- Executive Summary

- Global Idiopathic Thrombocytopenic Purpura Therapeutics Market Snapshot, 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Mn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Drug Class Adoption Analysis

- Recent Drug Class Launches

- Regulatory Landscape

- Value Chain Analysis

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Trend Analysis, 2020 - 2033

- Key Highlights

- Key Factors Impacting Drug Class Prices

- Pricing Analysis, By Drug Class Type

- Regional Prices and Drug Class Preferences

- Global Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook:

- Key Highlights

- Market Size (US$ Mn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Mn) Analysis and Forecast

- Historical Market Size (US$ Mn) Analysis, 2020-2025

- Market Size (US$ Mn) Analysis and Forecast, 2026-2033

- Global Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook: Drug Class

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis and Volume (Units) Analysis, By Drug Class, 2020 - 2025

- Market Size (US$ Mn) Analysis and Volume (Units) Analysis and Forecast, By Drug Class, 2026 - 2033

- Corticosteroids

- Intravenous Immunoglobulin (IVIG)

- Anti-D Immunoglobulins

- Thrombopoietin Receptor Agonists (TPO-RA)

- Others

- Market Attractiveness Analysis: By Drug Class

- Global Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook: Disease Type

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Disease Type, 2020 - 2025

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2026 - 2033

- Acute ITP

- Chronic ITP

- Others

- Market Attractiveness Analysis: By Disease Type

- Global Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook: Distribution Channel

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Distribution Channel, 2020 - 2025

- Market Size (US$ Mn) Analysis and Forecast, By Distribution Channel, 2026 - 2033

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Pharmacies

- Market Attractiveness Analysis: Distribution Channel

- Key Highlights

- Global Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Region, 2020 - 2025

- Market Size (US$ Mn) Analysis and Forecast, By Region, 2026 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2020 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Distribution Channel

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2026 - 2033

- U.S.

- Canada

- Market Size (US$ Mn) Analysis and Volume (Units) Analysis and Forecast, By Drug Class, 2026 - 2033

- Corticosteroids

- Intravenous Immunoglobulin (IVIG)

- Anti-D Immunoglobulins

- Thrombopoietin Receptor Agonists (TPO-RA)

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2026 - 2033

- Acute ITP

- Chronic ITP

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Distribution Channel, 2026 - 2033

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Pharmacies

- Market Attractiveness Analysis

- Europe Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2020 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Distribution Channel

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2026 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Mn) Analysis and Volume (Units) Analysis and Forecast, By Drug Class, 2026 - 2033

- Corticosteroids

- Intravenous Immunoglobulin (IVIG)

- Anti-D Immunoglobulins

- Thrombopoietin Receptor Agonists (TPO-RA)

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2026 - 2033

- Acute ITP

- Chronic ITP

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Distribution Channel, 2026 - 2033

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Pharmacies

- Market Attractiveness Analysis

- East Asia Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2020 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Distribution Channel

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2026 - 2033

- China

- Japan

- South Korea

- Market Size (US$ Mn) Analysis and Volume (Units) Analysis and Forecast, By Drug Class, 2026 - 2033

- Corticosteroids

- Intravenous Immunoglobulin (IVIG)

- Anti-D Immunoglobulins

- Thrombopoietin Receptor Agonists (TPO-RA)

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2026 - 2033

- Acute ITP

- Chronic ITP

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Distribution Channel, 2026 - 2033

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Pharmacies

- Market Attractiveness Analysis

- South Asia & Oceania Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2020 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Distribution Channel

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2026 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Mn) Analysis and Volume (Units) Analysis and Forecast, By Drug Class, 2026 - 2033

- Corticosteroids

- Intravenous Immunoglobulin (IVIG)

- Anti-D Immunoglobulins

- Thrombopoietin Receptor Agonists (TPO-RA)

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2026 - 2033

- Acute ITP

- Chronic ITP

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Distribution Channel, 2026 - 2033

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Pharmacies

- Market Attractiveness Analysis

- Latin America Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2020 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Distribution Channel

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2026 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Mn) Analysis and Volume (Units) Analysis and Forecast, By Drug Class, 2026 - 2033

- Corticosteroids

- Intravenous Immunoglobulin (IVIG)

- Anti-D Immunoglobulins

- Thrombopoietin Receptor Agonists (TPO-RA)

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2026 - 2033

- Acute ITP

- Chronic ITP

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Distribution Channel, 2026 - 2033

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Pharmacies

- Market Attractiveness Analysis

- Middle East & Africa Idiopathic Thrombocytopenic Purpura Therapeutics Market Outlook:

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2020 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Distribution Channel

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2026 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Mn) Analysis and Volume (Units) Analysis and Forecast, By Drug Class, 2026 - 2033

- Corticosteroids

- Intravenous Immunoglobulin (IVIG)

- Anti-D Immunoglobulins

- Thrombopoietin Receptor Agonists (TPO-RA)

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2026 - 2033

- Acute ITP

- Chronic ITP

- Others

- Market Size (US$ Mn) Analysis and Forecast, By Distribution Channel, 2026 - 2033

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Pharmacies

- Market Attractiveness Analysis

- Competition Landscape

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Recent Developments)

- Amgen Inc.

- Overview

- Segments and Drug Class & Distribution Channel

- Key Financials

- Market Developments

- Market Strategy

- Novartis AG

- F. Hoffmann-La Roche Ltd

- GSK plc.

- Grifols, S.A.

- Rigel Pharmaceuticals, Inc.

- Swedish Orphan Biovitrum AB (publ)

- argenx SE

- Sanofi S.A.

- Takeda Pharmaceutical Company Limited

- CSL Limited

- Octapharma AG

- Pfizer Inc.

- Bristol Myers Squibb Company

- Kissei Pharmaceutical Co., Ltd.

- Others

- Amgen Inc.

- Market Structure

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Pharmaceuticals

- Idiopathic Thrombocytopenic Purpura Therapeutics Market

Idiopathic Thrombocytopenic Purpura Therapeutics Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Idiopathic Thrombocytopenic Purpura Therapeutics Market by Drug Class (Corticosteroids, Intravenous Immunoglobulin (IVIG), Anti-D Immunoglobulins, Thrombopoietin Receptor Agonists (TPO-RA), and Others), by Disease Type (Acute ITP, Chronic ITP, and Others) Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, and Specialty Pharmacies), and Regional Analysis from 2026 - 2033

Key Industry Highlights:

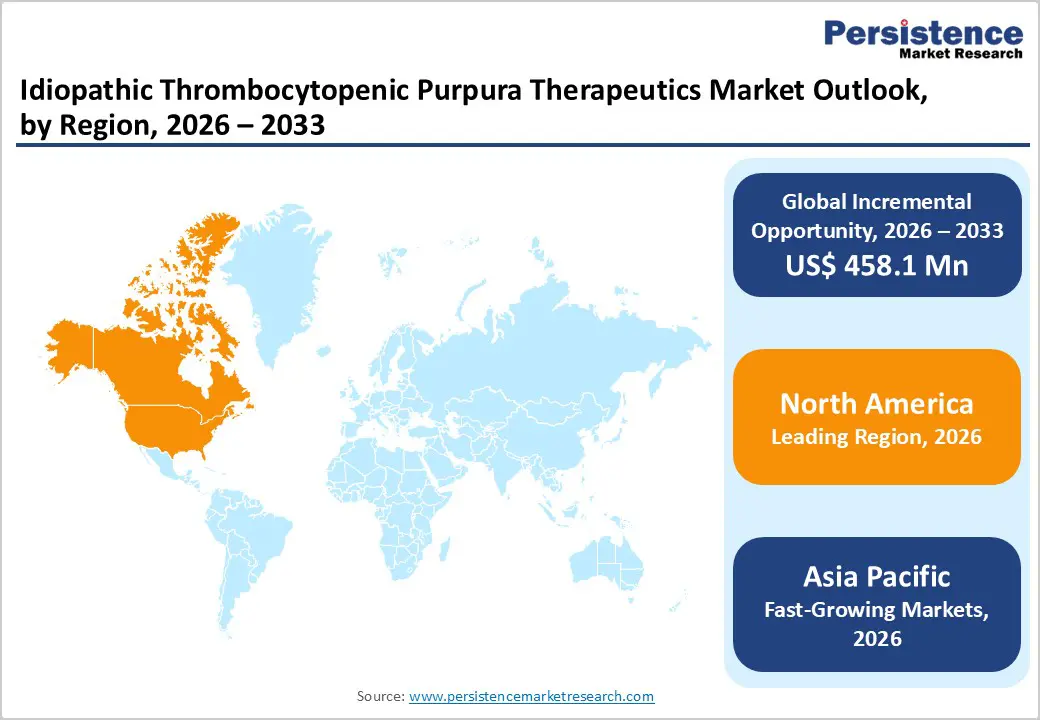

- Leading Region: North America holds 46.7% of the global market, driven by strong hematology care infrastructure, high awareness of autoimmune blood disorders, advanced diagnostic capabilities, and rapid adoption of targeted immune-modulating therapies.

- Fastest-Growing Region: Asia Pacific is witnessing the most rapid expansion due to improving healthcare infrastructure, increasing hematology diagnosis rates, rising healthcare investments, and expanding availability of advanced specialty treatments across developing economies.

- Leading Drug Class Segment: Corticosteroids represent the largest therapeutic segment, primarily because they remain the standard first-line treatment used to rapidly increase platelet counts and suppress immune-mediated platelet destruction during the early stages of disease management.

- Fastest-Growing Drug Class Segment: Intravenous Immunoglobulin (IVIG) is gaining strong adoption as physicians increasingly use it for rapid platelet recovery in severe cases and during emergency management of bleeding episodes.

- Leading Disease Type Segment: Acute ITP accounts for 27.9% of the market, reflecting the high volume of newly diagnosed patients who require immediate therapeutic intervention to stabilize platelet levels.

- Fastest-Growing Disease Type Segment: Chronic ITP is expanding at a faster pace as a growing number of patients require long-term treatment with targeted therapies to maintain sustained platelet response and reduce relapse risk.

| Key Insights | Details |

|---|---|

|

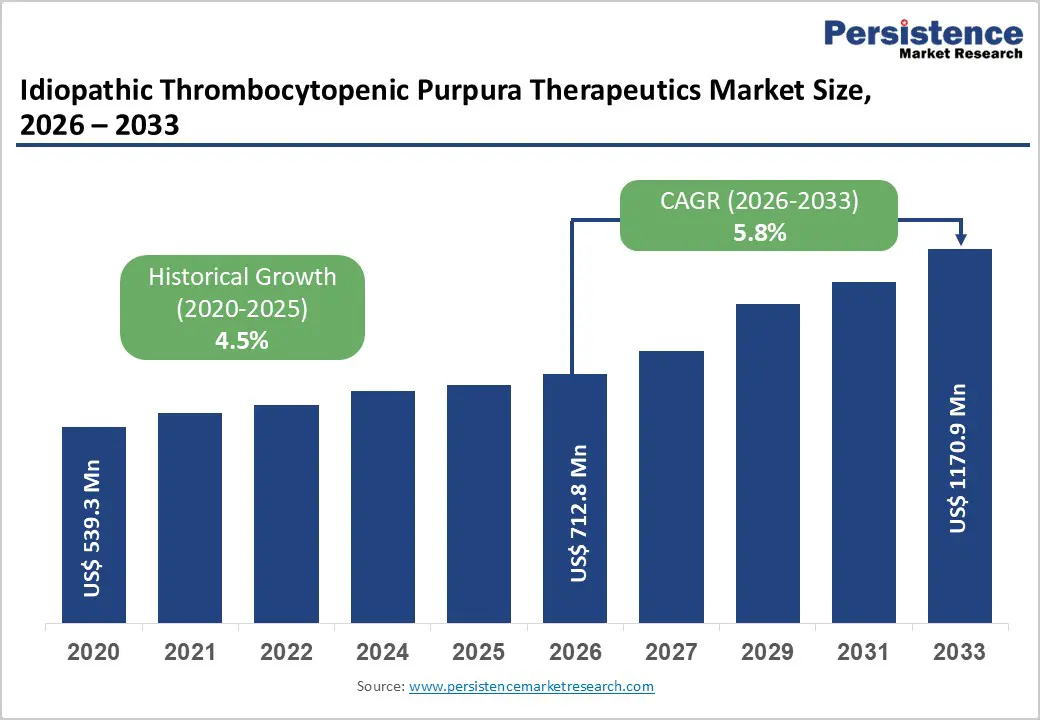

Idiopathic Thrombocytopenic Purpura Therapeutics Market Size (2026E) |

US$ 712.8 Mn |

|

Market Value Forecast (2033F) |

US$ 1170.9 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Dynamics

Driver - Increasing Diagnosis of Immune Thrombocytopenia and Expansion of Targeted Therapeutic Options

The growing recognition and diagnosis of immune-mediated platelet disorders are significantly contributing to the expansion of therapeutic demand worldwide. Idiopathic thrombocytopenic purpura (ITP) is an autoimmune condition characterized by accelerated platelet destruction and impaired platelet production, which can lead to bleeding complications if untreated. Rising awareness among physicians and improved diagnostic capabilities, including advanced hematological testing and platelet monitoring technologies, are enabling earlier detection and intervention. As a result, more patients are receiving pharmacological therapy during both acute and chronic disease stages. Additionally, pharmaceutical innovation has introduced a broader range of targeted treatment options designed to improve platelet response and long-term disease control.

Therapies such as thrombopoietin receptor agonists, including Romiplostim and Eltrombopag, stimulate platelet production and have significantly improved treatment outcomes for patients who do not respond adequately to first-line corticosteroid therapy. The introduction of spleen tyrosine kinase inhibitors such as Fostamatinib has further expanded therapeutic strategies by targeting immune-mediated platelet destruction mechanisms. Clinical guidelines from hematology associations increasingly emphasize individualized treatment strategies based on disease severity, bleeding risk, and patient response to therapy. Healthcare providers are therefore adopting a wider range of pharmacological options to manage refractory or chronic disease cases more effectively. Furthermore, the growing number of hematology specialists and specialized treatment centers has improved access to advanced therapies. These combined clinical and therapeutic advancements are strengthening physician confidence in available treatments and supporting continued growth in global ITP therapeutics demand.

Restraints - High Cost of Biologic Therapies and Long-Term Treatment Complexity

Despite ongoing therapeutic advancements, several structural and economic challenges continue to influence treatment accessibility and market expansion. One of the most notable limitations is the high cost associated with newer targeted therapies used in the management of chronic immune thrombocytopenia. Biologic drugs and advanced immunomodulatory therapies often require long-term administration to maintain adequate platelet levels, which can substantially increase overall treatment expenses. In healthcare systems with limited reimbursement coverage, particularly in low- and middle-income countries, these costs may restrict patient access to innovative therapies. Another challenge arises from the complexity of long-term disease management. Many patients with chronic ITP require continuous monitoring of platelet counts, periodic dose adjustments, and ongoing evaluation by hematology specialists. Treatment responses can vary widely between individuals, making it necessary for physicians to frequently modify therapeutic regimens.

Additionally, certain therapies may be associated with adverse effects such as liver function abnormalities, immune suppression, or increased risk of infection, which may limit their use in specific patient populations. Healthcare infrastructure limitations in some regions also contribute to treatment disparities. Access to specialized hematology clinics, diagnostic laboratories, and advanced biologic therapies may be limited in smaller hospitals or rural healthcare systems. Furthermore, patient adherence can be influenced by treatment burden, especially when therapies require frequent hospital visits or injectable administration. These combined economic, clinical, and healthcare access factors continue to present challenges for broader adoption of advanced ITP treatment strategies.

Opportunity - Development of Novel Immunotherapies and Expansion of Precision Treatment Approaches

Ongoing advancements in immunology and targeted drug development are creating promising opportunities for the next generation of immune thrombocytopenia therapies. Researchers and pharmaceutical companies are actively exploring innovative treatment strategies aimed at addressing the underlying immune dysregulation responsible for platelet destruction. Novel biologics, monoclonal antibodies, and targeted immune-modulating agents are currently being evaluated in clinical trials to improve treatment response rates and achieve longer-lasting remission in patients with chronic disease. A key area of development involves therapies designed to selectively regulate immune pathways involved in platelet clearance without broadly suppressing the immune system. Such precision-focused approaches may reduce treatment-related adverse effects while improving therapeutic efficacy. In addition, advances in molecular diagnostics and biomarker research are helping clinicians better understand patient-specific disease mechanisms. This progress may enable physicians to tailor therapy selection based on individual immune profiles, thereby improving treatment outcomes and minimizing unnecessary drug exposure.

Emerging markets are also expected to play a crucial role in expanding therapeutic adoption. Governments across Asia, Latin America, and parts of the Middle East are increasing healthcare investments and strengthening hematology care infrastructure. Greater availability of specialty drugs, improved insurance coverage, and growing physician awareness are gradually improving patient access to advanced therapies. Combined with ongoing clinical research and regulatory approvals for new immunomodulatory treatments, these developments present significant opportunities for innovation and long-term growth within the global ITP therapeutics landscape.

Category-wise Analysis

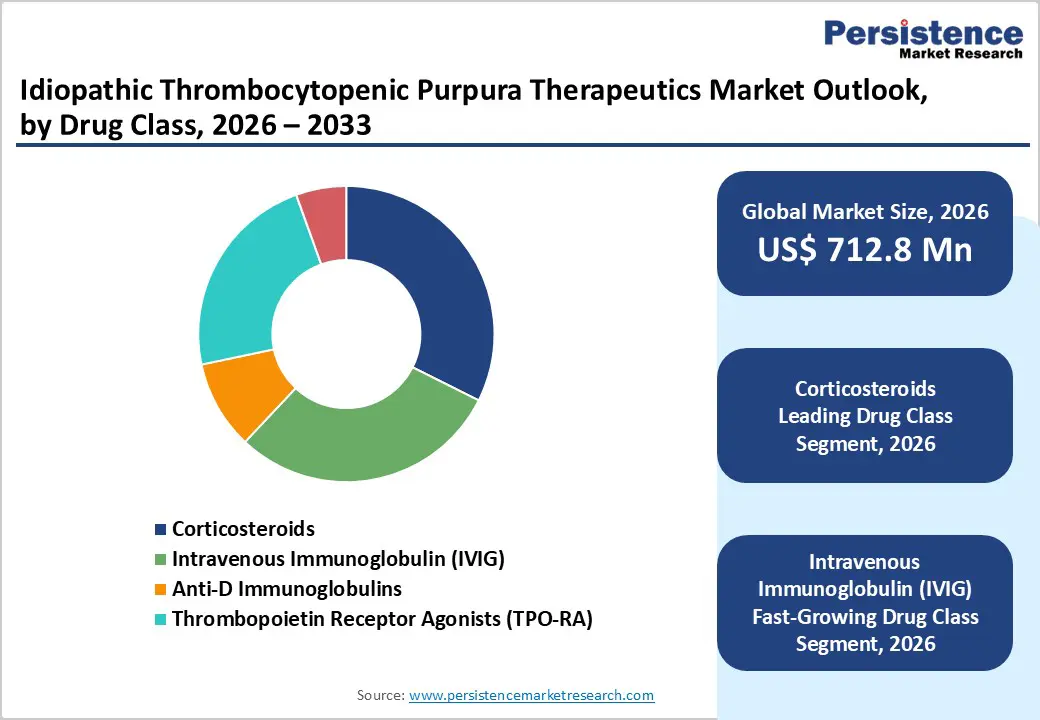

By Drug Class Insights

The corticosteroids segment is projected to remain the leading therapeutic category in 2026, accounting for 32.4% of total market revenue. Their dominance is primarily linked to their role as the first-line therapy for immune thrombocytopenia, where rapid suppression of immune-mediated platelet destruction is essential to prevent bleeding complications. Drugs such as Prednisone and Dexamethasone are widely prescribed during the early stages of treatment because they quickly elevate platelet counts and are accessible across most healthcare settings. Physicians commonly initiate corticosteroid therapy immediately after diagnosis, especially in patients presenting with symptomatic thrombocytopenia or active bleeding. Clinical guidelines from major hematology organizations continue to support corticosteroids as the standard initial intervention before progressing to second-line targeted therapies. In addition, their relatively low cost and widespread availability across hospital and retail pharmacies make them an accessible option in both developed and emerging healthcare systems. Although long-term use may lead to adverse effects, short-course treatment strategies and optimized dosing protocols have improved patient management. As global awareness of immune thrombocytopenia increases and early diagnosis becomes more common, corticosteroids are expected to remain the most frequently utilized therapeutic option.

By Disease Type Insights

The acute ITP segment is expected to capture 27.9% of the global idiopathic thrombocytopenic purpura therapeutics market in 2026. This segment’s prominence reflects the urgent clinical management required when patients initially present with severe thrombocytopenia or bleeding manifestations. Acute ITP frequently develops suddenly, particularly in children and younger adults, requiring prompt pharmacological intervention to stabilize platelet levels. Physicians typically initiate treatment using corticosteroids or intravenous immunoglobulin therapies to rapidly increase platelet counts and reduce hemorrhagic risk. Because acute cases often demand immediate medical attention and monitoring, they account for a substantial proportion of treatment volumes within hospitals and specialty hematology clinics. Improvements in diagnostic testing and platelet monitoring technologies have enabled clinicians to identify immune-mediated platelet destruction more efficiently, facilitating early therapeutic intervention.

Additionally, physician awareness and clinical guideline updates have improved standardized management of newly diagnosed patients. While some individuals experience spontaneous remission, many still require short-term pharmacological treatment during the acute phase. The consistent need for immediate therapy and physician supervision ensures that acute ITP remains a major contributor to therapeutic demand across global healthcare systems.

By Distribution Channel Insights

Hospital pharmacies are anticipated to represent 46.7% of the idiopathic thrombocytopenic purpura therapeutics market in 2026. Their leadership is largely attributed to the administration of specialized hematology drugs and the clinical monitoring required for many ITP treatments. Biologic and targeted therapies such as Romiplostim, Eltrombopag, and Fostamatinib are frequently initiated under hospital supervision to ensure appropriate dosage adjustments and patient safety. Hospitals also manage severe thrombocytopenia cases where patients require rapid platelet recovery through intravenous immunoglobulin or immunomodulatory therapies.

The presence of hematologists, transfusion specialists, and advanced laboratory services enables hospitals to provide comprehensive care for patients experiencing complex immune-mediated platelet disorders. Furthermore, tertiary care centers and academic hospitals handle a significant share of ITP diagnoses and follow-up monitoring, leading to higher prescription volumes within institutional pharmacy networks. Many healthcare systems also reimburse specialty drugs primarily through hospital-based distribution channels, reinforcing their market dominance. As targeted biologic therapies continue expanding and clinical monitoring remains essential for treatment optimization, hospital pharmacies are expected to remain the central distribution channel for ITP therapeutics.

Region-wise Insights

North America Idiopathic Thrombocytopenic Purpura Therapeutics Market Trends

North America is expected to hold the largest share of the idiopathic thrombocytopenic purpura therapeutics market in 2026, accounting for 46.7% of global revenue. The region benefits from an advanced hematology treatment ecosystem supported by specialized clinics, academic medical centers, and extensive pharmaceutical research activity. The United States represents the primary contributor due to high awareness of rare autoimmune disorders and strong diagnostic capabilities that allow physicians to identify immune thrombocytopenia at earlier stages. Well-established reimbursement frameworks enable patients to access high-cost biologic therapies and targeted treatments that significantly improve platelet response rates.

Additionally, the presence of leading pharmaceutical companies developing innovative therapies, including thrombopoietin receptor agonists and kinase inhibitors, accelerates the adoption of new treatment options. Hospitals across North America also participate actively in clinical trials investigating next-generation immunomodulatory drugs designed to improve long-term disease control. Growing awareness campaigns conducted by hematology associations and patient advocacy organizations are further improving disease recognition and treatment adherence. Continuous investment in biotechnology research, strong healthcare infrastructure, and rapid regulatory approvals for novel therapies collectively reinforce North America’s leadership position in the global ITP therapeutics landscape.

Europe Idiopathic Thrombocytopenic Purpura Therapeutics Market Trends

Europe represents a well-established yet steadily expanding market for idiopathic thrombocytopenic purpura therapeutics. Countries including Germany, France, the United Kingdom, and Italy form the core of the regional market due to their strong public healthcare systems and well-developed hematology treatment networks. Clinical management across Europe typically follows standardized treatment guidelines developed by leading hematology societies, ensuring consistent therapeutic strategies for newly diagnosed and chronic ITP patients. Increasing awareness of autoimmune blood disorders and improved access to hematology specialists have contributed to more accurate diagnosis and early intervention. Hospitals and specialty clinics across the region are increasingly adopting advanced therapies such as thrombopoietin receptor agonists and targeted immune-modulating drugs to achieve sustained platelet response in patients with refractory disease.

Additionally, European academic institutions and research hospitals are actively engaged in clinical trials aimed at improving long-term remission rates and reducing treatment-related side effects. Aging demographics across several European countries may also contribute to higher diagnosis rates of immune-related hematologic conditions. Combined with strong regulatory oversight and emphasis on evidence-based clinical practice, Europe continues to maintain a stable and technologically progressive position in the global ITP therapeutics market.

Asia Pacific Idiopathic Thrombocytopenic Purpura Therapeutics Market Trends

Asia Pacific is projected to be the fastest-growing regional market for idiopathic thrombocytopenic purpura therapeutics, registering a CAGR of approximately 7.4% between 2026 and 2033. Rapid expansion of healthcare infrastructure across countries such as China, India, Japan, and South Korea is improving access to specialized hematology care and advanced diagnostic testing. Increased awareness of autoimmune blood disorders among healthcare professionals has led to improved identification of immune thrombocytopenia cases that previously remained undiagnosed. Governments across the region are investing heavily in strengthening hospital networks and expanding specialty medical services, including hematology departments capable of managing complex platelet disorders. Pharmaceutical companies are also expanding their regional presence to introduce advanced therapies such as thrombopoietin receptor agonists and targeted kinase inhibitors.

Growing healthcare expenditure and improving insurance coverage are gradually making these innovative treatments more accessible to a broader patient population. Furthermore, Asia Pacific is witnessing an increase in clinical research collaborations and regional trials evaluating emerging therapies for immune thrombocytopenia. As diagnostic awareness improves and healthcare infrastructure continues to modernize, the region is expected to become a major contributor to the long-term growth of the global ITP therapeutics market.

Competitive Landscape

The global idiopathic thrombocytopenic purpura therapeutics market is highly competitive, with strong participation from Amgen Inc., Novartis AG, F. Hoffmann-La Roche Ltd., GSK plc, Grifols, S.A., and Rigel Pharmaceuticals, Inc. These players leverage strong hematology portfolios, global specialty-drug distribution networks, physician awareness programs, and continued innovation in thrombopoietin receptor agonists, monoclonal antibodies, and immunomodulatory therapies to support effective ITP management.

Growing diagnosis rates of chronic immune thrombocytopenia and rising demand for targeted therapies are accelerating innovation, with manufacturers focusing on novel mechanisms of action, improved long-term platelet response therapies, expanded clinical trials, and broader access across emerging healthcare systems to enhance treatment outcomes and patient quality of life.

Key Industry Developments:

- In August 2025, the U.S. Food and Drug Administration approved Wayrilz (rilzabrutinib) for the treatment of adults with persistent or chronic immune thrombocytopenia (ITP) who have shown an inadequate response to prior therapy. The approval was supported by findings from the Phase 3 LUNA 3 clinical trial, where the therapy successfully achieved both primary and secondary study endpoints, demonstrating sustained improvements in platelet counts along with meaningful reductions in other disease-related symptoms.

- In August 2025, Novartis AG reported positive top-line results from the Phase III VAYHIT2 clinical trial, which evaluated Ianalumab in combination with Eltrombopag for patients with primary immune thrombocytopenia previously treated with corticosteroids. The combination therapy significantly extended time to treatment failure compared with placebo plus eltrombopag. Ianalumab is also being studied in additional B-cell–driven autoimmune diseases, including ongoing Phase III trials in first-line ITP and warm autoimmune hemolytic anemia, with results expected in 2026.

Companies Covered in Idiopathic Thrombocytopenic Purpura Therapeutics Market

- Amgen Inc.

- Novartis AG

- F. Hoffmann-La Roche Ltd

- GSK plc.

- Grifols, S.A.

- Rigel Pharmaceuticals, Inc.

- Swedish Orphan Biovitrum AB (publ)

- argenx SE

- Sanofi S.A.

- Takeda Pharmaceutical Company Limited

- CSL Limited

- Octapharma AG

- Pfizer Inc.

- Bristol Myers Squibb Company

- Kissei Pharmaceutical Co., Ltd.

- Others

Frequently Asked Questions

The global idiopathic thrombocytopenic purpura therapeutics market is projected to be valued at US$ 712.8 Mn in 2026.

Rising diagnosis rates of chronic ITP and increasing adoption of advanced therapies such as Eltrombopag, Romiplostim, and Fostamatinib are major drivers of the global idiopathic thrombocytopenic purpura therapeutics market.

The global idiopathic thrombocytopenic purpura therapeutics market is poised to witness a CAGR of 5.8% between 2026 and 2033.

Expansion of targeted biologics and thrombopoietin receptor agonists, along with improved access to specialty therapies in emerging healthcare markets, presents significant opportunities in the global idiopathic thrombocytopenic purpura therapeutics market.

Amgen Inc., Novartis AG, F. Hoffmann-La Roche Ltd., GSK plc., Grifols, S.A., and Rigel Pharmaceuticals, Inc. are some key players in the idiopathic thrombocytopenic purpura therapeutics market.