- Biotechnology

- Metabolic Testing Market

Metabolic Testing Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Metabolic Testing Market by Product (CPET Systems, Metabolic Carts, Body Consumption Analyzers, ECGs/EKGs Attachable to CPET Systems, Software), Technology (VO2 Max Analysis, RMR Analysis, Body Composition Analysis), Application (Lifestyle Diseases, Critical Care, Human Performance Testing, Dysmetabolic Syndrome X, Metabolic Disorders, Others), End User (Pharmaceutical and Biotechnology Companies, Academic & Research Institutes, Others), and Regional Analysis from 2026 to 2033.

Metabolic Testing Market Size and Trends

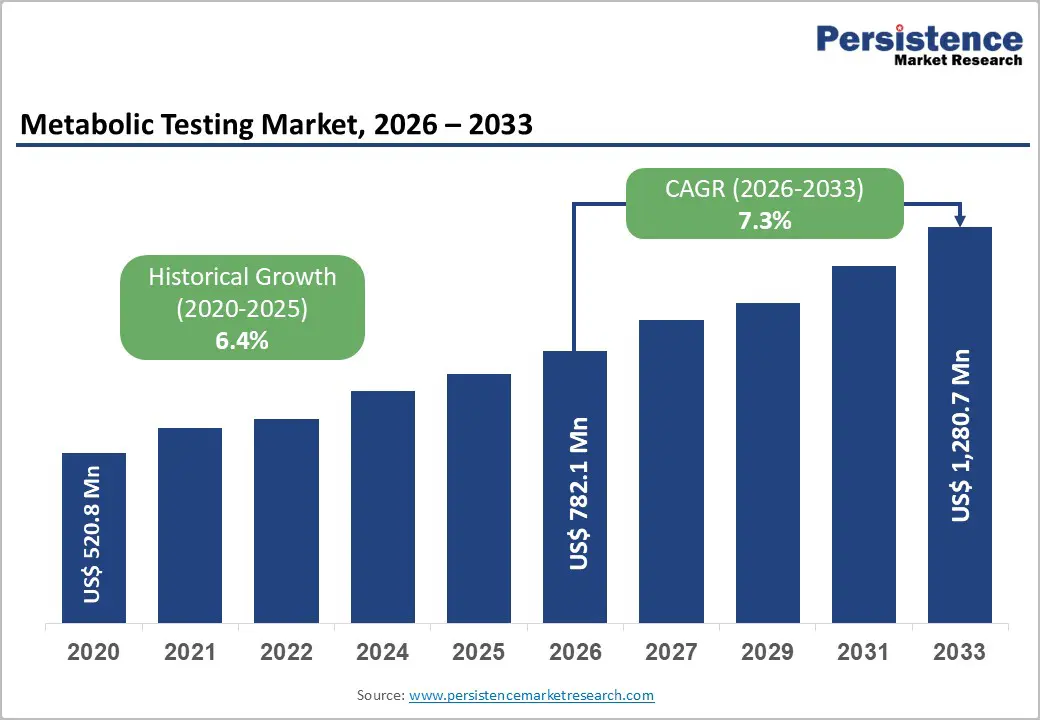

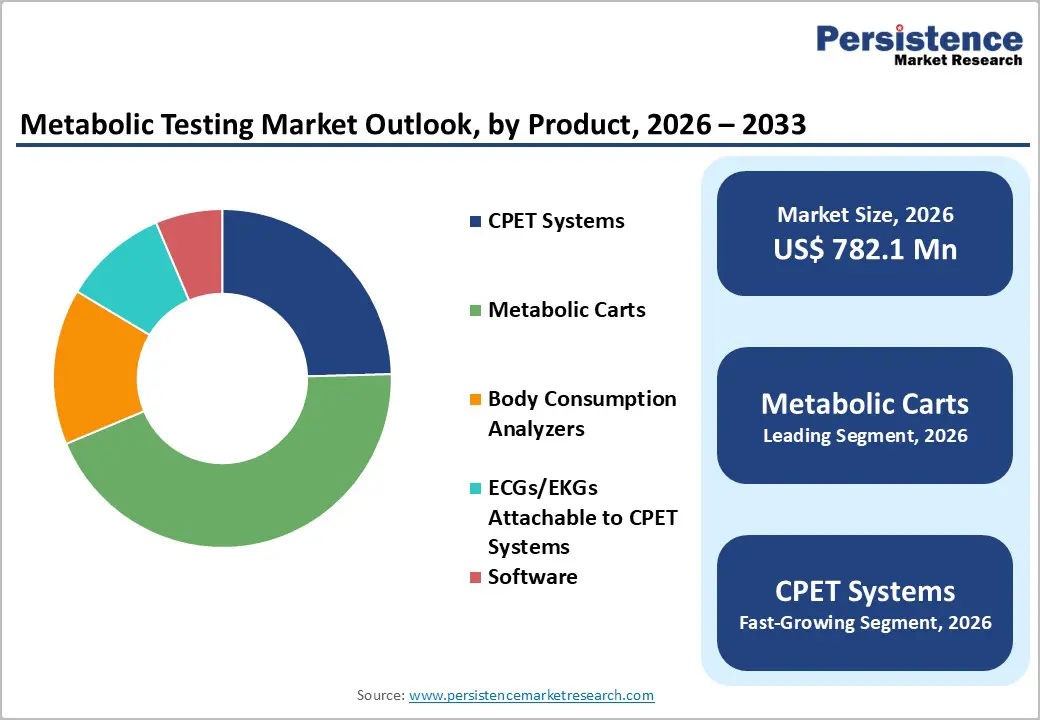

The global metabolic testing market is estimated to grow from US$ 782.1 Mn in 2026 to US$ 1,280.7 Mn by 2033. The market is projected to record a CAGR of 7.3% during the forecast period from 2026 to 2033.

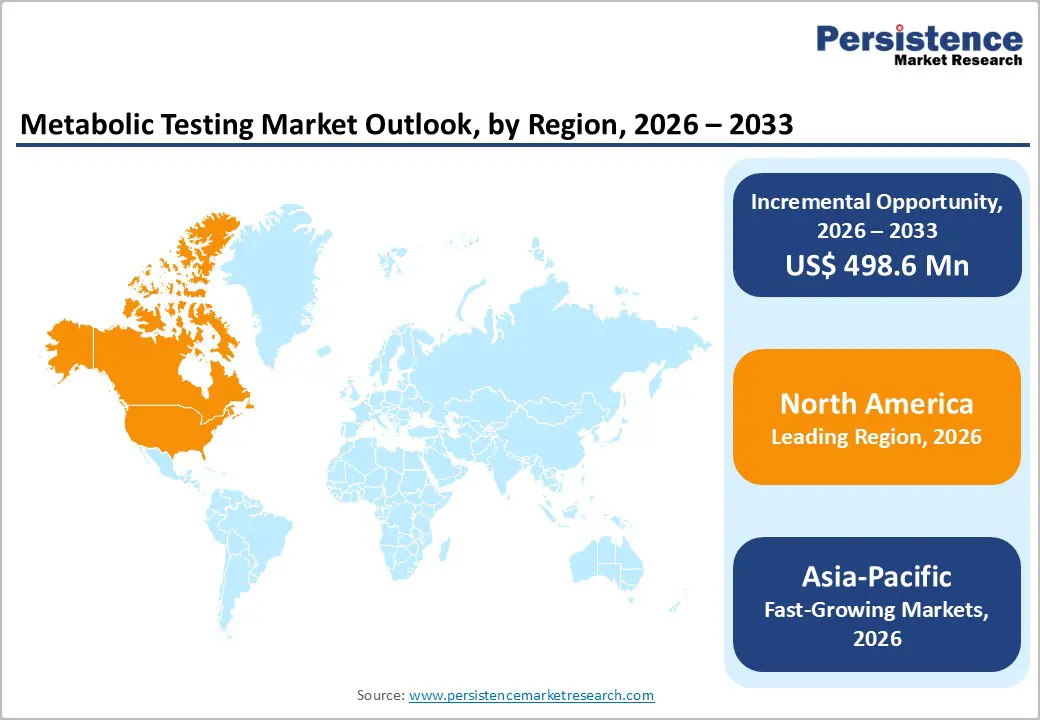

The global metabolic testing market is growing steadily, fueled by digital healthcare adoption, telehealth, and advanced analytics. North America leads with robust infrastructure, strict regulations, and high-quality laboratory standards. Asia-Pacific is the fastest-growing region, driven by expanding healthcare facilities, government digital initiatives, rising patient awareness, and increased investments in diagnostic software, services, and interoperable testing solutions.

Key Industry Highlights

- Dominant Segment: Metabolic Carts holds 44.1% share in the Metabolic Testing Market by product, driven by widespread use in clinical exercise testing, cardiopulmonary assessments, and metabolic rate evaluations. Their accuracy, reproducibility, and compatibility with high-throughput and digital monitoring systems enable precise patient assessment, optimized exercise and nutrition planning, improved clinical outcomes, and seamless integration with health IT and laboratory information systems.

- Dominant Region: North America leads with 45.0% market share, supported by advanced healthcare infrastructure, strong regulatory frameworks, and high adoption of routine metabolic screening. Asia-Pacific is the fastest-growing region, fueled by expanding healthcare facilities, rising prevalence of metabolic disorders, government health initiatives, and increasing investments in diagnostic laboratories and digital testing solutions.

- Market Drivers: Growth is driven by rising prevalence of diabetes and obesity, increasing demand for early diagnosis, advances in assay technologies, and integration of digital health monitoring systems.

- Market Opportunity: Key opportunities include point-of-care metabolic testing, AI-enabled diagnostics, multiplex metabolic panels, personalized disease management, integration with telehealth, and expansion in emerging healthcare markets.

| Global Market Attributes | Key Insights |

|---|---|

| Global Metabolic Testing Market Size (2026E) | US$ 782.1 Mn |

| Market Value Forecast (2033F) | US$ 1,280.7 Mn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Dynamics

Driver: Rising prevalence of metabolic disorders, including diabetes, obesity, and cardiovascular diseases

The rising prevalence of metabolic disorders such as diabetes, obesity, and cardiovascular diseases is a major driver of the Metabolic Testing Market because these conditions require ongoing diagnosis, monitoring, and management. In India, a comprehensive ICMR study reported that the prevalence of diabetes reached 11.4%, affecting about 101?million people, with pre?diabetes in another 15.3% of adults. Additionally, generalized obesity was present in 28.6?% and hypertension in 35.5% of the population, highlighting widespread metabolic risk factors. These conditions contribute to increased clinical demand for metabolic testing to monitor glucose, lipid profiles, and cardiovascular risk indicators, reinforcing the need for expanded diagnostic capacity.

Globally, metabolic disorders have escalated substantially; prevalence of diabetes among adults has roughly doubled over recent decades, reflecting broader trends in lifestyle?related conditions. Elevated body mass index and hypertension, both linked to metabolic dysfunction, increase the risk of heart disease, stroke, and other complications, driving healthcare providers to prioritize early detection and routine metabolic assessment. Regular metabolic testing enables clinicians to identify abnormalities in glucose tolerance, lipid levels, and blood pressure, which supports effective disease management and prevention strategies. This sustained clinical demand underpins market expansion for metabolic diagnostic solutions in hospitals, clinics, and preventive health programs worldwide.

Restraints: Inconsistent reimbursement policies across regions for metabolic testing

Inconsistent reimbursement policies across regions for metabolic testing restrict the metabolic testing market because coverage varies widely among health systems, payers, and national programs. Diagnostic reimbursement rates differ by payer type and geography, with some insurers reimbursing at levels that do not cover actual test costs, forcing laboratories to absorb financial losses. Healthcare providers often navigate complex reimbursement systems and variable coding requirements, and some tests may be denied coverage due to policy limitations or perceived lack of medical necessity. These inconsistencies can discourage investment in metabolic diagnostics and limit patient access to testing services, particularly where reimbursement frameworks are underdeveloped or unclear.

Regional reimbursement disparities also drive unequal access to metabolic testing. For example, U.S. Medicare and Medicaid programs follow different fee schedules and coverage criteria compared with private insurers, and reimbursement cuts such as those under the Protecting Access to Medicare Act (PAMA) have reduced payment for laboratory services, potentially limiting test availability. In contrast, many low and middle income countries lack comprehensive coverage for diagnostics under public insurance schemes, leaving patients to pay out of pocket for essential metabolic assessments. This fragmentation in reimbursement policy across regions creates barriers to uniform adoption of metabolic testing, slows market growth, and perpetuates inequities in diagnostic access.

Opportunity: Development of portable and point-of-care metabolic testing solutions

The development of portable and point of care (POC) metabolic testing solutions is a significant opportunity for the metabolic testing market because these tools enable rapid, decentralised assessment of key metabolic indicators close to the patient. POC devices, such as handheld glucose meters, allow immediate results without laboratory infrastructure, supporting timely clinical decisions and improved disease management, particularly for diabetes care. These devices are increasingly used outside traditional labs, including hospitals, clinics, and home settings facilitating broader access to metabolic monitoring and reducing turnaround time for results.

The value of portable POC testing is underscored by the rapid growth of POC glucose monitoring, an integral part of metabolic assessment. According to FDA documentation, there has been a marked rise in POC and at?home diagnostic testing, driven by innovations that bring lab quality assays into accessible formats. Glucose meters and related POC analyzers are widely used to track glycemic status in diabetes, a metabolic disorder affecting hundreds of millions globally, with over 537 million adults living with diabetes as reported by the International Diabetes Federation. This trend toward accessible metabolic testing solutions supports better chronic disease management and expands market potential.

Category-wise Analysis

By Product, Metabolic Carts Dominates the Metabolic Testing Market

Metabolic Carts occupies 44.1% share of the global market in 2025, because they provide precise, real-time measurements of energy expenditure, oxygen consumption, and carbon dioxide production, which are critical for assessing metabolic function in patients with obesity, diabetes, and other metabolic disorders. Indirect calorimetry using metabolic carts is considered the clinical gold standard for determining caloric needs, guiding nutrition therapy, and monitoring cardiopulmonary health. Their accuracy, reproducibility, and ability to integrate with digital health systems make them indispensable in hospitals, research institutions, and specialized clinics. This combination of precision and clinical utility drives their widespread adoption and establishes metabolic carts as the leading product segment in metabolic testing.

By Technology, RMR Analysis dominates by accurately measuring energy expenditure, guiding personalized nutrition, obesity, and metabolic disorder management

Resting Metabolic Rate (RMR) analysis dominates the metabolic testing market because it measures the largest component of total daily energy expenditure, typically 60–70?% of a person’s energy use at rest making it indispensable for accurate metabolic assessment and clinical decision?making. RMR provides an objective basis for determining daily caloric needs, guiding treatment of obesity, diabetes, and cardiovascular risk, and tailoring nutrition and weight?management plans, far beyond estimates from predictive equations. Reliable RMR measurement, usually via indirect calorimetry, informs individualized care and helps avoid under or over feeding in clinical settings, which supports better outcomes and broader clinical adoption.

Regional Insights

North America Metabolic Testing Market Trends

North America dominates the metabolic testing market with 45.0% share in 2025, because its advanced healthcare infrastructure and high chronic disease burden drive extensive diagnostic demand. The United States and Canada possess well established clinical laboratory networks and comprehensive screening programs, supported by federal regulatory standards like CLIA that ensure reliable test results and widespread adoption of metabolic assessments. Because metabolic disorders such as diabetes and obesity are highly prevalent U.S. adults with obesity often exhibit significantly higher diabetes rates clinicians increasingly rely on metabolic testing for diagnosis and management. Regular blood glucose and metabolic screenings are common in preventive care, reflecting regional emphasis on early detection, personalized treatment, and robust healthcare spending that supports advanced diagnostic technologies and broad patient access.

Europe Metabolic Testing Market Trends

Europe is an important region in the metabolic testing market because its well?established healthcare systems, strong regulatory frameworks, and high burden of metabolic disorders drive sustained diagnostic demand. Universal healthcare in countries such as Germany, France, and the United Kingdom ensures broad access to metabolic screenings like glucose and lipid assessments, supporting early detection and chronic disease management. The WHO European Region has tens of millions of adults living with diabetes, reinforcing the need for regular metabolic testing. European public health initiatives emphasize preventive medicine and standardized diagnostics, integrating metabolic panels into routine patient care and enhancing regional clinical utility.

Asia-Pacific Metabolic Testing Market Trends

Asia Pacific is the fastest growing region in the metabolic testing market due to a rapidly increasing burden of metabolic disorders and expanding healthcare infrastructure. The region is home to hundreds of millions living with type 2 diabetes, with estimates indicating around 227 million people affected, and many unaware of their condition, underscoring substantial unmet diagnostic demand. Rising obesity and metabolic syndrome prevalence further fuel demand for diagnostic testing, as nearly one fifth or more of adults in several Asia Pacific countries have metabolic syndrome. At the same time, government health initiatives and expanding laboratory services strengthen capacity for metabolic assessments, enabling broader screening and monitoring.

Market Competitive Landscape

Leading companies in the metabolic testing market focus on advanced assay development, scalable platforms, and regulatory compliance. Investments in process optimization, AI-enabled analysis, and high-throughput testing improve accuracy and reproducibility. Collaborations with healthcare institutions and research organizations accelerate innovation, while quality control, standardized protocols, and integrated supply chains support widespread adoption in clinical diagnostics and preventive metabolic care.

Key Industry Developments:

- In November 2025, OSI Systems received a $20 million order to supply radiation monitoring solutions. The contract expanded the company’s deployment of advanced detection and monitoring systems, supporting safety and regulatory compliance across critical facilities.

- In October 2024, MGC Diagnostics Corporation received 510(k) substantial equivalence clearance from the FDA for its Ascent™ Cardiorespiratory Diagnostic Software. The approval confirmed that the software met regulatory standards and was comparable to existing legally marketed devices.

Companies Covered in Metabolic Testing Market

- CareFusion Corporation

- General Electric Company

- Geratherm Medical AG

- MGC Diagnostics Corporation

- OSI Systems, Inc.

- AEI Technologies, Inc.

- Cortex Biophysik GmbH

- COSMED

- Korr Medical Technologies, Inc.

- Microlife Medical Home Solutions, Inc.

- Parvo Medics, Inc.

Frequently Asked Questions

The global metabolic testing market is projected to be valued at US$ 782.1 Mn in 2026.

Rising metabolic disorders, demand for early diagnosis, technological advancements, and expanding healthcare infrastructure drive market growth.

The global metabolic testing market is poised to witness a CAGR of 7.3% between 2026 and 2033.

Opportunities include point-of-care testing, wearable devices, AI integration, multiplex panels, and expansion in emerging markets.

CareFusion Corporation, General Electric Company, Geratherm Medical AG, MGC Diagnostics Corporation, OSI Systems, Inc., AEI Technologies, Inc.