- Biotechnology

- Fibroblast Growth Factors Market

Fibroblast Growth Factors Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Fibroblast Growth Factors Market by Product Type (FGF1, FGF2, FGF7, FGF10,FGF19, FGF21, FGF23, Others), Form (Research Grade, GMP Grade, Finished Formulations, Kits & Diagnostic Reagents), Application (Oncology, Hematology, Wound Healing, Dermatology, Cardiovascular Disease & Diabetes, Cell Therapy, Others), End User (Pharmaceutical & Biotechnology Companies, Research Centers & Academic Institutes, Contract Research & Manufacturing Organizations), and Regional Analysis from 2025 - 2032

Fibroblast Growth Factors Market Size and Share Analysis

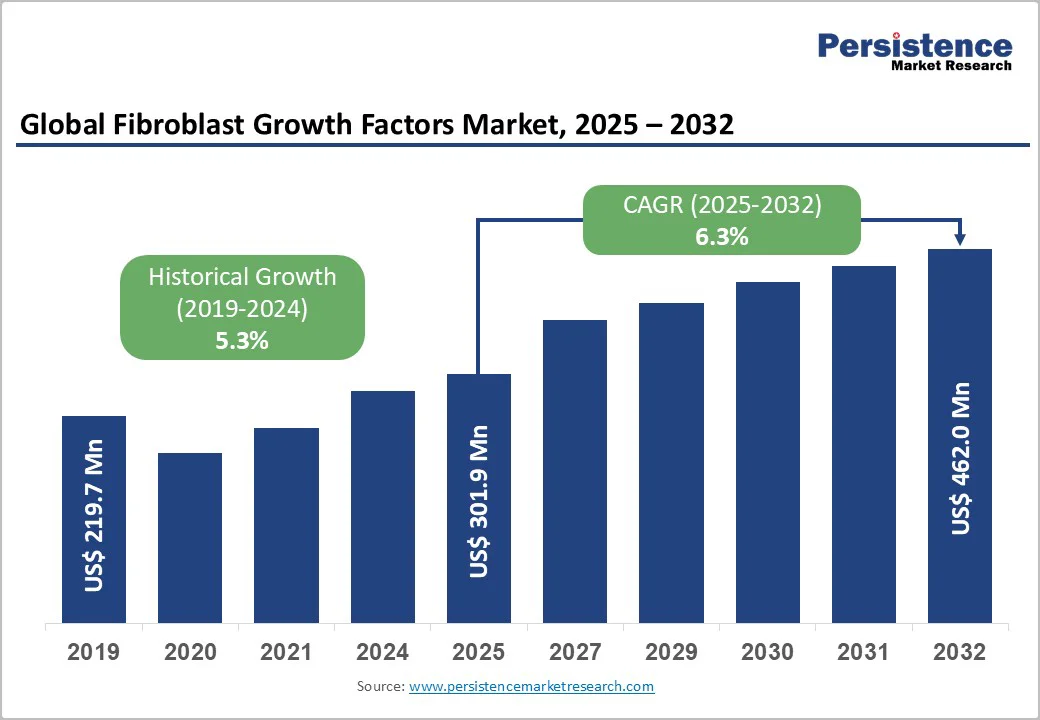

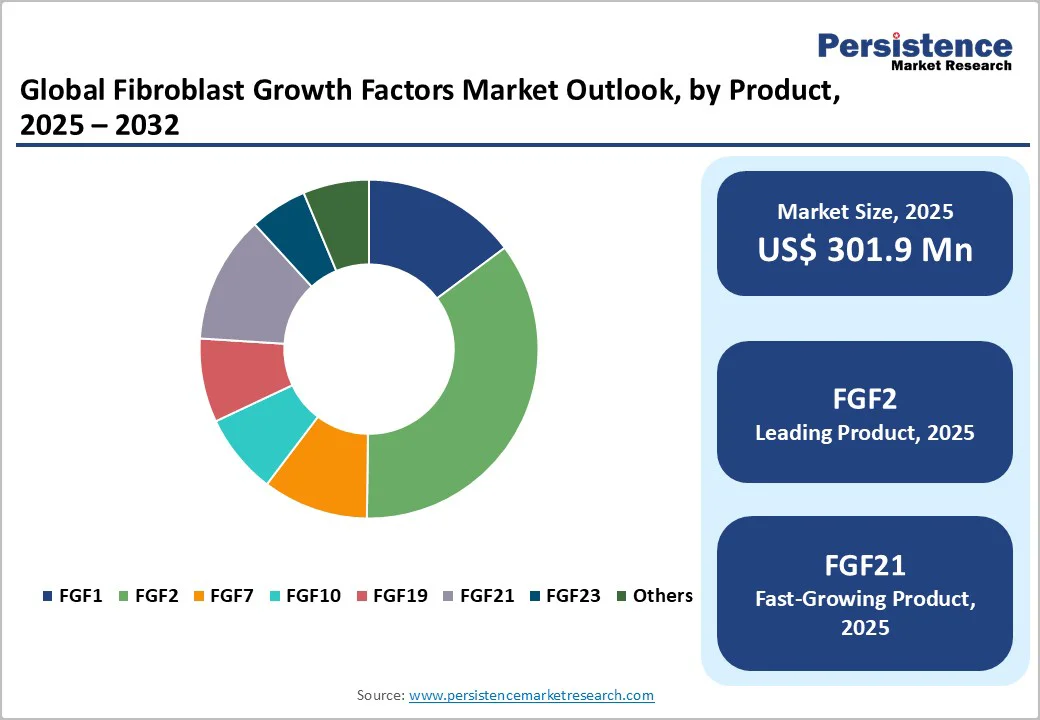

The global fibroblast growth factors market is estimated to grow from US$301.9 Mn in 2025 to US$462.0 Mn by 2032. The market is projected to grow at a CAGR of 6.3% over the forecast period from 2025 to 2032.

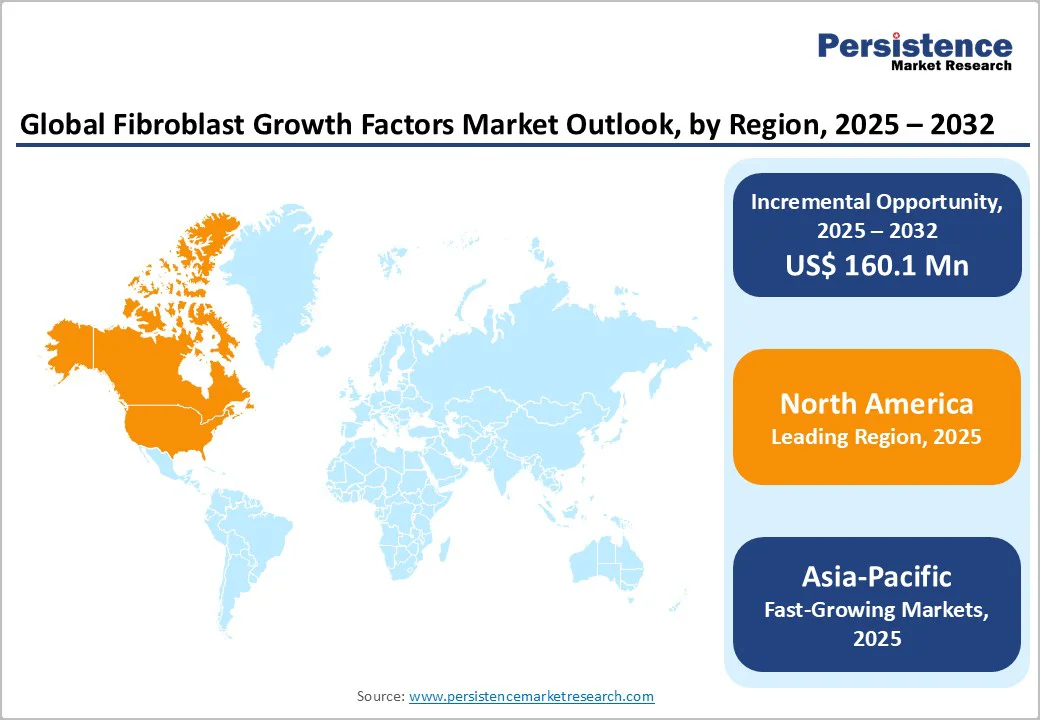

The global fibroblast growth factors (FGFs) market is growing steadily, driven by rising demand in regenerative medicine, wound healing, and biopharmaceutical research. North America dominates due to its strong biotech infrastructure and ongoing clinical trials. At the same time, Asia-Pacific records the fastest growth, supported by expanding biomanufacturing, government-backed stem cell programs, and increasing collaborations between regional and global life science companies.

Key Industry Highlights

- Dominant Product Type: FGF2 (basic fibroblast growth factor) holds about 35.4% share of the fibroblast growth factors market, driven by its extensive use in cell culture, regenerative medicine, and wound-healing research. Its proven role in tissue repair and stem cell proliferation supports its leadership in both research-grade and clinical-grade applications.

- Dominant Form: Research-grade FGFs account for around 53.6% share, supported by widespread adoption across academic labs, biotech firms, and CROs for cell-based studies and drug discovery. High reproducibility, easy availability, and demand for high-purity reagents sustain this dominance.

- Dominant Region: North America, contributing roughly 38.1% of global revenue, leads the market owing to its advanced biotechnology ecosystem, extensive R&D investments, strong presence of recombinant protein manufacturers, and active clinical trials targeting metabolic and liver disorders.

- Investment Plans: Asia-Pacific is the fastest-growing region, propelled by expanding biomanufacturing infrastructure, government support for stem cell research, rising healthcare investments, and collaborations between domestic biotechs and global protein suppliers.

- Market Drivers: Growing focus on regenerative medicine, increasing therapeutic applications of FGFs in wound healing and tissue repair, expansion of biopharmaceutical R&D, and rising use of recombinant proteins in cell culture and drug development.

- Market Opportunity: Development of engineered or long-acting FGF analogs, integration into advanced biomaterials, strategic collaborations for clinical-grade production, and expansion into emerging markets emphasizing biotech innovation and translational research.

| Key Insights | Details |

|---|---|

|

Global Fibroblast Growth Factors Market Size (2025E) |

US$ 301.9 Mn |

|

Market Value Forecast (2032F) |

US$ 462.0 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

6.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.3% |

Market Dynamics

Driver - In-depth Understanding of Wound Healing Mechanisms and Advancements in Molecular Science

Wound healing poses an ongoing therapeutic perplex within the medical community, given the intricacies involved in assessing and managing wounds. This involves navigating a complex process influenced by several critical factors on the healing journey.

Tissue injury is a common denominator across all medical specialties. Wound healing, regardless of the tissue involved, follows a consistent sequence of events. A comprehensive understanding of this sequence, the involved cells, their timing, and the molecular signals involved can significantly optimize patient care.

Remarkable progress has been achieved in comprehending the intricate mechanisms of wound healing. Advancements in molecular science have enabled modern medicine to gain a profound understanding of the intricate interactions between cells during different phases of wound healing. As knowledge of growth factors deepens, the future of patient care is expected to encompass scar-free wound healing and the transplantation of tissues cultivated from stem cell precursors.

Increasing research and development in this field is likely to open new avenues for the application of fibroblast growth factors, thereby providing market players with lucrative growth opportunities.

Restraints - High Cost Associated with Development and Production of FGFs

The intricate process of developing and producing FGFs entails substantial financial implications, underscoring the complex nature of modern medical research and biotechnology. While the potential benefits of FGFs across various therapeutic applications are undeniable, the high costs of their development and production pose significant challenges that require careful consideration.

The initial research phase involves in-depth investigations into FGFs' molecular mechanisms, interactions, and potential applications. These studies often require specialized equipment, skilled personnel, and extensive resources. Subsequent preclinical testing aims to assess FGFs' safety and efficacy, necessitating comprehensive studies in animal models, thereby further increasing the financial burden.

The pinnacle of FGF development lies in conducting rigorous clinical trials to validate their therapeutic potential in human subjects. These trials, spanning multiple phases, involve substantial investments in patient recruitment, medical monitoring, data analysis, and regulatory compliance. The costs escalate as trials progress, and the potential for unexpected challenges or setbacks further emphasizes the financial risk. These challenges are expected to hinder market growth.

Opportunity - Therapeutic Development of FGF21 and FGF19 Analogs

Therapeutic development of FGF21 and FGF19 analogs is a high-value opportunity in the FGFs market because several engineered FGF21 candidates have delivered meaningful clinical signals (reduced liver fat, improved fibrosis markers) and advanced into late-stage testing.

For example, the pegozafermin phase 2b ENLIVEN study showed fibrosis and metabolic benefits. Regulatory momentum is visible: the U.S. FDA granted Breakthrough Therapy designation to pegozafermin in September 2023, and a Phase III program began in 2024, accelerating commercial pathways. Published reviews and clinical registries list multiple active FGF21 analog trials and evolving FGF19 studies, indicating a sustained pipeline across NASH, severe hypertriglyceridemia, and metabolic indications. Because no FGF21/F19 drug was widely approved as of recent reviews, successful phase-3 outcomes would create first-mover therapeutics with large addressable markets in metabolic liver disease and cardiometabolic comorbidities.

Category-wise Analysis

By Product, FGF2 Dominates the Fibroblast Growth Factors Market

FGF2 occupied 35.4% share of the global market in 2024. FGF2 has gained popularity due to its broad range of biological activities and applications in various fields. It is one of the most extensively studied and characterized members of the FGF family, contributing to its widespread recognition and utilization.

The relatively simple structure and well-understood signaling pathways of FGF2 have facilitated its study and manipulation in research and therapeutic contexts. Its interactions with cell surface receptors are well-documented, making it a more accessible target for experimental and clinical interventions.

By Product Form, Research Grade is gaining traction due to extensive global R&D use in cell culture and regenerative studies

Research-grade FGFs dominate the market as they are widely used in cell culture, stem cell expansion, and regenerative biology research. Data from the U.S. NIH RePORT indicate over 1,200 active projects referencing fibroblast growth factors between 2020 and 2024, while PubMed lists more than 8,000 FGF-related studies in the past five years.

These figures reflect extensive academic and preclinical demand for laboratory-grade FGFs, especially FGF2 and FGF10, which are vital for cell proliferation and differentiation experiments. In contrast, GMP-grade FGFs are primarily used in clinical trials, accounting for a smaller share of the market. The widespread scientific use, affordability, and accessibility of recombinant proteins have made research-grade FGFs the leading product form in the global fibroblast growth factors market

Regional Insights

North America Fibroblast Growth Factors Market Trends

North America dominates the fibroblast growth factors (FGFs) market with a 38.1% share in 2024, driven by its strong biotechnology ecosystem, extensive R&D funding, and therapeutic innovation. The U.S. alone accounts for about 35.6% of global biotechnology revenue, with California receiving over US $5.3 billion annually in biomedical research funding and generating 40% of U.S.

life-sciences patents. Rising cancer incidence further fuels FGF demand, according to ASCO (2023), about 297,790 women were projected to be diagnosed with invasive breast cancer and 26,500 new cases of stomach cancer were reported in 2022 (American Cancer Society). The growing need for FGFs and cytokines in carcinoma treatment, alongside strong FDA support and government-backed research in regenerative and precision medicine, continues to strengthen North America’s global leadership in the FGFs market.

Europe Fibroblast Growth Factors Market Trends

Europe stands as a leading region in the fibroblast growth factors (FGFs) market due to its strong life sciences ecosystem, high R&D spending, and supportive government policies. The European Commission reports that the life sciences sector contributes nearly €1.5 trillion in value and supports 29 million jobs across the EU, with business R&D investment reaching €247 billion in 2023. Within Europe, Germany leads in biotechnology and regenerative medicine, focusing on FGF-based innovations that promote tissue regeneration for chronic wounds, musculoskeletal disorders, and neurological conditions. Supported by programs like Bioeconomy International, Germany’s collaboration between academia, biotech firms, and government bodies fosters rapid translation of research into clinical applications, positioning Europe, especially Germany, as a powerhouse in the global FGFs market.

Asia-Pacific Fibroblast Growth Factors Market Trends

Asia-Pacific is the fastest-growing region in the fibroblast growth factors (FGFs) market, fueled by rising healthcare expenditure, robust biotech innovation, and a strong oncology research focus. According to the OECD, public health spending per capita in APAC countries grew by 4.7% annually between 2010 and 2019, while the region’s healthcare market is expected to surpass US$ 5 trillion by 2030. Within this, China plays a leading role, with FGFs emerging as therapeutic targets for solid tumors due to their roles in angiogenesis and tumor progression. Supported by a thriving biopharmaceutical sector and active clinical research on FGF inhibitors in breast, lung, and gastrointestinal cancers, China’s advancements are accelerating regional adoption of FGF-based regenerative and oncology therapies, strengthening the Asia-Pacific’s rapid market expansion.

Market Competitive Landscape

Leading companies in the fibroblast growth factors (FGFs) market are focusing on biotechnological innovation, therapeutic development, and strategic collaborations. They are investing in advanced protein engineering, regenerative medicine research, and clinical-grade production to expand global reach, enhance treatment efficacy, and meet rising demand for cell therapy, oncology, and wound-healing applications.

Key Industry Developments:

- In January 2025, Roche announced that the U.S. FDA approved a label expansion for the PATHWAY® anti-HER2/neu (4B5) Rabbit Monoclonal Primary Antibody. The expansion allows the identification of patients with HR-positive, HER2-ultralow metastatic breast cancer who may be eligible for treatment with ENHERTU®. ENHERTU, a HER2-directed antibody-drug conjugate, was discovered by Daiichi Sankyo and is being jointly developed and commercialized by Daiichi Sankyo and AstraZeneca.

- In January 2025, Bio-Techne launched AI-engineered designer proteins under its R&D Systems brand. The new portfolio included IL-2 Heat Stable Agonist, Activin A Hyperactive, FGF basic Heat Stable (RUO & GMP), and Wnt/RSPO Agonists, designed for research and therapeutic applications.

- In August 2024, Leadgene Biomedical expanded its presence in northern Taiwan with the launch of two new facilities: an Innovation & Research Center in Xike and a Cell Line Development (CLD) Center in Taipei. The expansion strengthens Leadgene’s capabilities in R&D and cell line development, reinforcing its position in the biomedical sector.

Companies Covered in Fibroblast Growth Factors Market

- Thermo Fisher Scientific, Inc.

- Merck KGaA

- Bio-Rad Laboratories, Inc.

- Lonza Group AG

- F. Hoffmann-La Roche Ltd.

- Bio-Techne Corporation

- Abcam PLC (Danaher)

- Cell Signaling Technology, Inc.

- Creative Bioarray

- Proteintech Group, Inc.

- Sartorius CellGenix GmbH

- GenScript

- Miltenyi Biotec.

- Sino Biological Inc.

- ACROBiosystems

- Applied Biological Materials (abm) Inc.

- Meridian Bioscience Inc.

- Aviva Systems Biology Corporation (GenWay Biotech)

- Leadgene Biomedical, Inc.

- Boster Bio

- Prospec-Tany Technogene Ltd.

- AJINOMOTO CO.,INC

- STEMCELL Technologies

- Akron Biotech

- Others

Frequently Asked Questions

The global fibroblast growth factors market is projected to be valued at US$ 301.9 Mn in 2025.

Rising regenerative medicine research, cancer therapy advancements, and increased R&D investments in protein-based biologics drive the global FGF market.

The global fibroblast growth factors market is poised to witness a CAGR of 6.3% between 2025 and 2032.

Development of FGF-based therapeutics, expansion in regenerative medicine, and partnerships for oncology, wound healing, and cell therapy applications offer opportunities.

Thermo Fisher Scientific, Inc., Merck KGaA, Bio-Rad Laboratories, Inc., Lonza Group AG, F. Hoffmann-La Roche Ltd., Bio-Techne Corporation.