- Food Ingredients & Additives

- Guar Gum Market

Guar Gum Market Size, Share, and Growth Forecast 2026 - 2033

Guar Gum Market by Grade (Food-Grade, Industrial-Grade, Pharmaceutical-Grade), by Application (Food & Beverage, Oil & Gas (Hydraulic Fracturing/Fracking), Pharmaceuticals, Cosmetics & Personal Care, Textile Industry, Others), by Regional Analysis, 2026 - 2033

Guar Gum Market Size and Trend Analysis

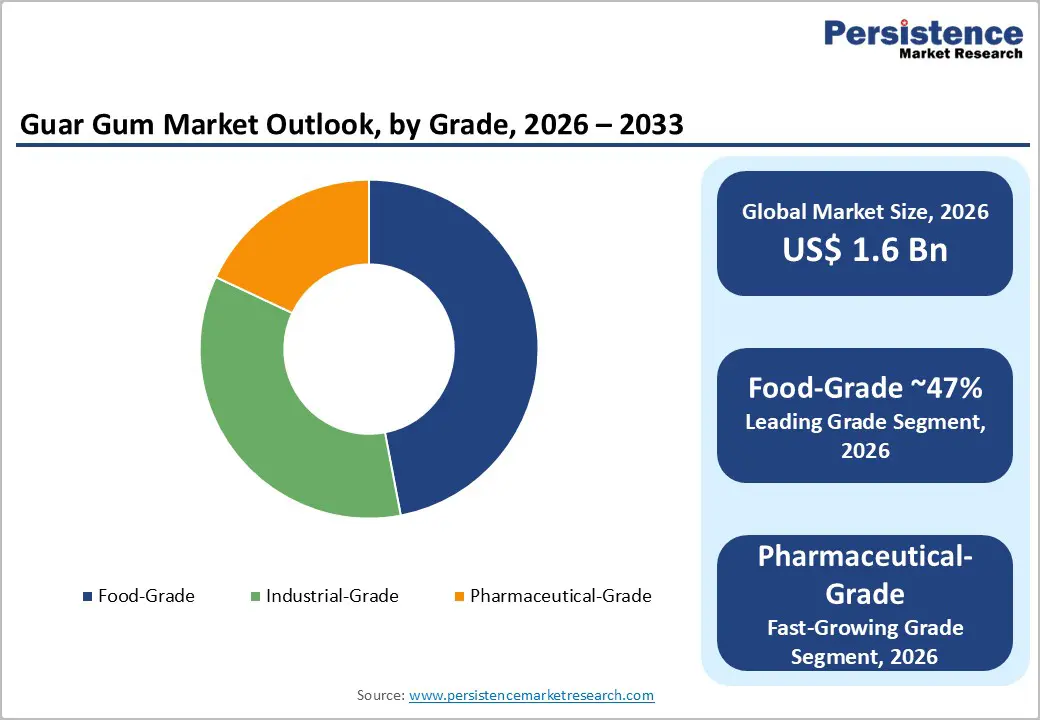

The global guar gum market size is expected to be valued at US$ 1.6 billion in 2026 and projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 6.9% between 2026 and 2033. It is driven by its versatile functionality as a natural thickening, stabilizing, and binding agent derived from guar beans.

Widely used across food & beverage, oil & gas, pharmaceuticals, and personal care industries, guar gum plays a critical role in improving texture, viscosity, and product stability. Demand is strongly influenced by hydraulic fracturing activities in the energy sector and increasing preference for clean-label, plant-based ingredients in food applications. With India as the leading producer and exporter, the market benefits from strong supply dynamics. Growing industrial applications and sustainability trends continue to support steady global market expansion.

Key Industry Highlights:

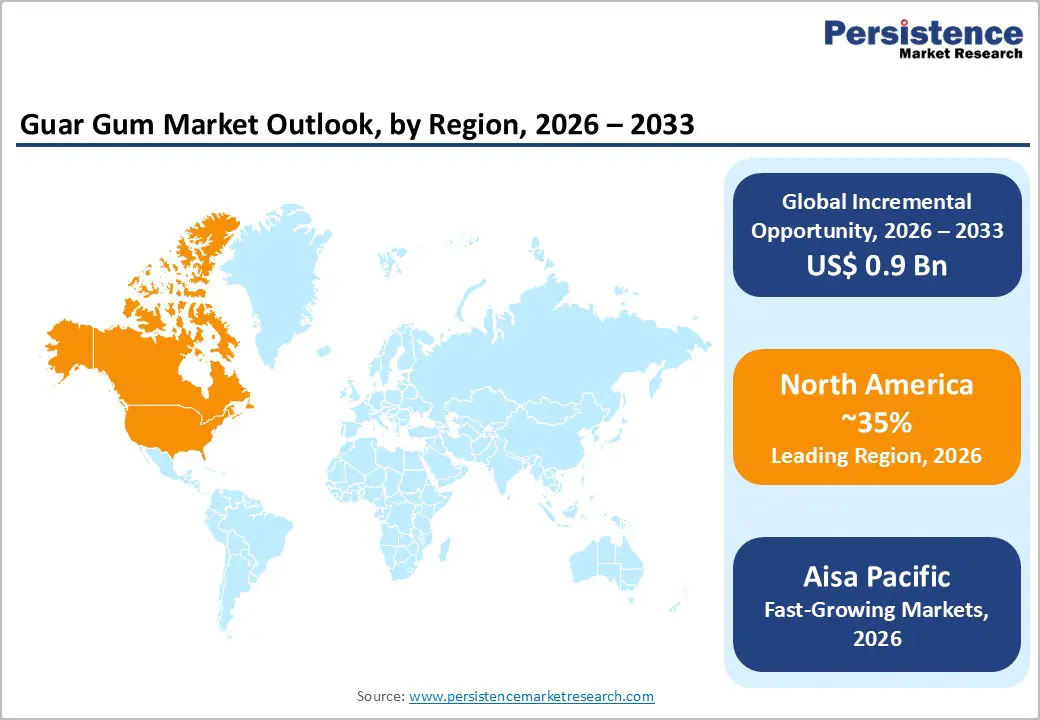

- Leading Region: North America accounts for 40% share, driven by strong oil & gas fracturing activity in the U.S., high processed food consumption, and well-established regulatory frameworks such as FDA GRAS approvals supporting guar gum usage.

- Fastest Growing Region: Asia Pacific is the fastest growing, led by India as the global production hub, along with rising consumption in China, Japan, and ASEAN driven by demand for natural hydrocolloids in food, beverage, and personal care applications.

- Dominant Segment: The food-grade segment is expected to capture 47% of the market in 2025, driven by the growing preference for gluten-free and clean-label products.

- Fastest Growing Segment: Pharmaceutical-grade guar gum is the fastest growing, driven by increasing use as a natural excipient and controlled-release agent in oral solid dosage forms and nutraceuticals, along with rising demand for fiber-based health ingredients.

- Key Opportunity: Growth opportunities lie in sustainable and traceable guar sourcing, where suppliers adopting responsible farming practices, water-efficient cultivation, and certification programs can secure long-term contracts with global food, personal care, and oil & gas companies focused on ESG and transparent supply chains.

| Key Insights | Details |

|---|---|

| Global Guar Gum Market Size (2026E) | US$ 1.6 billion |

| Market Value Forecast (2033F) | US$ 2.5 billion |

| Projected Growth CAGR (2026 - 2033) | 6.9% |

| Historical Market Growth (2020 - 2025) | 6.2% |

Market Dynamics

Drivers - Expanding oil & gas output supporting demand for fracturing fluids

The rising global oil production outlook is significantly strengthening demand for hydraulic fracturing inputs, particularly hydrocolloids used as viscosifying agents. Global liquid fuel production is projected to increase by approximately 1.3 million barrels per day in 2025 and 1.2 million barrels per day in 2026, driven largely by expansion in the U.S., Canada, Brazil, and Guyana. These countries are accelerating upstream investments, shale exploration, and production capacity additions, all of which directly increase the consumption of fracturing fluids where guar gum plays a critical functional role in maintaining viscosity and proppant suspension.

Additionally, OPEC+ production is expected to grow by around 0.5 million barrels per day in 2026, while non-OPEC+ countries contribute significantly to supply expansion. The revival of drilling activities, particularly in North America and emerging South American basins, supported by relatively stable crude prices, is boosting the adoption of cost-efficient and performance-driven additives. This sustained momentum in unconventional oil extraction is expected to remain a key demand driver for industrial-grade guar gum in the coming years.

Restraints - Facility closures in Japan create structural supply constraints

The post-pandemic recovery of the global pharmaceutical sector is being constrained by tightening healthcare budgets across several economies. According to global projections, nearly 41 governments are expected to reduce healthcare spending by 2027 compared to pre-pandemic levels, particularly affecting low- and middle-income countries. This reduction is leading to decreased production of non-essential drugs and supplements, where excipients such as guar gum are commonly used as stabilizers and binding agents. As a result, demand from the pharmaceutical segment is facing structural pressure.

Moreover, rise in inflation, increased public health debt, and the burden of aging populations are forcing healthcare systems to prioritize cost efficiency over product enhancement. Pharmaceutical companies are increasingly optimizing formulations to reduce input costs, limiting the inclusion of specialty excipients. Reduced hospital procurement levels and shrinking public drug inventories are further dampening demand, particularly in price-sensitive markets, thereby restraining growth potential for pharmaceutical-grade guar gum.

Opportunities - Accelerating innovation in sustainable food systems across the Europe

The European food and beverage industry is undergoing a structural shift toward sustainability, creating strong opportunities for natural and plant-based ingredients. With the sector generating approximately €1.2 trillion in turnover and €250 billion in value-added, there is increasing regulatory and consumer pressure to adopt clean-label, bio-based, and environmentally sustainable ingredients. Around 65% of intra-regional exports and strong external trade further highlight the scale at which reformulation trends can influence ingredient demand.

This transition is encouraging manufacturers to replace synthetic emulsifiers and stabilizers with natural hydrocolloids such as guar gum. The demand for biodegradable, traceable, and sustainably sourced ingredients is rising, driven by EU regulations and corporate ESG commitments. While reformulation may involve short-term cost pressures, it opens long-term growth avenues for suppliers offering scalable and environmentally compliant solutions. Companies investing in sustainable sourcing, certification, and innovation in food-grade applications are well-positioned to capitalize on this evolving market landscape.

Category wise Analysis

Grade Insights

Food-grade guar gum accounts for the highest share of approximately 46.9%, primarily driven by the increasing global preference for natural, clean-label, and plant-based ingredients in food and beverage applications. Manufacturers are increasingly incorporating it as a thickening, stabilizing, and emulsifying agent in dairy products, bakery items, confectionery, sauces, and gluten-free formulations. Rising consumer awareness regarding gut health, dietary fiber intake, and improved food texture has further strengthened its demand. Regulatory approvals across major markets such as the U.S., EU, and Asia-Pacific have reinforced its safe and widespread adoption.

Additionally, rapid urbanization, rising disposable incomes, and the expansion of organized retail and packaged food sectors in developing economies are fueling consumption. The shift toward convenience foods and ready-to-eat products is further accelerating usage. Growth remains strong in regions focusing on natural food additives, where manufacturers are actively reformulating products to replace synthetic ingredients with plant-derived alternatives like guar gum.

Application Insights

The oil & gas segment accounts for the largest share among application areas, reflecting its critical role in hydraulic fracturing operations. Guar gum is extensively used as a viscosifying agent in fracturing fluids, helping to suspend and transport proppants during drilling. Increasing global energy demand and rising investments in upstream exploration and production activities are key factors driving this segment. Major regions such as North America, the Middle East, and India continue to expand drilling operations, boosting demand for efficient and cost-effective additives.

India’s refining capacity expansion, projected to grow significantly in the coming years, along with strong petroleum export activity, is further supporting upstream investments. Additionally, the presence of a global supply cushion and continued focus on energy security are encouraging exploration and production activities worldwide. Countries such as the U.S., India, and Gulf nations are expected to remain key demand centers, sustaining long-term growth in this application segment.

Regional Insights

North America Guar Gum Market Trends and Insights

North America is the leading regional market for guar gum, with an estimated 35% share of global demand in 2026, underpinned by its large oil & gas and advanced processed food industries. The U.S. is a major importer of guar gum from India, historically accounting for tens of thousands of tonnes annually, mainly for hydraulic fracturing fluids in shale plays. Technical analysis confirms that guar gum remains one of the most frequently used polymers in fracturing fluids due to its ability to form highly viscous solutions and effectively suspend proppants. This entrenched use in energy applications, combined with high per-capita processed food consumption, sustains robust baseline demand.

From a regulatory perspective, the FDA’s GRAS listing and detailed usage limits across multiple food categories, coupled with established industry standards, provide a predictable framework for food-grade guar gum usage. In addition, North American food manufacturers are at the forefront of clean-label and plant-based innovation, increasing reliance on natural hydrocolloids like guar in dairy alternatives, meat analogues, and reduced-fat formulations. As sustainability gains importance, large ingredient companies and oil & gas operators are also examining traceability and environmental footprints in guar sourcing, further shaping supplier selection and partnership models.

Europe Guar Gum Market Trends and Insights

In Europe, guar gum demand is driven primarily by the food & beverage and personal care industries, supported by a mature regulatory environment and high safety expectations. The European Food Safety Authority (EFSA) has re-evaluated guar gum (E412) as a food additive, concluding that there is no need for a numerical acceptable daily intake while recommending stricter limits for heavy metal impurities, which has encouraged manufacturers to invest in higher-purity grades. Guar gum is widely used in products such as dairy desserts, bakery fillings, sauces, and specialty beverages across Germany, the U.K., France, and Spain.

The European Commission database and cosmetics regulations also recognize guar gum as a viscosity-controlling, film-forming, and stabilizing agent in haircare and skincare formulations, underpinning its use in shampoos, conditioners, and lotions. As European consumers increasingly favor organic, vegan, and natural cosmetics, demand for plant-derived polymers like guar gum is benefiting from this shift. Harmonized food additive rules across EU member states, along with stringent quality and sustainability requirements from retailers and brand owners, will continue to shape supplier strategies, favoring producers that can guarantee traceability and compliance with both food and cosmetic standards.

Asia Pacific Guar Gum Market Trends and Insights

Asia Pacific is the fastest-growing regional market for guar gum, driven by its dual role as both a production hub and an expanding demand center. India dominates global guar production, accounting for about 80% of output, with Rajasthan alone contributing around 72% of the country’s production. Export statistics show that India shipped over 453,000 MT of guar gum in FY 2023-24, with a significant portion destined for energy and industrial applications worldwide. At the same time, domestic consumption in India and neighboring markets is increasing in processed foods, dairy, and snack segments as urbanization and incomes rise.

In China, Japan, and key ASEAN economies, guar gum is used in food, beverages, and personal care applications, often in combination with other hydrocolloids to optimize texture and stability. Regional ingredient companies are investing in blending and application centers to support local formulation needs, while global players such as Ingredion Incorporated have expanded specialty starch and texturizing capacity in China, indirectly reinforcing broader hydrocolloid supply chains. Cost-competitive manufacturing, proximity to guar-growing regions, and rising demand for natural, plant-based stabilizers position Asia Pacific as the key growth engine for the guar gum market over the forecast period.

Competitive Landscape

The global guar gum market is moderately concentrated at the processing level, with a cluster of Indian manufacturers such as Hindustan Gum & Chemicals Ltd., Vikas WSP Ltd., Altrafine Gums, Neelkanth Polymers, and others playing a pivotal role in converting guar seed into splits and powder for export. These firms benefit from proximity to guar-growing regions and established export infrastructure, yet compete on product quality, viscosity profiles, and reliability of supply. Large multinational ingredient companies including Cargill Corporation and Ingredion Incorporated integrate guar gum into broader hydrocolloid and texturizer portfolios, leveraging application labs and technical service to differentiate. Key strategic themes include capacity optimization, vertical integration from farm to finished gum, sustainability programs, and tailored grades for high-growth segments such as pharmaceuticals, personal care, and oilfield services.

Key Developments:

- In June 2024, Altrafine Gums unveiled its Ultrapure Guar Tech series, a new line of high purity guar gum grades produced on state of the art processing lines, delivering markedly improved viscosity, stability, and emulsification for food, beverage, and personal care formulations. This launch leverages advanced infrastructure and proprietary purification methods to outperform synthetic substitutes in quality and functionality.

- In April 2022, Solvay announced that P&G Beauty joined its Sustainable Guar Initiative (SGI), launched in 2015, to scale up eco responsible guar production in Rajasthan’s Bikaner district. This partnership aims to empower women smallholder farmers through training in sustainable agronomic practices, enhance traceability of guar bean sourcing, and improve livelihoods by securing a stable, high-quality supply for natural polymers used in beauty care formulations.

Companies Covered in Guar Gum Market

- Cargill Corporation

- Ingredion Incorporated

- Altrafine Gums.

- Vikas WSP Ltd.

- Neelkanth Polymers

- Ashapura Proteins Ltd.

- Hindustan Gum & Chemicals Ltd.

- Shree Ram India Gums

- India Glycols Ltd.

- Others

Frequently Asked Questions

The global guar gum market size is projected to reach around US$ 1.6 billion in 2026.

Rising oil & gas exploration alongside growing demand for clean-label, plant-based ingredients in the food and beverage industry drives the market, supported by increased shale recovery efforts and consumer shifts toward natural and sustainable products.

North America leads the global guar gum market, driven by large‑scale oil & gas fracking activity in the U.S. and extensive use of guar as a texturizing agent in processed foods, dairy products, and beverages.

Accelerating innovation in sustainable food systems across Europe, driven by regulatory support and rising consumer demand for eco-friendly, plant-based alternatives.

Cargill Corporation, Ingredion Incorporated, Altrafine Gums, Vikas Wsp Ltd., Neelkanth Polymers, Ashapura Proteins Ltd., Hindustan Gum & Chemicals Ltd., Shree Ram India Gums, and India Glycols Ltd.