- Metals & Minerals

- Flake Graphite Market

Flake Graphite Market Size, Share, and Growth Forecast, 2026 - 2033

Flake Graphite Market by Product Type (Natural Flake Graphite, Synthetic Flake Graphite), Purity Level (High Purity, Medium Purity, Low Purity), Application (Energy Storage, Automotive, Industrial, Aerospace, Others), and Regional Analysis for 2026 - 2033

Flake Graphite Market Share and Trends Analysis

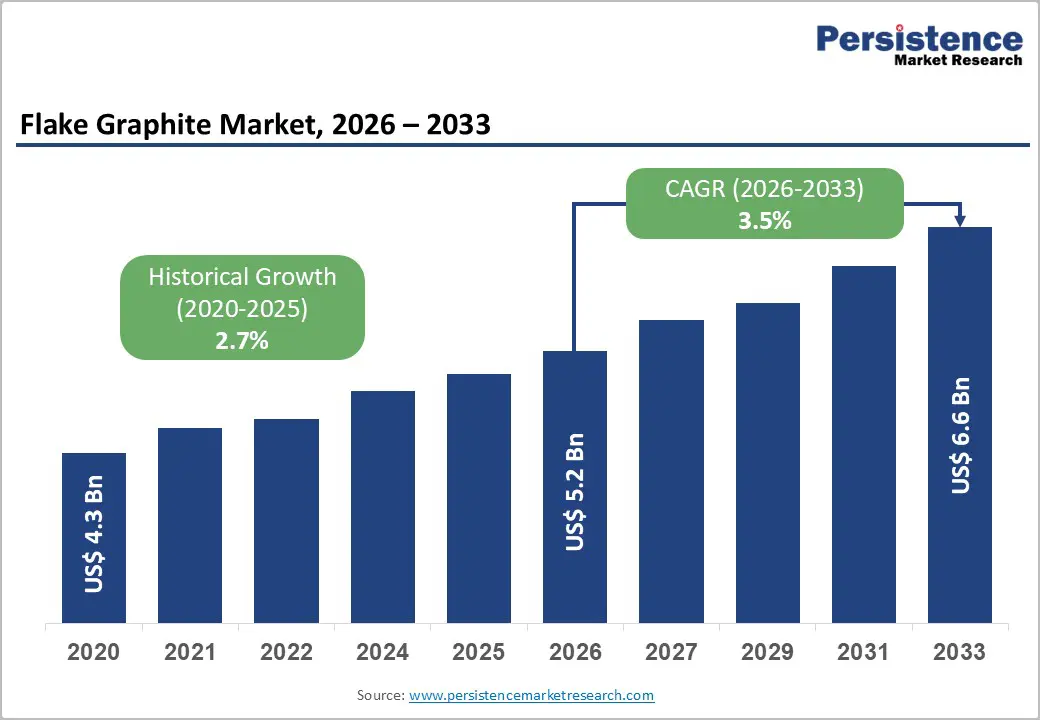

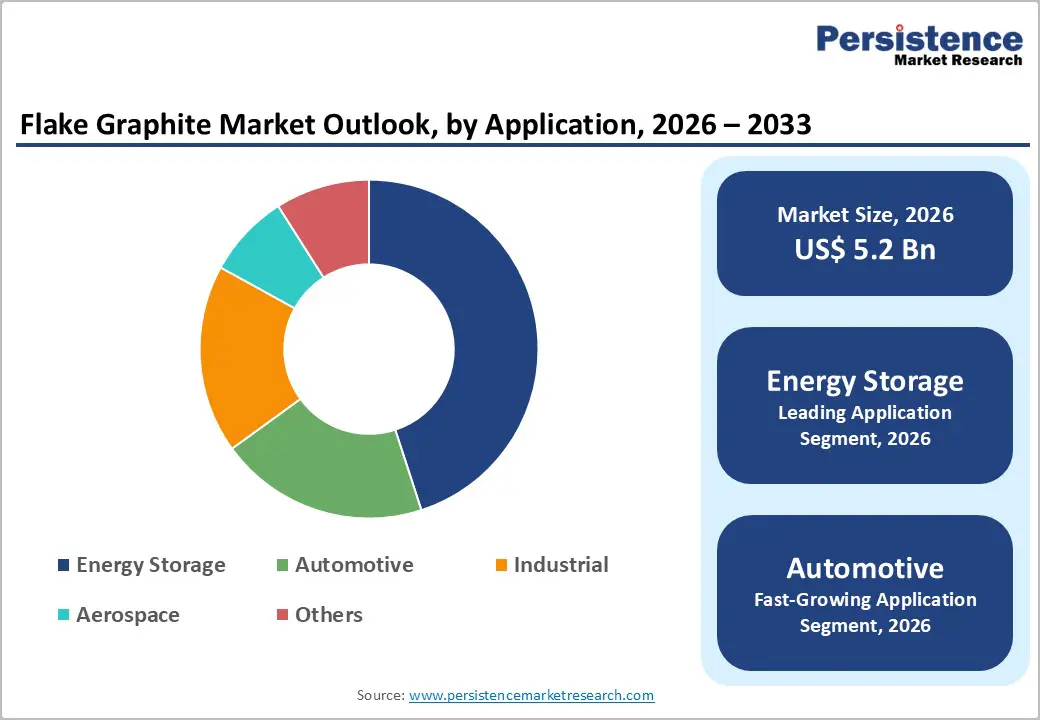

The global flake graphite market size is likely to be valued at US$ 5.2 billion in 2026, and is projected to reach US$ 6.6 billion by 2033, growing at a CAGR of 3.5% during the forecast period 2026−2033. Growth is primarily driven by the rising demand for high-performance energy storage solutions, which require high-quality graphite materials for battery anodes. Increasing adoption in automotive and industrial sectors reinforces the need for efficient conductive materials.

Technological advancements in graphite processing and purification enhance product consistency, supporting industrial scalability. Expansion of manufacturing infrastructure in emerging economies improves accessibility and reduces supply chain constraints. Regulatory frameworks that support sustainable mining practices and low-emission materials incentivize investment in graphite production. The integration of graphite into high-tech applications, such as aerospace composites, demonstrates the material's versatility, thereby contributing to its adoption.

Key Industry Highlights

- Application Leadership: Energy storage is positioned as the leading segment with about 45% revenue share in 2026, supported by lithium-ion battery integration, high conductivity, and thermal stability.

- Fastest-growing Application: Automotive applications are expected to be the fastest-growing between 2026 and 2033, driven by soaring electric vehicle (EV) adoption.

- Regional Dominance: Asia Pacific is slated to dominate with over 50% market share in 2026, driven by the large presence of mining reserves and manufacturing hubs.

- Fastest-growing Market: North America is forecasted to be the fastest-growing market through 2033, stimulated by EV growth, energy storage, and high-purity graphite demand.

| Key Insights | Details |

|---|---|

|

Flake Graphite Market Size (2026E) |

US$ 5.2 Bn |

|

Market Value Forecast (2033F) |

US$ 6.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Escalating Demand for Energy Storage Solutions

Energy storage systems (ESS) are integral to modern electricity infrastructure as they address core grid challenges identified by the U.S. Department of Energy (DOE), including balancing supply with demand, enhancing reliability, and enabling higher penetration of variable generation sources such as wind and solar. Storage technologies buffer excess generation during low demand and discharge during peak demand, reducing stress on transmission assets and lowering overall operational costs for utilities and consumers. Storage also mitigates frequency and voltage fluctuations, supports ancillary services that keep grids stable, and helps avoid costly infrastructure upgrades by deferring investment in new generation or transmission capacity.

Energy system transformation is reflected in recent deployment trends, with U.S. installations surpassing historic levels in 2025 as operators and states seek flexibility and resilience for a demand profile shaped by data centers, electrification, and renewable growth. According to recent industry data, the United States added a record 57.6 gigawatt-hours (GWh) of new energy storage capacity in 2025, up 30% from the previous year and four times the level of three years prior. This expansion indicates the strategic role of storage in accommodating intermittent renewables, managing peak loads, and stabilizing grids facing increasing load volatility, driving sustained requirements for enabling materials and technologies.

Industrial and Automotive Integration

Integration of flake graphite in the industrial and automotive sectors drives market expansion by enhancing material performance and operational efficiency. Flake graphite exhibits superior thermal conductivity, chemical stability, and lubricity, which are critical for high-performance applications in manufacturing and automotive components. In industrial machinery, the material contributes to wear-resistant parts, high-temperature seals, and advanced lubricants, ensuring prolonged equipment life and minimizing maintenance downtime. Automotive applications leverage flake graphite in EV batteries, brake systems, and lightweight composite materials, supporting improved energy density, thermal management, and fuel efficiency.

The rising adoption of electric mobility and automation is intensifying demand for high-purity graphite solutions. Flake graphite enables efficient energy storage in lithium-ion batteries, directly influencing EV range and charging performance. Production processes integrating flake graphite enable manufacturers to achieve precise thermal regulation, reduced friction, and mechanical reliability, enhancing overall product quality and system durability. In automated industrial environments, consistent material performance supports robotics, additive manufacturing, and precision tooling, contributing to operational consistency and reduced failure rates.

Geopolitical supply concentration risks

Concentration of supply in a limited number of countries creates acute strategic vulnerabilities for end-users and producers. When a single country or a small group of suppliers dominates extraction and processing, political shifts, trade restrictions, or export policy changes can quickly tighten availability, force sudden price escalations, and erode negotiating leverage for downstream industries such as battery manufacturers and automotive original equipment manufacturers (OEMs). Buyers outside dominant supply regions face longer lead times and elevated inventory financing costs, compelling investment in costly strategic stockpiles or contingent supplier relationships to safeguard operations.

Fiscal policies and trade actions driven by geopolitical considerations can materially disrupt planned production and investment decisions across supply chains. Policymakers may impose export permits or tariffs to protect domestic interests or respond to foreign trade barriers, altering global flows and increasing uncertainty for international stakeholders. Infrastructure for refining, purification, and conversion into value-added forms is similarly concentrated, meaning disruptions in logistics or regulatory environments can cascade into shortages of critical intermediate and finished products.

High Processing Costs for Battery-Grade Material

High costs associated with producing battery-grade material stem from the extensive capital and operational inputs required to reach extremely high purity levels demanded by lithium-ion batteries, a necessity highlighted in U.S. government documentation showing natural graphite must be purified to at least 99.95% carbon content for battery use, which involves energy-intensive refining and precise processing steps. Purification and shaping processes involve conditioning, flotation, chemical or thermal treatments, and coating to create spherical graphite that meets electrical performance specifications; each stage raises energy and chemical costs. Environmental and occupational health regulations in many jurisdictions increase compliance expenditures for waste handling and emissions control, and limited economies of scale outside established hubs keep per-unit costs elevated.

Supply concentration also leads to trade policies or tariffs that can indirectly raise landed costs for raw and processed material inputs. Such structural cost drivers hinder competitive supply chain development in regions with smaller existing refining footprints, as the ramp-up of new facilities requires significant upfront investment and time to qualify products to technical standards. Long qualification cycles of up to several years for battery manufacturers to adopt new sources delay revenue realization and discourage investment absent policy support or incentives.

Technological Convergence in High-Performance Application

Convergence of multiple advanced technologies into high-performance application platforms is creating a significant strategic advantage for the graphite industry. Demand for material that supports enhanced electrical conductivity, thermal stability, and lightweight performance in next-generation energy and electronics solutions is reshaping investment priorities. Integrating innovations in materials processing, digital manufacturing, and energy-dense designs allows producers and users to meet stringent performance thresholds in sectors such as electrification, aerospace, and industrial systems.

Investments in novel synthesis pathways, digital optimization of production, and end-use integration strategies are enabling cross-sector benefits that amplify material utility. For instance, combining refined processing techniques with computational design tools enhances purity and structural consistency, enabling broader adoption in applications where mechanical and electrochemical performance directly impacts product lifecycle and competitiveness. Close alignment between material capabilities and application demands reduces technical barriers for product developers and end users seeking performance gains in electric mobility infrastructures, grid storage systems, and high-speed computing hardware.

Advancements in Renewable Energy Storage Integration

Integration of energy storage with renewable power sources enables a continuous and reliable electricity supply, addressing variability in solar and wind generation. Storage systems allow excess energy produced during periods of high renewable output to be retained and dispatched during peak demand or low generation periods. This capability improves grid stability, enhances operational efficiency, and supports the adoption of decentralized energy systems. Government programs emphasize advanced storage deployment to optimize transmission and distribution performance, enhance resilience, and enable strategic energy planning aligned with sustainable targets.

Deployment of high-performance storage materials improves the performance of lithium-ion and alternative battery technologies critical for long-duration applications. Stored energy supports ancillary services such as frequency regulation and congestion relief, creating value beyond simple energy shifting. Industrial and utility-scale integration of storage strengthens asset utilization, reduces operational constraints, and unlocks potential for higher renewable penetration across transmission networks. Policy support and infrastructure investment reinforce economic and operational incentives for storage adoption, shaping strategic priorities for technology suppliers and system operators in energy transition initiatives.

Category-wise Analysis

Product Type Insights

Natural flake graphite is likely to be the leading segment with an estimated 65% revenue share in 2026, due to extensive availability and suitability for energy storage, industrial, and automotive applications. Its high electrical conductivity and mechanical stability make it an ideal candidate for incorporation into lithium-ion battery anodes, improving charge efficiency and cycle life. Industrial applications benefit from its thermal stability and strength, allowing use in refractories, lubricants, and conductive composites. Manufacturers value natural graphite for its consistent quality, predictable performance, and established extraction and processing methods. Established global supply chains in major producing regions ensure reliable access, reducing operational risk for large-scale production.

Synthetic flake graphite is expected to witness the fastest growth between 2026 and 2033, as technological innovations improve product uniformity and high-temperature performance. Controlled production processes allow tuning of particle size, purity, and surface characteristics, meeting stringent specifications in aerospace, electronics, and specialty chemical industries. Its compatibility with high-performance composites, coatings, and conductive materials drives adoption in emerging industrial and energy applications. Manufacturers leverage synthetic graphite to achieve reproducible material properties, reduce impurity levels, and enable novel designs, supporting integration into advanced technologies. Customization potential positions synthetic graphite as a strategic material for high-value, specialized markets.

Application Insights

Energy storage is poised to command nearly 45% of the flake graphite market revenue share in 2026, supported by integration into lithium-ion battery anodes for automotive and renewable energy storage systems. Its high electrical conductivity and structural stability enable efficient charge-discharge cycles, extending battery lifespan and improving energy density. Thermal stability ensures safety under high-load operations, making it suitable for grid-scale and transportation applications. Regulatory policies promoting carbon reduction and clean energy adoption incentivize deployment, while long-standing relationships between suppliers and manufacturers reinforce procurement reliability. Advanced processing techniques further optimize particle morphology and purity, strengthening industrial preference and supporting large-scale adoption.

Automotive is expected to be the fastest-growing segment between 2026 and 2033, driven by the proliferation of electric vehicles and demand for lightweight, high-performance composites. Graphite enhances battery anode efficiency, reduces friction in lubrication systems, and improves thermal management in braking and drivetrain components. Integration of digital manufacturing technologies and robotics enables precise material placement and design optimization, improving overall vehicle performance and reliability. Adoption of advanced composites containing graphite supports weight-reduction targets while maintaining strength and durability, thereby increasing manufacturer preference. Strategic material development aligns with evolving vehicle electrification trends, stimulating sustained growth in automotive applications.

Regional Insights

North America Flake Graphite Market Trends

North America is forecasted to be the fastest-growing market for flake graphite between 2026 and 2033, stimulated by rapid expansion of electric vehicle production and large-scale energy storage deployment. Rising demand for high-purity graphite in lithium-ion battery anodes positions the market to benefit from strategic investment in domestic battery manufacturing and advanced material processing. Advanced production facilities enable precise control over particle size, conductivity, and thermal stability, meeting stringent performance requirements for transportation, aerospace, and grid storage applications. Policy incentives targeting low-emission technologies and domestic supply chain development encourage adoption, while industrial integration with high-performance composites, coatings, and specialty applications enhances material utilization across multiple sectors.

Technological innovation and supply chain localization support accelerated market expansion. Synthetic graphite production allows customization for high-temperature performance, particle morphology optimization, and uniform purity, supporting specialized industrial applications. Collaboration among battery manufacturers, automotive producers, and material suppliers reduces operational risk and enables rapid scaling of advanced graphite solutions. Deployment of grid-scale energy storage projects drives demand for materials capable of long-duration cycling, thermal stability, and high conductivity. Focused research and development improves integration into next-generation batteries and high-performance composites.

Europe Flake Graphite Market Trends

Europe maintains steady positioning through advanced manufacturing and sustainability focus. Growth is supported by integration of graphite into lithium-ion battery anodes for renewable energy storage and electric transportation systems, enabling energy transition initiatives. Industrial sectors utilize high-performance composites, thermal management solutions, and specialty coatings, improving operational efficiency and product reliability. Well-established infrastructure for mining, processing, and material distribution ensures consistent supply, allowing manufacturers to meet rigorous quality and performance standards. Research and development efforts focus on enhancing particle purity, conductivity, and thermal stability, facilitating adoption in aerospace, electronics, and energy storage applications. Policy frameworks incentivizing low-emission technologies further reinforce material utilization across transportation, energy, and manufacturing segments.

Technological capability and industrial collaboration strengthen market position. Production facilities enable precise control over particle morphology, surface treatment, and structural integrity, supporting integration into advanced composites, battery anodes, and high-performance coatings. Strategic partnerships between suppliers and manufacturers optimize supply chain efficiency, reduce operational risk, and allow scalable deployment for energy storage and transportation projects. Rising demand for renewable energy storage solutions, lightweight transportation materials, and thermal management components drives material consumption. Development of next-generation battery technologies and high-conductivity industrial applications further expands adoption potential.

Asia Pacific Flake Graphite Market Trends

Asia Pacific is expected to lead with an estimated over 50% of the flake graphite market share in 2026, supported by extensive mining reserves and proximity to major manufacturing hubs that facilitate large-scale production and efficient distribution. High-purity graphite availability allows integration into lithium-ion battery anodes, industrial composites, and electronic components with reduced processing cost and improved supply reliability. Well-established infrastructure for refinement, quality control, and logistics ensures consistent material delivery to energy storage, automotive, and industrial sectors. Industrial policies promoting clean energy adoption and electrification further reinforce material demand, driving sustained market dominance across high-value applications.

Technological expertise in the processing of synthetic and natural graphite strengthens competitive advantage. Advanced facilities enable tailoring of particle size, purity, and structural properties to meet stringent requirements in energy storage, high-performance composites, and thermal management applications. Strategic collaborations between mining, processing, and manufacturing entities optimize supply chains, reduce operational risks, and improve scalability. Investment in research and development fosters innovation in material integration, coatings, and high-performance composites, expanding application potential.

Competitive Landscape

The global flake graphite market structure is moderately fragmented, with leading players holding approximately 40% market share. Companies such as Syrah Resources Limited, Imerys, Asbury Advanced Materials, Focus Graphite, Tirupati Carbons & Chemicals, and Mason Resources operate across natural and synthetic production, targeting high-purity applications in energy storage, automotive, and industrial sectors. Emphasis on consistent material quality, thermal stability, and electrical conductivity allows suppliers to meet stringent performance requirements for lithium-ion battery anodes, high-performance composites, and specialty coatings. Integration of advanced processing technologies and quality assurance protocols ensures reliability and repeatability, supporting adoption in high-value applications where material performance directly impacts operational efficiency and product longevity.

Competitive positioning in the market relies on technological expertise, strategic global distribution networks, and adherence to regulatory standards. Leading players invest in research and development to enhance particle morphology, purity levels, and structural integrity, enabling customization for specific industrial, energy, and aerospace applications. Well-established supply chains and regional production facilities allow efficient material delivery while mitigating operational risk, supporting both domestic and international demand. Collaboration with battery manufacturers, automotive producers, and industrial fabricators strengthens market presence, allowing players to capture high-growth opportunities in emerging applications.

Key Industry Developments

- In March 2026, Northern Graphite partnered with Metalshub to digitalize its graphite sales by running online auctions for flake graphite from its Lac des Iles mine in Quebec, aiming to improve market transparency and enable competitive price discovery through structured digital bidding.

- In January 2026, Titan Mining Corporation initiated production of natural flake graphite concentrate at its Kilbourne demonstration facility as part of a “Made-in-America” strategy to secure critical mineral supply chains for domestic battery, defense, and industrial use.

- In October 2025, Nouveau Monde Graphite Inc. and Traxys North America LLC finalized a binding offtake and marketing agreement for 20,000 tons per annum of natural flake graphite concentrate from NMG’s Phase-2 Matawinie Mine, targeting refractory applications in western supply chains.

Companies Covered in Flake Graphite Market

- Syrah Resources Limited

- Imerys

- Asbury Advanced Materials.

- Focus Graphite

- Tirupati Carbons & Chemicals Pvt Ltd

- Mason Resources Inc.

- Graphit Kropfmühl GmbH

- SGL Carbon

- Northern Graphite

- Mersen

- Imerys S.A.

Frequently Asked Questions

The global flake graphite market is projected to reach US$ 5.2 billion in 2026.

Massive demand for lithium-ion batteries, energy storage, industrial applications, and surging electric vehicle adoption are driving the market.

The market is poised to witness a CAGR of 3.5% from 2026 to 2033.

Integration into renewable energy storage, electric vehicles, high-performance composites, and advanced industrial applications presents key market opportunities.

Some of the key market players include Syrah Resources Limited, Imerys, Asbury Advanced Materials, Focus Graphite, Tirupati Carbons & Chemicals Pvt Ltd, and Mason Resources Inc.