- Pharmaceuticals

- Generic Oncology Drugs Market

Generic Oncology Drugs Market Size, Share, and Growth Forecast, 2025 - 2032

Generic Oncology Drugs Market By Molecule (Large Molecule, Small Molecule), Route of Administration (Oral, Parenteral), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis for 2025 - 2032

Generic Oncology Drugs Market Size and Trends Analysis

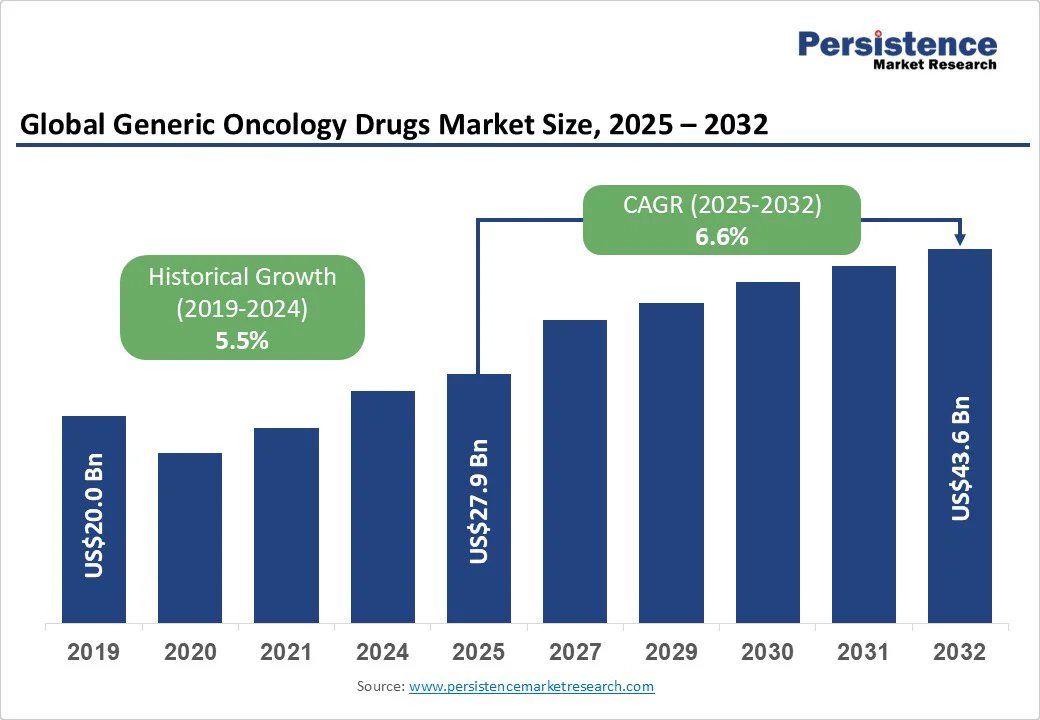

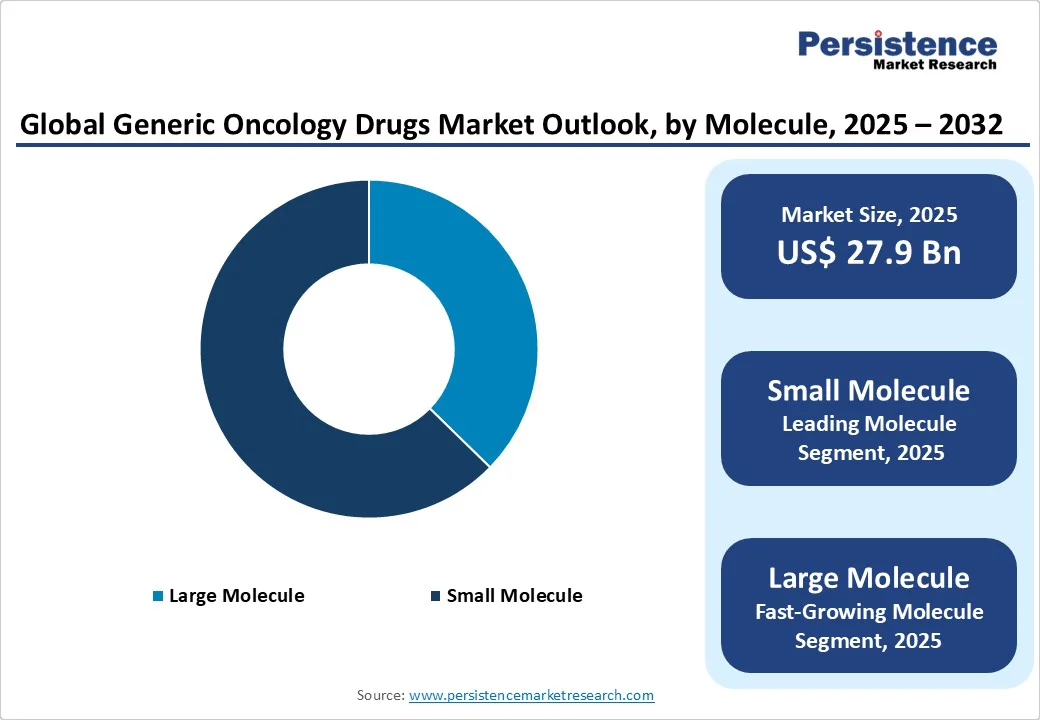

The global generic oncology drugs market size is likely to be valued at US$27.9 Bn in 2025 and is expected to reach US$43.6 Bn by 2032, growing at a CAGR of 6.6% during the forecast period from 2025 to 2032, driven by the growing demand for generic oncology drugs that offer patients affordable alternatives to high-cost branded therapies. As patents for numerous blockbuster drugs expire, generic manufacturers are seizing the opportunity to enter the market with effective and accessible options.

Key Industry Highlights

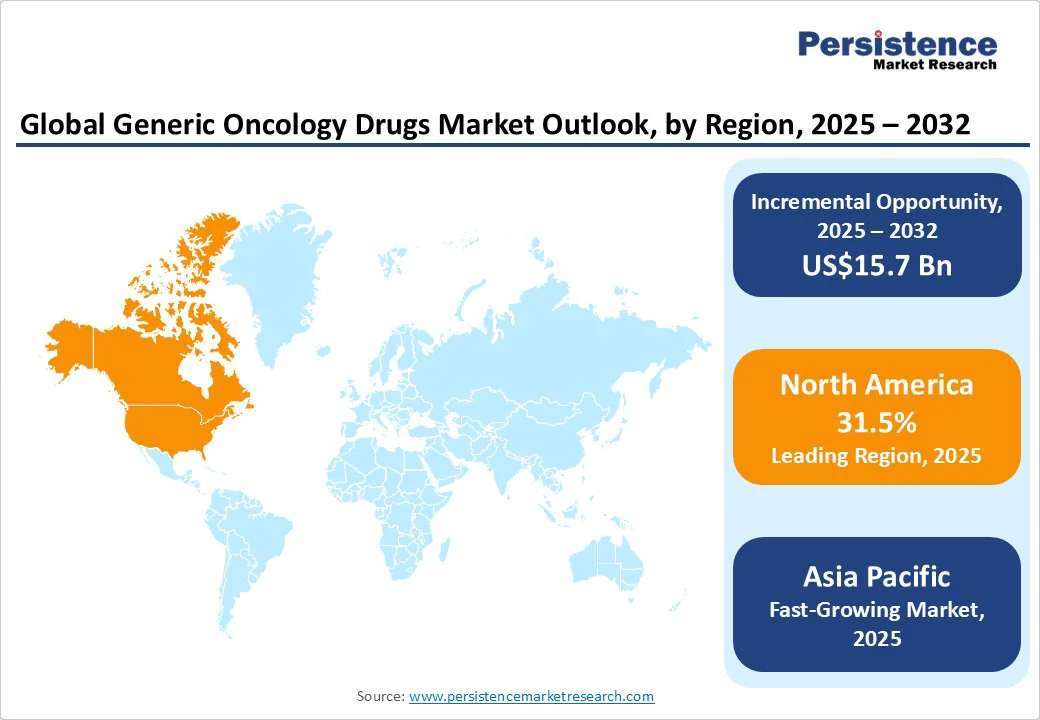

- Leading Region: North America is expected to hold a leading market share of around 31.5% in 2025, driven by the rising incidence of cancer and the growing demand for effective and affordable treatment options, which is boosting the adoption of generic oncology drugs.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by a high cancer burden that underscores the need for affordable treatment options, thereby increasing demand for generic oncology therapies.

- Dominant Molecule Type: The small molecule segment is projected to dominate the market, accounting for a 62.7% share in 2025, driven by its simpler manufacturing and distribution processes, which enhance accessibility for both patients and healthcare providers.

- Leading Distribution Channel: The hospital pharmacies segment is expected to dominate the market with a 52.3% market share, driven by the rising incidence of cancer cases that require specialized treatment, prompting hospitals to expand their pharmacy services.

- Leading Route of Administration: The parenteral route of administration is leading with a market share of 56.3% in 2025, due to its superior efficacy in delivering cancer therapies directly into the bloodstream.

| Key Insights | Details |

|---|---|

|

Generic Oncology Drugs Market Size (2025E) |

US$27.9 Bn |

|

Market Value Forecast (2032F) |

US$43.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Insurance Coverage for Generic Oncology Drugs

Expanded insurance coverage for generic oncology drugs greatly improves patient access to affordable cancer treatments. As more insurance plans include generics in their formularies, patients are encouraged to choose these cost-effective alternatives, reducing out-of-pocket expenses. This shift not only alleviates the financial burden on individuals but also promotes adherence to treatment regimens, improving health outcomes.

Insurers benefit from lower overall healthcare costs, as generics typically provide the same efficacy and safety as branded medications. As demand for affordable cancer care increases, expanded insurance coverage for generics becomes a crucial factor in promoting equitable access to essential oncology therapies.

Rising Cancer Incidence Fueling Demand for Generic Drugs

The growing incidence of cancer globally is significantly driving the market for cost-effective and affordable generic drugs. According to the American Cancer Society 2024 statistics, there were around 20 million new cancer cases in 2022, with nearly 9.7 million cancer deaths globally, breast, lung, colorectal, prostate, and stomach cancers being the most diagnosed ones.

The rising burden of cancer is intensified by an aging population, lifestyle choices, and environmental factors, leading to greater demand for cancer treatments. In such scenarios, generic oncology drugs are crucial for ensuring that patients receive timely and appropriate care. Additionally, as healthcare systems worldwide focus on cost containment and improving patient access, the importance of generics becomes increasingly prominent.

Regulatory Delays for Bioequivalence Approvals to Hinder Market Growth

Oncology drugs often contain high-potency active pharmaceutical ingredients (HPAPIs) and, therefore, require a detailed bioequivalence study, precise dosage adjustments, and compliance with toxicity profiles. Bioequivalence (BE) testing is crucial for ensuring that generic oncology drugs possess the same safety, efficacy, and pharmacokinetic properties as their branded counterparts.

Meeting the strict standards of regulatory bodies such as the U.S. FDA and EMA is complex and can delay product launches. Additionally, regulatory authorities frequently update their BE guidelines to align with evolving scientific knowledge and pharmacovigilance requirements, which can complicate the process, especially for advanced drug delivery systems. Such evolving requirements can force manufacturers to redesign clinical trials mid-process, adding both time and cost burdens.

Growing Acceptance of Biosimilars in Cancer Care Creates New Opportunities

The acceptance of biosimilar oncology drugs is growing significantly worldwide, presenting a substantial opportunity for generic manufacturers. Biologics, particularly monoclonal antibodies such as Rituxan, Avastin, and Herceptin, play a critical role in cancer treatment; however, the high costs associated with these drugs might strain the healthcare systems.

With patents on these biologics nearing expiration, biosimilars are expected to gain significant momentum, as they offer cost-effective alternatives with a similar safety profile and efficacy. Countries such as India, Brazil, and China are rapidly adopting biosimilars to address the affordability of cancer care.

In Europe, biosimilars have already significantly reduced oncology expenses, while U.S. regulatory incentives are facilitating faster approvals, enhancing access in low- and middle-income regions. Increased insurance coverage and a shift toward value-based care further support the transition to these affordable options.

Capitalizing on Patent Loss in Oncology Drugs to Drive Growth

The generic oncology drugs market is poised for significant growth as patents for numerous high-cost cancer treatments are set to expire. This shift opens the door for generic manufacturers to introduce affordable alternatives, addressing the increasing demand for accessible cancer therapies worldwide. Key drugs, including Imbruvica and Revlimid, have already transitioned to generic alternatives, resulting in price reductions and enhanced patient access.

In February 2022, Sandoz Group AG, headquartered in Switzerland, launched a generic version of Revlimid (lenalidomide) in 19 European countries.

In March 2022, Israel-based Teva Pharmaceuticals launched the first generic version of REVLIMID® (lenalidomide) in the U.S., with dosages available at 5mg, 10mg, 15mg, and 25mg capsules.

In 2023, Teva and NATCO announced the launch of additional strengths for the generic version of Revlimid®1 (lenalidomide capsules), in 2.5 mg and 20 mg strengths, in the U.S.

The rise of biosimilars, particularly in regions such as Southeast Asia, Latin America, and Africa, further enhances market opportunities. As governments and healthcare providers seek cost-effective solutions, generic oncology drugs are poised to play a crucial role in enhancing healthcare affordability while maintaining treatment quality.

Category-wise Analysis

Molecule Insights

The small molecule segment is expected to lead the market with a 62.7% market share in 2025, driven by its ease of manufacturing and distribution, which makes it more readily available to healthcare providers and patients. Their established efficacy and well-understood mechanisms of action also contribute to their popularity in oncology. The increasing focus on cost containment in healthcare is encouraging the use of small-molecule drugs, as they often present a more budget-friendly option compared to larger biologics and biosimilars.

Route of Administration Insights

The parenteral route of administration is expected to lead the market with a 56.3% market share in 2025, owing to its high efficacy in delivering cancer treatments directly into the bloodstream, ensuring faster onset of action and improved bioavailability compared to oral formulations. Many oncology drugs, especially chemotherapy agents and biologics, are unstable or poorly absorbed through the gastrointestinal tract, making parenteral administration the preferred option. Additionally, hospitals and oncology centers rely heavily on injectable generics for precision dosing and controlled treatment, reinforcing the segment’s dominance.

Distribution Channel Insights

The hospital pharmacies segment is projected to hold the largest market share, at 52.3%, driven by the increasing number of cancer cases requiring specialized care, which leads hospitals to enhance their pharmacy services. The segment is projected to exhibit a CAGR of 6.0% during the period from 2025 to 2032.

Hospital pharmacies play a crucial role in providing patients with immediate access to generic oncology drugs, ensuring they receive timely and effective treatment. Additionally, the rise of personalized medicine and the growing focus on integrated healthcare services within hospitals are further driving demand. As hospitals enhance their capabilities to manage complex cancer therapies, the reliance on hospital pharmacies is expected to strengthen significantly.

Regional Insights

North America Generic Oncology Drugs Market Trends

North America is projected to hold a leading market share of approximately 31.5% in 2025, driven by the rising incidence of cancer and increasing demand for effective, affordable treatment options, contributing to the growing adoption of generic oncology drugs. The U.S. is anticipated to record a considerable CAGR of 6.1% through 2032. The rising incidence of cancer drives the demand for effective treatment options, leading to increased utilization of generic oncology drugs. Additionally, growing consumer awareness of the benefits of generics, coupled with the emphasis on cost-effectiveness in healthcare, supports this trend.

According to the 2022 report by the American Association of Accessible Medicine, 91% of prescriptions dispensed in the U.S. are generic and biosimilars, due to their low cost and high value to patients. The generic drugs sector accounts for nearly 3% of the total U.S. healthcare spending.

Leading pharmaceutical companies are also expanding their portfolios to include a wider range of generic therapies, fostering competition and innovation. Also, supportive regulatory policies are enhancing market accessibility, further propelling growth in this segment.

Europe Generic Oncology Drugs Market Trends

Europe is projected to capture a significant 28.1% revenue share in 2025, highlighting its strong position within the global landscape. This dominance is driven by the high prevalence of cancer across the region, coupled with the increasing adoption of cost-effective generics as healthcare systems face mounting financial pressures.

Supportive government policies promoting generic substitution, along with the patent expiry of several blockbuster oncology drugs, further accelerate market growth. Additionally, the presence of advanced healthcare infrastructure, widespread hospital networks, and a strong focus on affordable patient access ensure sustained demand for generic oncology drugs across key European countries.

Asia Pacific Generic Oncology Drugs Market Trends

Asia Pacific is the fastest-growing region, driven by a high cancer burden that underscores the need for affordable treatment options, thereby increasing demand for generic oncology therapies. In the Asia Pacific, market growth is estimated to rise, with India set to exhibit a CAGR of around 7.5% through 2032. The country's high cancer burden necessitates affordable treatment options, fueling demand for generic therapies. India’s pharmaceutical sector is characterized by a strong emphasis on research and development, enabling the introduction of a diverse range of oncology drugs.

Supportive government policies and initiatives aimed at enhancing healthcare infrastructure and access to medications are significant contributors to this improvement. Growing patient awareness about the effectiveness of generic drugs further supports market expansion in the region.

Competitive Landscape

The global generic oncology drugs market is characterized by a mix of established leaders and smaller, local players. Leading companies with significant presence globally leverage their resources and expertise to shape market trends and drive innovation. Domestic firms contribute to the industry's dynamism by focusing on developing cost-effective formulations to meet local healthcare needs as well as improve access to cancer treatments, introducing products and specialized services that address specific regional needs. As various branded drugs and biologics approach patent expiry, the market is set to provide significant opportunities for the generic manufacturers to develop biosimilars and other generics that uphold quality and efficacy.

Key Industry Developments

- In July 2025, Zydus Lifesciences received the U.S. FDA's tentative approval for its generic versions of ibrutinib (Imbruvica) tablets in 140 mg, 280 mg, and 420 mg strengths, for patients with chronic lymphocytic leukemia (CLL)/small lymphocytic lymphoma (SLL) with 17p deletion and Waldenström macroglobulinemia (WM), where ibrutinib plays a pivotal role.

- In January 2025, Lupin received U.S. FDA approval for its abbreviated new drug application for Lenalidomide Capsules, bioequivalent to Bristol-Myers Squibb Company’s Revlimid capsules, in different strengths, for the treatment of multiple myeloma.

- In October 2024, Sandoz launched the first FDA-approved generic version of paclitaxel—a lyophilized powder for injection in the U.S., following its approval on October 8, 2024.

- In July 2024, Apotex Inc., a Canada-based company, entered into an exclusive agreement with Coherus Biosciences, Inc. to license the Canadian rights to toripalimab, an anti-PD-1 monoclonal antibody, marking a major expansion of its oncology franchise with its first novel biologic, pending regulatory approval.

Market Growth Drivers

By Molecule

- Large Molecule

- Small Molecule

By Route of Administration

- Oral

- Parenteral

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Region

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

Companies Covered in Generic Oncology Drugs Market

- Teva Pharmaceutical Industries Ltd.

- Fresenius Kabi AG

- Mylan N.V. (Viatris)

- Sandoz Group AG

- Biocon

- Pfizer Inc.

- Apotex Inc.

- Zydus Cadila

- Hikma Pharmaceuticals

- Sun Pharmaceutical Industries Ltd.

- Cipla Limited

- Lupin Pharmaceuticals

Frequently Asked Questions

The generic oncology drugs market is projected to be valued at US$27.9 Bn in 2025.

Rising cancer prevalence and cost pressures on healthcare systems drive the generic oncology drugs market.

The generic oncology drugs market is poised to witness a CAGR of 6.6% between 2025 and 2032.

Patent expiries of blockbuster oncology drugs and increasing adoption of affordable generics present key market opportunities.

Major players in the generic oncology drugs market include Teva Pharmaceutical Industries Ltd., Fresenius Kabi AG, Mylan N.V. (Viatris), Sandoz Group AG, Biocon, and Pfizer Inc.