- Pharmaceuticals

- Genital Herpes Treatment Market

Genital Herpes Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Genital Herpes Treatment Market by Drug Type (Acyclovir, Valacyclovir, Famciclovir, Others), by Route of Administration (Oral, Topical, Injectable / IV), by Distribution Channel (Hospital pharmacies, Retail pharmacies, Online pharmacies), by Regional Analysis, 2026 - 2033

Genital Herpes Treatment Market Share and Trends Analysis

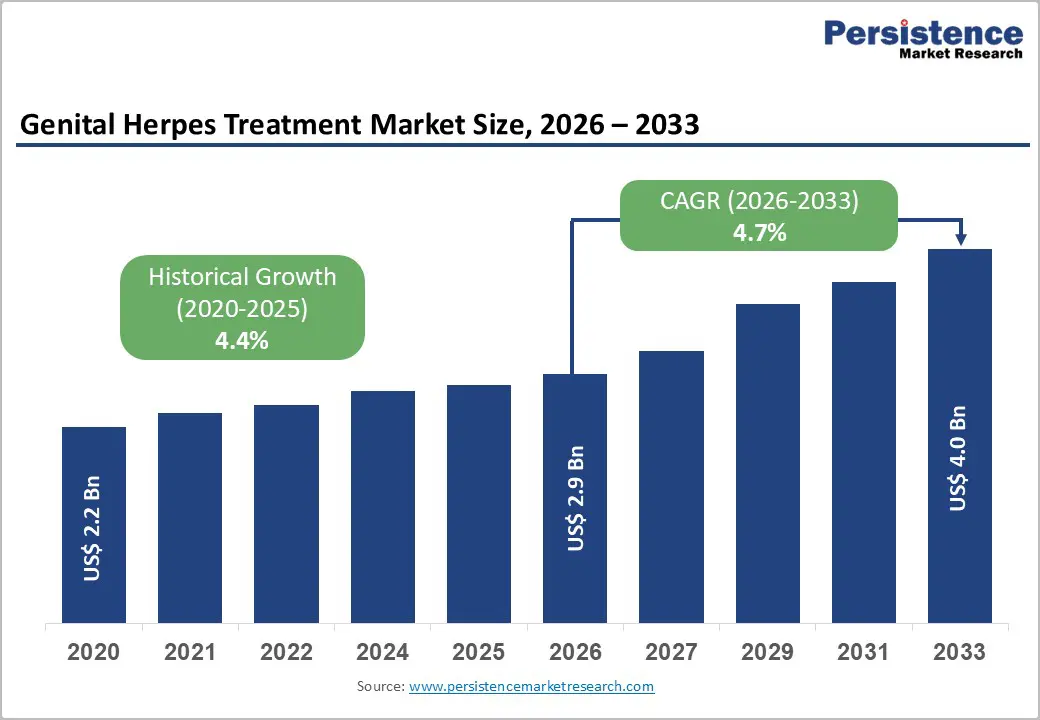

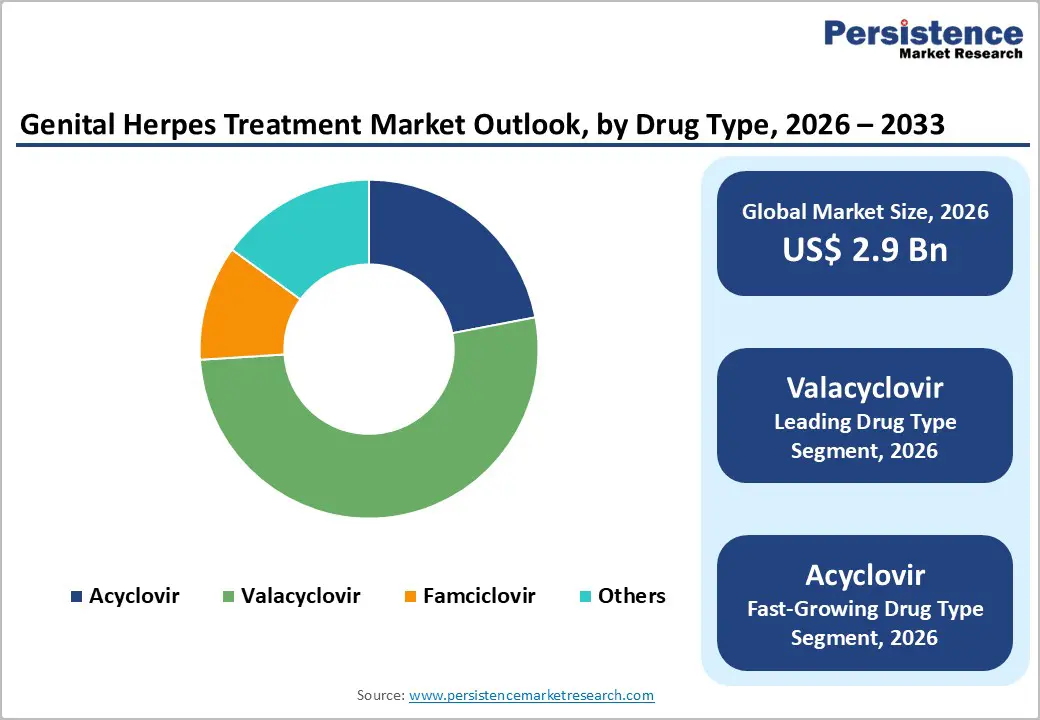

The global genital herpes treatment market size is expected to be valued at US$ 2.9 billion in 2026 and projected to reach US$ 4.0 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033. The market is experiencing robust growth driven by the escalating global prevalence of herpes simplex virus infections and enhanced diagnostic capabilities.

According to the World Health Organization (WHO), about 67% of the global population under 50 years is infected with oral or genital HSV-1. In contrast, genital HSV-2 affects hundreds of millions of adults worldwide, with a particularly high burden in low and middle-income countries. Growing public health focus on sexually transmitted infections, along with improved access to type-specific serologic tests, is bringing more patients into the formal care pathway. In parallel, the availability of effective oral antivirals and increasing use of long-term suppressive therapy to reduce recurrences and transmission are supporting steady adoption of prescription treatments.

Key Industry Highlights:

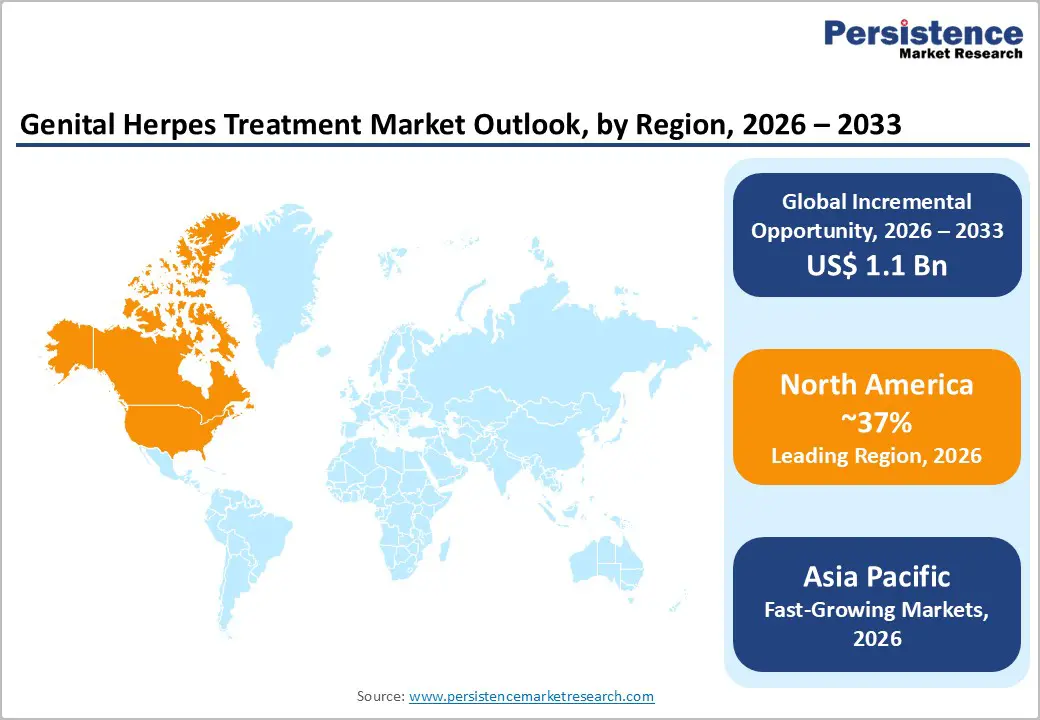

- North America is the leading regional market with about 37% share in 2025, supported by high genital herpes prevalence, strong diagnostic capacity, comprehensive insurance coverage, and broad availability of oral antivirals through mature retail and mail-order pharmacy channels across the United States and Canada.

- Asia Pacific is the fastest-growing region, driven by a large at-risk population in China, India, Japan, and ASEAN, rising STI awareness, expanding hospital and outpatient infrastructure, and strong local manufacturing bases that supply cost-effective acyclovir and valacyclovir throughout regional and export markets.

- Valacyclovir is the dominant drug type with an estimated 42% share in 2025, owing to its improved oral bioavailability versus acyclovir, convenient once or twice daily dosing for both episodic and suppressive therapy, and extensive generic availability endorsed in major European and international treatment guidelines.

- Online pharmacies represent the fastest-growing distribution channel, leveraging telemedicine, e-prescribing, and discreet home delivery; professional pharmacy organizations have documented rapid expansion of licensed internet pharmacies and emphasized regulatory frameworks to ensure safe online antiviral supply.

- Long-acting and novel-mechanism antivirals, particularly helicase-primase inhibitors and emerging HSV vaccine and immunotherapy candidates, offer a key opportunity to address adherence challenges, reduce recurrence burden, and create higher-value therapeutic niches beyond traditional nucleoside analogues over the next decade.

| Key Insights | Details |

|---|---|

| Genital Herpes Treatment Market Size (2026E) | US$ 2.9 billion |

| Market Value Forecast (2033F) | US$ 4.0 billion |

| Projected Growth CAGR (2026 - 2033) | 4.7% |

| Historical Market Growth (2020 - 2025) | 4.4% |

Market Dynamics

Drivers - Rising Global Burden of HSV Infections and Recurrent Disease

The fundamental growth driver for the genital herpes treatment market is the large and persistent burden of HSV-1 and HSV-2 infections worldwide. WHO estimates that in 2016, about 491 million people aged 15-49 years were living with HSV-2, corresponding to a global prevalence of around 13% in this age group. More recent pooled analyses suggest that both incidence and prevalence remain high, with tens of millions of new genital herpes cases occurring annually, especially in Africa and the Western Pacific. Because genital herpes is lifelong and many patients experience multiple symptomatic recurrences per year, demand for both episodic and suppressive antiviral therapy remains structurally strong. Additionally, genital HSV infection increases the risk of acquiring and transmitting HIV, which has prompted global and national programs to strengthen STI services and counseling, indirectly supporting higher diagnosis and treatment of genital herpes.

Digital Health, Telemedicine, and Growing Access Through Pharmacy Channels

Expansion of digital health and telemedicine is substantially improving access to genital herpes diagnosis, counseling, and prescription fulfillment. In high-income markets such as the United States, virtual STI clinics and teledermatology services now allow patients to receive confidential assessments and antiviral prescriptions without an in-person visit, lowering stigma-related barriers. At the same time, retail pharmacies and online pharmacies are assuming a larger role in chronic therapy dispensing; analyses of U.S. retail pharmacy trends highlight rising prescription volumes and the shift toward omnichannel models that combine in store, mail-order, and same-day delivery. Professional pharmacy bodies have also documented the rapid growth of licensed internet pharmacies and discussed good practice standards for safe online supply of prescription medicines, including antivirals. This evolution in care delivery and distribution channels makes it easier for patients with recurrent genital herpes to initiate and maintain long-term antiviral regimens, supporting sustained market growth.

Restraints - Antiviral Resistance and Limited Novel Mechanisms of Action

Although resistance to nucleoside analogues such as acyclovir remains uncommon in immunocompetent patients, studies in immunocompromised populations show clinically relevant resistance rates, particularly among individuals with advanced HIV or post-transplant immunosuppression. Resistance typically arises via mutations in the viral thymidine kinase (UL23) or DNA polymerase genes, reducing susceptibility to acyclovir, valacyclovir, and famciclovir, and necessitating use of more toxic or less convenient alternatives such as foscarnet. This phenomenon complicates management, increases healthcare costs, and underscores the need for antivirals with new mechanisms of action. However, the pipeline of late-stage small-molecule agents remains relatively limited, and the scientific and regulatory challenges of demonstrating superior long-term outcomes can slow the introduction of innovative products.

Stigma, Under-Diagnosis, and Limited Awareness in Low-Resource Settings

Social stigma around sexually transmitted infections continues to be a major barrier to care for genital herpes. Surveys in multiple regions indicate that many people with recurrent genital ulcer disease do not seek medical attention or disclose symptoms to healthcare providers, leading to under-diagnosis and under-treatment. In low- and middle-income countries, syndromic management is still common in primary care, and laboratory confirmation of HSV infection is rarely performed, which limits the use of targeted antivirals. In addition, limited public awareness that effective oral treatments can shorten outbreaks and reduce recurrences means that some patients accept recurrent symptoms as inevitable rather than pursuing long-term suppressive therapy. These behavioral and system-level factors constrain treatment volumes, especially outside high-income urban markets.

Opportunities - Next-Generation Long-Acting Antivirals and Novel Targets

One of the most promising opportunities lies in the development of long-acting antivirals that move beyond traditional nucleoside analogues and offer significantly extended dosing intervals. Helicase-primase inhibitors are a leading example: early-stage compounds targeting the HSV helicase-primase complex have shown high potency against both HSV-1 and HSV-2 in preclinical and early clinical work, with the goal of once weekly or even once monthly oral dosing. Clinical data presented at international infectious disease congresses suggest that such agents can markedly suppress viral replication and shedding, and partnerships between innovation focused biotechs and large pharmaceutical companies signal strong commercial interest in this class. If late-phase trials confirm durable suppression of recurrences with favorable safety profiles, long-acting agents would address key unmet needs around adherence, daily pill burden, and stigma associated with chronic antiviral use, creating a premium segment within the genital herpes treatment market.

Therapeutic and Prophylactic HSV Vaccines and Immunotherapies

Another major medium to long-term opportunity is the advancement of prophylactic and therapeutic HSV vaccines and immune-based therapies. WHO and other public health agencies have repeatedly highlighted the need for effective HSV vaccines, given the infection’s contribution to genital ulcer disease burden and its role as a cofactor in HIV transmission. Several academic and industry groups are testing novel vaccine platforms, including subunit, vector-based, and mRNA approaches; for example, mRNA-based genital herpes vaccine candidates have entered early-phase clinical trials to assess safety and immunogenicity in adults with recurrent disease. Although a number of candidates have failed to meet efficacy endpoints in past programs, ongoing innovation in antigen design and delivery technologies continues. Success in developing even partially protective vaccines or effective therapeutic immunotherapies would not eliminate the need for antivirals but could substantially reduce recurrence rates and transmission, opening new combination treatment paradigms and driving significant incremental demand for adjunctive therapies and prophylaxis programs.

Category-wise Analysis

Drug Type Insights

Within drug type, valacyclovir is the leading segment, accounting for about 42% of the genital herpes treatment market in 2025, as specified in the scope. Valacyclovir is a prodrug of acyclovir that offers roughly 3-5 fold higher oral bioavailability, enabling less frequent dosing while maintaining comparable antiviral efficacy against HSV-1 and HSV-2. Clinical guidelines in North America and Europe frequently recommend valacyclovir for both episodic treatment and chronic suppressive therapy because once- or twice daily regimens improve adherence compared with acyclovir’s more frequent dosing. In addition, generic valacyclovir is widely available following expiry of key patents, with multiple manufacturers such as GlaxoSmithKline plc’s original brand and generic suppliers from India, Israel, and other regions, making it cost-effective for a large patient population. The combination of strong evidence, convenient dosing, and broad reimbursement has cemented valacyclovir’s position as the dominant drug type, even as acyclovir remains important in injectable and topical forms.

Route of Administration Insights

By route of administration, oral formulations hold the largest share and can reasonably be considered the leading segment in 2025, supported by extensive clinical experience and patient preference. Oral acyclovir, valacyclovir, and famciclovir are the standard of care for both first-episode and recurrent genital herpes in major guidelines, including the 2024 European guidelines for the management of genital herpes, which emphasize oral regimens for most immunocompetent adults. Oral therapy allows self-administration at home, rapid initiation at the onset of prodromal symptoms, and straightforward use in long-term suppressive strategies, all of which contribute to higher adherence and better quality of life. In contrast, topical agents are generally reserved for localized symptom relief and have limited impact on systemic viral replication, while intravenous antivirals are used mainly for severe or disseminated disease in hospitalized or immunocompromised patients. Given these patterns, oral administration is likely to account for well over half of total treatment volumes and will remain the core modality as new oral agents are introduced.

Distribution Channel Insights

In terms of distribution channel, retail pharmacies can be identified as the leading segment by market share in 2025, reflecting their central role in dispensing chronic and acute prescriptions in both developed and many emerging markets. Analyses of the U.S. pharmacy sector show that community and chain retail pharmacies collectively handle the majority of outpatient prescriptions, and similar patterns are seen in Europe and parts of Asia, where community pharmacies are often the first point of contact for STI-related care and counseling. Retail pharmacies provide convenient access, extended opening hours, and opportunities for pharmacist-led adherence support, which are crucial for chronic suppressive antiviral regimens. At the same time, online pharmacies and mail-order services are the fastest-growing channel, benefiting from digitalization and patient desire for privacy and home delivery of sensitive medications such as genital herpes treatments. Hospital pharmacies, while essential for managing severe or complicated cases requiring inpatient care, represent a smaller share, given that most genital herpes management occurs in outpatient settings.

Regional Insights

North America Genital Herpes Treatment Market Trends and Insights

North America is the leading regional market, accounting for about 37% of global genital herpes treatment revenues in 2025, as indicated in the scope. In the United States, STI surveillance data from the Centers for Disease Control and Prevention (CDC) show millions of new STI cases each year, and genital herpes remains highly prevalent; earlier CDC estimates indicated that roughly one in 6 people aged 14-49 years have genital HSV-2 infection. The region benefits from high awareness, broad access to primary care and specialist services, and widespread availability of type-specific serologic testing, all of which support early diagnosis and long-term management.

Regulatory and reimbursement frameworks further underpin market strength. The U.S. Food and Drug Administration (FDA) has issued guidance for the development of drugs to treat recurrent herpes labialis, illustrating the agency’s structured expectations around clinical endpoints and safety monitoring that also inform genital herpes drug development. Large pharmaceutical companies such as Pfizer Inc., GlaxoSmithKline plc, and Abbott Laboratories maintain substantial antiviral portfolios and invest in lifecycle management and patient-support programs, while insurers and pharmacy benefit managers shape formulary access and generic use. Expansion of telemedicine, integration of antivirals into digital STI clinics, and growing use of mail-order and same-day pharmacy delivery are improving continuity of suppressive therapy and driving incremental prescription volumes in the region.

Asia Pacific Genital Herpes Treatment Market Trends and Insights

Asia Pacific is the fastest-growing regional market for genital herpes treatments, reflecting its large population base, rising STI burden, and expanding healthcare access. Countries such as China, India, Japan, and those in the ASEAN region are experiencing rapid urbanization and lifestyle changes that contribute to higher STI transmission, while improved diagnostic capabilities are leading to greater recognition of genital herpes as a distinct clinical entity. Market analyses of the broader herpes treatment segment in Asia Pacific indicate robust mid-single to high single-digit annual growth, with China often representing the largest share due to its sheer population size and investments in hospital and outpatient infrastructure.

Domestic pharmaceutical industries play a pivotal role. Manufacturers in India and China are major global suppliers of acyclovir, valacyclovir, and famciclovir active pharmaceutical ingredients and finished dosage forms, leveraging cost-effective production and strong export capabilities. In markets like India, the growth of organized pharmacy retail chains and e-pharmacy platforms is improving access to antivirals in both urban and semi-urban areas. Japan, with its mature healthcare system and high generic utilization, supports a stable demand for oral antivirals within a highly regulated environment. Nonetheless, significant unmet needs remain in rural and low-income populations across the region, where limited awareness, persistent stigma, and constraints on diagnostic services continue to suppress treatment rates; addressing these gaps represents a key growth frontier for the coming decade.

Competitive Landscape

The global genital herpes treatment market is moderately competitive and dominated by well-established antiviral therapies, supported by widespread generic availability and strong physician familiarity. Competition largely centers on pricing, formulation improvements, dosing convenience, and geographic reach rather than major product differentiation. Oral antivirals account for most revenues, while topical and injectable options serve niche or severe cases. Market participants are increasingly investing in life-cycle management strategies, combination approaches, and expanded access in emerging economies.

Key Developments:

- In December 2025, Gilead Sciences, Inc. and Assembly Biosciences, Inc. (Nasdaq: ASMB) announced that Gilead had exercised its combined option to exclusively license Assembly Bio’s herpes simplex virus (HSV) helicase-primase inhibitor programs, including the long-acting investigational candidates ABI-1179 and ABI-5366 for recurrent genital herpes. These became the first programs Gilead advanced under the ongoing Assembly Bio R&D collaboration, reinforcing both companies’ commitment to building a novel antiviral pipeline and driving long-term growth through innovative therapies addressing significant unmet needs.

Companies Covered in Genital Herpes Treatment Market

- GlaxoSmithKline plc.

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

- Novartis AG

- Pfizer Inc.

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy’s Laboratories Ltd.

- Cipla Limited

- Aurobindo Pharma Ltd.

- Abbott Laboratories

- Aicuris Anti-infective Cures AG

- Hikma Pharmaceuticals plc

- Assembly Biosciences

- Gilead Sciences, Inc.

- Moderna

- United BioPharma

- Maruho Co., Ltd.

Frequently Asked Questions

The global genital herpes treatment market is expected to reach about US$ 2.9 billion in 2026, supported by a large prevalent pool of HSV-1 and HSV-2 infections worldwide and steady uptake of oral antivirals for episodic and suppressive therapy in both high- and middle-income regions.

A primary demand driver is the high and ongoing incidence of genital herpes, with hundreds of millions of adults living with HSV-2 and substantial numbers experiencing recurrent symptomatic episodes each year, which necessitate repeated courses or continuous suppressive antiviral therapy for symptom control and transmission risk reduction.

North America is the leading regional market, anchored by the United States, where robust STI surveillance, broad access to diagnostic services, comprehensive insurance coverage, and strong presence of major antiviral manufacturers underpin high treatment rates for genital herpes.

Development of long-acting antivirals and novel-mechanism agents, such as helicase-primase inhibitors and therapeutic or prophylactic HSV vaccines, offers a major opportunity to improve adherence, reduce recurrence burden, and create differentiated premium therapies beyond traditional nucleoside analogues.

Key companies include GlaxoSmithKline plc, Teva Pharmaceutical Industries Ltd., Viatris Inc., Novartis AG, Pfizer Inc., Sun Pharmaceutical Industries Ltd., Dr. Reddy’s Laboratories Ltd., Cipla Limited, Aurobindo Pharma Ltd., Abbott Laboratories, Aicuris Anti-infective Cures AG, and Hikma Pharmaceuticals plc, along with innovators such as Assembly Biosciences, Gilead Sciences, Inc., and Moderna working on next-generation antivirals and vaccine candidates.