- Specialty & Fine Chemicals

- Monochloroacetic Acid Market

Monochloroacetic Acid Market Size, Share, and Growth Forecast 2026 - 2033

Monochloroacetic Acid Market by Grade (Technical/Industrial, USP/Chemical Grade), Form (Solid, Liquid), Application (Agrochemical Intermediates, Carboxymethyl Cellulose (CMC) Production, Pharmaceutical Intermediates, Surfactants & Detergents, Dyes, Pigments & Textile Chemicals, Others), Industry, and Regional Analysis, 2026 - 2033

Monochloroacetic Acid Market Size and Trend Analysis

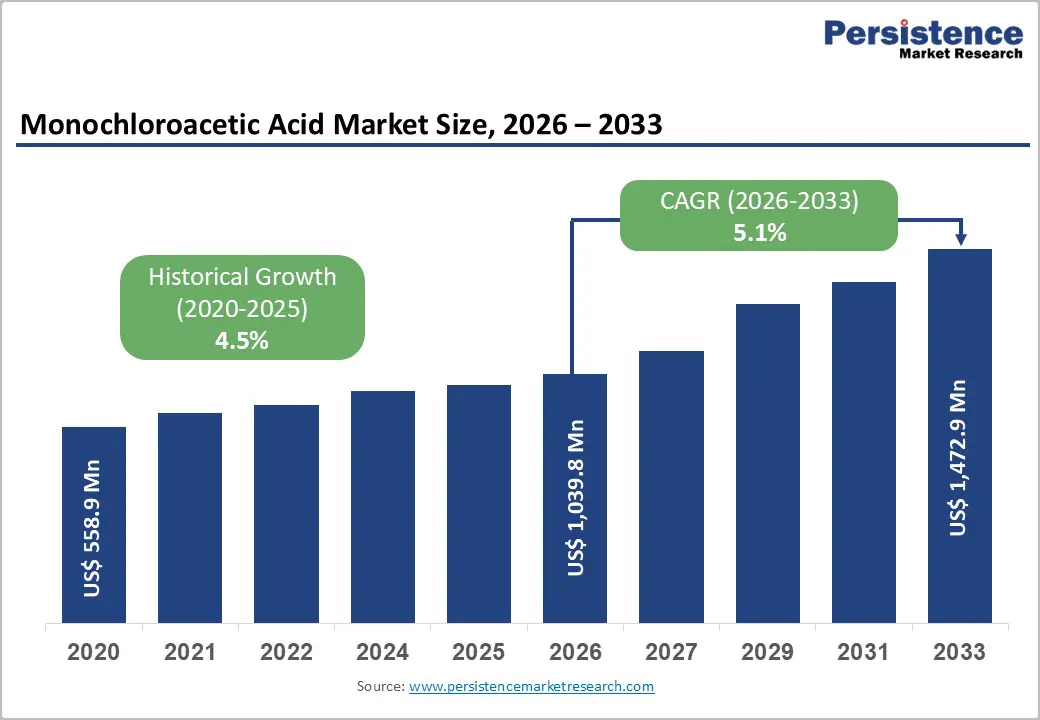

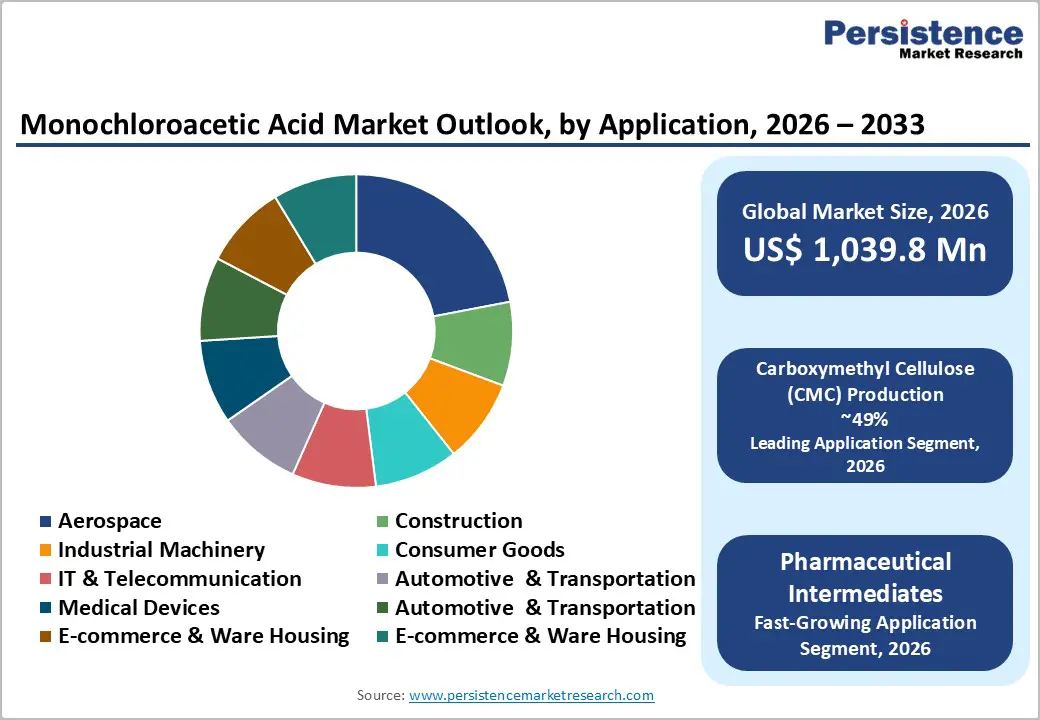

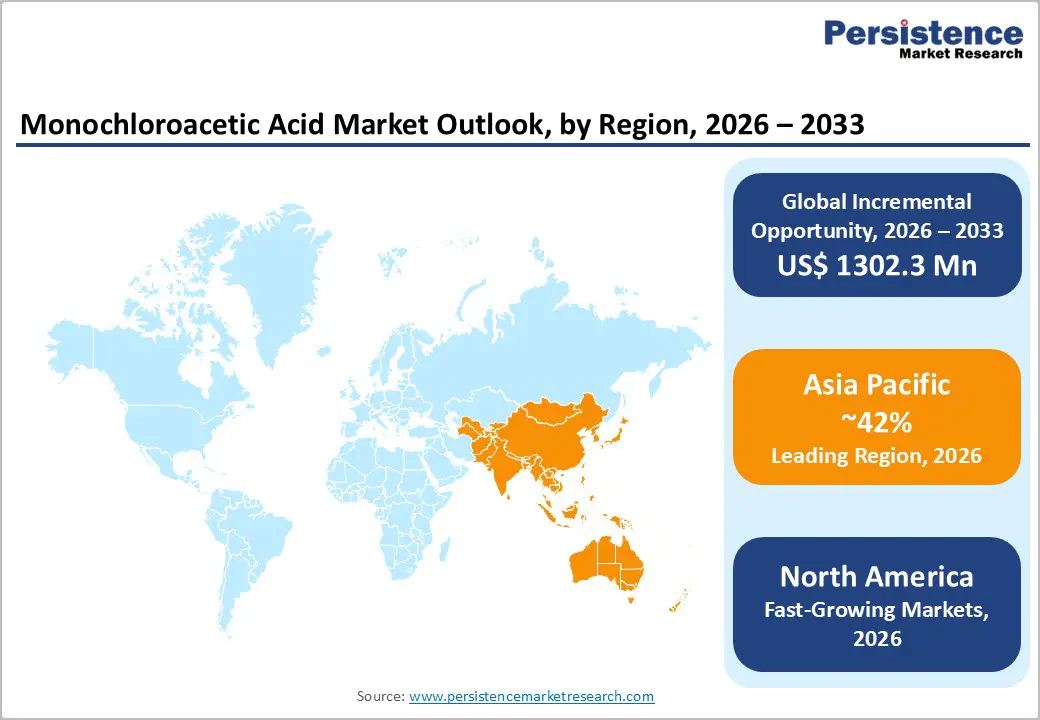

The global monochloroacetic acid market size is expected to be valued at US$ 1,039.8 million in 2026 and projected to reach US$ 1,472.9 million by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

This growth is primarily driven by increasing demand from the agrochemical and pharmaceutical industries, in which MCAA serves as a critical intermediate. Rising global food production requirements are increasing the use of agrochemicals, while ongoing pharmaceutical innovation is supporting steady consumption. Additionally, growing application of MCAA in carboxymethyl cellulose (CMC) for food processing and personal care products further strengthens demand, particularly as manufacturers emphasize high-purity inputs to meet evolving quality and regulatory standards.

Key Industry Highlights:

- Leading Region: Asia-Pacific dominates the monochloroacetic acid market with a 42% share in 2025, driven by manufacturing hubs in China and India.

- Fastest-Growing Region: Europe is growing steadily, with a 5.2% CAGR (2024 - 2030), driven by regulatory compliance and specialty applications.

- Leading Grade Category: Technical/Industrial grade leads with 68% share in 2025, ideal for bulk industrial applications in agrochemicals and CMC production.

- Fastest-Growing Grade Category: High-purity/USP grade is the fastest-growing segment, driven by pharmaceutical and specialty chemical demands.

- Leading Form: Solid form holds a 62% share in 2025 and is preferred for stability, transport, and precise dosing in industrial and pharma applications.

- Fastest-Growing Form: Liquid form is the fastest-growing, suitable for automated and continuous processing in specialty chemicals and pharmaceuticals.

- Key Opportunity: Bio-based MCA production offers growth potential amid sustainability regulations and environmental compliance trends.

| Key Insights | Details |

|---|---|

| Monochloroacetic Acid Market Size (2026E) | US$ 1,039.8 million |

| Market Value Forecast (2033F) | US$ 1,472.9 million |

| Projected Growth CAGR (2026 - 2033) | 5.1% |

| Historical Market Growth (2020 - 2025) | 4.5% |

Market Dynamics

Drivers - Significant Growth in Monochloroacetic Acid Demand Driven by Expanding Agrochemical Production Needs

Rising global agricultural production requirements are driving the consumption of monochloroacetic acid (MCA) as a critical intermediate in the synthesis of herbicides, including widely used chemicals such as 2,4-D and glyphosate. The United Nations Food and Agriculture Organization (FAO) projects that food production must increase by nearly 60% by 2050 to feed a population projected to reach 9.7 billion, thereby intensifying demand for agrochemicals.

Asia Pacific, in particular, faces shrinking arable land and changing climate conditions, which further amplify MCA usage in pesticide production. By enabling higher crop yields and supporting efficient agricultural practices, MCA ensures sustainable food supply chains while creating steady revenue opportunities for chemical manufacturers serving the agrochemical sector.

Rapid Expansion of Pharmaceutical Applications Driving High-Purity Monochloroacetic Acid Consumption

Monochloroacetic acid is a vital precursor for the manufacture of various pharmaceutical products, including vitamins, analgesics, and ibuprofen intermediates. Its application is driven by the growth of the global pharmaceutical industry, which increasingly relies on high-quality chemical intermediates to meet the demands of both generic and specialty drug production.

The World Health Organization reports that over 14 billion vaccine doses are administered annually, alongside rising chronic disease treatments, fueling MCA requirements. High-purity USP-grade MCA meets strict regulatory and quality standards, supporting innovation in biologics and drug synthesis. As pharmaceutical pipelines diversify and expand, MCA consumption rises steadily, strengthening market growth and reinforcing its role as a core industrial intermediate.

Restraints -Stringent Environmental and Safety Regulations Limiting Monochloroacetic Acid Production Expansion

Monochloroacetic acid (MCA) production is significantly affected by stringent environmental and chemical safety regulations, particularly given its corrosive and toxic properties. Regulatory frameworks, such as the European Union’s REACH legislation, require comprehensive safety data, rigorous testing, and documentation for chlorine-based intermediates, significantly increasing compliance costs for manufacturers. Industry reports indicate that adherence to these requirements can increase operational expenses by up to 20%, thereby reducing overall profitability.

Additionally, stringent wastewater treatment and emission control standards further elevate production costs. These regulatory pressures often slow capacity expansions and discourage new investments, particularly in regions with stringent chemical safety norms, such as Europe. As a result, producers must carefully balance regulatory compliance with operational efficiency to maintain competitiveness in the global MCA market.

Raw Material Price Volatility Posing Challenges to Monochloroacetic Acid Profitability

The profitability of MCA production is closely tied to the cost of its key feedstocks, chlorine and acetic acid, both of which are highly susceptible to market fluctuations. In 2024, chlorine prices in Europe surged by 15-20% due to energy crises and supply constraints, disrupting chemical supply chains and increasing production expenses for manufacturers reliant on stable petrochemical inputs.

Such price volatility not only affects profit margins but can also lead to intermittent production slowdowns, contract renegotiations, and challenges in long-term planning. Manufacturers must implement risk mitigation strategies, including hedging and supplier diversification, to maintain consistent output while managing cost uncertainties. This restraint continues to challenge MCA producers globally, particularly in regions with fluctuating energy and feedstock markets.

Opportunities - Innovative Bio-Based Production Methods Present Sustainable Growth Opportunities in MCA

Advancements in sustainable and bio-based production of monochloroacetic acid (MCA) are creating significant market opportunities for producers seeking to reduce their carbon footprints and meet environmental targets. Emerging enzymatic and green chemistry processes allow manufacturers to align with global initiatives, including the European Union Green Deal, which aims for a 55% reduction in emissions by 2030. These eco-friendly synthesis routes not only improve environmental compliance but also enhance brand reputation.

Producers targeting pharmaceutical and high-purity applications can leverage these innovations to command premium pricing for bio-based MCA. Investments in research and partnerships focused on green chemistry can accelerate adoption, reduce dependency on traditional chlorination methods, and create differentiation in a competitive market. This strategic focus positions companies to capture a growing segment of environmentally conscious consumers and downstream industries.

Rising Demand for Carboxymethyl Cellulose (CMC) in Personal Care Boosts MCA Applications

The increasing use of monochloroacetic acid in the production of carboxymethyl cellulose (CMC) presents a lucrative opportunity, particularly in the personal care sector. Post-pandemic hygiene awareness has led to increased consumption of CMC as a thickener and stabilizer in cosmetics, skincare, and other personal care formulations. Industry associations report that CMC demand is growing at 4-5% annually, with Asia Pacific leading due to rising disposable incomes and expanding consumer markets.

Companies investing in this application benefit from high-margin segments while diversifying downstream revenue streams. By focusing on demand driven by personal care and hygiene, MCA producers can strengthen their market position, capitalize on emerging consumer trends, and expand their presence in regions with rapidly evolving lifestyles and consumption patterns.

Category-wise Analysis

Grade Insights

The Technical/Industrial grade dominates the MCAA market with a 68% share in 2025, driven by its cost-effectiveness for bulk applications in agrochemicals and surfactants. Its lower purity is sufficient for large-scale carboxymethyl cellulose (CMC) and detergent production, where volume is prioritized over precision. Manufacturing hubs in China, producing over half of global herbicides, exemplify the efficiency and scale benefits of this grade, reinforcing its leadership position in industrial processes.

High-purity/USP-grade MCA is emerging as the fastest-growing segment, driven by expanding pharmaceutical and specialty chemical applications. Its stringent compliance with regulatory standards makes it essential for drug intermediates, biologics, and high-value CMC production, positioning producers targeting precision markets for higher margins and consistent demand growth globally.

Form Insights

The solid form leads the market with a 62% share in 2025 due to its stability, crystalline structure, and ease of storage and transport. It reduces corrosion risk relative to liquid MCA, making it suitable for pharmaceutical and agrochemical formulations that require precise dosing. Global trade data indicate that solid MCA shipments predominate, reflecting widespread adoption across industrial supply chains and bulk chemical distribution networks.

The liquid form is the fastest-growing category, preferred for continuous processing in chemical plants. Its suitability for automated blending, precise reactions, and integration into downstream production lines drives adoption in specialty chemicals, CMC, and surfactant synthesis, particularly where handling efficiency and process automation are key priorities.

Application Insights

Carboxymethyl cellulose (CMC) production accounts for the largest share at 49% in 2025, with MCA reacting with cellulose to form thickeners essential for the food, pharmaceutical, and oil drilling industries. Global CMC consumption exceeds 1 million tons annually, underscoring its critical role as a stabilizer, binder, and viscosity modifier across multiple sectors. This dominance is reinforced by MCA’s versatility and compatibility in large-scale CMC synthesis.

Emerging applications of pharmaceutical intermediates are growing rapidly, as MCA serves as a precursor to vitamins, analgesics, and other high-purity drugs. Innovations in biologics, generics, and specialty pharmaceuticals continue to expand the use of MCA in precise chemical synthesis, opening new high-margin opportunities for manufacturers worldwide.

Industry Analysis

The agrochemical industry accounts for the largest share of end-user consumption, with a 35% share in 2025, primarily for herbicide synthesis amid rising global crop protection needs. FAO data shows pesticide demand in developing regions growing 2-3% annually, driving MCA usage for efficient and large-scale herbicide production. This leadership is supported by intensive farming practices and the need to enhance food security through higher crop yields.

The pharmaceutical industry is the fastest-growing end-user segment, driven by the rising demand for high-purity MCA in drug intermediates and biologics. Expanding healthcare needs, chronic disease treatments, and vaccine production fuel consumption, creating new opportunities for manufacturers targeting specialized, regulated markets.

Regional Insights

North America Monochloroacetic Acid Market Trends

North America accounts for 28% of the global market in 2025, led by the U.S. Robust chemical infrastructure, advanced production technologies, and strong innovation ecosystems support high-purity MCA for pharmaceuticals and carboxymethyl cellulose (CMC) used in food processing. EPA regulations ensure safe handling and quality compliance, fostering trust in specialty chemical supply chains and enhancing market reliability.

Recent capacity expansions by regional producers have strengthened supply stability, thereby meeting the growing demand for herbicides and crop protection chemicals. Additionally, investments in R&D for sustainable and environmentally friendly production processes position North America to maintain leadership in high-value MCA applications, particularly in pharma and food-grade intermediates.

Europe Monochloroacetic Acid Market Trends

Europe’s monochloroacetic acid market is characterized by steady growth, with a 5.2% CAGR between 2024 and 2030, driven by stringent regulations and technological innovation. Germany, the U.K., France, and Spain lead regional demand through regulatory harmonization under REACH, ensuring safe handling of corrosive chemicals and promoting high-purity MCA usage.

Nouryon’s 2024 expansion of its Netherlands facility underscores investment in sustainable production to meet pharmaceutical and specialty chemical needs. The market benefits from environmental compliance requirements that boost adoption of MCA in dyes, textiles, and specialty applications, reinforcing Europe’s position as a high-value, quality-focused regional market.

Asia Pacific Monochloroacetic Acid Market Trends

Asia Pacific dominates global production with a 42% share in 2025, driven by China, India, and ASEAN countries. China accounts for over 40% of global MCA production, largely to meet herbicide and agrochemical demand, while India’s expanding agricultural sector further drives regional consumption. Cost-efficient manufacturing, lower labor costs, and economies of scale confer a competitive advantage on bulk industrial-grade MCA.

Government initiatives such as Made in China 2025 support capacity expansion, technology upgrades, and export competitiveness. Rapid industrialization, growing pharmaceutical production, and increasing CMC consumption for food, personal care, and specialty chemicals position the region as the fastest-growing and most strategic market globally.

Competitive Landscape

The monochloroacetic acid market exhibits a consolidated structure, with leading producers controlling a significant majority of global production through integrated operations. Market strategies focus on capacity expansions, technological upgrades, and innovation in low-emission and sustainable production processes, ensuring consistent supply and compliance with stringent regulatory standards.

Key differentiators among players include high-purity certifications, adherence to environmental regulations, and sustainable sourcing of raw materials. Emerging business models emphasize bio-based MCA production, regional partnerships, and joint ventures, allowing manufacturers to expand geographically, serve niche high-value segments, and meet growing demand across agrochemical, pharmaceutical, and specialty chemical applications.

Key Developments:

- In March 2024, Nouryon announced an expansion of its monochloroacetic acid production capacity at its Netherlands facility to address rising global demand from agrochemical and pharmaceutical sectors, aiming to strengthen supply reliability and support high-purity MCA applications across international markets.

- In February 2024, CABB Group invested USD 16.35 million to upgrade its MCA manufacturing facilities in Germany, enhancing operational efficiency and meeting the increasing requirements of pharmaceutical applications, while reinforcing compliance with quality standards and supporting growth in high-value, regulated chemical intermediates.

- In 2024, AkzoNobel completed a 25% expansion of its MCA production capacity, focusing on sustainable and environmentally friendly processes. The move aims to strengthen global supply, improve low-emission production, and meet the growing demand from pharmaceuticals, agrochemicals, and specialty chemical applications.

Companies Covered in Monochloroacetic Acid Market

- Nouryon

- CABB Group

- AkzoNobel

- Tiande Chemical

- FMC Corporation

- Dow Chemical

- Niacet

- Meridian Chem-Bond Ltd.

- Shri Chlorchem

- China Pingmei Shenma Group

- Jiangsu New Century Salt Chemistry

Frequently Asked Questions

The global monochloroacetic acid market is expected to reach US$ 1,039.8 million in 2026.

Rising agrochemical demand for herbicides like glyphosate drives MCA consumption amid growing global food production needs.

Asia Pacific leads with 42% share in 2025, driven by manufacturing hubs in China and India.

Bio-based production innovations align with green regulations, opening premium sustainable segments.

Leading players include Nouryon, CABB Group, AkzoNobel, and Tiande Chemical.