- Food Ingredients & Additives

- Edible Flakes Market

Edible Flakes Market Size, Share, and Growth Forecast 2026 - 2033

Edible Flakes Market by Product (Corn Flakes, Oat Flakes, Wheat Flakes, Others), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail Stores, Others), Nature (Organic, Conventional), by Regional Analysis, 2026 - 2033

Edible Flakes Market Size and Trend Analysis

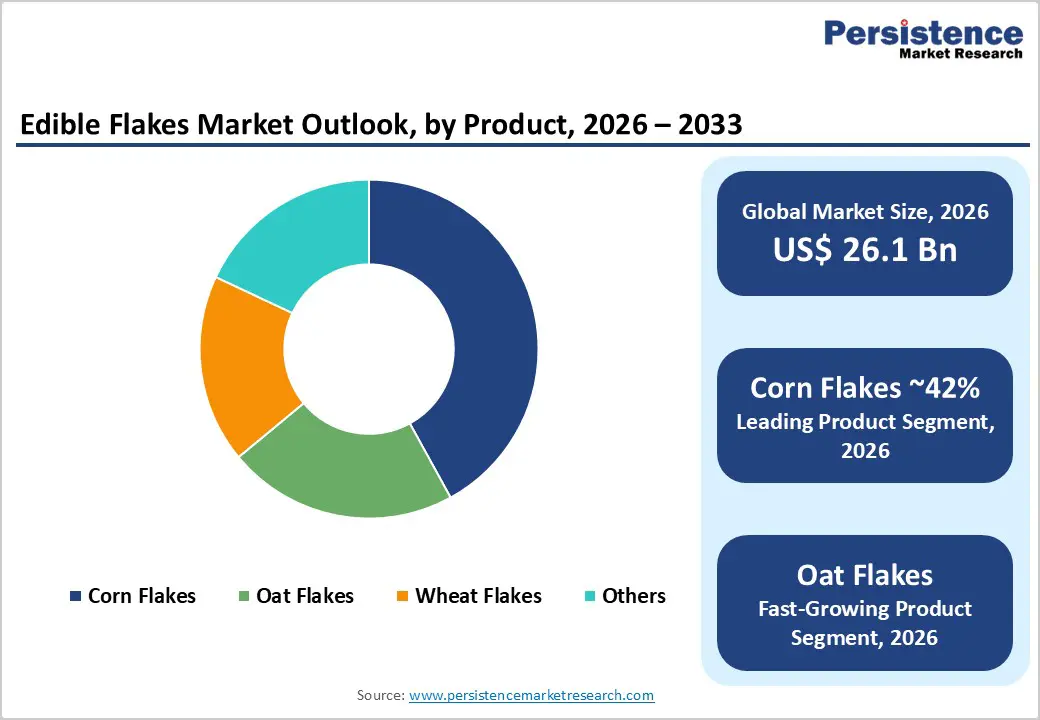

The global Edible Flakes market size is expected to be valued at US$ 26.1 billion in 2026 and projected to reach US$ 38.3 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

Rise in global consumer demand for convenient, nutritious, and time-efficient breakfast and snack options drives the market growth. Urbanization-driven lifestyle shifts, growing awareness of whole-grain and high-fiber dietary benefits, and the rapid proliferation of modern retail formats and e-commerce grocery channels are the core forces. Simultaneously, product innovation across fortified, organic, and functional flake variants supported by investments from major players such as Kellogg Co. and General Mills Inc. is expanding the category's appeal across age groups and geographies.

Key Industry Highlights:

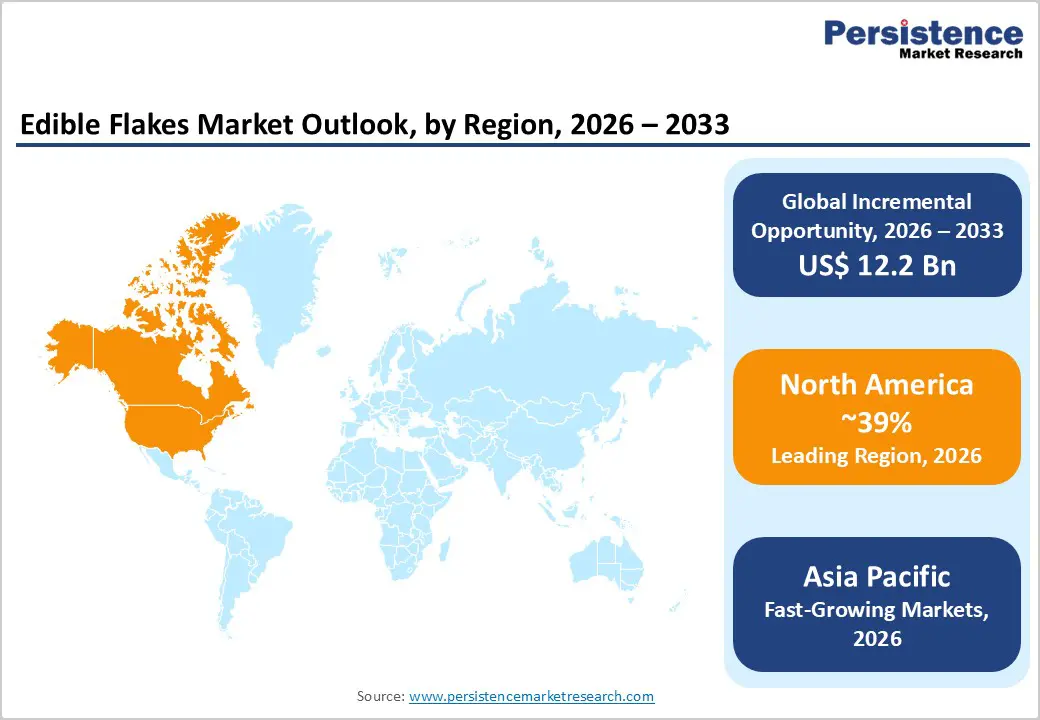

- Regional Leadership: North America is expected to dominate the market with a 39% revenue share in 2026, fueled by strong demand for ready-to-eat breakfast options and a high level of health consciousness among consumers.

- Fastest Growing Region: Asia Pacific is the fastest-growing region through 2033, fueled by rapid urbanization, expanding middle-class populations adopting Western breakfast habits, and strong e-commerce grocery infrastructure in China, India, and Southeast Asia.

- Dominant Product Segment: Corn flakes segment is expected to dominate the market with a 43% share in 2025, driven by their widespread popularity, strong brand presence, and long shelf life.

- Fast-growing Product Segment: Oat flakes are the fast-growing product category, propelled by the FDA-endorsed heart health claim for oat beta-glucan, rising consumer demand for high-fiber low-glycemic-index breakfasts, and the explosive popularity of overnight oats among health-conscious millennials.

- Key Opportunity: Increasing focus on health and wellness is driving innovation in the edible flakes market, with brands introducing healthier options such as gluten-free, high-protein, and low-sugar flakes to cater to health-conscious consumers.

Market Dynamics

Drivers - Increase in global prevalence of diabetes

According to the International Diabetes Foundation, approximately 589 million adults aged between 20 and 79 years are diagnosed with diabetes globally, while the number will cross 853 million by 2050. As more people are diagnosed with diabetes or pre-diabetes, there is a growing awareness about managing blood sugar levels through diet. This has led consumers to seek low-sugar, high-fiber, and functional foods, which are considered beneficial for blood sugar control.

Edible flakes that offer these health benefits, such as those with high fiber content, low glycemic index, or fortified with nutrients like omega-3 fatty acids, are becoming more popular.

As a result, the demand for these types of breakfast options is increasing as individuals with diabetes or those at risk look for healthier, convenient meal choices. To capitalize on this trend, companies are focusing on introducing innovative products to cater to the growing health-conscious consumers, which is likely to favor market growth.

Restraints - Wider availability of other healthier alternatives

The industry has faced intense competition from an expanding array of alternative breakfast and snack options. As consumers become more health-conscious, there is a noticeable shift toward convenient, on-the-go products such as smoothies, protein bars, and ready-to-eat meals. These alternatives often promise higher protein content, fewer artificial ingredients, and greater versatility compared to traditional breakfast cereals, leading to their high consumption. For example, as per a 2024 study, 70% of health-conscious adults consume protein bars at least 3-4 times a week to meet their nutritional requirements on the go.

This shift is attributed to the increasing demand for plant-based, low-sugar, and functional ingredients in snacks, aligning with modern dietary preferences. As a result, the availability of other healthier alternatives is expected to hinder market growth to a certain extent in the forthcoming years.

Opportunities - Product customization a key to unlock exciting growth opportunities

The increasing trend of personalized nutrition has sparked a shift in consumer expectations, particularly in the breakfast category. As more individuals focus on their specific dietary needs, whether it is protein intake, managing sugar levels, or incorporating superfoods, the demand for customizable food options is always constant. Edible flakes that allow consumers to customize their breakfast by choosing grains, flavors, and added ingredients such as nuts, seeds, and superfoods. This level of customization not only empowers consumers to create a product that fits their lifestyle but also creates an emotional connection with the brand, as consumers feel their specific health and taste preferences are being met.

Moreover, the rising shift towards personalization opens up exciting opportunities for companies to tap into the growing demand for subscription-based models and direct-to-consumer channels. Brands that offer personalized breakfast options through a subscription service, where consumers receive customized flakes based on their dietary needs, are projected to gain significantly. This is due to such models facilitating recurring revenue and providing a more engaging, personalized customer experience. With health and wellness becoming top priorities, providing customized product options is likely to create new revenue opportunities for companies to further consolidate their position.

Category-wise Analysis

Product Insights

Based on product, the market is divided into corn flakes, oat flakes, wheat flakes, and others. Among these, the corn flakes segment is projected to dominate and hold a share of about 43% in 2025. This dominance is attributed to their widespread popularity, long-standing consumer familiarity, and extensive availability across stores globally. Corn flakes have become a staple breakfast option for many due to their convenience, long shelf life, and strong presence of global brands such as Kellogg’s, which continue to drive product visibility and consumer loyalty.

Oat flakes segment, on the other hand, is anticipated to witness the fastest growth in the forthcoming years. High demand for oat flakes is primarily due to increasing consumer awareness regarding health and wellness. Oats are recognized for their high fiber content, heart health benefits, and role in weight management, making them highly appealing to health-conscious consumers.

Distribution Channel Analysis

By distribution channel, the supermarkets/hypermarkets segment is likely to register a share of approximately 60% in 2025 and further dominate. Offline distribution channels include supermarkets, hypermarkets, convenience stores, and grocery outlets, where consumers prefer to physically check product quality, compare brands, and make immediate purchases. Besides, bulk buying and promotional offers at brick-and-mortar stores attract large consumers, driving the segment’s growth in the forthcoming years.

On the other hand, the online segment is projected to register the fastest growth, driven by increasing internet penetration, smartphone usage, and shifting consumer preferences toward convenience and time-saving shopping methods. Urban consumers, particularly millennials and Gen Z, are turning to e-commerce platforms for grocery purchases, including breakfast items such as edible flakes. For example, as per studies, about 1.4 billion people globally use online grocery delivery services monthly.

Regional Insights

North America Edible Flakes Market Trends and Insights

North America is projected a revenue share of about 39% in 2025. Consumers strongly prefer convenient and ready-to-eat breakfast options such as corn and oat flakes. The presence of major manufacturers such as Kellogg Co, Post Holdings, and General Mills, innovative product launches, and increasing demand for health-oriented cereal products continue to support market growth in the region. Additionally, high awareness of nutritional benefits and the growing trend of fortified breakfast cereals are expected to boost product adoption.

U.S. Edible Flakes Market Size

The United States accounts for approximately 80% of North American edible flakes revenue, backed by per-capita cereal consumption among the highest globally. SPINS data indicates U.S. natural and conventional cereal sales remain a multi-billion-dollar annual category. Product innovation in fortified and organic oat flakes by Quaker Oat Company and Nature's Path Foods sustains market momentum through 2033.

Europe Edible Flakes Market Trends and Insights

Europe represents the second-largest edible flakes market, holding approximately 26% of global share, driven by high whole-grain cereal consumption traditions in Germany, United Kingdom, and Scandinavia. The European Green Deal's Farm to Fork strategy is supporting organic cereal production, while private-label organic flakes gaining mainstream traction across Aldi, Lidl, and Tesco formats.

Germany Edible Flakes Market Size

Germany is Europe's largest edible flakes market, contributing approximately 18–20% of regional revenue, supported by a strong muesli and whole-grain oat flake consumption culture. German consumers' preference for clean-label and organic products verified by Agrarmarkt Informations-Gesellschaft (AMI) data showing steady organic food growth positions premium flake brands for continued expansion through 2033.

U.K. Edible Flakes Market Size

The United Kingdom accounts for approximately 14–16% of European edible flakes market value, with one of the highest per-capita breakfast cereal consumption rates in Europe. Kellogg's and Nestlé's Shredded Wheat dominate the market. Rising oat flakes demand, driven by NHS dietary guidelines promoting oat-based breakfasts for cardiovascular health, supports category premiumization through 2033.

Asia Pacific Edible Flakes Market Trends and Insights

Asia Pacific is anticipated to witness considerable growth by 2033. Rapid urbanization, changing dietary habits, and an increasing shift toward western-style breakfast options are growth factors in this region. In addition, rising middle-income population, growing awareness of healthy eating, and busy lifestyles push consumers toward convenient and nutritious breakfast alternatives. With expanding retail infrastructure and the growing influence of digital marketing, edible flakes are becoming more visible and accessible to a wider population in the region for example, according to a 2024 study, 62% of Indian and Chinese consumers spent high on buying online grocery.

China Edible Flakes Market Size

China edible flakes market leads in terms of growth and volume in the region. The country is experiencing a significant rise in demand for packaged and functional foods, especially in metropolitan areas. Consumers are increasingly opting for healthier and quick-to-prepare meals due to their hectic work schedules. Moreover, domestic and international brands are actively launching region-specific flavors such as red dates or goji berries to appeal to regional tastes. Thereby, all these factors help China maintain its dominance in the region.

India Edible Flakes Market Size

India represents approximately 14–16% of the Asia Pacific edible flakes market, with demand anchored by Kellogg's India, Marico Ltd., and Patanjali's growing indigenous brand presence. Rising urban health consciousness, expanding modern retail, and growing school breakfast programs are key demand drivers. India's young demographic profile and rapid nutrition awareness growth support sustained double-digit regional market expansion through 2033.

Competitive Landscape

The global edible flakes market is moderately fragmented, featuring a mix of established players, regional companies, and emerging health-conscious startups. Key companies compete on parameters such as product variety, nutritional value, pricing, brand reputation, and distribution reach. While multinational corporations have traditionally held strong positions due to brand recognition and extensive distribution networks, the landscape is shifting with the rise of local brands and niche players tapping into evolving consumer preferences.

There is a clear trend toward health and wellness, which has intensified competition. Companies are diversifying their product lines to include organic, gluten-free, high-fiber, low-sugar, and protein-enriched flakes to cater to the demand for healthier alternatives. Brands are launching new flavors, experimenting with ancient grains like quinoa or millet, and offering products targeted at specific demographics. Additionally, growing adoption of online retail and direct-to-consumer (DTC) models is allowing companies to reach niche audiences more effectively without relying solely on traditional retail shelf space.

Key Developments

- In September 2024, Tata Soulfull, a brand from the house of Tata Consumer Products, announced the launch of Masala Muesli. This innovative product is projected to transform the traditional muesli category with a unique flavor twist. The product will be available in two flavors such as Teekha Twist and Mast Masala, as per the company.

- In April 2024, Fuel10K expanded its breakfast portfolio with the launch of a new duo of multigrain flakes. The new range includes chocolate multigrain flakes and honey multigrain flakes, aimed at health-conscious consumers seeking high-protein, low-sugar options.

Global Edible Flakes Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 20.3 billion |

|

Current Market Value (2026) |

US$ 26.1 billion |

|

Projected Market Value (2033) |

US$ 38.3 billion |

|

CAGR (2026–2033) |

5.6% |

|

Leading Region |

North America, ~39% market share (2025) |

|

Dominant Product |

Corn Flakes, ~42% market share (2025) |

|

Top-Ranking Distribution Channel |

Supermarkets/ Hypermarkets, ~52% market share (2025) |

|

Incremental Opportunity |

US$ 12.2 billion |

Companies Covered in Edible Flakes Market

- Kellogg Co.

- PepsiCo Inc.

- Nature’s Path Foods

- Quakers Oat Company

- Nestle SA

- Patanjali

- General Mills Inc.

- Marico Ltd.

- Post Holdings Inc.

- The Hain Celestial Group Inc.

- Others

Frequently Asked Questions

The global edible flakes market is valued at US$ 26.1 billion in 2026.

The market is driven by increasing consumer demand for healthier, more convenient breakfast options, along with the rising awareness of the nutritional benefits of high-fiber, low-glycemic, and fortified flakes, particularly among individuals with diabetes or those at risk.

North America leads with approximately 39% of global edible flakes market share in 2025.

The key opportunities include the growing trend of personalized nutrition, allowing customizable edible flakes, the rise of subscription-based models and direct-to-consumer channels, offering consumers personalize breakfast cereals options to meet their specific dietary needs.

Major players in the edible flakes industry include Kellogg, Nestle, PepsiCo Inc., Quakers Oat Company, and Marico.