- Medical Devices

- Syndromic Multiplex Diagnostics Market

Syndromic Multiplex Diagnostics Market Size, Share, and Growth Forecast 2026 - 2033

Syndromic Multiplex Diagnostics Market by Application (Respiratory, Gastrointestinal, Central Nervous System, Others), End-user (Hospitals, Diagnostic Laboratories, Others), and Regional Analysis, 2026–2033

Syndromic Multiplex Diagnostics Market Size and Trend Analysis

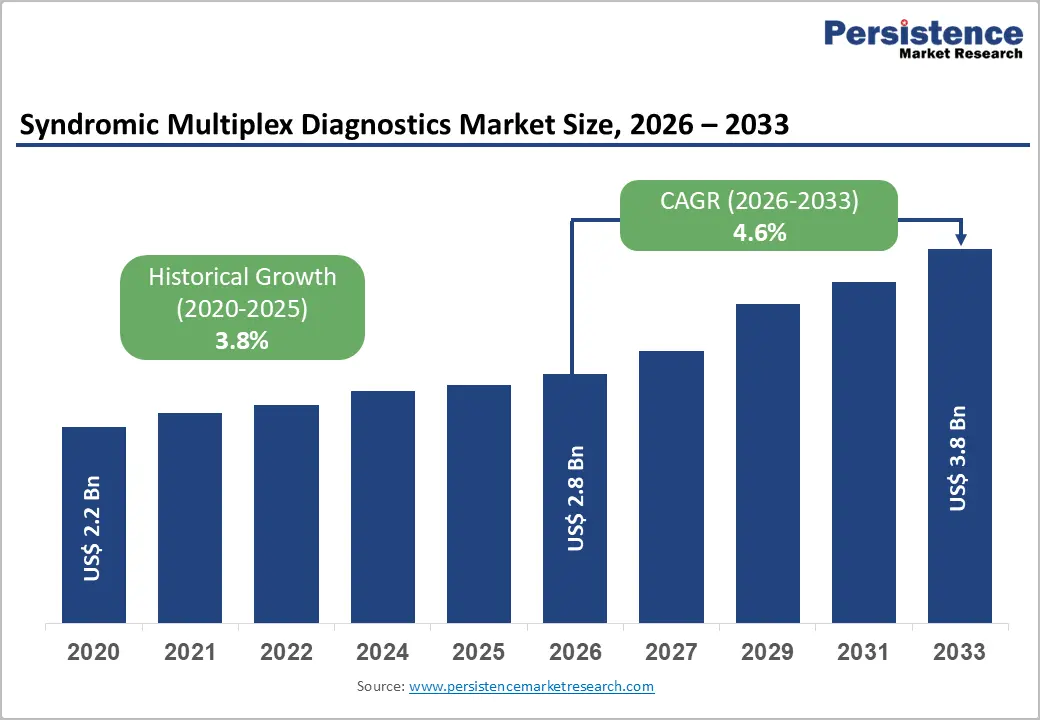

The global syndromic multiplex diagnostics market size is expected to be valued at US$ 2.8 billion in 2026 and projected to reach US$ 3.8 billion, growing at a CAGR of 4.6% between 2026 and 2033. The rising need for rapid and accurate detection of multiple pathogens from a single patient sample. These diagnostic panels help improve clinical decision-making, enable timely antimicrobial stewardship, and support better patient outcomes.

Increasing concerns over antimicrobial resistance, identified by the World Health Organization (WHO) as a major global health threat, are accelerating the adoption of advanced molecular testing solutions. Growing respiratory, gastrointestinal, and CNS infection cases, along with favorable reimbursement policies in North America and Europe, are further supporting market expansion. Additionally, rising investments in infectious disease surveillance and laboratory modernization across the Asia Pacific are expected to sustain market growth through

Key Industry Highlights

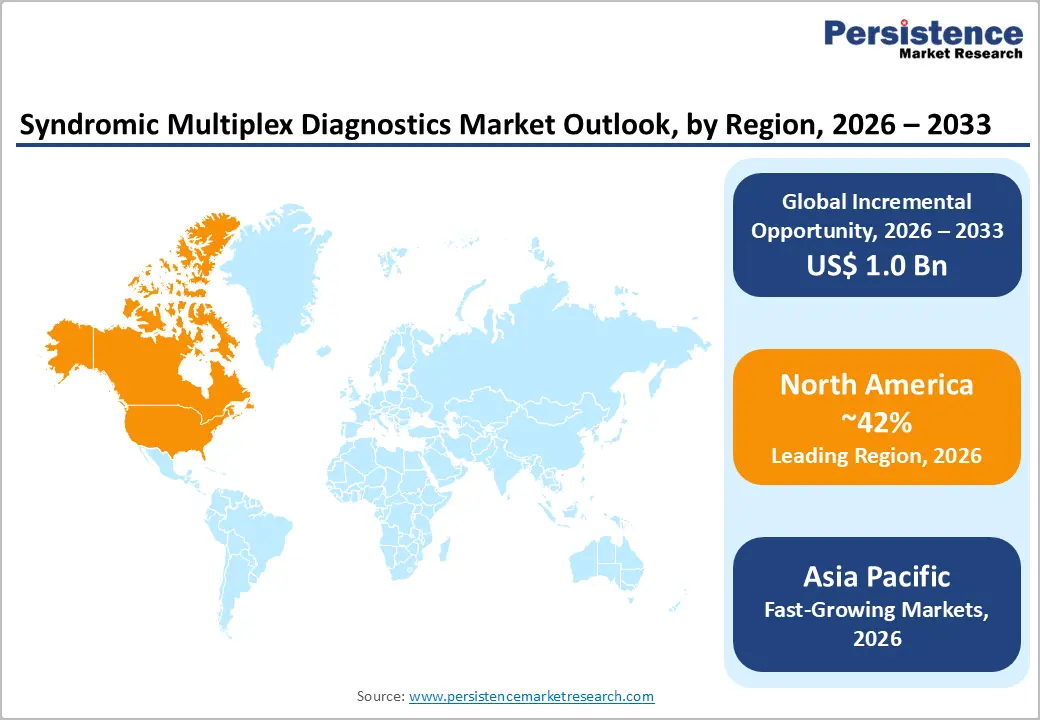

- Leading Region – North America is anticipated to generate 42% share in 2026 with strong public health initiatives and supportive reimbursement policies.

- Fastest Growing Region – Asia Pacific is the fastest-growing market driven by China’s lab expansion, India’s Ayushman Bharat growth, and Southeast Asia’s diagnostic modernization initiatives.

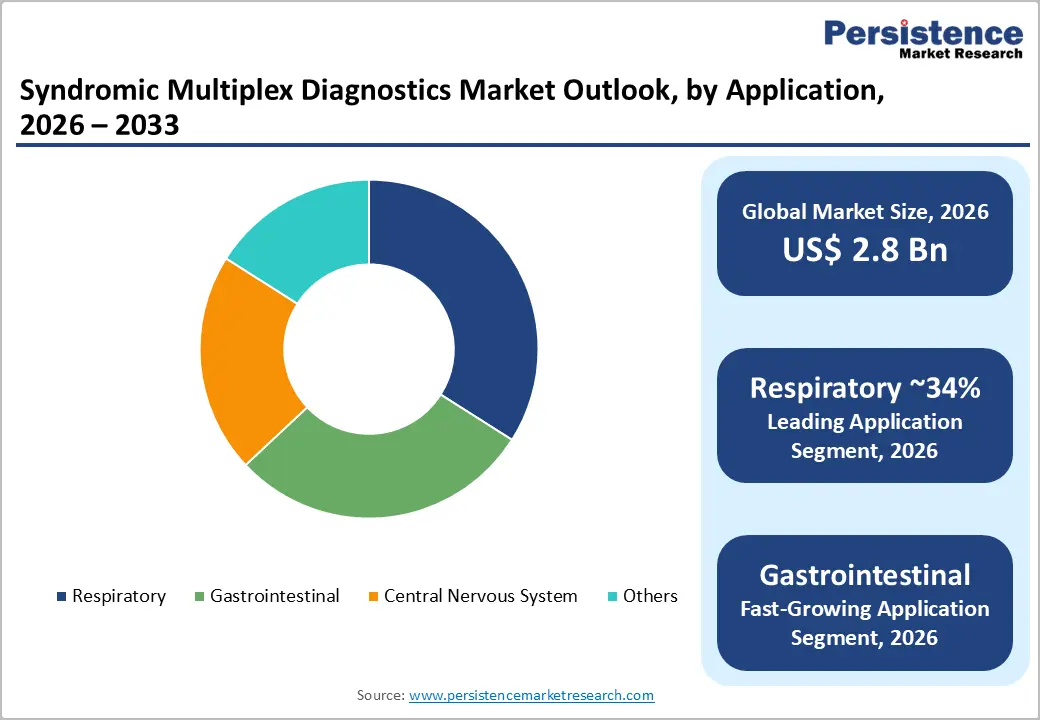

- Dominant Segment – Respiratory is the leading application with ~34% share in 2026, due to the high incidence of respiratory infections and overlapping symptoms.

- Fast-Growing Segment – Gastrointestinal syndromic panels are the fastest-growing segment, driven by updated IDSA guidelines, unmet diagnostic demand, lower penetration, and new platform launches.

- Key Opportunity – Rising investments in infectious disease surveillance programs create avenues for syndromic multiplexed diagnostics integration.

Market Dynamics

Drivers - Pandemic-Accelerated Adoption of Multiplex Respiratory Pathogen Panels

The COVID-19 pandemic fundamentally transformed clinical diagnostics by demonstrating the critical value of simultaneous pathogen detection platforms. The emergence of co-infection scenarios where SARS-CoV-2 presented alongside influenza A/B, RSV, and other respiratory pathogens drove rapid procurement of multiplex panels across hospital emergency departments globally.

The U.S. Centers for Disease Control and Prevention (CDC) estimated that respiratory illnesses caused over 3.5 million hospitalizations annually in the U.S. prior to the pandemic, a burden that intensified institutional demand for comprehensive respiratory syndromic panels. Abbott Laboratories' ID NOW and bioMérieux's BioFire Respiratory Panel achieved unprecedented adoption levels during this period, with post-pandemic demand remaining structurally elevated as clinicians recognized the antimicrobial stewardship benefits of distinguishing viral from bacterial etiology at the point of care.

Growing Antimicrobial Resistance Crisis Driving Precision Diagnostics Demand

The global antimicrobial resistance (AMR) crisis is serving as a powerful structural demand driver for syndromic multiplex diagnostics. The Lancet published a landmark 2022 study estimating that AMR was directly responsible for 1.27 million deaths globally in 2019, underscoring the urgency of rapid, accurate pathogen identification to guide targeted therapy and reduce empirical broad-spectrum antibiotic use. The WHO's Global Action Plan on Antimicrobial Resistance specifically identifies diagnostics as a cornerstone intervention. Syndromic multiplex panels, by identifying causative pathogens within one to two hours versus 24–72 hours for traditional culture, enable clinicians to de-escalate therapy rapidly, a capability increasingly mandated by hospital accreditation bodies and national stewardship program frameworks across North America, Europe, and the Asia Pacific.

Restraints - Elevated Per-Test Costs and Reimbursement Gaps in Emerging Markets

Syndromic multiplex diagnostic panels carry substantially higher per-test costs than conventional microbiological methods, ranging from US$ 200–500 for comprehensive molecular panels versus US$ 10–30 for standard cultures. In Asia Pacific, Latin America, and Middle Eastern markets, where out-of-pocket healthcare expenditure dominates, limited reimbursement coverage for advanced multiplex tests severely constrains adoption. This cost differential restricts syndromic panel utilization to tertiary hospitals and well-funded academic medical centers, leaving large patient populations in lower-income healthcare settings without access to comprehensive syndromic diagnostics.

Post-Pandemic Demand Normalization and Volume Volatility

The extraordinary volume spike in multiplex respiratory panel testing during 2020–2022 created an inflated demand baseline that has subsequently normalized, introducing short-term revenue volatility for manufacturers. bioMérieux SA reported significant revenue adjustments in its molecular diagnostics division in 2023 as COVID-specific testing volumes declined sharply. This post-pandemic normalization has led some institutional customers to defer capital investments in syndromic panel platforms, creating near-term headwinds to instrument placement growth and creating uncertainty for commercial planning cycles among manufacturers reliant on COVID-era demand levels.

Opportunities - Rapidly Expanding Gastrointestinal Syndromic Panel Adoption as Fastest-Growing Application

The Gastrointestinal (GI) application segment represents the most compelling near-term growth opportunity within syndromic multiplex diagnostics, projected to deliver the strongest CAGR through 2033. The CDC estimates 48 million Americans suffer from foodborne illness annually, yet GI syndromic multiplex panel penetration in hospital laboratories remains significantly below respiratory panel adoption rates, representing substantial untapped volume potential.

QIAGEN's QIAstat-Dx Gastrointestinal Panel and DiaSorin S.p.A.'s LIAISON MDX platform are actively expanding their GI panel menus to capture this opportunity. Furthermore, the Infectious Diseases Society of America (IDSA) has updated clinical guidelines recommending multiplex molecular testing as the preferred diagnostic approach for acute gastroenteritis, providing a strong clinical evidence foundation driving physician adoption and institutional reimbursement approval across North America and Europe.

Central Nervous System Syndromic Panel Expansion in Neurological Intensive Care Settings

Central Nervous System (CNS) syndromic panels represent a high-value, underserved growth opportunity within the syndromic multiplex diagnostics market. Meningitis and encephalitis are medical emergencies where pathogen identification speed directly impacts survival outcomes, yet traditional CSF (cerebrospinal fluid) culture results may take 48–72 hours, far too slow for optimal clinical decision-making. bioMérieux's BioFire Meningitis/Encephalitis (ME) Panel, which simultaneously detects 14 bacterial, viral, and fungal targets from CSF in ~one hour, has demonstrated the transformative clinical value of this modality.

A study published in Clinical Infectious Diseases found the BioFire ME Panel reduced time-to-targeted therapy by over 30 hours in confirmed meningitis cases. As neurology ICU investment expands across Asia Pacific and Europe, CNS panel adoption is expected to accelerate significantly, generating a high-margin incremental revenue stream for diagnostic manufacturers.

Category-wise Analysis

Application Insights

By application, the market is trifurcated into respiratory, gastrointestinal, and the central nervous system. Among these, the respiratory segment will likely generate a share of approximately 33% in 2026 due to the overlapping clinical presentations of a wide range of pathogens, which make conventional diagnosis both time-consuming and prone to error. Acute respiratory illnesses caused by viruses such as SARS-CoV-2, rhinovirus, and influenza often present with indistinguishable symptoms. This makes respiratory panels particularly valuable for differential diagnosis.

Gastrointestinal syndromic multiplex diagnostics, on the other hand, have become increasingly important owing to the high prevalence of diarrheal diseases with overlapping symptoms. These panels offer simultaneous detection of multiple pathogens, allowing clinicians to quickly pinpoint the etiology and avoid unnecessary empirical treatment. A 2023 study from the University of Zurich, for example, showed that implementing multiplex gastrointestinal panels in emergency departments resulted in a 50% reduction in antibiotic prescriptions for viral gastroenteritis cases.

End-user Insights

By end-user, the market is bifurcated into hospitals and diagnostic laboratories. Out of these, diagnostic laboratories are predicted to lead with nearly 60% of the syndromic multiplex diagnostics market share in 2026, backed by their ability to manage high sample volumes, ensure regulatory compliance for complex molecular tests, and maintain quality control standards. These laboratories possess the infrastructure required to handle multiplex assays efficiently. In 2023, for instance, France’s Résapath network used BioFire and QIAstat-Dx platforms in regional labs to process up to 600 syndromic tests daily, which is otherwise unmanageable for small clinics.

Hospitals are likely to witness a considerable growth rate in the coming years as they face urgent clinical decision-making requirements, mainly in infectious disease wards, ICUs, and emergency departments. These settings require rapid pathogen identification to initiate targeted therapy and prevent complications. The Cleveland Clinic recently deployed multiplex respiratory panels in its emergency department during the flu season. This lowered the average time to initiate appropriate antibiotic or antiviral treatment from 12 hours to under 2 hours.

Regional Insights

North America Syndromic Multiplex Diagnostics Market Trends and Insights

North America leads the global market with 42% share in 2025, supported by broad FDA clearance of multiplex syndromic panels, strong reimbursement under Medicare and Medicaid, and well-established antimicrobial stewardship program infrastructure. The region benefits from high per capita healthcare expenditure and early market access for novel syndromic diagnostic platforms from leading IVD manufacturers.

U.S. Syndromic Multiplex Diagnostics Market Size

The U.S. accounts for ~88% of North America's syndromic multiplex diagnostics revenue. The country's dense hospital network, CDC-mandated infectious disease surveillance programs, and robust clinical guideline infrastructure from the IDSA and ATS sustain the highest per-institution multiplex panel adoption rates globally, anchoring the region's market leadership.

Europe Syndromic Multiplex Diagnostics Market Trends and Insights

Europe represents the second-largest regional market, shaped by EU IVDR (Regulation 2017/746) compliance requirements, growing AMR action plan investments across member states, and increasing multiplex panel procurement under national health service frameworks. Germany, the UK, and France lead adoption, with respiratory and GI syndromic panel penetration accelerating in teaching hospitals and reference diagnostic networks.

Germany Syndromic Multiplex Diagnostics Market Size

Germany holds ~23% of European syndromic multiplex diagnostics revenue, driven by its DART 2030 national AMR strategy, which mandates structured rapid diagnostics integration in hospital antimicrobial stewardship programs. Germany's network of university hospitals and Robert Koch Institute (RKI)-affiliated surveillance laboratories provides a strong institutional base for multiplex panel adoption.

UK Syndromic Multiplex Diagnostics Market Size

The UK contributes ~18% of European market revenue, supported by NHS England's structured antimicrobial stewardship framework and UKHSA infectious disease surveillance programs. The UK AMR National Action Plan 2024–2029 specifically prioritizes rapid diagnostic deployment, creating favorable institutional procurement conditions for syndromic multiplex platforms.

France Syndromic Multiplex Diagnostics Market Size

France accounts for ~15% of European syndromic multiplex diagnostics revenues. Santé publique France's national infectious disease surveillance infrastructure and HAS-approved reimbursement pathways for validated multiplex panels have created a structured adoption environment. France's strong hospital sector and regional reference laboratory networks support consistent commercial uptake of respiratory and CNS syndromic panels.

Asia Pacific Syndromic Multiplex Diagnostics Market Trends and Insights

Asia Pacific is the fastest-growing regional market for syndromic multiplex diagnostics, driven by China's rapidly expanding hospital laboratory infrastructure with the National Medical Products Administration (NMPA) approving domestic multiplex panel platforms alongside universal health coverage expansion in India, Japan, and Southeast Asia. China alone represents ~35% of Asia Pacific market revenue, with domestic manufacturers increasingly competing with global IVD brands.

India Syndromic Multiplex Diagnostics Market Size

India contributes ~10% of Asia Pacific syndromic multiplex diagnostics revenue and is among the region's fastest-growing markets. The Ayushman Bharat healthcare expansion and rising private hospital investments are driving laboratory upgrades. High respiratory and GI infection burden including tuberculosis, typhoid, and seasonal influenza creates significant structural demand for multiplex pathogen panels.

Japan Syndromic Multiplex Diagnostics Market Size

Japan accounts for ~20% of Asia Pacific market revenues, reflecting its advanced healthcare infrastructure and rigorous Ministry of Health, Labour and Welfare (MHLW) infectious disease surveillance mandates. Japan's aging population with heightened vulnerability to severe respiratory infections, combined with high hospital investment in automated diagnostic platforms, sustains strong multiplex panel adoption, particularly for respiratory applications.

Southeast Asia Syndromic Multiplex Diagnostics Market Size

Southeast Asia contributes ~13% of Asia Pacific syndromic multiplex diagnostics revenues. Nations including Thailand, Vietnam, and Indonesia are investing in diagnostic laboratory modernization under ASEAN health security frameworks. High tropical infectious disease burden including dengue, enteric fevers, and respiratory viruses is driving increasing institutional interest in syndromic multiplex panel platforms.

Competitive Landscape

The syndromic multiplex diagnostics market houses various renowned molecular diagnostics firms and niche players focused on syndromic panels. The market is heavily influenced by constant innovation in cartridge-based automation and assay design. Key players are striving to balance comprehensive pathogen detection with ease of use and speed. Regional companies, especially in China, are developing localized multiplex diagnostics for infectious disease panels. In Europe, firms are focusing on developing portable multiplex PCR platforms for decentralized testing in low-resource settings.

Key Developments:

- In September 2024, Roche introduced the cobas® Respiratory flex test. It is the first to utilize the company’s innovative and proprietary Temperature-Activated Generation of Signal (TAGS) technology. This technology uses multiplex Polymerase Chain Reaction (PCR) testing, combined with data, temperature, and color processing to detect as many as 15 pathogens in a single PCR test.

- In September 2024, South Korea-based Seegene Inc. extended its strategic partnership with Springer Nature to introduce Nature Awards MDx Impact Grants. It is a new project for the development of diagnostic assays. The program empowers researchers globally to develop novel diagnostic assays using Seegene's innovative multiplex PCR technology.

Global Syndromic Multiplex Diagnostics Market - Key Insights & Details

|

Key Insights |

Details |

|

Historical Market Value (2020) |

US$ 2.2 Billion |

|

Current Market Value (2026) |

US$ 2.8 Billion |

|

Projected Market Value (2033) |

US$ 3.8 Billion |

|

CAGR (2026–2033) |

4.6% |

|

Leading Region |

North America, 42% market share (2026) |

|

Dominant Application |

Respiratory, ~34% market share (2026) |

|

Top-ranking End-user |

Hospitals, ~58% market share (2026) |

|

Incremental Opportunity |

US$ 1 Billion (2026–2033) |

Companies Covered in Syndromic Multiplex Diagnostics Market

- Abbott Laboratories

- bioMérieux

- Thermo Fisher Scientific, Inc.

- Hologic, Inc.

- F. Hoffmann-La Roche Ltd.

- DiaSorin S.p.A (Luminex Corporation)

- QIAGEN N.V.

- Applied BioCode

- Becton, Dickinson and Company (BD)

- Hologic, Inc.

- Others

Frequently Asked Questions

The global syndromic multiplex diagnostics market is projected to reach US$ 2.8 billion in 2026.

Key demand drivers include rising antimicrobial resistance, increasing need for rapid pathogen identification, growing respiratory panel adoption, updated GI testing guidelines, and expanding CNS panel use in intensive care settings.

North America leads the global market with 42% share in 2025.

Major growth opportunities lie in expanding gastrointestinal syndromic panel adoption and increasing CNS panel deployment in neurology ICUs, especially across the Asia Pacific and Europe, where penetration remains comparatively low.

Leading companies include bioMérieux SA, Abbott Laboratories, F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific Inc., DiaSorin S.p.A. (Luminex Corporation), QIAGEN N.V.