- Hardware & Software IT Services

- Harbor Management Software Market

Harbor Management Software Market Size, Share, and Growth Forecast, 2026 – 2033

Harbor Management Software Market by Solution (Software, Services), Deployment (Cloud-based, On-premises), Application (Harbor Operations Management, Vessel Traffic & Berth Planning, Cargo & Terminal Management, Billing, Invoicing & Revenue Management, Asset & Maintenance Management, Safety, Security & Compliance, Analytics & Decision Support, Others), and Regional Analysis for 2026 – 2033

Harbor Management Software Market Size and Trends

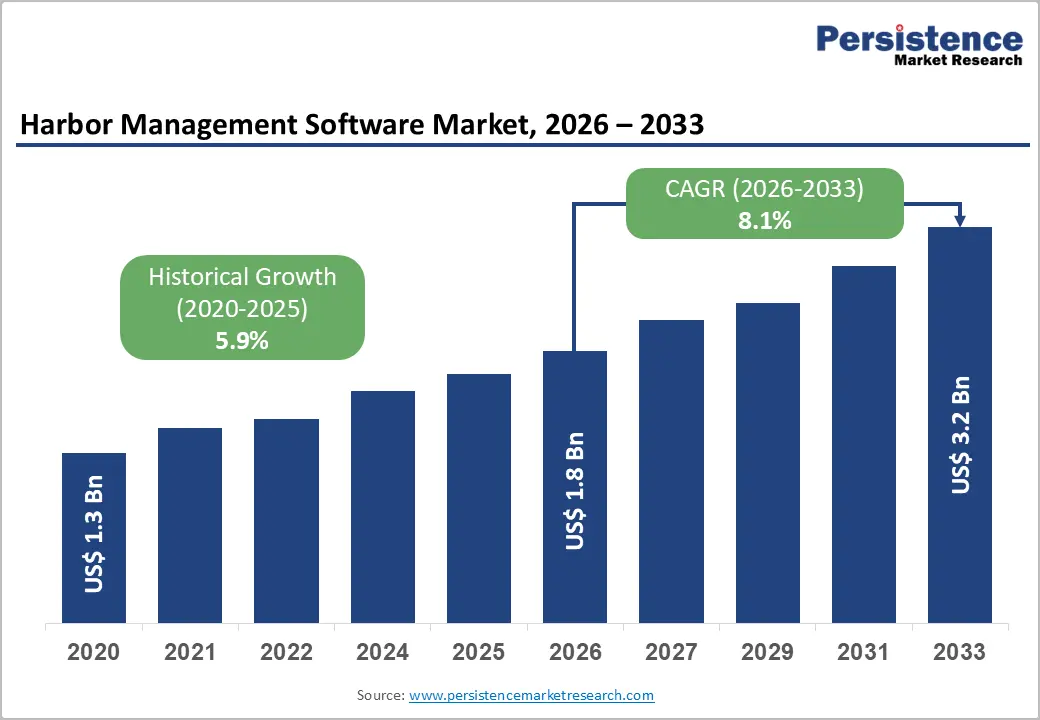

The global harbor management software market size is projected to rise from US$1.8 Bn in 2026 to US$3.2 Bn by 2033. It is anticipated to witness a CAGR of 8.1% during the forecast period from 2026 to 2033, driven by the exponential growth in international maritime trade volumes, increasingly stringent environmental and safety regulations mandated by the International Maritime Organization (IMO), and the technological convergence of artificial intelligence, cloud computing, and Internet of Things (IoT) solutions that enable real-time port optimization and autonomous operations.

Key Industry Highlights:

- Leading Solution: Software dominates with over 68% market share in 2026, valued at more than US$ 1.2 Bn, driven by the need for real-time analytics, automated workflows, and optimized vessel traffic and cargo handling. Services are the fastest-growing segment at 11.7% CAGR, fueled by demand for implementation, integration, training, and managed cybersecurity solutions.

- Leading Deployment: Cloud-based deployment holds over 56% market share in 2026, valued at over US$ 1.0 Bn, preferred for scalability, remote access, and multi-stakeholder collaboration. On-premises deployment is growing at 7.9% CAGR, driven by data sovereignty, cybersecurity, low-latency operations, and deep integration with legacy systems.

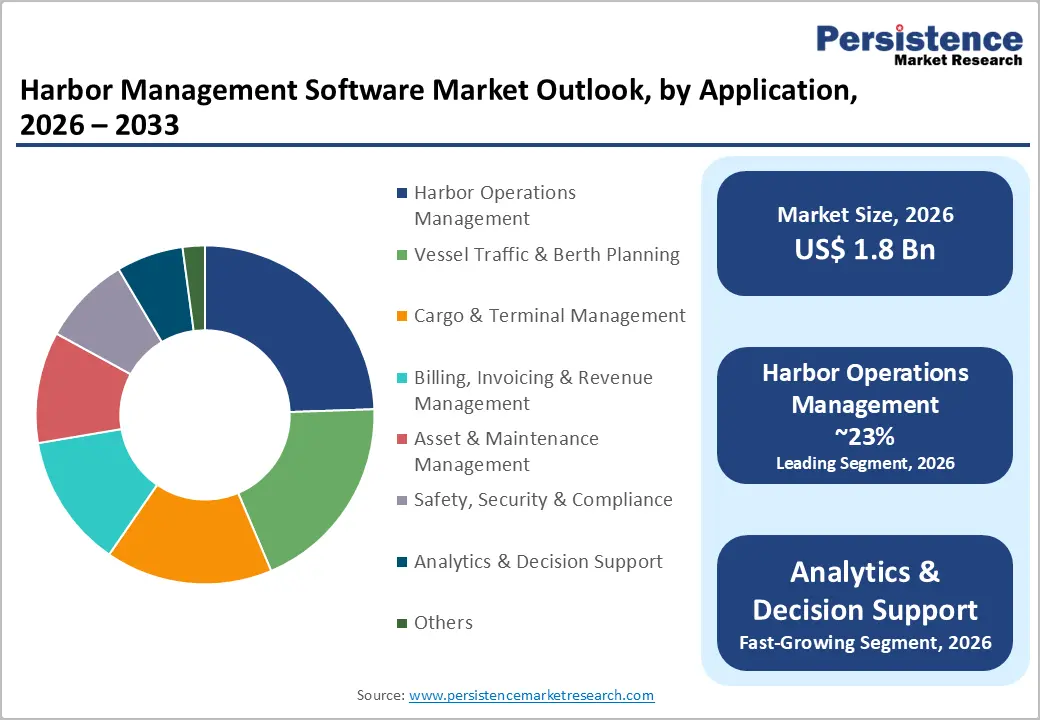

- Leading Application: Harbor operations management commands over 23% market share in 2026, valued at more than US$ 421.4 Mn, due to real-time visibility, predictive analytics, and automated berth scheduling and resource allocation. Analytics & decision support is the fastest-growing application at 12.8% CAGR, supported by rising congestion, larger vessels, and demand for AI-driven predictive insights.

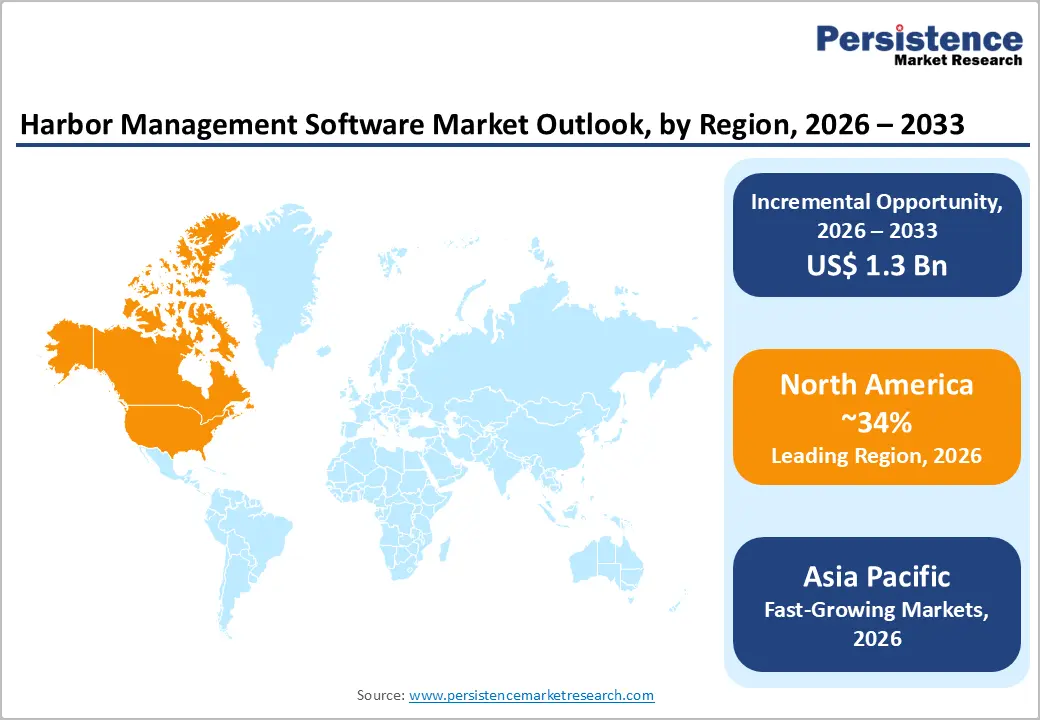

- Leading Region: North America leads with over 34% share in 2026, valued at US$ 622.9 Mn, driven by mature port infrastructure, high trade volumes, and regulatory compliance requirements. Asia Pacific grows fastest at 13.2% CAGR, fueled by rapid port expansion, government-backed smart port initiatives, and large-scale digital modernization projects. Europe holds over 26% share, driven by smart port investments, stringent regulations, and green port infrastructure adoption.

| Key Insights | Details |

|---|---|

| Harbor Management Software Market Size (2026E) | US$1.8 Bn |

| Market Value Forecast (2033F) | US$3.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Dynamics

Driver

Digital Transformation and Port Modernization as a Strategic Imperative

Port authorities and terminal operators worldwide are investing heavily in digital infrastructure to address escalating operational complexity and competitive pressures. The European Union's Digital Europe Programme and the Digital Sovereign Infrastructure Strategy underscore this commitment, with governments allocating substantial capital to modernizing port ecosystems. In Asia-Pacific region, China's Belt and Road Initiative and India's Sagarmala Programme are catalyzing infrastructure investments that directly translate into increased adoption of harbor management software. These initiatives extend beyond software procurement; they represent systemic transformations that require integrated platforms for vessel scheduling, yard management, cargo tracking, and real-time visibility.

Accelerating Global Maritime Trade Volumes and Supply Chain Complexity

International maritime trade volumes are approaching unprecedented levels. In 2024, Global maritime trade volumes reached approximately 12.72 billion tons, growing by about 2.2% compared with the previous year. This surge, combined with e-commerce-driven last-mile logistics and complex multi-modal supply chains, creates operational bottlenecks at key ports. Advanced harbor management solutions with predictive analytics help optimize terminal operations by enabling proactive equipment maintenance and minimizing downtime, ensuring smoother, more efficient port operations.

Restraint

Integration Complexity and Legacy System Interoperability

Harbor management software faces significant restraints due to the complexity of interoperating with heterogeneous legacy systems such as TOS, ERP, customs, and third-party logistics platforms, each using proprietary data formats and protocols. The lack of standardization across ports using EDI, API, SOAP, REST, FTP/SFTP, CSV, XML, and JSON require extensive customization, increasing implementation time, cost, and operational risks. Smaller and medium-sized terminals (SMEs) are especially impacted, as limited technical infrastructure and financial resources hinder complex multi-system integration, slowing market growth.

High Capital Investment and Implementation Challenges

Substantial upfront costs for software licensing, infrastructure upgrades, customization, and professional services limit the adoption of HMS. SMEs face barriers due to limited capital budgets and the need for extensive staff training, which adds operational expenses and organizational change challenges. Long implementation periods of 12–24 months disrupt terminal operations, reduce productivity, and impact customer satisfaction, making smaller ports cautious about adopting advanced HMS solutions.

Opportunity

AI and Machine Learning–Driven Predictive Operations

Artificial intelligence and machine learning integration are creating growth opportunities by enabling predictive, data-driven port operations. AI-powered systems optimize berth allocation, tug and pilot deployment, and vessel scheduling, reducing operating distances by up to 20% and significantly lowering vessel waiting times. Machine learning models analyze historical vessel, weather, equipment, and port-constraint data to predict maintenance needs and forecast demand with higher accuracy. Vendors such as Tideworks Technology are launching advanced data platforms to capture and normalize real-time operational data. Continuous learning across global terminals allows early adopters to achieve compounding efficiency gains and stronger competitive positioning.

Blockchain-Driven Transaction Automation and Documentation Efficiency

Blockchain integration in port operations creates significant opportunities by streamlining documentation and customs clearance processes. Smart contracts automate approvals, payments, and cargo release, reducing processing times by up to 60-80% and minimizing manual intervention. Successful pilots at ports such as Antwerp, Rotterdam, and Valencia highlight strong operational validation. Blockchain strengthens fraud prevention, enables real-time cargo tracking with immutable records, and simplifies trade finance workflows. As regulations increasingly mandate digital trade documentation and cyber transparency, blockchain-enabled harbor management solutions are becoming mission-critical systems.

Category-wise Analysis

Solution Analysis,

Software dominates the global market, capturing more than 68% market share in 2026 with a value exceeding US$ 1.2 Bn, due to increasing prioritization of digital tools to manage complex maritime operations. Advanced software enables real-time data analytics, automated workflows, and better decision-making, which are essential to optimize vessel traffic, cargo handling, and resource allocation as trade volumes rise. It also supports cloud-based, scalable platforms that improve collaboration across stakeholders and reduce turnaround times, making software solutions more indispensable than services. Integration with IoT, AI, and machine learning further enhances operational efficiency and responsiveness, driving software adoption.

Services demonstrate the highest growth rate at 11.7% CAGR due to the increasing complexity of enterprise port management systems creating demand for implementation, systems integration, and managed services, the skills gap in maritime technology requiring extensive training and change management support, and the growing emphasis on managed security services to address heightened cybersecurity risks. Major vendors are expanding their services organizations to capture the high-margin, sticky revenue opportunities that professional services provide, creating increasingly bundled solutions that combine software licensing with comprehensive managed services.

Deployment Analysis,

Cloud-based holds over 56% market share in 2026, with a value exceeding US$ 1.0 Bn, due to the need for flexible, scalable, and cost-effective solutions. These platforms allow remote access to real-time operational data and collaboration across multiple stakeholders, which is essential for optimizing vessel scheduling, cargo handling, and resource allocation in today’s dynamic maritime environment. They also reduce upfront IT infrastructure costs and ongoing maintenance burdens, making advanced software accessible to ports of all sizes.

On-premises are expected to grow at a significant rate, with a CAGR of 7.9% due to the need for data sovereignty, cybersecurity, and operational control. Large and strategic ports handle sensitive vessel, cargo, and customs data, making local deployment preferable to meet national security and regulatory compliance requirements. It supports low-latency, uninterrupted operations, which are critical during peak traffic and limited connectivity scenarios. Many ports rely on deep integration with legacy TOS and infrastructure, where on-premises solutions offer greater customization and reliability.

Application Analysis,

Harbor operations management commands the largest market share at over 23% in 2026 with a value exceeding US$ 421.4 Mn, driven by efficient handling of vessel traffic, cargo operations, berth scheduling and resource allocation is central to everyday port functioning. Ports under pressure from rising global maritime trade need real-time visibility and automated workflows to cut turnaround times, optimize asset use, and reduce costs. Advanced software delivers data-driven decision support, predictive analytics, and integrated dashboards that directly address these operational challenges.

Analytics & decision support are expected to grow at a CAGR of 12.8% as ports face rising congestion, vessel size growth, and tighter turnaround time requirements. Port authorities and terminal operators increasingly need real-time visibility, predictive insights, and scenario planning to optimize berth allocation, yard utilization, and workforce deployment. Growing cargo volumes and weather-related disruptions are driving demand for AI-based forecasting and risk management tools. Data-driven decision support is becoming essential to meet regulatory compliance, sustainability targets, and cost-efficiency goals across port operations.

Regional Insights

North America Harbor Management Software Market Trends

North America holds over 34% share in 2026, reaching US$ 622.9 Mn value, driven by mature port infrastructure, high trade volumes, and strong digital readiness. Regulatory pressure is a key accelerator, particularly the U.S. Coast Guard’s January 2025 final rule 33 CFR Part 6 mandating cybersecurity plans, incident reporting, and designated Cybersecurity Officers for ports and vessels. These near-term compliance deadlines create urgent software adoption needs, exceeding regulatory timelines in Europe and Asia-Pacific. A robust technology ecosystem combining venture capital, consulting expertise, and high cloud adoption supports the rapid deployment of advanced, API-driven harbor platforms. While established vendors dominate large ports, cloud-native HMS providers are gaining share among operators modernizing legacy systems.

Asia Pacific Harbor Management Software Market Trends

Asia Pacific is expected to grow at the highest rate with a CAGR of 13.2%, due to rapid expansion in maritime trade, large-scale port infrastructure investments, and government-backed smart port programs. China leads the region, with Shanghai, Shenzhen, and Ningbo collectively handling ~200 million TEU annually, supported by advanced harbor management systems integrating AI, autonomous terminals, and predictive analytics. Technology leadership is further reinforced by Singapore and Japan’s Port of Tokyo through autonomous vessel guidance and end-to-end digital logistics platforms. Meanwhile, India’s major ports Mumbai, JNPT, Paradip, are undergoing digital modernization under national initiatives, while ASEAN ports in Vietnam, Thailand, and Indonesia are expanding capacity, driving demand for integrated, scalable harbor management software.

Europe Harbor Management Software Market Trends

Europe is expected to hold more than 26% share by 2026, driven by smart port leaders such as Rotterdam, Hamburg, and Antwerp, which are heavily investing in automation, AI-driven optimization, and green port infrastructure. Stringent EU regulations including EU ETS, environmental compliance mandates, and the European Maritime Single Window (EMSW) create sustained demand for advanced, multi-jurisdictional harbor management software. European HMS deployments emphasize environmental sustainability modules, NIST-aligned cybersecurity, and integration with LNG and zero-emission vessel infrastructure. Additionally, frameworks like the EU Digital Identity Wallet (EU 2024/1183) and strict data sovereignty requirements favor EU-based vendors and cloud providers that ensure cross-border trust, secure documentation, and in-region data residency.

Competitive Landscape

The harbor management software market is largely fragmented, with numerous regional and global players vying for contracts with port authorities and private terminal operators. Manufacturers focus on customization and integration capabilities, ensuring their solutions seamlessly connect with existing port operating systems and logistics platforms. Many emphasize advanced analytics, AI, and automation features to differentiate themselves, while some leverage strategic partnerships and service-based offerings to expand their client base.

Key Industry Developments

- In March 2025, HarborLab launched HL AI, an AI-powered feature that optimizes Disbursement Account (DA) analysis and streamlines port expense management. Innovation helps shipowners and operators gain real-time insights, automate processes, and reduce financial risks associated with managing millions in annual port-related spending.

- In January 2024, Harbor Lab partnered with Great Eastern Shipping Co. Ltd., India’s largest private-sector shipping company, to optimize port cost management. Great Eastern Shipping will leverage Harbor Lab’s full suite of solutions for all commercial and husbandry port calls, enhancing operational efficiency and streamlining agency operations.

Companies Covered in Harbor Management Software Market

- Navis LLC

- Harba ApS

- Harbour Mastery Inc.

- Saab Technologies

- INEA Port Solutions

- PortPro

- J.F. Brennan Company Inc.

- Nautical Software Solution

- Pacsoft International Ltd.

- Leonardo Spa

- Kongsberg Gruppen

- Softship AG

- Others

Frequently Asked Questions

The global market is projected to be valued at US$1.8 Bn in 2026.

The need for efficient port operations, real-time vessel tracking, and streamlined cargo and logistics management to reduce congestion and operational costs is a key driver of the market.

The market is expected to witness a CAGR of 8.1% from 2026 to 2033.

Adopting AI and IoT for predictive port operations, digitalizing maritime logistics, and expanding smart port initiatives is creating strong growth opportunities.

Navis LLC, Harba ApS, Harbour Mastery Inc., Saab Technologies, INEA Port Solutions, PortPro are among the leading key players.