- Pharmaceuticals

- Non-muscle Invasive Bladder Cancer Therapeutics Market

Non-muscle Invasive Bladder Cancer Therapeutics Market Size, Share, and Growth Forecast 2026 - 2033

Non-muscle Invasive Bladder Cancer Therapeutics Market by Cancer Grade (Low-grade, High-grade), by Drug Type (Immunotherapy, Chemotherapy, Targeted Therapy), by Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Specialty Pharmacies, Online Pharmacies), by Regional Analysis, 2026-2033

Non-muscle Invasive Bladder Cancer Therapeutics Market Size and Share Analysis

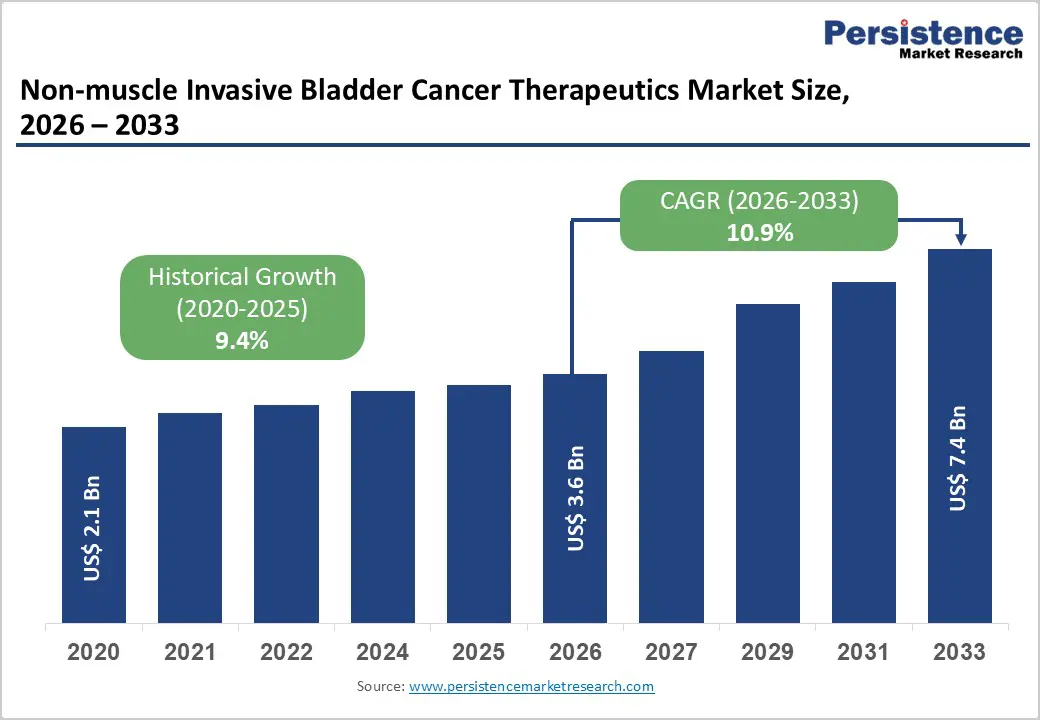

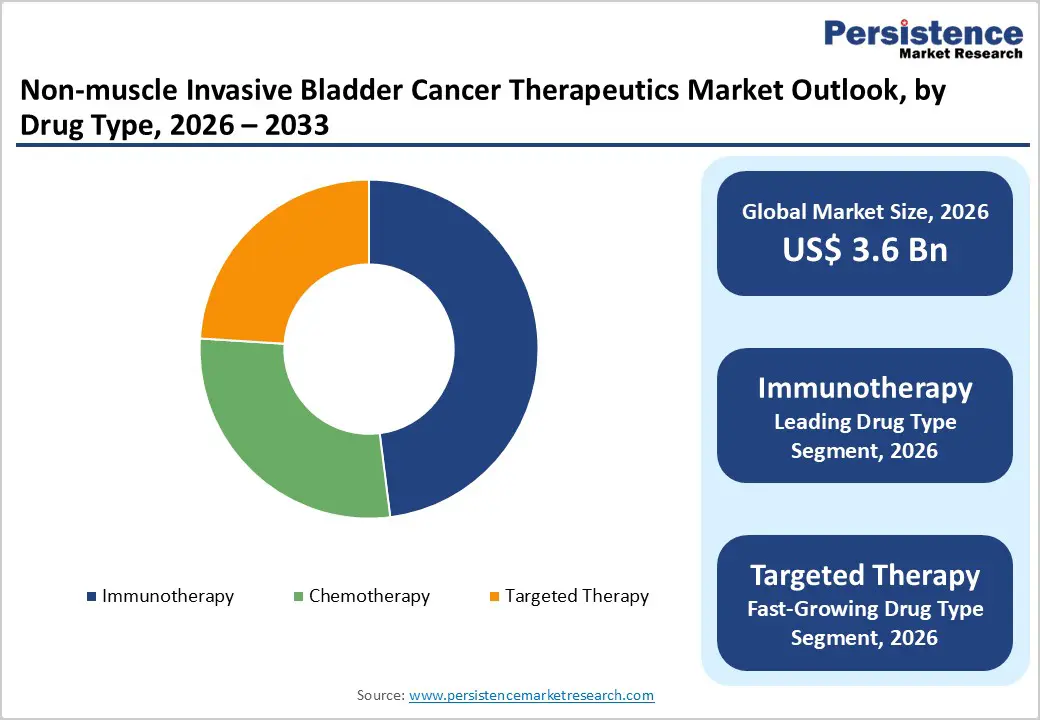

The global non-muscle invasive bladder cancer therapeutics market size is expected to be valued at US$ 3.6 billion in 2026 and projected to reach US$ 7.4 billion by 2033, growing at a CAGR of 10.9% between 2026 and 2033.

The market expansion is driven by the increasing prevalence of bladder cancer globally and the development of novel therapeutic approaches beyond traditional BCG therapy. According to World Health Organization (WHO) estimates and GLOBOCAN data, approximately 573,000 new bladder cancer cases and 213,000 deaths occurred in 2020 globally, with incidence rates projected to increase by 73% by 2040. The rising adoption of immunotherapeutic agents, particularly PD-1 and PD-L1 inhibitors such as pembrolizumab, nivolumab, and avelumab, combined with the FDA approval of innovative combination therapies and gene therapy options for BCG-unresponsive patients, is substantially driving market growth. Additionally, increasing awareness of bladder-preserving treatment alternatives and supportive healthcare policies is strengthening market demand across diagnostic and treatment pathways globally.

Key Market Highlights

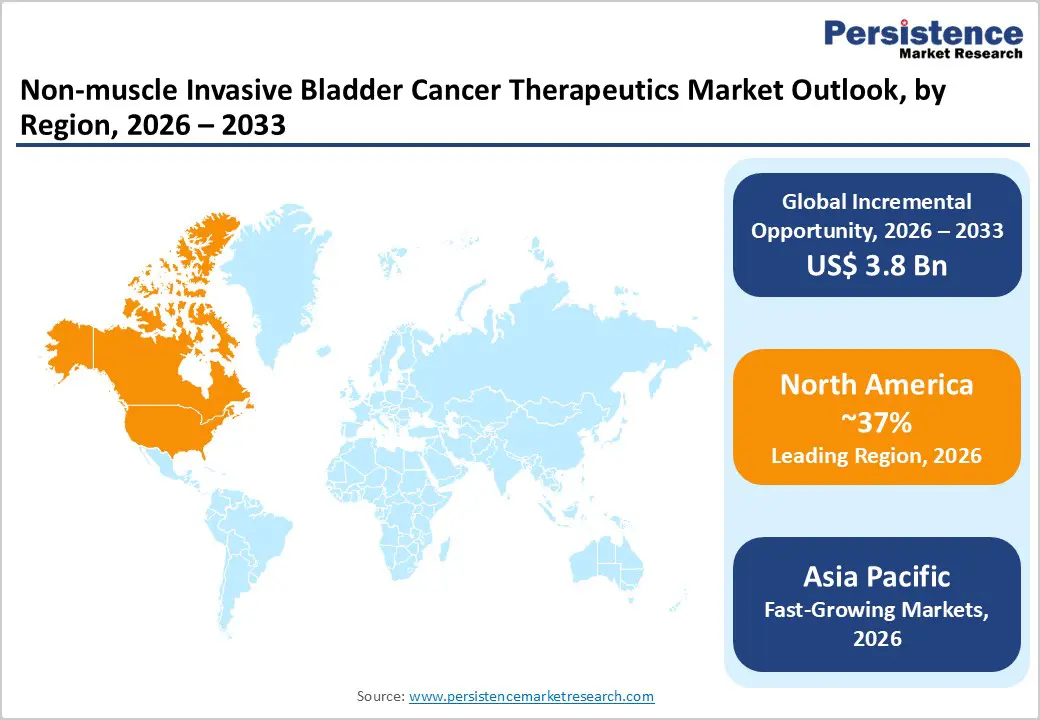

- Leading Region: North America held ~37% of the global NMIBC therapeutics market in 2025, driven by high disease incidence, rapid adoption of FDA-approved therapies, strong healthcare infrastructure, and favorable reimbursement.

- Fastest-Growing Region: Asia Pacific is expected to grow at the fastest CAGR during 2026–2033, supported by a large patient base, improving diagnostics, healthcare modernization, and rising access to advanced immunotherapies.

- Dominant Segment: Immunotherapy accounted for ~48% market share in 2025, supported by widespread BCG use, recent regulatory approvals, and a shift toward bladder-preserving immune-based treatments.

- Fastest-Growing Segment: Targeted therapy is expanding rapidly, driven by FGFR inhibitors, novel intravesical delivery platforms, and personalized treatment approaches.

- Key Opportunity: Combination immunotherapy strategies for BCG-unresponsive and high-risk NMIBC offer strong growth potential through improved outcomes and broader treatment access.

| Report Attribute | Details |

|---|---|

|

Non-muscle Invasive Bladder Cancer Therapeutics Market Size (2026E) |

US$ 3.6 billion |

|

Market Value Forecast (2033F) |

US$ 7.4 billion |

|

Projected Growth CAGR (2026-2033) |

10.9% |

|

Historical Market Growth (2020-2025) |

9.4% |

Market Dynamics

Market Growth Drivers

Rising Prevalence of Non-Muscle Invasive Bladder Cancer and Treatment Needs

The global burden of non-muscle invasive bladder cancer continues to escalate, with NMIBC comprising approximately 75% of all newly diagnosed bladder cancer cases according to recent clinical evidence. GLOBOCAN data demonstrates that bladder cancer accounts for 3% of global cancer diagnoses, with incidence rates significantly higher in developed nations. The WHO projects a 73% increase in annual bladder cancer cases by 2040, while mortality rates are expected to rise by 87% globally. In developed regions, Southern and Western Europe report the highest incidence rates at 26.5 and 21.5 per 100,000 population, respectively, while North America reports 10.9 per 100,000. The critical challenge of BCG treatment failures affecting approximately 40% of patients who fail to respond initially and 50% experiencing recurrence after initial response has created substantial demand for alternative therapeutic options. This escalating disease burden drives consistent demand for novel therapeutics across hospital pharmacies, specialty clinics, and retail pharmacy channels.

FDA Approvals and Innovative Therapeutic Options

Recent FDA approvals have significantly expanded the therapeutic landscape for non-muscle invasive bladder cancer, particularly for BCG-unresponsive patients. The FDA approval of Anktiva (nogapendekin alfa inbakicept-pmln) in April 2024 represents a major milestone, combining BCG for BCG-unresponsive NMIBC treatment and offering improved complete response rates. Pembrolizumab received FDA approval for BCG-unresponsive high-grade carcinoma in situ, demonstrating 41% complete response rates at three months with 80% maintaining remission beyond six months. Nadofaragene firadenovec, approved in December 2022, represents the first intravesical gene therapy option. Additionally, the gemcitabine and docetaxel combination has gained prominence as a salvage option, with 60% and 50% one- and two-year recurrence-free survival rates in BCG-unresponsive patients. These innovative therapeutics with diverse mechanisms of action, including immunotherapy, gene therapy, and chemotherapy combinations, create multiple revenue streams and substantially expand treatment options beyond traditional approaches.

Market Restraints

High Cost of Novel Therapeutics and Healthcare Access Disparities

The high cost of emerging non-muscle invasive bladder cancer therapeutics represents a significant market constraint, particularly in developing nations and lower-income healthcare systems. Immunotherapeutic agents such as pembrolizumab, nivolumab, and avelumab, while offering superior efficacy, command substantially higher prices than traditional BCG therapy and standard chemotherapy. Novel delivery systems such as the TAR-200 intravesical drug delivery platform, though offering improved patient convenience and reduced systemic toxicity, require specialized implantation procedures and premium pricing. Limited healthcare insurance coverage for emerging therapies in many developing countries restricts patient access and adoption rates. The WHO's epidemiological data reveals that 60% of bladder cancer cases occur in less developed countries, yet these regions have limited infrastructure to support expensive therapeutic innovations. Geographic disparities in treatment availability and the substantial burden on healthcare budgets in resource-constrained settings significantly constrain overall market growth and create accessibility barriers for patients.

BCG Supply Shortages and Treatment Standardization Challenges

Despite being the gold standard for intermediate and high-risk NMIBC, BCG supply disruptions have periodically constrained treatment availability and shifted demand toward alternative therapeutics. The critical reliance on BCG monotherapy and combination approaches as first-line treatment creates supply chain vulnerabilities that periodically disrupt market dynamics. Additionally, the lack of established treatment standardizationthe protocols across different geographies limits widespread adoption of emerging therapies. Different regional treatment guidelines, ranging from 29-31 conditions screened in North American programs to 15-40 in European programs, create fragmented market demand. The substantial adverse event profiles associated with some immunotherapies and emerging therapeutics, including systemic toxicity and immunotherapy-related complications, result in treatment discontinuation in certain patient populations. These regulatory, supply chain, and clinical standardization challenges represent material constraints to market expansion, particularly in developing regions with limited healthcare infrastructure.

Market Opportunities

Advancement of Combination Immunotherapy Strategies and BCG-Sparing Approaches

Significant market opportunities exist through the development and commercialization of combination immunotherapy approaches that enhance efficacy while potentially reducing BCG dosage requirements or providing alternatives to BCG therapy. The POTOMAC and PATAPSCO clinical trials, evaluating durvalumab in combination with BCG in BCG-naïve high-risk NMIBC patients, demonstrate the promising potential of combination approaches. Recent clinical evidence shows that nivolumab combined with gemcitabine-cisplatin achieves 48% complete response rates with 100% one-year survival in metastatic disease settings. The development of interleukin-based therapies and NK cell activators exemplified by Anktiva's mechanism of enhancing immune cell activity creates novel treatment pathways. Emerging PD-1/PD-L1 targeting combinations with intravesical chemotherapy agents present substantial revenue opportunities for pharmaceutical companies developing dual-mechanism therapeutics. The shift toward bladder-preserving strategies and personalized medicine approaches, particularly for high-risk and BCG-unresponsive populations, is expected to generate significant demand for specialized therapeutics across hospital and specialty pharmacy channels globally.

Expansion into Asian and Emerging Market Segments

Substantial market opportunities exist through geographic expansion into high-growth emerging markets in Asia, Latin America, and Africa, where bladder cancer prevalence is rising, yet treatment options remain limited. Eastern Asia reports the greatest absolute number of bladder cancer cases globally, with 1.68 million cases representing 21.5% of worldwide incidence according to GLOBOCAN data. China alone operates approximately 150 newborn screening laboratories and demonstrates a rapidly expanding oncology treatment infrastructure. India and Southeast Asian nations show rising bladder cancer incidence with emerging healthcare modernization initiatives. The relatively lower penetration of novel therapeutics in these regions, combined with rising healthcare spending and government cancer control initiatives, creates substantial growth opportunities. Strategic partnerships between multinational pharmaceutical companies and regional healthcare providers can establish market presence in high-growth Asian markets. The development of cost-effective generic versions of emerging therapeutics and localized manufacturing capabilities presents additional opportunities to capture price-sensitive segments in emerging market while addressing unmet treatment needs in populations currently underserved by advanced therapeutics.

Category-wise Insights

Cancer Grade Analysis

High-grade NMIBC represents the dominant cancer grade segment, commanding the most substantial portion of the non-muscle invasive bladder cancer therapeutics market. High-grade urothelial carcinomas, including high-grade carcinoma in situ (CIS) and papillary tumors, demonstrate substantially higher risk profiles with greater propensity for progression to muscle-invasive disease and systemic metastasis. Clinical evidence demonstrates that high-grade NMIBC patients require more aggressive and sustained therapeutic interventions, including extended BCG maintenance therapy protocols and combination immunotherapeutic approaches.

The FDA-approved therapies, including pembrolizumab, nadofaragene, and Anktiva, specifically target high-grade disease phenotypes, particularly BCG-unresponsive high-grade CIS. Recent clinical trials, including the KEYNOTE-057 trial, demonstrated durable complete response rates in high-grade BCG-unresponsive patients treated with pembrolizumab, establishing high-grade disease as the primary clinical focus. The complexity of managing high-grade disease, the need for specialized treatment protocols, and the substantial healthcare expenditures associated with advanced therapeutics and surveillance strategies position high-grade NMIBC as the market's dominant revenue-generating segment across all distribution channels globally.

Drug Type Analysis

Immunotherapy represents the leading drug type segment in the non-muscle-invasive bladder cancer therapeutics market, commanding approximately 48% of market share in 2025 and demonstrating the strongest growth trajectory. This dominance reflects the revolutionary transformation of NMIBC treatment following the successful integration of Bacillus Calmette-Guérin (BCG) immunotherapy and the emergence of checkpoint inhibitor therapeutics. BCG therapy remains the cornerstone intravesical immunotherapeutic approach, with established clinical efficacy spanning decades and proven reduction in recurrence and progression in intermediate and high-risk NMIBC.

The emergence of PD-1 and PD-L1 inhibitors, including pembrolizumab, nivolumab, durvalumab, and avelumab, has significantly expanded the immunotherapy armamentarium. Pembrolizumab monotherapy achieves 41% complete response rates in BCG-unresponsive high-grade CIS patients, while nivolumab demonstrates 19.6% objective response rates in metastatic urothelial carcinoma. The recent FDA approval of Anktiva, an interleukin-15 receptor agonist for combination BCG therapy, further strengthens the immunotherapy segment's market position. The superior efficacy profiles, bladder-preserving mechanisms, and extensive clinical trial support have established immunotherapy as the preferred treatment approach for both BCG-naïve and BCG-unresponsive patients, driving consistent market growth.

Regional Insights

North America Non-muscle Invasive Bladder Cancer Therapeutics Market Trends

North America maintains the leading regional position in the global non-muscle invasive bladder cancer therapeutics market, commanding approximately 37% of the total market share in 2025. The United States reports 80,500 bladder cancer diagnoses annually, representing 4.6% of all cancer diagnoses and making it the sixth most common cancer diagnosis.

The National Cancer Institute (NCI) and Surveillance, Epidemiology, and End Results (SEER) program document comprehensive epidemiological data indicating incidence rates of 18.1 per 100,000 population, with NMIBC comprising 75% of newly diagnosed cases. The advanced healthcare infrastructure, comprehensive insurance coverage, and rapid adoption of FDA-approved therapeutics have positioned North America as the largest revenue generator in the market.

Asia Pacific Non-muscle Invasive Bladder Cancer Therapeutics Market Trends

The Asia Pacific region represents the fastest-growing market for non-muscle-invasive bladder cancer therapeutics, projected to expand at exceptional rates during the 2026-2033 forecast period. GLOBOCAN data documents that Eastern Asia reports the largest absolute number of bladder cancer cases globally at 1.68 million cases, representing 21.5% of worldwide incidence. China alone reports an incidence of 4.3 per 100,000 population, with an estimated 14 million births annually, creating a substantial disease burden. India and Southeast Asian nations demonstrate rising bladder cancer incidence, yet historically limited access to advanced therapeutics compared to developed regions.

The Asia Pacific region demonstrates exceptional growth potential through healthcare modernization and increasing pharmaceutical accessibility. China's healthcare transformation initiatives and government-sponsored cancer control programs are accelerating the adoption of immunotherapies and novel treatment approaches. Recent FDA and EMA approvals of emerging therapeutics are being rapidly integrated into Asian treatment protocols, with Japan and South Korea demonstrating particularly high adoption rates of advanced immunotherapies.

Manufacturing advantages in countries like India and China enable cost-effective production of therapeutic agents, supporting regional accessibility. The combination of massive patient populations, rising healthcare spending, expanding hospital infrastructure, and improving regulatory frameworks positions Asia Pacific as the highest-growth region, with particular opportunities in intermediate- and high-risk NMIBC segments driven by advancing diagnostic capabilities and treatment availability.

Competitive Landscape

Market Structure Analysis

The non-muscle invasive bladder cancer therapeutics market is moderately competitive, shaped by a mix of established treatment standards and emerging innovative therapies. Competition centers on improving efficacy in BCG-unresponsive patients, reducing recurrence rates, and enhancing patient convenience through novel delivery methods. Companies are focusing on intravesical formulations, gene-based and targeted therapies, and combination approaches to differentiate their pipelines. Strategic priorities include regulatory approvals, clinical trial expansion, and partnerships with healthcare institutions.

Key Market Developments

- In January 2026, ImmunityBio, Inc. has received approval from the Saudi Food and Drug Authority (SFDA) for ANKTIVA® (nogapendekin alfa inbakicept) in combination with Bacillus Calmette-Guérin (BCG) for the treatment of adult patients with BCG-unresponsive non-muscle invasive bladder cancer carcinoma in situ, with or without papillary disease. This regulatory action by the SFDA added to the existing approvals in the United States and the United Kingdom, as well as the conditional approval in the European Union.

Key Market Highlights

Leading Region: North America commands approximately 37% of the global non-muscle invasive bladder cancer therapeutics market share in 2025, driven by the highest disease incidence rates globally, rapid adoption of FDA-approved novel therapeutics, comprehensive healthcare infrastructure, and strong pharmaceutical reimbursement supporting continuous market expansion and investment.

Fastest Growing Region: Asia Pacific demonstrates the highest growth trajectory with exceptional CAGR expansion during 2026-2033, supported by the region's massive patient population representing 21.5% of global bladder cancer cases, rapid healthcare modernization in China and Southeast Asia, improving diagnostic capabilities, and increasing accessibility to advanced immunotherapeutic treatments.

Dominant Segment: Immunotherapy drug type represents the leading market segment, capturing approximately 48% of market share in 2025, driven by superior clinical efficacy of BCG and checkpoint inhibitor therapeutics, recent FDA approvals for pembrolizumab, nivolumab, durvalumab, and Anktiva, and the shift toward bladder-preserving treatment paradigms emphasizing immune-based approaches.

Fastest Growing Segment: Targeted Therapy demonstrates the fastest growth rate within the drug type category, driven by emerging FGFR inhibitors including erdafitinib for FGFR3-mutant NMIBC populations, the TAR-210 intravesical delivery platform, personalized medicine approaches, and clinical trial validation of molecularly-targeted approaches in BCG-resistant patient populations.

Key Market Opportunity: Development and commercialization of combination immunotherapy approaches combining BCG with checkpoint inhibitors and interleukin-based therapies for BCG-unresponsive and high-risk NMIBC represents the most significant market opportunity, offering potential revenue growth through reduced healthcare costs, improved patient outcomes, and expansion of treatment options in underserved geographic regions.

Companies Covered in Non-muscle Invasive Bladder Cancer Therapeutics Market

- Pfizer Inc.

- Merck KGaA

- AstraZeneca PLC

- Roche Holding AG (Genentech)

- Astellas Pharma Inc.

- Johnson & Johnson (Janssen Biotech)

- Cipla Inc.

- Amneal Pharma

- Bristol Myers Squibb Co.

- Dr. Reddy's Laboratories Inc.

- Gilead Sciences Inc.

- Endo Pharma

- UroGen Pharma Inc.

- Teva Pharmaceuticals (Actavis)

- Seagen Inc.

- Janssen Oncology

- Genentech (Roche subsidiary)

- Immunocore Ltd.

- Adaptimmune Therapeutics

- Atheneum Pharma

Frequently Asked Questions

The global non-muscle invasive bladder cancer therapeutics market is expected to reach US$ 3.6 billion in 2026.

The principal demand drivers include the rising global prevalence of bladder cancer with 573,000 annual cases and 213,000 deaths, FDA approvals of innovative therapeutics including pembrolizumab, nadofaragene, and Anktiva, the critical challenge of BCG treatment failure affecting 40% of patients, and the growing shift toward bladder-preserving immunotherapeutic strategies emphasizing improved patient quality of life and clinical outcomes.

North America, primarily the United States, commands approximately 37% of the global non-muscle invasive bladder cancer therapeutics market share in 2025, supported by the highest disease incidence rates, rapid FDA therapeutic approvals, comprehensive healthcare infrastructure, strong reimbursement policies, and the highest per-capita pharmaceutical spending on cancer therapeutics globally.

The Asia Pacific region represents the fastest-growing market, driven by the region's massive patient population accounting for 21.5% of global bladder cancer incidence, rapid healthcare modernization in China, India, and Southeast Asia, expanding diagnostic capabilities, increasing pharmaceutical accessibility, and government-sponsored cancer control initiatives creating substantial treatment demand.

Major market opportunities include development of combination immunotherapy approaches combining BCG with checkpoint inhibitors and interleukin-based therapies, advancement of personalized medicine strategies for molecularly-stratified patient populations, expansion into high-growth Asian and emerging markets, development of cost-effective therapeutic alternatives for price-sensitive regions, and commercialization of novel intravesical delivery systems reducing treatment burden and improving patient compliance.