- Pharmaceuticals

- Juvenile Idiopathic Arthritis Therapeutics Market

Juvenile Idiopathic Arthritis Therapeutics Market Size, Share, and Growth Forecast, 2025 - 2032

Juvenile Idiopathic Arthritis Therapeutics Market by Product Type (Computed Tomography, Magnetic Resonance Imaging, Ultrasonography and Echocardiography, Nuclear Imaging), Route of Administration (Orally, Subcutaneously), Drug Class, and Regional Analysis for 2025 - 2032

Juvenile Idiopathic Arthritis Therapeutics Market Size and Trend Analysis

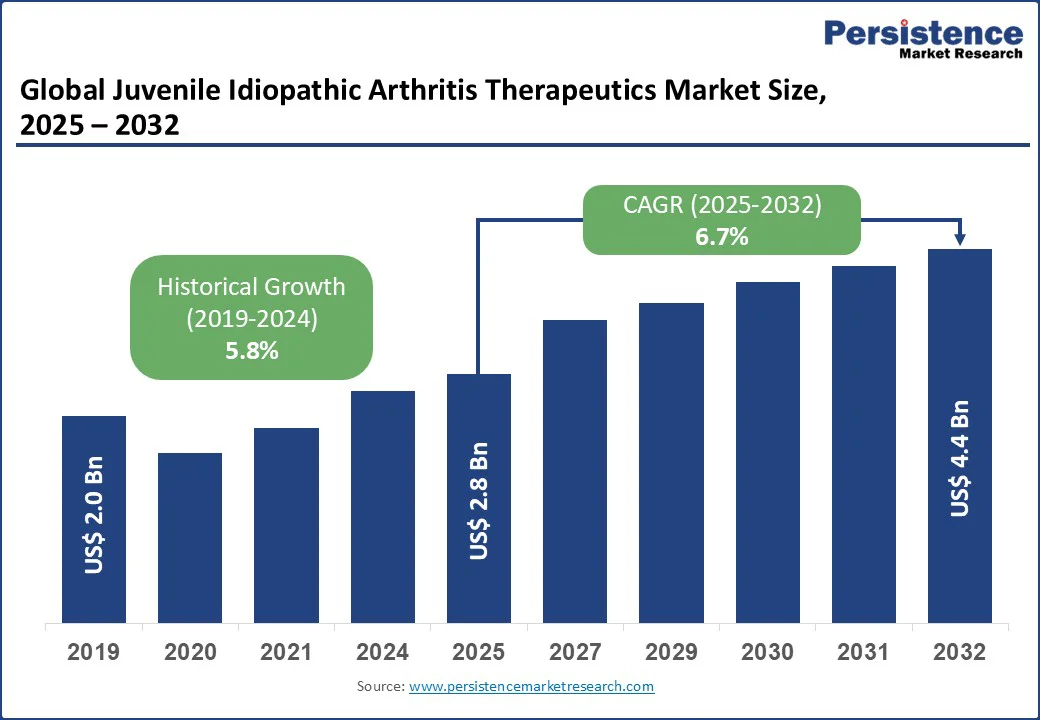

The global juvenile idiopathic arthritis therapeutics market size is likely to be valued at US$2.8 Bn by 2025 and is expected to reach US$4.4 Bn by 2032 at a CAGR of 6.7% during the forecast period from 2025 to 2032, driven by increasing awareness of early diagnosis and treatment options for juvenile idiopathic arthritis (JIA), advancements in biologic therapies, and the rising prevalence of autoimmune disorders among children globally.

Key Industry Highlights:

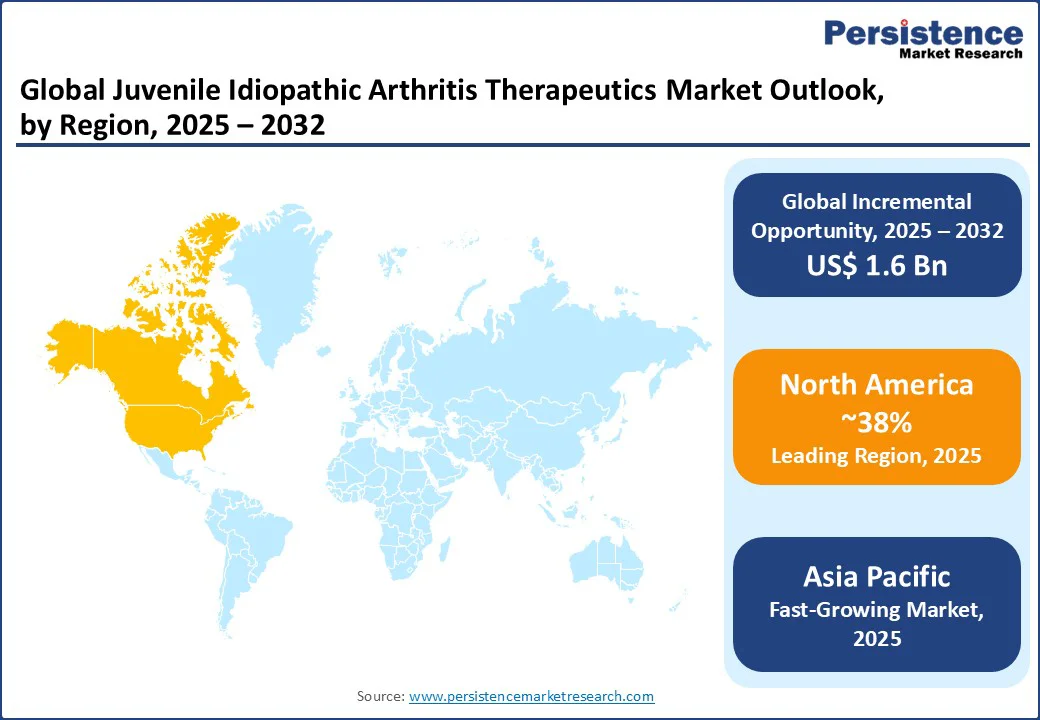

- Leading Region: North America is likely to hold a 38% share in 2025, driven by advanced healthcare infrastructure and high awareness of autoimmune disorders in the U.S.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, fueled by rising pediatric healthcare investments and increasing diagnosis rates in China and India.

- Dominant Product Type: Ultrasonography and Echocardiography account for a 35% share, favored for their non-invasive nature and real-time monitoring capabilities in JIA assessment.

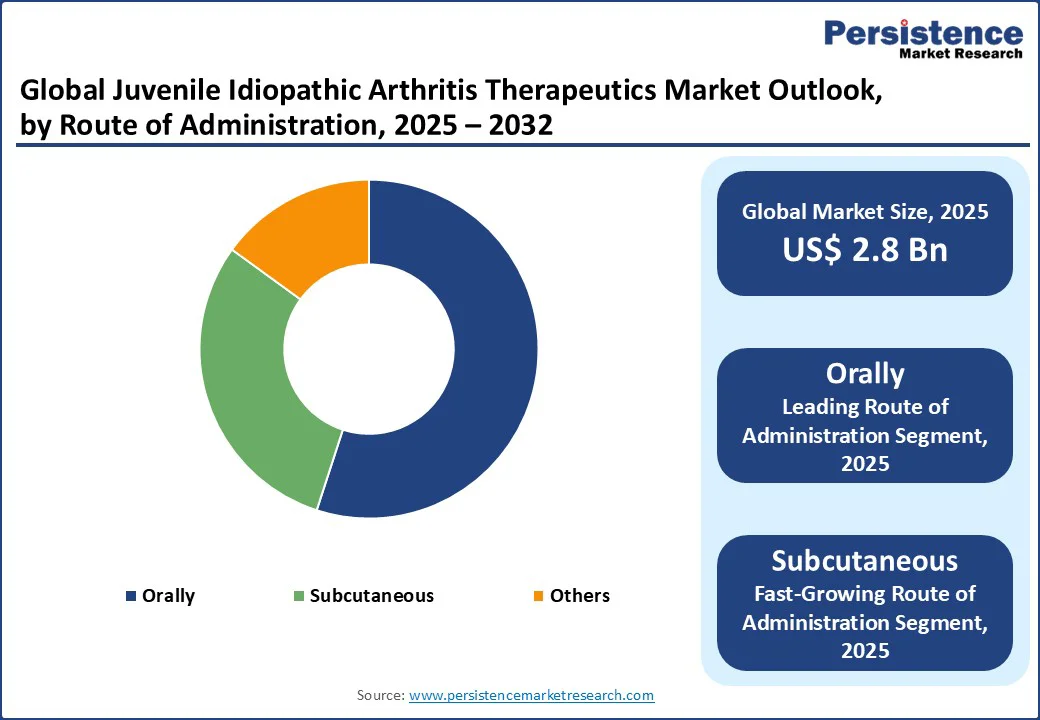

- Leading Route of Administration: Orally administered therapeutics dominate with over 55% of market revenue, driven by ease of use in pediatric populations.

- Leading Drug Class: Disease-modifying antirheumatic drugs (DMARDs) hold a 40% share, due to their role in long-term disease management and remission induction.

| Key Insights | Details |

|---|---|

| Juvenile Idiopathic Arthritis Therapeutics Market Size (2025E) | US$ 2.8 Bn |

| Market Value Forecast (2032F) | US$ 4.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.8% |

Market Dynamics

Driver: Rising Demand for Biologic Therapies and Early Diagnosis

The increasing consumer preference for biologic therapies and early diagnostic interventions is a primary driver of the juvenile idiopathic arthritis therapeutics market. Early diagnosis within the first few months of symptom onset significantly reduces joint damage, creating strong demand for advanced imaging techniques and targeted therapies.

Biologic prescriptions for JIA have continued to rise, supported by new approvals such as subcutaneous TNF inhibitors that provide better remission outcomes compared to traditional DMARDs. This shift is further reinforced by the growing prevalence of JIA in urban populations, where lifestyle factors play a role, and by parents actively seeking safer, non-steroidal alternatives to avoid growth-related side effects.

Advancements in monoclonal antibodies, particularly those directed at IL-6 pathways, are delivering high levels of efficacy and accelerating market growth. Pediatric rheumatology centers have been steadily expanding worldwide, and therapeutic uptake has followed a similar trend.

In regions such as Asia Pacific, government health initiatives have made biologics more accessible through subsidies, further driving adoption. At the same time, heightened parental awareness-amplified by online health education and advocacy campaigns-has encouraged a shift toward proactive disease management, helping to preserve long-term skeletal health and reduce the healthcare burden associated with untreated cases.

Restraint: High Costs Associated with Biologic Drugs and Advanced Imaging

The high costs linked to biologic drugs and advanced imaging technologies serve as a major restraint for the juvenile idiopathic arthritis therapeutics market. While biologics provide superior efficacy and long-term disease control, their premium pricing places them out of reach for many families, particularly in countries where healthcare spending is predominantly out-of-pocket.

This cost barrier creates a sharp divide between high-income nations, where broader insurance coverage supports access, and low- to middle-income regions, where availability remains limited.

Reimbursement issues further compound the problem, as advanced diagnostic tools such as MRI scans are often excluded from coverage in underinsured populations, leading to delays in accurate diagnosis and treatment initiation.

Additionally, supply chain interruptions can disrupt the availability of critical biologics, inflate prices and limit continuity of care. The requirement for specialized paediatric formulations, involving precise dosing and customized production, adds further expense. Together, these challenges significantly restrict scalability and equitable adoption.

Opportunity: Expansion of Subcutaneous Administration and Personalized Medicine

The growing shift toward subcutaneous administration routes and personalized medicine represents a significant opportunity for the juvenile idiopathic arthritis therapeutics market. Subcutaneous biologics are increasingly favored by patients and caregivers, as they reduce the need for frequent clinic visits, offer greater convenience, and improve adherence.

This trend not only enhances patient quality of life but also eases the burden on healthcare systems by lowering treatment-associated costs. Alongside this, the integration of personalized medicine approaches, particularly genetic profiling, holds immense promise. By identifying JIA subtypes and tailoring therapies accordingly, treatment responses can be optimized, minimizing trial-and-error prescribing and improving long-term outcomes.

In Asia Pacific where the cost of underdiagnosis remains high, diagnostic solutions such as portable ultrasonography kits are affordable and are easily accessible for early detection. These cost-effective tools can reach underserved populations and open new revenue streams. Collectively, these advancements foster a patient-centred ecosystem, positioning the juvenile idiopathic arthritis therapeutics market for sustained growth and broader global adoption.

Category-wise Analysis

Product Type Insights

Ultrasonography and echocardiography hold a 35% market share in 2025 due to their non-invasive, cost-effective nature and real-time capabilities for joint effusion detection in JIA. Portable pediatric ultrasound systems from companies such as GE Healthcare and Philips support bedside evaluations, with rising adoption in North America and Europe through routine screening protocols that enhance early diagnosis and management.

Magnetic resonance Imaging is emerging as the fastest-growing segment due to its superior ability to detect subclinical synovitis. Growing adoption of gadolinium-free protocols and pediatric-friendly low-field scanners enhances tolerance, while urban markets with higher juvenile idiopathic arthritis incidence continue driving demand.

Route of Administration Insights

Orally administered therapeutics account for over 55% share in 2025, favored for compliance in young patients and ease in home settings. Oral DMARDs such as methotrexate remain the most common initial therapy, with Pfizer and Teva offering child-friendly formulations, supported by innovations such as taste-masked options and growing e-commerce adoption, particularly across North America.

Subcutaneously administered options are the fastest-growing, supported by self-injection devices that simplify biologic delivery. Their convenience appeals to families, with companies such as AbbVie and Amgen leading with pre-filled syringes and expanding alongside telemedicine adoption in Asia Pacific.

Drug Class Insights

Disease-modifying antirheumatic drugs (DMARDs) account for a 40% share in 2025, Driven by their foundational role in slowing disease progression and inducing remission in oligoarticular JIA cases, DMARDs remain essential. Methotrexate continues as the gold standard, with generic availability improving affordability. Companies such as Bristol Myers Squibb and Sanofi supply high-purity formulations globally, with strong focus on North America and Europe.

Tumor necrosis factor blockers are the fastest-growing segment owing to their targeted efficacy in polyarticular JIA. Biologics such as adalimumab continue to drive demand, while biosimilars expand accessibility. Innovators such as Johnson & Johnson and UCB are strengthening their presence in Asia Pacific amid rising systemic JIA cases.

Regional Insights

North America Juvenile Idiopathic Arthritis Therapeutics Market Trends

North America dominates with a 38% global share in 2025, supported by strong research and development initiatives and favorable healthcare infrastructure. The region benefits from extensive insurance coverage, which enhances patient access to advanced biologics and diagnostic modalities.

In the United States, robust funding for clinical trials accelerates the approval of innovative therapies, while an expanding pool of pediatric rheumatologists ensures timely diagnosis and specialized care.

A strong trend toward the integration of biologics, particularly subcutaneous formulations, reflects both patient preference for convenience and the increasing role of telehealth in streamlining consultations and follow-ups. Canada contributes significantly through its universal healthcare system, placing strong emphasis on early screening methods such as MRI to detect subclinical disease.

Together, these factors highlight North America’s leadership, where policy support, clinical expertise, and patient-centered innovations continue to drive adoption, shaping the region as a hub for advanced JIA management and long-term market growth.

Europe Juvenile Idiopathic Arthritis Therapeutics Market Trends

Europe represents a significant share of the juvenile idiopathic arthritis therapeutics market, with Germany and the UK leading regional growth. Germany’s focus on precision medicine, coupled with widespread insurance coverage, has accelerated the adoption of advanced therapies such as TNF blockers.

The UK strengthens its position through National Health Service guidelines that encourage ultrasonography, reducing reliance on invasive diagnostic procedures and supporting early detection. France and Italy contribute steadily, backed by strong public health frameworks and collaborative research initiatives across the region.

EU-funded programs continue to stimulate innovation, particularly in pediatric rheumatology, while fostering cross-border partnerships that improve biosimilar availability and help contain treatment costs. Rising incidences of JIA, influenced by lifestyle and environmental factors, further support sustained demand.

Overall, Europe’s integrated approach-combining supportive policies, advanced healthcare infrastructure, and coordinated research-creates a favorable environment for growth, ensuring patients gain wider access to both innovative biologics and affordable biosimilar options.

Asia Pacific Juvenile Idiopathic Arthritis Therapeutics Market Trends

Asia Pacific is emerging as the fastest-growing region in the juvenile idiopathic arthritis therapeutics market, with China and India at the forefront. In China, government health programs such as Healthy China initiatives are expanding access to essential therapies, including DMARDs, while encouraging the use of oral formulations for easier administration.

India contributes significantly through Ayushman Bharat, improving healthcare accessibility in underserved rural areas and expanding the use of ultrasonography for earlier diagnosis. Japan and South Korea place strong emphasis on biologics, supported by favorable regulatory approvals and demographic trends that prioritize pediatric care.

Across the region, increasing investments in local pharmaceutical manufacturing are reducing reliance on imports, ensuring more sustainable and affordable supply chains. Together, these advancements highlight Asia Pacific’s growing role as a key contributor to market expansion, combining government support, regulatory momentum, and infrastructure development to meet rising demand for innovative and accessible JIA treatments.

Competitive Landscape

The competitive landscape of the global juvenile idiopathic arthritis therapeutics market is moderately consolidated, with leading players maintaining dominance through strategic alliances, research pipelines, and innovation. Key priorities include advancing biosimilars to improve affordability and expanding pediatric-specific formulations. These initiatives aim to address unmet needs, support early intervention, and strengthen long-term market positioning globally.

Key Developments

- June 2024: Regeneron and Sanofi received FDA approval for Kevzara (sarilumab) as a treatment for active polyarticular juvenile idiopathic arthritis in eligible pediatric patients, marking a significant advancement in expanding therapeutic options for childhood arthritis management.

- October 2024: Shorla Oncology’s Jylamvo (liquid methotrexate) was granted expanded FDA approval to include treatment of polyarticular juvenile idiopathic arthritis and acute lymphoblastic leukemia in pediatric patients.

Companies Covered in Juvenile Idiopathic Arthritis Therapeutics Market

- Pfizer

- Roche

- Bristol Myers Squibb

- Mylan

- Eli Lilly

- Takeda

- Celgene

- Johnson & Johnson

- AstraZeneca

- Amgen

- AbbVie

- UCB

- GSK

- Others

Frequently Asked Questions

The juvenile idiopathic arthritis therapeutics market is projected to reach US$2.8 Bn in 2025.

The rising demand for biologic therapies and early diagnosis, along with advancements in imaging technologies, are key market drivers.

The juvenile idiopathic arthritis therapeutics market is poised to witness a CAGR of 6.7% from 2025 to 2032.

The expansion of subcutaneous administration and personalized medicine approaches is a key market opportunity.

Pfizer, Roche, Bristol Myers Squibb, AbbVie, and Johnson & Johnson are key market players.