- Clothing, Footwear, & Accessories

- Lingerie Market

Lingerie Market Size, Share, and Growth Forecast 2026 - 2033

Lingerie Market by Product Type (Briefs, Bras, Shapewear, Sports Lingerie, Others), Material (Cotton, Lace, Silk, Satin, Nylon, Others), Price (Mass, Premium, Luxury), Sales Channel (Specialty Stores, Department Stores, Supermarkets/Hypermarkets, Online channels, Others), by Regional Analysis, 2026 - 2033

Lingerie Market Size and Trend Analysis

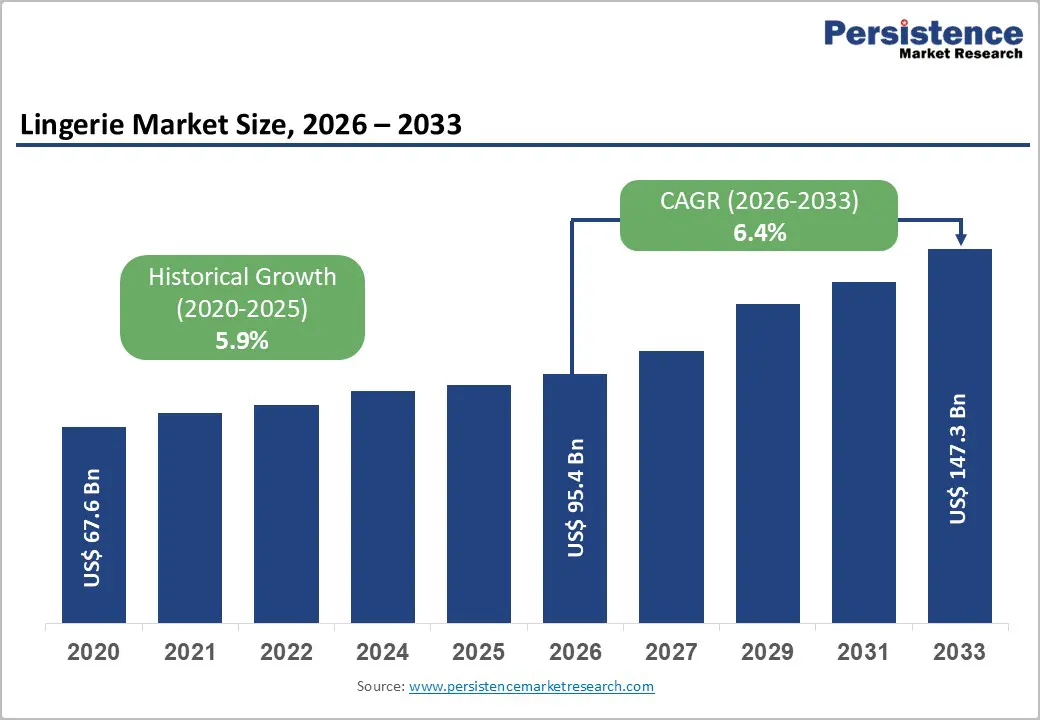

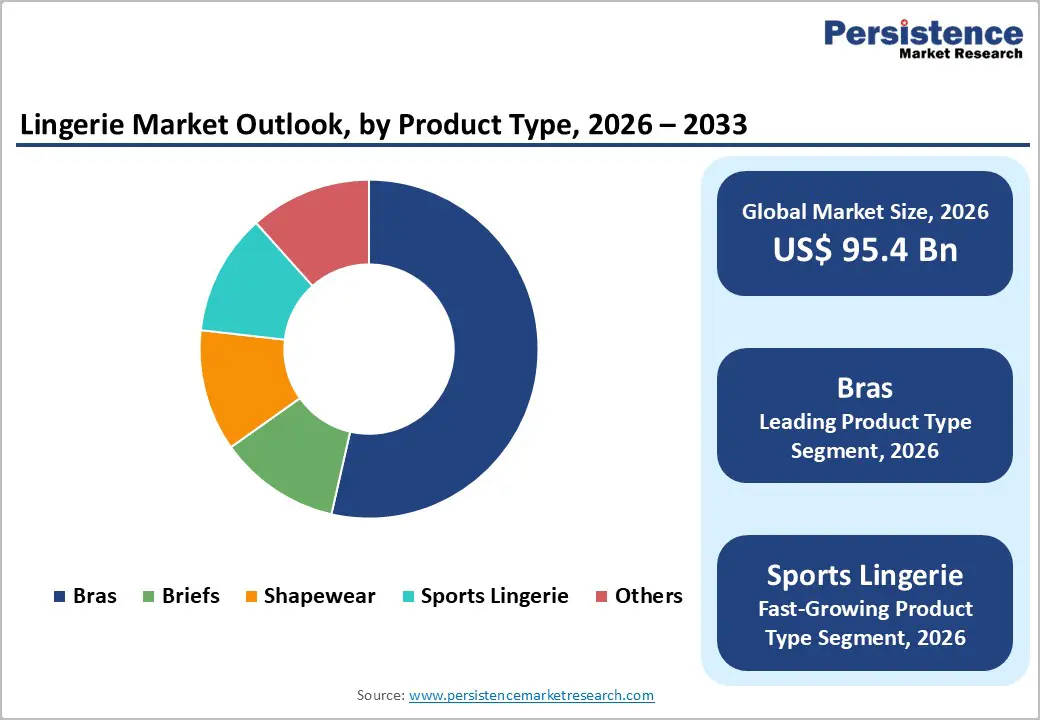

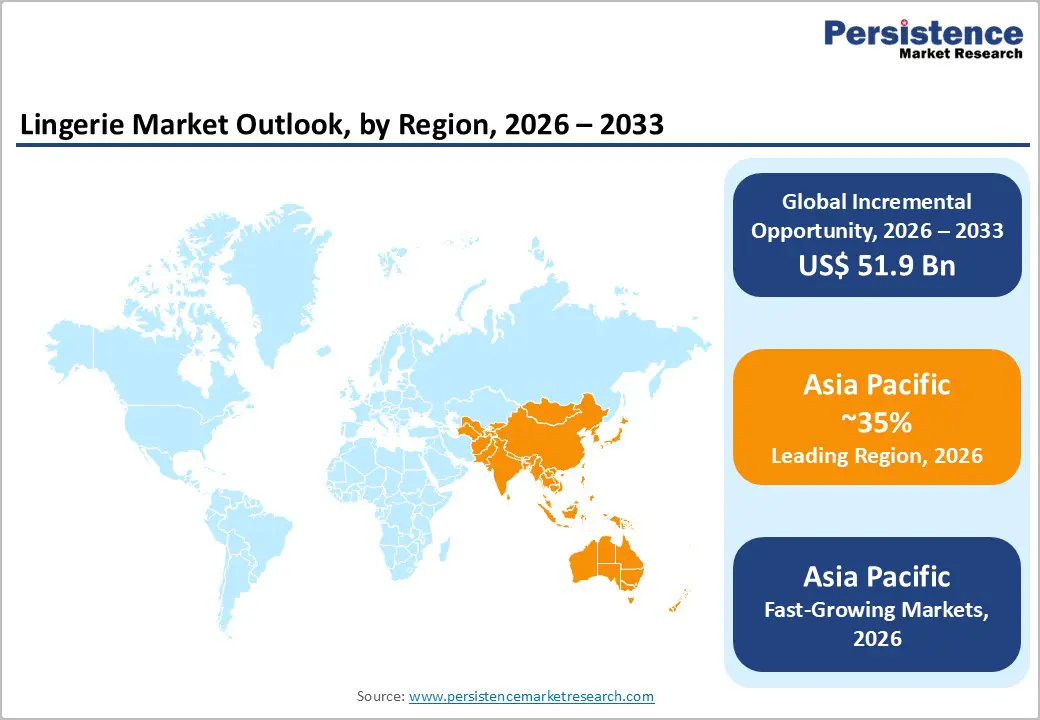

The global lingerie market size is expected to be valued at US$ 95.4 billion in 2026 and projected to reach US$ 147.3 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033. The lingerie market is experiencing robust expansion driven by a convergence of factors reshaping consumer preferences and purchasing behavior. Body positivity and inclusivity movements have catalyzed a 30% increase in sales for brands actively promoting diverse sizing and authentic representation.

Simultaneously, the explosive growth of e-commerce platforms and digital commerce channels has fundamentally transformed distribution landscapes, with online penetration accelerating beyond traditional retail. Additionally, rising female workforce participation and increasing disposable incomes, particularly across emerging markets in the Asia Pacific, are generating sustained demand for premium and diverse lingerie offerings beyond basic functional requirements.

Key Market Highlights

- Largest Regional Market: Asia Pacific commands 35% global market share in 2025, driven by enormous consumer populations, urbanization acceleration, rising female workforce participation, and expansion of middle-class purchasing power across China, India, and ASEAN nations, generating sustained demand for premium and diverse lingerie offerings.

- Fastest-Growing Region: Asia Pacific is the fastest-growing geographic segment, with emerging markets such as India and Southeast Asia expanding at double-digit CAGR driven by e-commerce penetration, digital infrastructure development, and consumer preference shifts toward organized retail formats and online shopping platforms.

- Dominant Product Segment: The brassiere segment maintains dominance with 56% global market share in 2025, commanding leadership through continuous innovation in comfort technologies, wireless designs, and size-inclusive offerings that address evolving consumer preferences for wearability and diverse body type accommodation.

- Fastest-Growing Product Segment: Sports lingerie is the fastest-growing category at 12.5% CAGR, driven by accelerating female sports participation, the integration of athleisure into lifestyle, and performance fabric innovations that create specialized, supportive garments combining functional engineering with aesthetic sophistication.

- Key Market Opportunity: Sustainable material adoption and eco-conscious production present substantial growth opportunities, with emerging consumer demand for environmentally responsible intimate apparel creating premium positioning opportunities among affluent millennial and Gen Z consumers willing to pay price premiums for authentic sustainability credentials and transparent supply chain practices.

| Key Insights | Details |

|---|---|

|

Lingerie Market Size (2026E) |

US$ 95.4 Billion |

|

Market Value Forecast (2033F) |

US$ 147.3 Billion |

|

Projected Growth CAGR (2026-2033) |

6.4% |

|

Historical Market Growth (2020-2025) |

5.9% |

Market Dynamics

Drivers - Body Positivity and Inclusive Design Revolution

The body positivity movement has fundamentally transformed the lingerie industry by challenging traditional, narrow aesthetic standards and creating authentic connections with previously underserved consumer segments. Brands that authentically embrace size inclusivity and celebrate diverse body types have experienced measurable market outperformance, with 30% sales increases documented among leading inclusive brands. This paradigm shift extends beyond marketing rhetoric into tangible product development, with major manufacturers now offering extended size ranges from petite to plus-size.

The American Psychological Association has documented this trend’s commercial impact, revealing that brands emphasizing body positivity command premium pricing power and enhanced customer loyalty. Companies like Aerie have pioneered unretouched marketing campaigns and inclusive sizing strategies that resonate particularly with millennial and Gen Z consumers, driving disproportionate growth rates within these demographics and creating sustainable competitive advantages.

Digital Commerce Transformation and E-Commerce Acceleration

The lingerie industry is experiencing unprecedented digital disruption, with e-commerce channels projected to command 52% of global market share by 2035, exceeding specialty retail for the first time. This acceleration reflects technological solutions that address historical online purchase barriers, including virtual fitting technologies, AI-powered size recommendation systems, and immersive AR/VR shopping experiences that mitigate fit-uncertainty concerns. The Indian online lingerie market exemplifies this trajectory, expanding at 10.9% CAGR between 2024 and 2029, driven by platform proliferation across Amazon, Flipkart, Nykaa, and Myntra. Direct-to-consumer digital strategies are enabling brands to capture higher margins while maintaining direct customer relationships, particularly valuable for premium and luxury segments. Victoria’s Secret & Co. reported international digital sales growth of 34% in Q3 2025, demonstrating sustained momentum despite macroeconomic headwinds, while Zivame leveraged omnichannel integration across its website, app, and 170+ proprietary retail stores to achieve 150% revenue growth post-COVID.

Restraint - Rising Material and Production Costs

Lingerie manufacturers face headwinds from escalating input costs and supply chain disruptions, constraining margin expansion and limiting retailers’ pricing flexibility with cost-conscious consumer segments. Material cost inflation particularly impacts the mass-market segment, which commands 77% global market share but operates under margin compression. Victoria’s Secret & Co. disclosed approximately $90 million in tariff-related impacts for fiscal year 2025 alone, representing a material headwind that requires strategic sourcing optimization. Labor cost pressures in primary manufacturing hubs—particularly Asia Pacific regions where production concentrates—alongside geopolitical trade tensions and supply chain fragmentation have elevated overall production costs. Budget-constrained consumers, especially in emerging markets, exhibit greater price sensitivity and a willingness to defer purchases when price-to-value ratios deteriorate, thereby directly constraining volume growth in economically sensitive regions.

Complex Regulatory and Compliance Requirements

Lingerie retailers operating across multiple jurisdictions face escalating regulatory complexity, encompassing data privacy frameworks (GDPR, CCPA), consumer protection standards, material composition regulations, and labeling requirements that vary significantly by geography. GDPR compliance violations carry penalties of up to €20 million or 4% of global revenue (whichever is higher), creating substantial legal risk for e-commerce-centric business models that require extensive customer data. Online retailers must navigate jurisdiction-specific consumer protection standards covering accurate product representation, complex return policies, and the prevention of deceptive advertising. The heterogeneity of global regulatory frameworks creates compliance complexity and requires dedicated legal and operational infrastructure, particularly challenging for smaller regional players and emerging brands lacking sophisticated compliance frameworks.

Opportunity - Sports Lingerie and Athleisure Integration

The sports bra segment is the fastest-growing product category in lingerie, expanding at a 12.5% CAGR and projected to reach US$ 56.76 billion by 2034, up from US$ 15.74 billion in 2024. This extraordinary growth trajectory reflects structural shifts in consumer lifestyle preferences, with female sports participation and fitness consciousness driving sustained demand for specialized, supportive garments that combine performance engineering with aesthetic appeal. The athleisure market, valued at US$ 431.70 billion globally in 2024, has created adjacency opportunities for lingerie brands to develop movement-ready, moisture-wicking offerings, blurring boundaries between intimate apparel and activewear.

Innovation in performance fabrics-including micromodal, moisture-wicking technologies, and seamless construction-enables lingerie to serve dual functionality for gym sessions and casual daily wear. Brands such as Nike, Adidas, Lululemon, and Champion have expanded their sports bra portfolios substantially, while emerging niche players are capturing market share with specialized designs that address specific athletic needs. The convergence of health consciousness, social media fitness influencer culture, and expanding female athletic participation creates a secular growth tailwind for premium sports lingerie positioning.

Sustainable and Eco-Conscious Material Innovation

Consumer demand for environmentally responsible and ethically produced intimate apparel is driving the accelerated adoption of sustainable material technologies, presenting substantial growth opportunities for manufacturers that integrate circular economy principles. Organic cotton, bamboo fabric, Tencel (Lyocell), and recycled synthetic fibers are gaining market traction, with emerging preferences among Gen Z and millennial consumers who prioritize environmental footprints. Sustainable lingerie addresses multiple consumer value drivers simultaneously-environmental impact reduction, ethical labor practices, superior comfort characteristics from natural fibers, and alignment with broader personal values regarding consumption sustainability.

Major brands, including Stella McCartney, Organic Basics, and Naja, have established premium positioning around sustainability credentials, commanding price premiums despite smaller production volumes. The sustainable lingerie market is projected to experience accelerated growth exceeding conventional segment rates as regulatory frameworks increasingly mandate environmental disclosure, consumer certifications proliferate, and manufacturing technologies improve sustainability economics. Brands successfully communicating transparent supply chains and authentic environmental commitments are capturing mindshare and loyalty among value-conscious affluent consumers, creating defensible market positions.

Category-wise Analysis

Product Type Insights

The brassiere segment dominates the lingerie market with 56% market share in 2024, representing the category’s established primacy and consumer centrality within intimate apparel. Bras maintains dual leadership status as both the largest segment and the fastest-growing category, driven by continuous innovation in comfort-enhancing technologies, underwire-free designs, and adaptive fit solutions that respond to evolving consumer preferences. Wireless and seamless bras have transitioned from niche comfort-focused offerings to mainstream preference drivers, with major manufacturers HanesBrands Inc., Triumph International Ltd., Hunkemöller, and Wacoal Holdings Corp. prioritizing product innovation in this space.

The segment’s sustained growth reflects broadening demographic appeal, inclusive sizing expansion enabling previously underserved body types to access well-fitting options, and fashion credibility enhanced through runway integration and celebrity endorsement. Sports lingerie, representing the fastest-growing product subcategory with a 12.5% CAGR, addresses specialized functional requirements by combining support engineering with aesthetic sophistication, capturing growing female athletic participation and athleisure lifestyle adoption.

Material Type Insights

Cotton emerges as the dominant material in lingerie formulations, leveraging its inherent breathability, moisture-absorption capacity, hypoallergenic properties, and consumer familiarity to drive preference for everyday, comfort-focused intimate apparel. Premium cotton variants, including Pima and Supima, command price premiums justified by their superior softness and durability, appealing to affluent consumers. Lace maintains established premium positioning as the fastest-growing material segment among luxury consumers, offering aesthetic sophistication and sensory appeal, driving consumer willingness to pay substantial premiums.

Silk and satin materials support luxury market positioning through tactile luxury perception, temperature-regulating properties, and aspirational brand associations. Nylon offers practical durability, easy care, and elasticity, particularly valuable in shapewear and athletic applications, while emerging sustainable material adoption, including organic cotton, bamboo, Tencel, and recycled fiber integration, reflects evolving consumer environmental consciousness and reshapes material selection criteria.

Price Range Insights

Mass-market lingerie maintains a dominant position with 77% global market share, driven by an extensive distribution infrastructure across supermarkets, hypermarkets, and expanding online channels, enabling broad consumer access. Mass-market segment dominance reflects fundamental economic accessibility requirements for intimate apparel categories with essential functional demands, though traditional quality-value perceptions disadvantage these categories under competitive pressure from premium mass-market offerings that deliver premium-adjacent attributes at accessible price points.

The premium segment, while representing a smaller absolute market share reflecting structural bifurcation in consumer spending patterns, treats premium lingerie as accessible luxury rather than discretionary expenditure. Rising disposable incomes, particularly across emerging Asian markets and increasing female economic independence drive premium segment expansion, while sustainability credentials and ethical production positioning support premium pricing justification. The luxury lingerie market is projected to reach US$ 20 billion by 2033 at a 7% CAGR, demonstrating sustained appeal among affluent consumers who prioritize exclusivity, craftsmanship, and heritage brand associations.

Distribution Channel Analysis

Specialty stores currently command 44% market share in lingerie distribution, leveraging expert service quality, instant product access, and curated brand assortments, justifying continued consumer preference despite e-commerce alternatives. Specialty lingerie retailers, including Victoria’s Secret, Triumph International Ltd., and Hunkemöller, maintain market leadership through sophisticated in-store experiences, professional fitting services, and exclusive product lines unavailable elsewhere.

Online retail channels are projected to grow at a 6.8% CAGR, substantially exceeding overall market growth rates, indicating fundamental distribution preference shifts driven by digital convenience, broader selection access, and expanding virtual fitting technologies that address historical online purchase barriers.

Regional Insights

North America Lingerie Market Trends and Insights

North America represents a mature and innovation-led lingerie market, shaped by high disposable incomes, advanced retail infrastructure, and strong digital penetration. Consumer demand is increasingly oriented toward premium, comfort-driven, and lifestyle-focused lingerie, positioning the category as a form of self-expression rather than purely functional apparel. E-commerce and omnichannel strategies play a critical role in sustaining growth, with brands leveraging data-driven personalization, subscription models, and social commerce to offset saturation in traditional brick-and-mortar channels.

Premiumization remains a defining trend, as luxury and mid-to-premium segments outperform mass-market offerings, supported by demand for superior fabrics, fit innovation, and brand storytelling. Body positivity and size inclusivity initiatives have significantly reshaped purchasing behavior, enabling brands to tap underserved demographic segments and younger consumers. Regulatory requirements related to digital commerce, data privacy, and cross-border transactions add compliance complexity; however, established legal and operational frameworks in the region allow leading participants to manage these constraints efficiently while maintaining stable margins and brand leadership.

Europe Lingerie Market Trends and Insights

Europe is an established and design-driven lingerie market, underpinned by strong heritage brand loyalty, refined consumer preferences, and harmonized regulatory standards across the European Union. Demand is concentrated in Western Europe, where consumers prioritize quality, craftsmanship, and brand authenticity, supporting sustained premium and luxury positioning. Sustainability is a central purchasing criterion, with higher-than-global-average adoption of organic, recycled, and ethically sourced materials influencing product development and pricing strategies. European consumers also show a strong preference for durability and timeless design, leading to longer replacement cycles than in other regions.

The region’s stringent data protection and consumer rights regulations raise operational requirements for digital channels but simultaneously enhance trust in e-commerce platforms. Competitive dynamics are characterized by selective consolidation, modernization of heritage brands, and gradual expansion of direct-to-consumer models. While specialty retailers and department stores remain important, online channels continue to gain share, increasing pressure on traditional distribution formats and accelerating digital transformation initiatives.

Asia Pacific Lingerie Market Trends and Insights

Asia Pacific dominates global lingerie market growth dynamics with 35% market share in 2025, driven by enormous addressable consumer populations across China, Japan, India, South Korea, and ASEAN, combined with accelerating urbanization, rising female workforce participation, and expanding middle-class purchasing power. China alone represents a substantial growth opportunity, with e-commerce penetration enabling rapid brand expansion and consumer adoption of premium offerings previously limited to developed markets. India’s online lingerie market exhibits exceptional dynamism, with Zivame acquired by Reliance Retail for US$ 160 million, exemplifying successful market consolidation. Zivame achieved 150% revenue growth post-COVID while expanding from fewer than 50 retail locations to 170+ proprietary stores, demonstrating omnichannel integration effectiveness capturing both online and physical retail market share.

Japanese market maturity and sophisticated consumer preferences support premium brand positioning, while ASEAN growth dynamics, including Thailand, Vietnam, and Indonesia, offer substantial frontier expansion opportunities characterized by expanding digital infrastructure, rising disposable incomes, and the adoption of Western fashion trends. Manufacturing concentration in Asia Pacific, particularly in Bangladesh, Cambodia, and Vietnam, through MAS Holdings and regional manufacturers, enables cost-competitive production that supports mass-market segment expansion. Body positivity and inclusivity concepts are gaining traction across the region, with local brands like Zivame and Clovia emphasizing size inclusivity and diverse representation, creating differentiated positioning against historical premium Western imports.

Competitive Landscape

The global lingerie market displays a highly fragmented competitive structure, characterized by a clear divide between large, established multinational players and a rapidly expanding pool of regional and digital-first brands. Premium and specialty segments are largely controlled by incumbents with strong brand equity, legacy retail networks, and vertically integrated supply chains, while mass-market volumes are increasingly captured through e-commerce-led, value-oriented models. Competitive strategies center on direct-to-consumer expansion, omnichannel integration, and continuous product innovation in high-growth categories such as sports lingerie, shapewear, and comfort-focused designs.

Sustainability, inclusive sizing, and body-positive positioning are emerging as critical differentiation levers, particularly among younger consumer cohorts. Leading participants leverage manufacturing consolidation and long-term supplier partnerships to achieve cost efficiencies and margin stability, whereas newer entrants favor asset-light structures that prioritize branding, influencer-led digital marketing, and rapid design cycles. Overall, competition is intensifying as digital penetration lowers entry barriers and accelerates brand proliferation across regional markets.

Key Market Developments

- January 2025: Victoria’s Secret & Co. raised full-year fiscal 2025 net sales guidance to US$ 6.45-6.48 billion, reflecting 9% comparable sales growth in Q3 2025, demonstrating sustained momentum in both domestic and international markets with particular strength in digital channels and product innovation initiatives.

- February 2025: HanesBrands Inc. reported Q4 2024 net sales of US$ 888 million, reflecting 4.5% year-over-year growth driven by innerwear innovation including Hanes Absolute Socks, Hanes Moves, Hanes Supersoft, and Bali Breathe product launches, alongside 30% increase in brand investments targeting consumer demand for innovative intimate apparel.

- March 2024: Zivame announced 150% revenue growth post-COVID, driven by the expansion of its retail footprint to 170+ stores across Indian markets, demonstrating a successful omnichannel integration strategy combining online platforms (website, app, and Amazon/Flipkart/Nykaa presence) with physical specialty retail locations, capturing emerging market opportunities.

Companies Covered in Lingerie Market

- Jockey International Inc.

- Victoria’s Secret & Co.

- Zivame

- Gap, Inc.

- HanesBrands Inc.

- Triumph International Ltd.

- Hunkemöller

- Calida Group

- Calvin Klein (PVH Corp.)

- MAS Holdings

- Wacoal Holdings Corp.

- PVH Corp.

- American Eagle Outfitters, Inc.

- La Perla Group

- Delta Galil Industries Ltd.

- Aerie (American Eagle Outfitters, Inc.)

- Savage X Fenty (LVMH partnership)

- Stella McCartney

- Marks & Spencer plc

- SKIMS

Frequently Asked Questions

The global lingerie market is projected to reach US$ 95.4 billion in 2026 and US$ 147.3 billion by 2033, growing at a 6.4% CAGR.

Key drivers include body-positivity trends, rapid e-commerce adoption, rising female workforce participation, and strong growth in sports lingerie.

Asia Pacific leads the market and is also the fastest-growing region due to large consumer bases, rising incomes, and expanding e-commerce.

Sports lingerie, athleisure integration, and sustainable materials represent major growth opportunities.

Leading market participants include Victoria’s Secret & Co., HanesBrands Inc., Zivame, Triumph International Ltd., Wacoal Holdings Corp., and emerging digital-native brands.