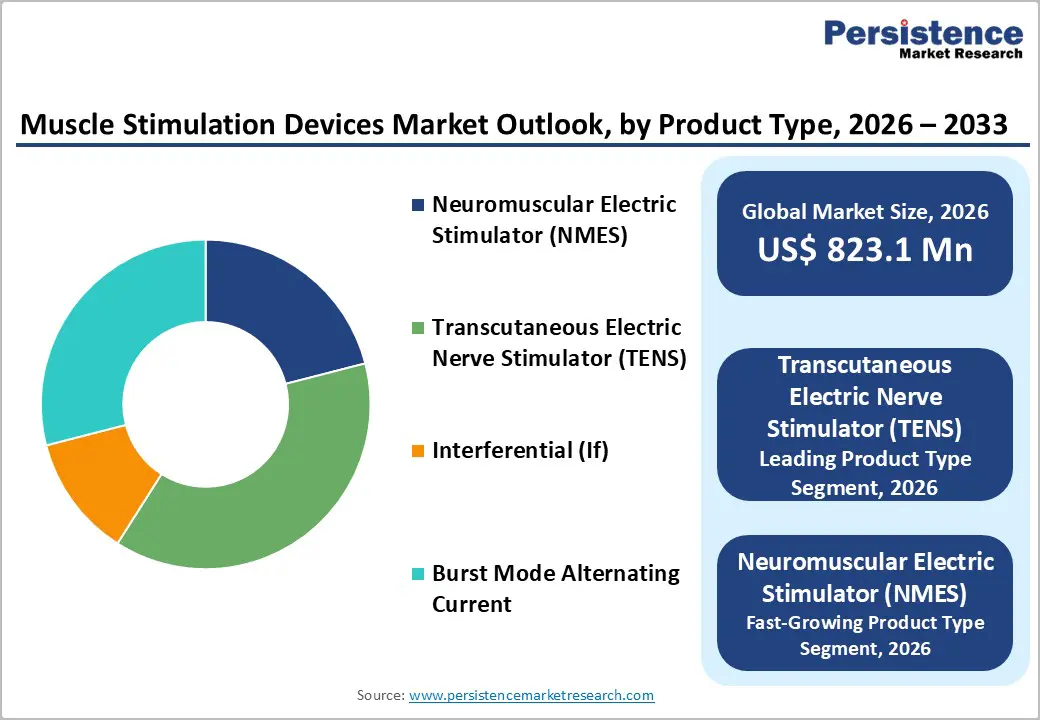

The global muscle stimulation devices market size is expected to be valued at US$ 823.1 million in 2026 and projected to reach US$ 1,077.6 million by 2033, growing at a CAGR of 3.9% between 2026 and 2033.

The rising prevalence of musculoskeletal disorders and chronic pain drives this expansion, supported by the increasing adoption of non-invasive therapies amid an aging population. Technological advancements in portable devices enhance accessibility for home use and rehabilitation, while growing sports injuries boost demand in clinical settings. These factors collectively drive sustained market growth by improving patient outcomes and increasing the preference for drug-free pain relief.

Key Industry Highlights:

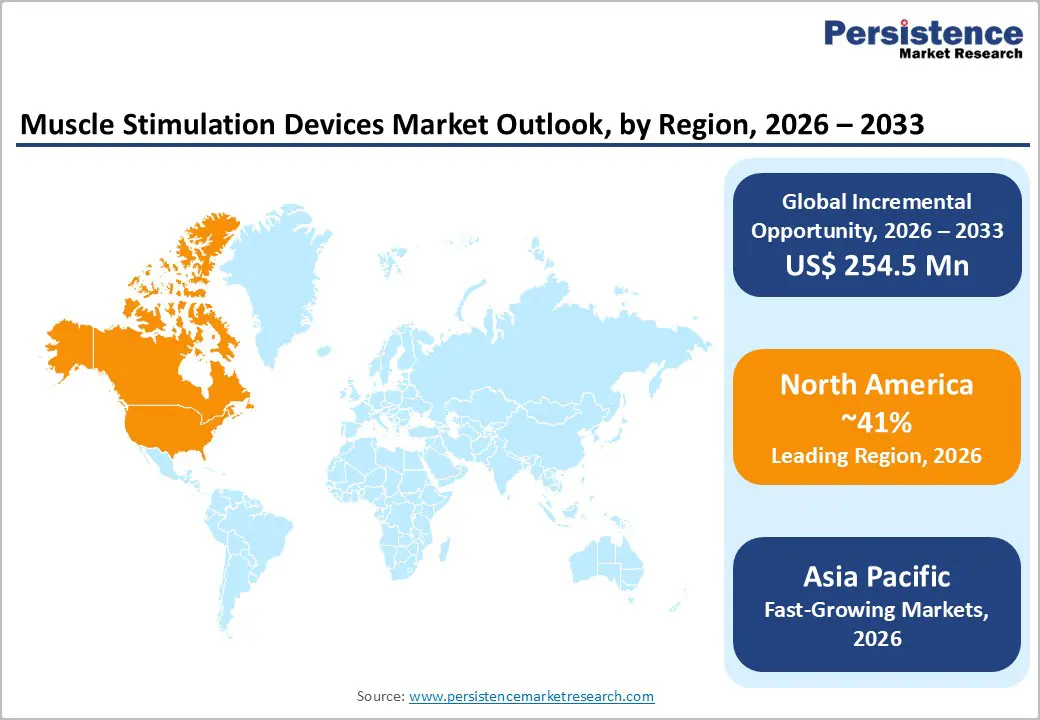

- North America leads with approximately 41% share in 2025, supported by strong U.S. FDA approvals, advanced rehabilitation infrastructure, high healthcare spending, and early adoption of innovative muscle-stimulation technologies.

- Asia Pacific is the fastest-growing region, driven by rapid healthcare infrastructure upgrades in China and India, expanding patient access, cost-efficient manufacturing, and rising prevalence of musculoskeletal disorders.

- TENS dominates the product landscape with nearly 38% share, owing to its long-established clinical use, proven pain relief efficacy, affordability, and widespread acceptance in both clinical and home settings.

- NMES represents the fastest-growing product segment, fueled by increasing adoption in sports rehabilitation, post-surgical recovery, and technological advances such as wireless and app-enabled stimulation systems.

- Home care expansion presents a key growth opportunity, as demand rises for portable, user-friendly muscle-stimulation devices that support long-term chronic pain management and post-operative rehabilitation at home.

| Key Insights | Details |

|---|---|

| Muscle Stimulation Devices Size (2026E) | US$ 823.1 million |

| Market Value Forecast (2033F) | US$ 1,077.6 million |

| Projected Growth CAGR (2026 - 2033) | 3.9% |

| Historical Market Growth (2020 - 2025) | 3.4% |

Market Dynamics

Driver - Rising Musculoskeletal Disorders Prevalence

The rising global prevalence of musculoskeletal disorders (MSDs) is a major driver for the muscle stimulation devices market, as these conditions significantly impair mobility, productivity, and quality of life. MSDs such as chronic back pain, osteoarthritis, rheumatoid arthritis, and muscle weakness are increasingly common due to sedentary work patterns, prolonged screen exposure, obesity, and rapidly aging populations. Older adults are particularly vulnerable to muscle degeneration, joint stiffness, and post-surgical weakness, creating sustained demand for effective rehabilitation solutions. Muscle stimulation devices, including NMES and TENS, offer non-invasive and drug-free management of pain and muscle dysfunction, making them highly attractive for long-term therapy. These devices are widely used in physiotherapy settings to stimulate muscle contractions, improve blood circulation, prevent muscle atrophy, and enhance functional recovery. Their ability to reduce dependence on pain medications and support home-based rehabilitation further strengthens adoption. As healthcare systems emphasize early intervention, faster recovery, and cost-effective chronic care management, muscle stimulation devices are increasingly integrated into standard musculoskeletal treatment protocols worldwide.

Surge in Sports Injuries and Rehabilitation Needs

The growing incidence of sports injuries and rehabilitation needs is significantly increasing demand for muscle stimulation devices. Increased participation in professional sports, recreational fitness, endurance training, and high-intensity workouts has led to a higher incidence of muscle strains, ligament injuries, post-surgical weakness, and overuse injuries. Athletes and physically active individuals increasingly seek faster and safer recovery methods to return to performance with minimal downtime. NMES devices are widely used in sports medicine to support muscle re-education, strength restoration, and the prevention of disuse atrophy following injuries or orthopedic surgeries, such as ACL reconstruction or total knee arthroplasty. These devices enhance neuromuscular activation, improve muscle endurance, and complement conventional physiotherapy programs. Sports rehabilitation centers, orthopedic clinics, and physiotherapy practices are integrating muscle-stimulation technologies as standard recovery tools owing to their proven clinical benefits. Additionally, the growing focus on injury prevention, performance optimization, and personalized rehabilitation programs further boosts adoption, positioning muscle stimulation devices as essential components in modern sports healthcare ecosystems.

Restraints - Stringent Regulatory Approvals

Stringent regulatory approval processes are a key restraint on the muscle stimulation devices market, as they extend development timelines and increase compliance costs. Regulatory authorities mandate extensive preclinical and clinical evaluations to validate device safety, performance consistency, and therapeutic efficacy before granting approvals. Concerns about improper use, electrical overstimulation, skin burns, and unintended nerve effects prompt regulators to enforce strict labeling, training, and post-market surveillance requirements. These obligations are particularly challenging for manufacturers developing compact, wireless, or home-use devices, as regulators closely scrutinize user safety outside supervised clinical environments. Prolonged approval cycles delay product launches, slow innovation, and reduce manufacturers’ ability to rapidly respond to evolving patient and clinician needs. Smaller companies and startups face greater barriers due to limited regulatory expertise and high documentation costs, ultimately restricting product variety and slowing overall market expansion despite demonstrated clinical benefits.

High Device Costs and Alternatives

High device costs significantly restrain the adoption of muscle stimulation technologies, especially in price-sensitive and developing healthcare markets. Advanced stimulators with programmable settings, wireless connectivity, and multi-channel outputs are often expensive, limiting affordability for patients and small physiotherapy clinics. In many regions, limited reimbursement coverage further increases out-of-pocket expenses, discouraging long-term use. As a result, patients frequently opt for lower-cost alternatives such as manual physiotherapy, oral pain medications, or basic exercise regimens. Additionally, effective use of stimulation devices often requires professional supervision to ensure correct electrode placement and intensity control, adding to treatment costs. Fear of adverse effects from improper use also deters self-administration. These economic and practical barriers impede market penetration, despite the clear advantages of muscle stimulation devices in rehabilitation efficiency and recovery outcomes.

Opportunity - Expansion into Home Care Settings

The expansion of muscle stimulation devices into home care settings presents a significant growth opportunity, driven by shifting healthcare delivery models and rising demand for convenient, patient-centric therapies. Aging populations and the increasing prevalence of chronic pain, post-surgical weakness, and mobility limitations are encouraging long-term rehabilitation outside hospital environments. Portable TENS and NMES devices enable patients to manage pain relief and muscle strengthening at home, reducing dependency on frequent clinic visits and lowering overall treatment costs. The COVID-19 pandemic further accelerated acceptance of home-based care, reinforcing patient confidence in self-administered therapeutic devices. Manufacturers are developing compact, lightweight, and intuitive designs that simplify electrode placement and intensity control, thereby enhancing safety and usability. Integration of guided therapy modes and preset programs supports adherence and consistent outcomes. As healthcare systems emphasize remote monitoring and continuity of care, home-use muscle-stimulation devices are increasingly regarded as essential tools for managing chronic conditions and supporting postoperative recovery, thereby expanding market reach beyond traditional clinical settings.

Advancements in Portable and Wireless Technologies

Advancements in portable and wireless muscle stimulation technologies create strong opportunities by enhancing treatment flexibility, personalization, and user engagement. Modern devices now feature wireless connectivity, smartphone app integration, and programmable stimulation protocols, enabling tailored therapy based on individual patient needs. These innovations are particularly appealing to sports rehabilitation centers and home users seeking mobility and uninterrupted therapy sessions. App-enabled platforms allow clinicians to remotely adjust treatment parameters, track progress, and improve therapy compliance. Next-generation NMES devices demonstrate improved muscle activation accuracy, thereby increasing their value in neurological rehabilitation and post-injury recovery. Ongoing regulatory clearances for advanced stimulation systems further validate their clinical effectiveness and safety. The shift toward non-invasive, drug-free rehabilitation solutions aligns well with these technological improvements. As demand grows for personalized recovery plans and performance-focused rehabilitation, particularly in the rapidly expanding NMES segment, portable and wireless muscle stimulation devices are poised to achieve widespread adoption across both clinical and consumer healthcare markets.

Category-wise Analysis

Product Type Insights

Transcutaneous Electric Nerve Stimulator (TENS) dominates the muscle stimulation devices market, with an estimated 38% share in 2025, primarily due to its broad use in pain management across both clinical and home care settings. TENS devices are widely prescribed for acute and chronic pain conditions, including musculoskeletal disorders, post-operative pain, and neuropathic pain, owing to their ability to interrupt pain signal transmission to the brain. Strong clinical validation, including meta-analyses demonstrating meaningful reductions in analgesic consumption, reinforces physician and patient confidence. Ease of use, affordability compared to advanced stimulators, and availability of portable, home-use models further support adoption. Additionally, long-standing regulatory approvals and inclusion in standard physiotherapy protocols have increased familiarity among healthcare professionals. These factors collectively position TENS as a first-line, noninvasive pain-relief modality, sustaining its leadership across diverse healthcare settings.

End-user Insights

Hospitals account for the largest share of the muscle stimulation devices market, supported by their advanced clinical infrastructure and high patient throughput. These settings manage a substantial volume of patients requiring musculoskeletal rehabilitation, post-surgical recovery, neurological therapy, and trauma care, where muscle stimulation plays a critical role. Hospitals are equipped with multi-channel, high-performance stimulation systems integrated into structured rehabilitation programs. The presence of skilled physiotherapists, orthopedic specialists, and rehabilitation teams ensures precise device application, optimal intensity control, and patient safety. Additionally, hospitals often serve as early adopters of technologically advanced devices, driven by access to capital budgets and regulatory compliance capabilities. Their ability to deliver intensive, supervised therapy protocols strengthens treatment outcomes, reinforcing preference for hospital-based care. This combination of clinical expertise, equipment availability, and patient volume sustains hospitals’ leading position in market adoption.

Regional Insights

North America Muscle Stimulation Devices Market Trends and Insights

North America leads the muscle stimulation devices market with an estimated 41% global share in 2025, supported by a strong innovation ecosystem and early adoption of advanced medical technologies. The United States remains the key contributor, driven by high prevalence of chronic pain, musculoskeletal disorders, and post-surgical rehabilitation needs. A well-established regulatory framework, with a large number of muscle stimulation devices registered and cleared, supports continuous product innovation and faster commercialization. Strong focus on sports medicine, orthopedic rehabilitation, and neurological recovery further accelerates demand across hospitals, clinics, and sports facilities. Favorable reimbursement policies and high healthcare spending encourage both clinician and patient adoption. Additionally, a rapidly growing geriatric population increases long-term demand for pain management and muscle strengthening solutions. The rising shift toward home-based care has also fueled uptake of portable and wireless devices, sustaining regional market leadership.

Asia Pacific Muscle Stimulation Devices Market Trends and Insights

Asia Pacific is emerging as the fastest-growing region in the muscle stimulation devices market, driven by expanding healthcare access and rising disease burden across major economies such as China, Japan, India, and ASEAN countries. Rapid urbanization, sedentary lifestyles, and increased sports participation are contributing to a growing incidence of musculoskeletal disorders and sports-related injuries. Governments and private players are investing heavily in healthcare infrastructure upgrades, strengthening rehabilitation and physiotherapy services. The region also benefits from strong local manufacturing capabilities, which help reduce device costs and improve affordability, particularly for NMES systems. An aging population in countries like Japan and China further boosts demand for muscle strengthening and pain management therapies. Growing awareness of non-invasive rehabilitation options and increasing adoption of portable, home-use devices are accelerating market penetration, positioning Asia Pacific as a high-growth opportunity.

Competitive Landscape

The muscle stimulation devices market shows moderate concentration, with leaders like DJO Global, Zynex, and Omron holding key shares amid smaller innovators. Fragmented traits emerge from niche players in home care. Strategies emphasize R&D for wireless tech, acquisitions for portfolios, and sports-focused differentiators like app integration. Emerging models prioritize direct-to-consumer sales.

Key Market Developments

- In November 2025, Motive Health, Inc., the innovative healthcare technology company behind the first FDA-cleared muscle stimulation device for knee pain, announced the launch of Motive Lower Back, an FDA-cleared at-home therapy designed to address a root cause of lower back issues by strengthening weak and imbalanced stabilizing muscles.

Companies Covered in Muscle Stimulation Devices Market

- DJO Global Inc.

- Zynex Inc.

- Neurometrix Inc.

- R.S. Medical Inc.

- Omron Corporation

- Beurer, EMS Physio Ltd

- Enovis, Abbott

- BTL Corporate

- Medtronic, Boston Scientific

Frequently Asked Questions

The muscle stimulation devices market is valued at US$ 823.1 million in 2026, growing from historical trends.

Rising musculoskeletal disorders and sports injuries fuel adoption of non-invasive rehab.

North America with 41% share in 2025, via U.S. innovation and regulations.

Home care growth with portable TENS/NMES for chronic pain self-management.

Leaders include DJO Global, Zynex, Omron, focusing on tech advancements.