- Semiconductor Materials & Components

- Sheet Lamination Market

Sheet Lamination Market Size, Share, and Growth Forecast, 2026 - 2033

Sheet lamination Market by Material Type (Polyester, Polypropylene, Vinyl, Paper), Application (Packaging, Printing, Labels and Tags, Photographic Products) and Regional Analysis for 2026 - 2033

Sheet Lamination Market Size and Trends Analysis

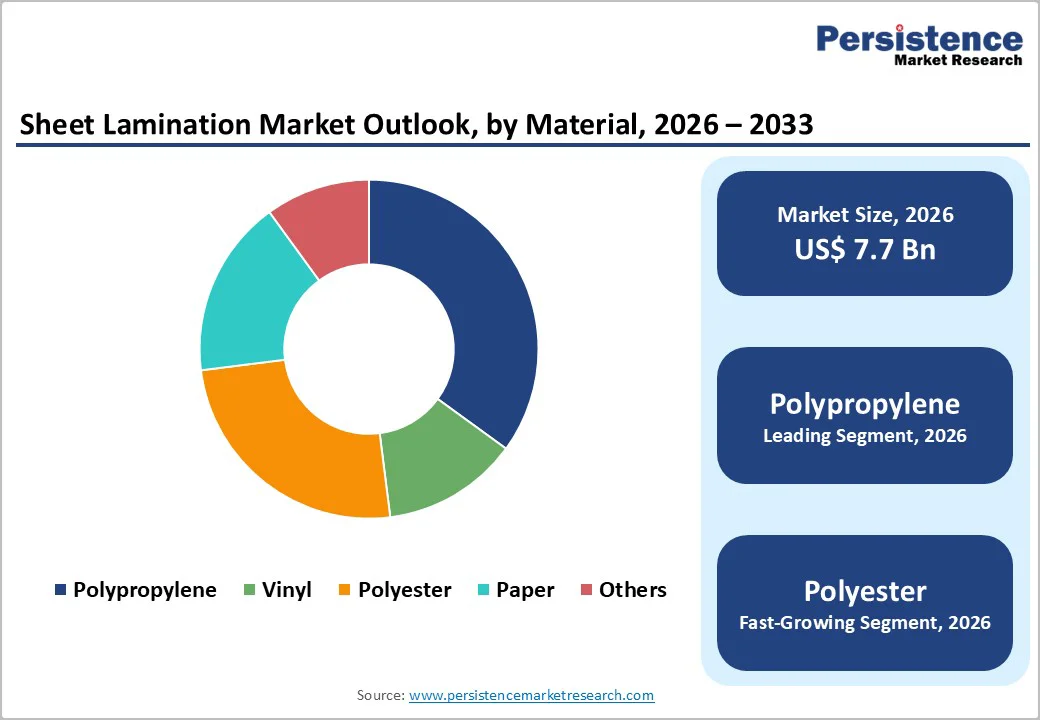

The global sheet lamination market size is likely to be valued at US$7.7 billion in 2026 and is expected to reach US$15.5 billion by 2033, growing at a CAGR of 10.5% during the forecast period from 2026 to 2033, driven by increasing demand for protective, durable, and visually enhanced finishing solutions across the packaging, printing, and graphic arts industries.

Rising consumption of packaged goods, coupled with the need to improve product shelf life, branding, and aesthetic appeal, is accelerating the adoption of lamination materials. The rapid expansion of e-commerce, digital printing, and labeling applications is boosting demand for high-quality laminated labels, tags, and printed surfaces. Technological advancements in lamination films and growing preference for cost-effective, lightweight, and sustainable materials support market expansion.

Key Industry Highlights:

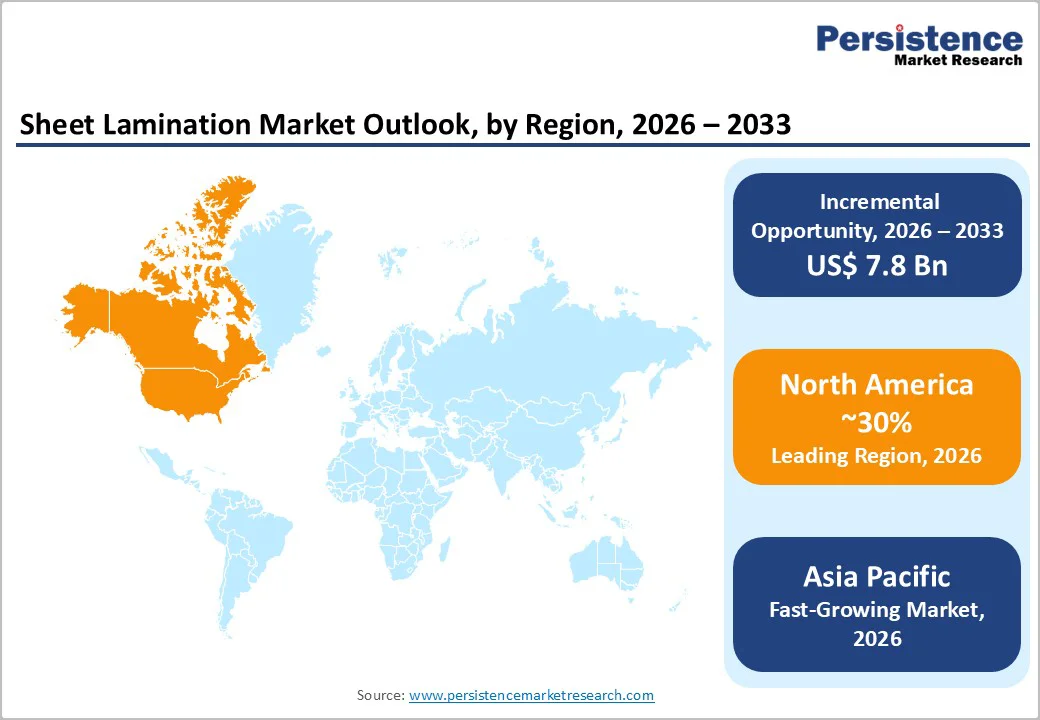

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 30% in 2026, driven by advanced digital printing technologies, strong food and retail packaging demand, stringent FDA regulations, and continued investment in sustainable, recyclable, and antimicrobial lamination solutions.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region in sheet lamination in 2026, driven by low-cost manufacturing, rising domestic consumption, e-commerce growth, pharmaceutical demand, and increasing adoption of sustainable lamination technologies.

- Leading Material Type: Polypropylene is projected to represent the leading material type in 2026, accounting for 40% of the revenue share, driven by its clarity, moisture resistance, and cost-effectiveness.

- Leading Application: Packaging is anticipated to be the leading application type, accounting for over 45% of the revenue share in 2026, supported by its essential role in protecting food, beverages, and consumer goods.

| Key Insights | Details |

|---|---|

|

Sheet Lamination Market Size (2026E) |

US$7.7 Bn |

|

Market Value Forecast (2033F) |

US$15.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

10.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Demand for Protective Packaging Solutions

The growing consumption of packaged foods, beverages, pharmaceuticals, and consumer goods is driving manufacturers to increasingly rely on laminated materials to improve product safety and durability. Sheet lamination offers an effective barrier against moisture, oxygen, and physical damage, helping ensure products reach consumers in optimal condition. The rapid expansion of e-commerce has further heightened demand for durable packaging solutions, as goods are shipped over long distances and subjected to multiple handling stages. Laminated films, particularly polypropylene and polyester, are widely preferred for their strength, clarity, and tear resistance, making them well-suited for applications such as food packaging, labels, and tags.

Protective packaging also plays a vital role in brand visibility and consumer appeal. Laminated films enhance packaging aesthetics through high gloss finishes, superior clarity, and excellent print compatibility, which are essential for effective branding and marketing. As competition intensifies across retail channels, companies are increasingly adopting laminated solutions to stand out on crowded shelves and strengthen brand differentiation. Innovation in sustainable and recyclable lamination materials is also gaining momentum, enabling businesses to meet environmental regulations without compromising performance. This combination of durability, functionality, and sustainability continues to drive the adoption of sheet lamination across the packaging industry.

Stringent Environmental Regulations on Plastics

Governments around the world are increasingly introducing policies to reduce plastic waste, restrict single-use plastics, and encourage sustainable packaging solutions. These regulations affect the use of conventional lamination films, especially non-recyclable polypropylene or vinyl, which are commonly employed in packaging, labels, and protective coverings. To comply, manufacturers often need to adopt alternative materials, such as recyclable or biodegradable films, which can raise production costs and complicate supply chains.

Regulatory oversight also focuses on the disposal and recyclability of laminated products. Many lamination processes involve combining multiple layers of different materials, making recycling difficult and heightening environmental concerns. Industries are exploring eco-friendly innovations, including PET-based recyclable films and water-based adhesives. While these approaches advance sustainability goals, they also pose challenges for market growth by limiting the use of traditional laminated plastics and increasing operational expenses. Manufacturers, therefore, must strike a balance between meeting regulatory requirements and maintaining product performance, functionality, and visual appeal in competitive markets.

Development of Sustainable and Bio-based Lamination Films

As environmental awareness grows and regulations on plastic use tighten, manufacturers are increasingly turning to eco-friendly alternatives to conventional lamination materials. Bio-based films, recyclable PET options, and biodegradable laminates provide similar durability, moisture resistance, and print quality while minimizing environmental impact. These innovations allow companies to achieve sustainability targets without compromising product protection or visual appeal, making them ideal for packaging, labels, and graphic arts applications.

Consumer demand is shifting toward products with environmentally responsible packaging, particularly in the food, beverage, and personal care sectors. Companies that invest in sustainable lamination technologies can gain a competitive advantage by supporting green initiatives, strengthening brand reputation, and appealing to eco-conscious consumers. The adoption of recyclable and compostable films also creates opportunities for collaboration with material suppliers, research institutions, and startups focused on circular economy solutions. This trend not only drives the broader adoption of sheet lamination in conventional markets but also fuels the growth of premium and innovative packaging applications.

Category-wise Analysis

Material Type Insights

The polypropylene segment is projected to lead the sheet lamination market in 2026, accounting for around 40% of total revenue. Its excellent clarity, moisture barrier properties, and cost-effectiveness make it ideal for packaging and labeling applications. The lightweight and flexible nature of polypropylene allows manufacturers to create laminated films that protect products during storage and transportation while maintaining visual appeal. For instance, in the food packaging sector, BOPP films are extensively used for snacks such as chips, cookies, and nuts, as well as for beverage labels, offering both durability and high clarity.

Polyester is expected to be the fastest-growing segment in 2026, driven by demand for high-strength, heat-resistant films in premium printing, photographic products, and industrial packaging. Polyester laminates are valued for their durability, clarity, and ability to withstand elevated temperatures, making them suitable for high-end product packaging. In the photographic industry, polyester-based lamination films protect printed photographs and photo books from moisture, scratches, and fading. Luxury beverage packaging also often employs polyester laminates to enhance visual appeal and provide a premium finish. The growth of recyclable PET-based polyester films further boosts this segment, as sustainability-focused brands increasingly adopt environmentally friendly packaging solutions.

Application Insights

The packaging segment is projected to dominate the sheet lamination market in 2026, accounting for approximately 45% of the total revenue. Laminated packaging is essential for protecting products across food, beverages, pharmaceuticals, and consumer goods, ensuring quality during storage, transit, and display. Its leadership is driven by the need for moisture resistance, barrier protection, and enhanced shelf appeal. For instance, beverage cartons incorporate laminated layers to provide durability, liquid resistance, and visual attractiveness. Technological advancements, including high-speed lamination and digitally printed films, have further reinforced packaging as the primary application. Growing consumer demand for durable and visually appealing packaging continues to drive the adoption of sheet lamination solutions, solidifying its position as the leading segment.

Labels and tags are expected to be the fastest-growing application in 2026, fueled by the expansion of e-commerce, regulatory requirements, and branding priorities. Laminated labels offer durability, moisture resistance, and superior print quality, making them critical for product identification and information display. For example, pharmaceutical packaging relies on laminated labels to ensure dosage and safety information remains intact throughout the product lifecycle. Increasing emphasis on brand visibility and premium packaging is also boosting demand for high-quality laminated labels in cosmetics, beverages, and consumer goods. Advances in digitally printed laminated labels enable cost-effective, customizable production at scale, further supporting market growth.

Regional Insights

North America Sheet Lamination Market Trends

North America is expected to lead the sheet lamination market in 2026, accounting for approximately 30% of the total market share. This leadership is supported by a mature printing and packaging industry, advanced technological infrastructure, and strong consumer demand for packaged goods. Companies are increasingly adopting sheet lamination solutions in food, beverage, and pharmaceutical packaging due to their durability, moisture resistance, and visual appeal. For instance, Amcor plc extensively uses laminated films in snack packaging and beverage labels to enhance shelf life and brand visibility. The adoption of laminated materials is further accelerated by technological advancements such as high-speed lamination equipment and integration with digital printing.

Regulatory compliance is another key factor shaping the market. Strict FDA regulations, along with rising environmental awareness, are driving the use of recyclable and biodegradable laminated films. Investments in R&D for antimicrobial, heat-resistant, and eco-friendly lamination solutions are increasing, particularly in pharmaceutical and e-commerce packaging. The focus on premium, durable, and sustainable laminates not only ensures regulatory compliance but also meets growing consumer demand for environmentally responsible packaging.

Europe Sheet Lamination Market Trends

Europe is expected to be a key market for sheet lamination in 2026, supported by a robust packaging and printing industry and rising demand for high-quality, durable laminated products. Laminated films are extensively used in food packaging, luxury goods, and labels, offering protection against moisture, oxygen, and physical damage while enhancing visual appeal. For instance, companies such as Tetra Pak employ laminated packaging in confectionery and beverage products to preserve freshness and extend shelf life. Advances in technology, including digital printing integration and precise lamination techniques, are further driving adoption across the region.

Regulatory compliance is also a major factor shaping the European market. The EU’s strict environmental regulations and initiatives to reduce plastic waste are encouraging the use of recyclable, biodegradable, and eco-friendly lamination films. PET-based recyclable laminates, for example, are increasingly utilized in food packaging and e-commerce labels to meet sustainability targets. There is a growing demand for premium laminated solutions in high-end consumer goods, cosmetics, and pharmaceuticals, where durability, aesthetics, and brand presentation are crucial. Innovations in bio-based and compostable films further reinforce Europe’s position as a market that balances performance, regulatory compliance, and sustainability in the sheet lamination industry.

Asia Pacific Sheet Lamination Market Trends

The Asia Pacific region is expected to be the fastest-growing market for sheet lamination in 2026, driven by rapid industrialization, increasing domestic consumption, and a strong manufacturing sector. Laminated films are increasingly applied in food packaging, labels, and consumer goods to provide durability, moisture resistance, and enhanced visual appeal. For instance, companies such as Toray Industries, Inc. in Japan use polyester laminates for luxury product packaging to achieve high-quality finishes. The region’s growth is further supported by the expansion of e-commerce, which demands durable, protective, and visually appealing laminated labels and tags.

Technological adoption is a key trend in the Asia Pacific market. Countries are progressively implementing environmental regulations, promoting the use of recyclable, biodegradable, and eco-friendly lamination films. The market is fragmented, with both local and international players investing in capacity expansion, specialty films, and integration with digital printing. Rising disposable incomes, urbanization, and growing consumer demand are collectively driving the rapid adoption of sheet lamination solutions across packaging, labeling, and premium product applications in the region.

Competitive Landscape

The global sheet lamination market demonstrates a moderately fragmented structure, characterized by the presence of both established manufacturers and innovative niche players competing across technology, product quality, and geographic reach. Leading companies invest heavily in R&D to improve lamination speeds, enhance material compatibility, and integrate with digital printing and additive manufacturing technologies, strengthening their positions across key end-use industries such as packaging, automotive, aerospace, and consumer goods. Competitive dynamics are further influenced by strategic partnerships, mergers, and expansion into emerging markets, as firms seek to diversify their portfolios and address specific industry requirements.

Key players in the market include Boxford, CAM-LEM, Cubic Technologies, Sterling Finishing, Mcor Technologies, and others, alongside broader additive manufacturing leaders such as Stratasys Ltd. and 3D Systems Corporation, who are increasingly focusing on sheet lamination solutions. These companies compete through continuous product innovation, strategic collaborations, superior customer support, and expanded distribution networks to capture larger shares in regional and global markets. Emphasis on sustainability, recyclable materials, and advanced lamination techniques serves as a key differentiator, enabling companies to comply with environmental regulations and meet growing consumer demand for high-performance, eco-friendly laminated products.

Key Industry Developments:

- In November 2025, Singapore startup Lapis unveiled a novel sheet lamination metal 3D printing process that produces high-resolution, dense metal parts without powder. Developed from Nanyang Technological University’s 3D Printing Centre, the technology merges Laminated Object Manufacturing with laser welding and ablation to create intricate components with high accuracy and lower costs than traditional metal additive methods.

- In October 2025, Nobelus introduced the Orbis Dual 61, an automated two-sided thermal laminating system engineered to improve efficiency and output quality for packaging and graphic arts. The system combines an automated feeder, thermal laminator, and trimmer, allowing high-speed sheet processing with precise temperature control and consistent lamination. It accommodates nylon, BOPP, and PET films up to 15 mils, and includes features such as swing-out film mandrels, cooling rollers, and edge slitters for smoother, more efficient operation.

Companies Covered in Sheet Lamination Market

- Boxford

- CAM LEM

- Cubic Technologies

- Sterling Finishing

- Mcor Technologies

- Wuhan Binhu Mechanical and Electrical

Frequently Asked Questions

The global sheet lamination market is projected to reach US$7.7 billion in 2026.

Rising demand for durable, protective, and visually enhanced laminated packaging, labels, and printed products.

The sheet lamination market is expected to grow at a CAGR of 10.5% from 2026 to 2033.

Key market opportunities in sheet lamination include the growth of sustainable and bio-based films, increasing demand from e-commerce and premium packaging segments, and the adoption of advanced digital printing integration.

Boxford, CAM LEM, Cubic Technologies, Sterling Finishing, Mcor Technologies, and Wuhan Binhu Mechanical and Electrical are the leading players.