- Pharmaceuticals

- Multiple Unit Pellet Systems (MUPS) Market

Multiple Unit Pellet Systems (MUPS) Market Size, Share, and Growth Forecast, 2026 - 2033

Multiple Unit Pellet Systems (MUPS) Market by Formulation (Extended Release Dosage Form, Delayed-Release Orodispersible Dosage Forms, Delayed Release Dosage Form), Dosage Form (Tablets, Capsules, Sachets, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Drug Stores), and Regional Analysis for 2026-2033

Multiple Unit Pellet Systems (MUPS) Market Share and Trends Analysis

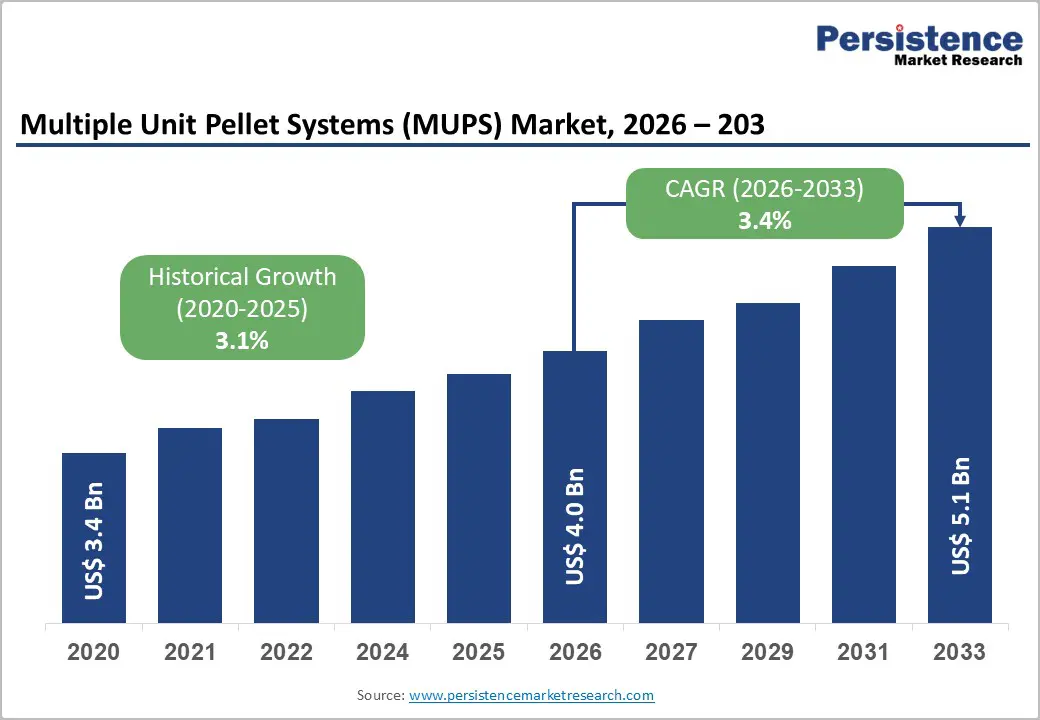

The global multiple unit pellet systems (MUPS) market size is likely to be valued at US$ 4.0 billion in 2026, and is projected to reach US$ 5.1 billion by 2033, growing at a CAGR of 3.4% during the forecast period 2026−2033. Increasing demand for modified-release and controlled-release formulations in pharmaceutical manufacturing is the main growth driver for the market.

Drug developers are increasingly incorporating pellet-based delivery systems to improve dose uniformity and therapeutic consistency. The rising global burden of chronic diseases such as cardiovascular disorders, diabetes, and gastrointestinal conditions is increasing the need for precision dosing and sustained drug release. As healthcare providers are prioritizing long-term disease management, pharmaceutical companies are continuing to integrate pelletization technologies to optimize pharmacokinetic performance and patient adherence. Technological advancements in extrusion-spheronization, fluid bed coating, and layering processes are improving pellet uniformity and scalability, which is strengthening manufacturing efficiency. Regulatory authorities are also enforcing stringent bioavailability and quality standards, encouraging the adoption of robust delivery platforms that can ensure consistent drug release profiles. Patient-centric drug delivery strategies are gaining traction, as oral solid dosage forms that reduce dosing frequency are enhancing treatment compliance. Widening adoption is also being witnessed in emerging economies due to expanding generic drug production and contract manufacturing activity.

Key Industry Highlights

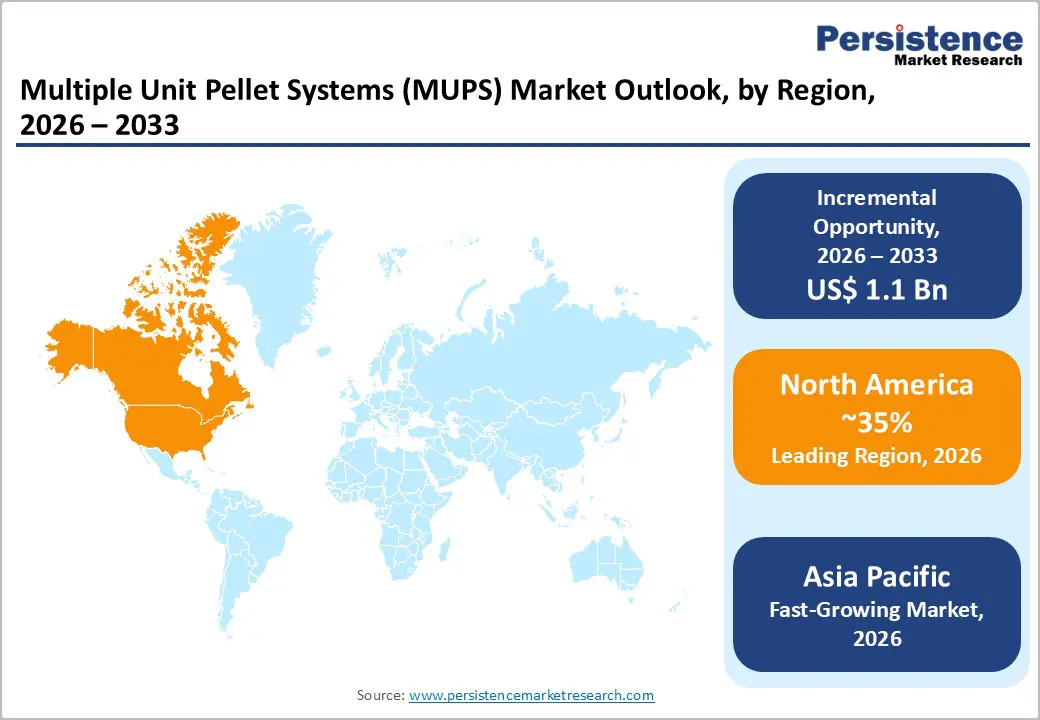

- Dominant Region: North America is expected to command about 38% market share in 2026, supported by high pharmaceutical and healthcare research & development (R&D) investment.

- Fastest-growing Market: The Asia Pacific market is poised to be the fastest-growing from 2026 to 2033, owing to substantial manufacturing capacity and expanding domestic demand led by India and China.

- Leading & Fastest-growing Formulations: Extended-release dosage forms are set to dominate with approximately 48% revenue share in 2026, while delayed-release orodispersible forms are likely to be the fastest-growing during the 2026-2033 forecast period.

- Distribution Channel Dominance: Hospital pharmacies are expected to lead about 45% market share in 2026, with retail pharmacies projected to grow the fastest through 2033.

- Market Driver: The pharmaceutical industry is actively pursuing controlled and sustained-release formulations, which is fueling the adoption of MUPS.

- Market Opportunity: The merging of MUPS technology seamlessly with digital therapeutics and precision medicine is unlocking compelling product differentiation advantages.

| Key Insights | Details |

|---|---|

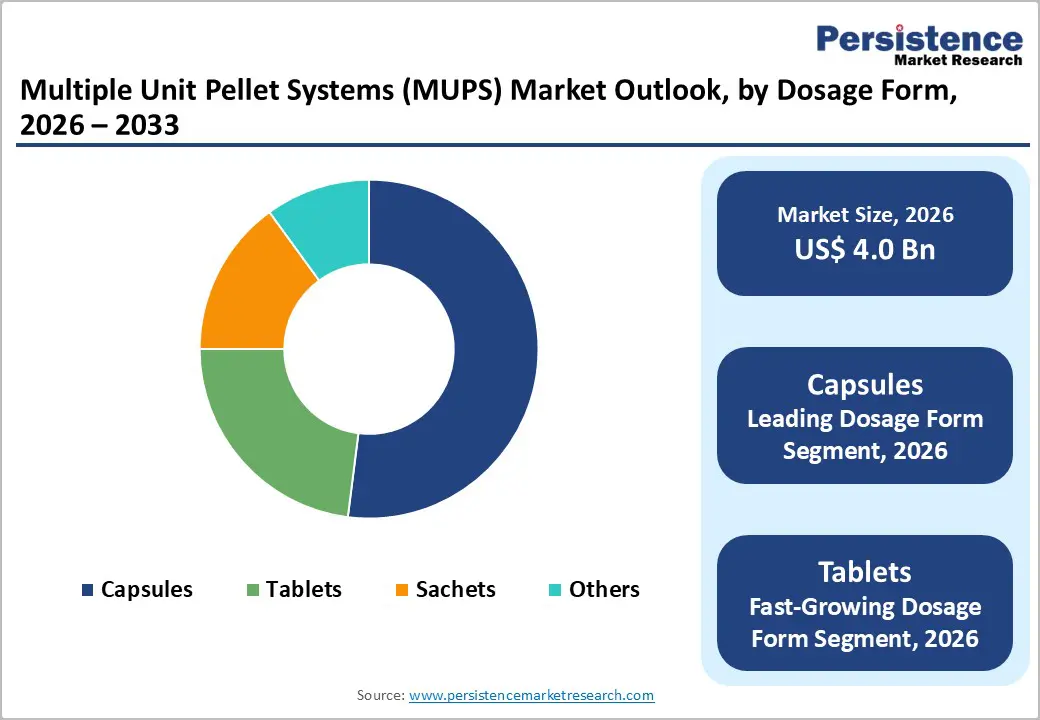

| Multiple Unit Pellet Systems (MUPS) Market Size (2026E) | US$ 4.0 Bn |

| Market Value Forecast (2033F) | US$ 5.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Modified-Release Drug Delivery Systems

The pharmaceutical industry is increasingly prioritizing controlled and sustained-release drug delivery systems, which is accelerating the adoption of multiple unit pellet systems. Drug manufacturers are selecting these formulations because they are enabling precise modulation of drug release kinetics and improving pharmacokinetic consistency. By reducing peak-trough fluctuations, MUPS is minimizing dosing frequency and enhancing long-term adherence, particularly in chronic disease management. Healthcare providers are recognizing clinical value across therapeutic areas such as cardiovascular disorders, gastrointestinal conditions, and central nervous system (CNS) therapies. Unlike conventional monolithic tablets, MUPS technology is allowing the integration of incompatible active pharmaceutical ingredients within a single dosage form, which is strengthening lifecycle management strategies and supporting differentiated product positioning. Companies are leveraging this capability to extend patent life, create fixed-dose combinations, and improve product resilience against generic substitution.

MUPS formulations are maintaining stable plasma drug concentrations, which is reducing adverse event incidence and improving therapeutic predictability. Patients are experiencing fewer interruptions in daily routines due to simplified dosing schedules, while physicians are achieving more consistent clinical outcomes through reliable delivery profiles. Healthcare systems are benefiting from lower complication rates and reduced hospitalization risk, which is contributing to overall cost containment. Pharmaceutical companies are continuing to invest in formulation science, analytical validation, and scale-up capabilities to meet growing demand for patient-centric therapies. Strategic collaborations with contract development and manufacturing organizations (CDMOs) that specialize in multiparticulate technologies are strengthening technical execution and accelerating time to market.

Complex Regulatory Requirements and Approval Processes

Regulatory authorities are applying stringent oversight to MUPS products, and they are scrutinizing dissolution behavior, bioequivalence performance, and manufacturing validation with significant rigor. The U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) are requiring comprehensive documentation that demonstrates uniform pellet characteristics, consistent drug distribution, and reproducible release kinetics across batches. Regulators are also assessing process controls, stability data, and in vitro–in vivo correlation to ensure predictable therapeutic performance. Pharmaceutical companies are navigating complex approval pathways that differ across jurisdictions, and they are adapting submission strategies to align with country-specific regulatory expectations. Organizations that are establishing dedicated regulatory affairs teams early in development are streamlining dossier preparation and reducing approval delays.

Divergent national requirements are complicating global product rollouts, particularly for generic MUPS formulations that often require comparative bioequivalence or additional clinical validation studies. These obligations are increasing development costs and extending commercialization timelines. Companies are responding by designing region-specific development plans that address local data expectations while preserving global consistency while prioritizing entry into markets with transparent regulatory frameworks before expanding into more complex jurisdictions. Strategic manufacturers are building modular global dossiers that can be adapted for multiple authorities without duplicating core data packages. This coordinated regulatory planning is strengthening international launch readiness and positioning organizations for sustainable expansion with reduced compliance risk.

Integration with Digital Health and Personalized Medicine

Multiple unit pellet systems are being increasingly integrated with digital therapeutics and precision medicine frameworks to deliver differentiated drug delivery solutions. Pharmaceutical companies are incorporating smart packaging technologies that are enabling real-time dose tracking and continuous patient adherence monitoring. These capabilities are aligning with global digital health initiatives that are transforming care delivery toward data-driven and outcomes-focused models. Leading manufacturers are developing personalized MUPS formulations that are matching individual pharmacokinetic behavior and metabolic variability. To support this customization at scale, companies are deploying 3D printing technologies alongside modular and flexible manufacturing systems. This approach is allowing rapid formulation adjustment while maintaining commercial production efficiency and regulatory compliance.

Industry leaders are positioning MUPS as core enablers of next-generation drug delivery architectures. They are combining adaptable pellet-based designs with real-time patient data analytics to optimize dosing accuracy and therapeutic response. Healthcare providers are gaining enhanced clinical decision tools that support dynamic treatment adjustments based on observed pharmacodynamic outcomes. Organizations that are investing early in these integrated platforms are establishing durable competitive advantages through exclusive partnerships with digital health and data analytics specialists. Development efforts are increasingly concentrating on high-value therapeutic areas such as chronic disease management and specialty care, where long-term adherence and individualized dosing are critical to outcomes. This strategic focus is strengthening portfolio resilience while aligning innovation investments with evolving healthcare delivery priorities.

Category-wise Analysis

Formulation Insights

Extended-release dosage forms are anticipated to dominate among formulations, commanding approximately 48% of the MUPS market revenue share in 2026, driven by their critical role in chronic disease management across cardiovascular, diabetes, and central nervous system therapeutic areas. The segment benefits from strong physician preference for improved patient compliance, established reimbursement pathways in major markets, and extensive clinical evidence demonstrating superior therapeutic outcomes. Major pharmaceutical companies have invested substantially in proprietary extended-release MUPS platforms, creating competitive barriers through patent protection and regulatory expertise that sustain market leadership.

Delayed-release orodispersible dosage forms are likely to be the fastest-growing segment during the 2026-2033 forecast period. This exceptional growth trajectory reflects increasing demand for patient-centric formulations addressing dysphagia, pediatric applications, and geriatric populations requiring administration flexibility. These innovative systems combine the gastro-protective benefits of delayed-release technology with rapid oral disintegration, enabling medication administration without water while protecting acid-labile active ingredients. Technological breakthroughs in taste-masking, fast-disintegrating excipients, and enteric coating materials applied to pellet systems have enabled commercial viability, attracting substantial pharmaceutical investment and regulatory approvals across multiple therapeutic categories.

Dosage Form Insights

Capsules are expected to represent the top application segment, capturing approximately 52% of the multiple unit pellet system market revenue share in 2026, attributed to their manufacturing flexibility, patient acceptability, and ease of administration. Hard gelatin and hydroxypropyl methylcellulose (HPMC) capsules accommodate varying pellet quantities, enabling dose customization and combination therapy delivery. The segment benefits from well-established filling technologies, minimal excipient requirements, and straightforward regulatory pathways for both branded and generic products.

Tablets are projected to be the fastest-growing dosage form over the 2026-2033 forecast period, reinforced by patient preference for solid oral dosage forms and manufacturing economies of scale. Compressed MUPS tablets combine the stability and portability advantages of conventional tablets with the controlled-release benefits of pellet systems. Recent innovations in tablet coating technologies and disintegration-enhancing excipients have addressed historical challenges related to pellet integrity during compression, expanding commercial viability. This segment particularly appeals to manufacturers seeking to differentiate generic products through enhanced delivery profiles while maintaining familiar dosage formats.

Distribution Channel Insights

Hospital pharmacies are projected to maintain leadership within the MUPS distribution landscape, accounting for approximately 45% revenue share in 2026. This dominance reflects the concentration of modified-release prescribing within inpatient and specialized outpatient environments, where clinicians initiate therapy for complex chronic conditions. Hospital-based physicians are directly supervising treatment plans and monitoring patient response, which is supporting early adoption of advanced release technologies. These institutions are maintaining structured relationships with pharmaceutical manufacturers, influencing formulary inclusion decisions and driving uptake through clinical education programs. Hospital pharmacies are also serving as primary launch channels for newly approved MUPS formulations, as healthcare providers evaluate therapeutic performance in controlled care settings. Infrastructure capability, prescribing authority, and integrated care pathways are reinforcing the segment’s continued leadership position.

Retail pharmacies are projected to expand at the fastest rate between 2026 and 2033 as chronic disease management increasingly shifts toward ambulatory care models. Growing prevalence of long-term conditions and broader prescription drug coverage are increasing outpatient demand for sustained-release formulations. Healthcare systems are encouraging community-based treatment strategies to contain costs, which is transferring dispensing volumes from hospitals to retail networks. Retail pharmacies are integrating digital prescription platforms, medication therapy management programs, and patient counseling services that are improving access to complex dosage forms such as MUPS. These operational enhancements are strengthening adherence monitoring and refill continuity. As patient-centric care models continue evolving, retail distribution channels are becoming critical growth drivers for advanced multi-particulate drug delivery technologies.

Regional Insights

North America Multiple Unit Pellet Systems (MUPS) Market Trends

North America is projected to account for approximately 38% of the multiple unit pellet systems market share in 2026, supported by advanced pharmaceutical manufacturing capacity and sustained research and development investment. The United States is generating the majority of regional activity due to strong capital allocation toward formulation science and lifecycle management strategies. Favorable reimbursement frameworks are supporting the uptake of modified-release products in chronic disease treatment pathways. The U.S. FDA is promoting quality-by-design principles and continuous manufacturing approaches, which are encouraging process standardization and innovation in multi-particulate technologies. These regulatory initiatives are strengthening the region’s leadership in pellet-based drug delivery systems. Intellectual property protections in the United States are safeguarding proprietary pellet coating techniques and release-modulation technologies, allowing innovators to preserve competitive positioning.

Rising prevalence of chronic conditions is sustaining demand for dependable and predictable drug delivery platforms. Healthcare systems are prioritizing formulations that improve long-term adherence and clinical stability. The FDA is maintaining rigorous pre-approval evaluation and active post-market surveillance, which is reinforcing confidence in approved products while favoring experienced manufacturers with established compliance systems. The Generic Drug User Fee Amendments (GDUFA) are expediting review timelines for follow-on applications, thereby intensifying competition among qualified producers. Venture capital firms are increasing investments in pharmaceutical technology companies that are developing advanced pelletization processes and scalable manufacturing systems. Strategic organizations are leveraging regulatory clarity, reimbursement support, and capital access to consolidate market share and build durable growth trajectories within the North America MUPS market landscape.

Europe Multiple Unit Pellet Systems (MUPS) Market Trends

Europe is projected to retain a substantial share of the MUPS market in 2026 and throughout the forecast period, supported by deep pharmaceutical manufacturing expertise and strong formulation science capabilities. Germany is leading regional production due to its advanced specialty chemicals infrastructure and integrated supply chains that improve pellet coating precision and scalability. The United Kingdom, France, and Spain are contributing through diverse therapeutic portfolios and established contract manufacturing networks. The EMA is coordinating regulatory standards across member states, which is harmonizing quality expectations and reducing duplication in approval submissions. Clear EMA guidance on oral modified-release products is providing structured development pathways for both innovative and generic manufacturers, thereby enhancing regulatory predictability and operational efficiency.

European healthcare systems are sustaining demand for advanced dosage technologies that support long-term disease management. Health technology assessment bodies are applying pricing scrutiny that is placing pressure on margins, particularly for follow-on products. Germany’s Industry 4.0 initiatives are promoting smart manufacturing environments with real-time monitoring and artificial intelligence optimization, which are strengthening production reliability and cost control. The United Kingdom is maintaining regulatory alignment with the European Union while introducing procedural flexibility that may accelerate certain approvals. Investors are channeling capital into advanced drug delivery platforms, including MUPS, to capture opportunities in chronic disease treatment.

Asia Pacific Multiple Unit Pellet Systems (MUPS) Market Trends

Asia Pacific is anticipated to become the fastest-growing market for multiple unit pellet systems from 2026 to 2033, driven by expanding pharmaceutical capacity and rising domestic demand. China is strengthening its leadership position through substantial manufacturing scale and increasing consumption of advanced oral formulations. Japan is contributing precision engineering capabilities and high standards in formulation development, while India is providing cost-efficient generic manufacturing that supports global supply chains. ASEAN members are expanding healthcare infrastructure and broadening patient access to modern therapies. Pharmaceutical companies are leveraging advantages such as competitive labor costs, established active pharmaceutical ingredient (API) networks, and policy incentives that encourage domestic production. Governments are further supporting industrial development programs that accelerate the adoption of sophisticated dosage technologies. As a result, manufacturers are establishing regional production hubs to efficiently serve both local markets and export channels, reinforcing Asia Pacific’s position as a primary growth center.

Regulatory agencies across the region are strengthening oversight frameworks to enhance international credibility. China’s National Medical Products Administration (NMPA) is tightening evaluation standards to align with global quality benchmarks and build confidence in locally manufactured products. India’s generic drug industry is integrating MUPS technology to enter higher-margin segments and differentiate beyond conventional immediate-release formats. Japan is addressing demographic aging by promoting patient-friendly formulations that simplify administration and improve adherence. ASEAN economies are benefiting from rising healthcare expenditure and an expanding middle-class population that demands advanced therapies.

Competitive Landscape

The global multiple unit pellet systems market structure is moderately consolidated, with AbbVie, AstraZeneca, Dr. Reddy’s Laboratories, Merck & Co., and Pfizer collectively commanding an estimated 47.5% of total market revenues. These organizations are strengthening their competitive positions through advanced multiparticulate dosage engineering that enables controlled release kinetics, flexible strength combinations, and improved gastrointestinal tolerability in chronic disease therapies. Their formulation expertise allows precise control over pellet size distribution, coating thickness, and drug diffusion rates, which enhances therapeutic reliability and supports lifecycle management strategies. By offering customized development services, including tailored release profiles and complex combination products, these firms are reinforcing product differentiation and extending commercial longevity across mature therapeutic categories.

Commercial strategy is increasingly centered on collaborative development models involving both originator pharmaceutical companies and generic manufacturers. Leading firms are co-developing scalable MUPS platforms that reduce regulatory uncertainty and streamline submission pathways across multiple jurisdictions. Innovation pipelines are focusing on solvent-free coating techniques, high drug load pellet configurations, and optimized encapsulation or compression systems that maintain release integrity during tableting. These technical advancements are improving manufacturing efficiency, lowering environmental impact, and preserving therapeutic performance across diverse production environments.

Key Industry Developments

- In January 2026, Renata Limited received approval from the United Kingdom’s Medicines and Healthcare products Regulatory Agency (MHRA) for its esomeprazole delayed-release tablets, enabling the company to market the product in the U.K. This authorization marks a strategic expansion for Renata into regulated international markets and strengthens its global specialty pharmaceuticals portfolio.

- In January 2026, AbbVie acquired an Arizona manufacturing facility from Taro Pharmaceutical to expand its domestic production capacity for APIs and specialty formulations. The acquisition strengthens AbbVie’s U.S. manufacturing footprint and supports long-term supply chain resilience for complex therapies.

- In September 2025, Department of Pharmaceutical Science, Oriental University Indore researchers developed MUPS capsules and tablets containing coated pellets of tolbutamide, saxagliptin, and verapamil to enable controlled-release combination therapy for diabetes and hypertension, using polymers such as HPMC and Eudragit to customize release profiles for each drug.

Companies Covered in Multiple Unit Pellet Systems (MUPS) Market

- AbbVie Inc.

- AstraZeneca PLC

- Boehringer Ingelheim International GmbH

- Catalent Pharma Solutions, Inc.

- Dr. Reddy's Laboratories Ltd.

- Grünenthal GmbH

- Lonza Group AG

- Lupin Limited

- Merck & Co., Inc.

- Pfizer Inc.

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

- Tillotts Pharma AG

- Tris Pharma, Inc.

- Zydus Lifesciences Limited

Frequently Asked Questions

The global multiple unit pellet systems (MUPS) market is projected to reach US$ 4.0 billion in 2026.

The market is driven by rising chronic disease prevalence, demand for controlled drug release to improve patient compliance and efficacy, and advancements in pellet manufacturing technology.

The market is poised to witness a CAGR of 3.4% from 2026 to 2033.

Major opportunities lie in combination therapies with multi-APIs, and integration of smart/3D-printed drug delivery innovations.

AbbVie Inc., AstraZeneca PLC, Dr. Reddy's Laboratories Ltd., Merck & Co., Inc. and Pfizer Inc. are some of the key players in the market.