- Automation & Robotics

- Emission Control Systems Market

Emission Control Systems Market Size, Share, and Growth Forecast 2026 - 2033

Emission Control Systems Market by Device Type (Selective Catalytic Reduction Systems, Flue Gas Desulfurization Units, Electrostatic Precipitators, Fabric/Baghouse Filters, Scrubbers/Absorbers, Catalytic Converters, Diesel & Industrial Particulate Filters, Others), End-user (Transportation, Power Generation, Oil & Gas, Chemicals, Petrochemicals & Fertilizers, Cement Manufacturing, Metals & Mining Others), Installation and Regional Analysis, 2026 - 2033

Emission Control Systems Market Size and Trend Analysis

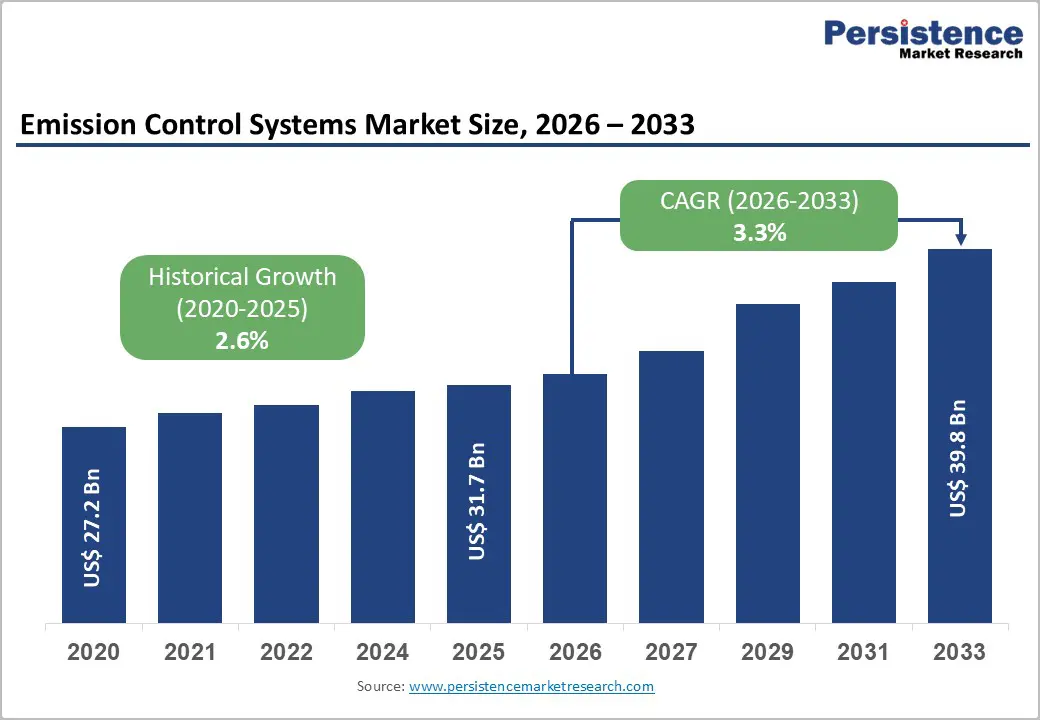

The global Emission Control Systems market size is expected to be valued at US$ 31.7 billion in 2026 and projected to reach US$ 39.8 billion by 2033, growing at a CAGR of 3.3% between 2026 and 2033.

Stringent environmental regulations enacted by governments across North America, Europe, and the Asia-Pacific are the primary catalysts driving market growth. Regulatory bodies, including the US Environmental Protection Agency (EPA), European Commission, and the Ministry of Environment, Forest & Climate Change in India, have mandated increasingly stringent emission standards for both mobile and stationary sources, compelling industries to invest in advanced emission control technologies. Rising air pollution concerns in major metropolitan areas have accelerated the adoption of emission control systems across transportation, power generation, and industrial sectors, creating sustained demand for these critical environmental protection solutions.

Key Industry Highlights:

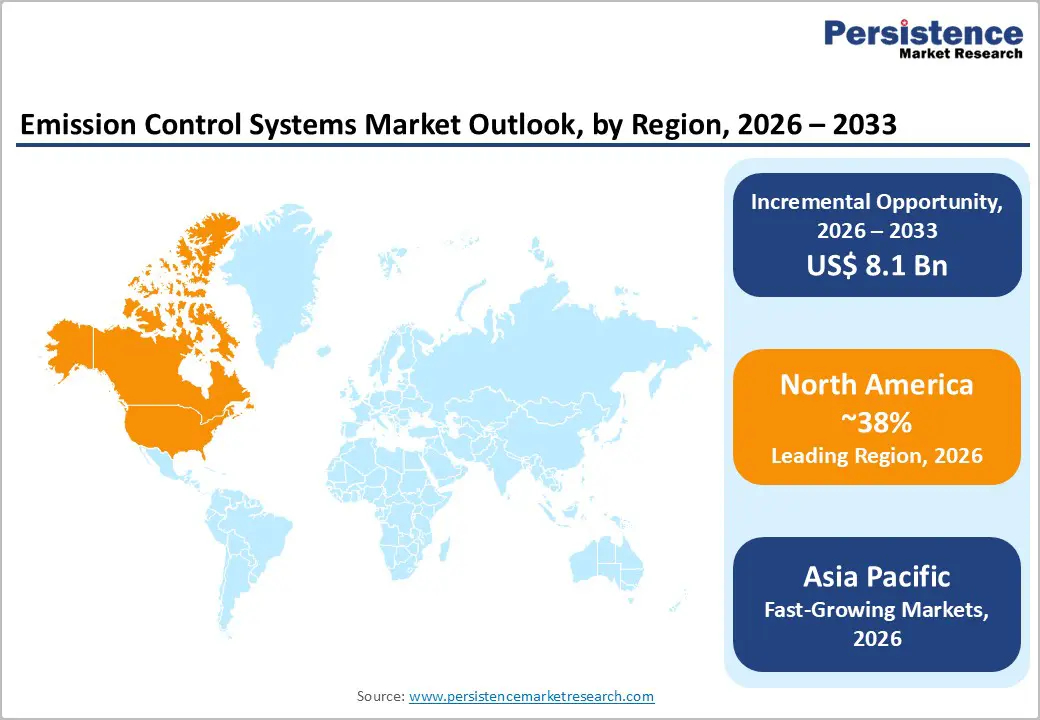

- Leading Region: North America commands the largest regional market share of approximately 38% in 2025, driven by stringent federal EPA regulations, established regulatory compliance culture, and substantial automotive manufacturing base.

- Emerging Region: Asia Pacific is the fastest-growing regional market, expanding at a CAGR of 4.8% between 2026 and 2033, driven by rapid industrial expansion in China and India, rising vehicle production volumes, and accelerating implementation of stringent automotive and industrial emission standards.

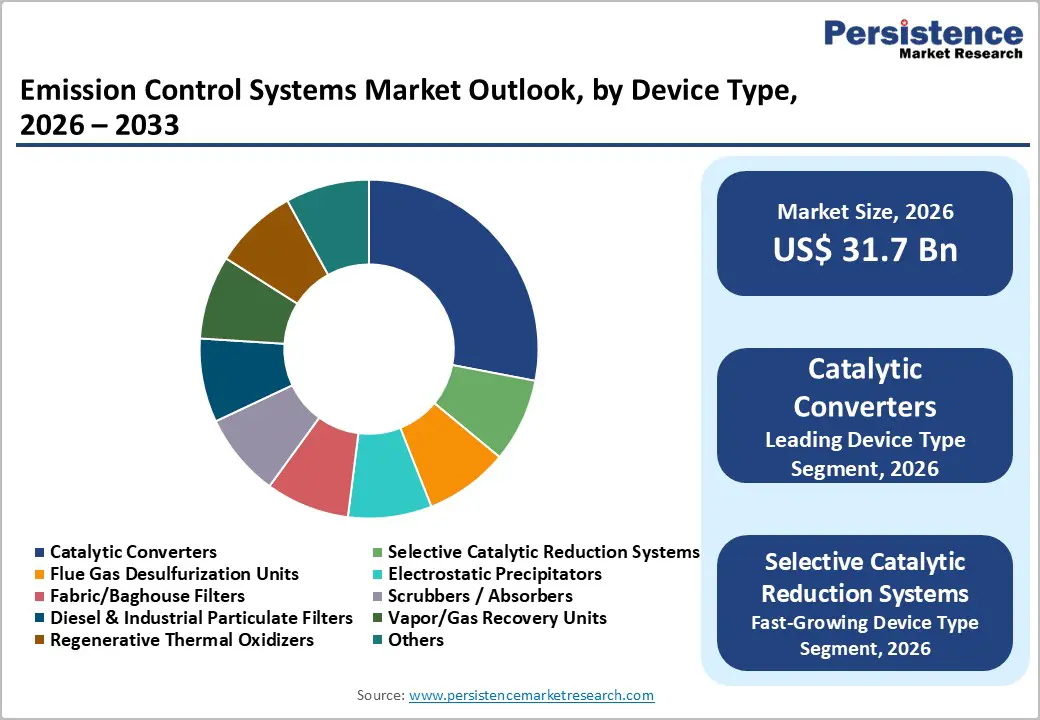

- Dominant Segment: Catalytic converters function as the dominant device type segment, commanding approximately 28% market share in 2025, reflecting their universal requirement across automotive platforms and their critical role in meeting stringent nitrogen oxide and particulate matter emission standards globally.

- Fastest Growing Segment: Selective catalytic reduction systems represent the fastest-growing device type segment, expanding at a CAGR of 4.2% between 2025 and 2032, driven by stringent nitrogen oxide emission standards for heavy-duty vehicles, power generation facilities, and industrial equipment, particularly in Asia Pacific and Europe.

- Key Opportunity: The emerging retrofit emission control market in developing economies presents substantial growth potential, as aging vehicle fleets and industrial equipment transition to compliant technologies through cost-effective retrofit programs supported by government incentives and enforcement actions.

| Key Insights | Details |

|---|---|

|

Emission Control Systems Market Size (2026E) |

US$ 31.7 billion |

|

Market Value Forecast (2033F) |

US$ 39.8 billion |

|

Projected Growth CAGR (2026-2033) |

3.3% |

|

Historical Market Growth (2020-2025) |

2.6% |

Market Dynamics

Drivers - Tightening Global Emission Standards and Regulatory Compliance

Stringent regulatory frameworks across major economies have become the foremost growth driver for the emission control systems market. The European Union’s Euro VI standards have set unprecedented limits on nitrogen oxide (NOx) emissions from vehicles and industrial equipment, achieving reductions of up to 95% compared to pre-regulation engines. Similarly, the United States EPA has implemented Tier 3 standards requiring fleet-average reductions of up to 80% for combined nitrogen oxide and non-methane organic gas emissions by 2025.

India’s Bharat Stage VI (BS-VI) emission norms, implemented for vehicles manufactured after April 1, 2020, mandate compliance with ultra-strict emission standards comparable to Euro 6 specifications. Additionally, the International Maritime Organization’s MARPOL Annex VI regulations impose strict limits on nitrogen oxide and sulfur oxide emissions from marine vessels, with Tier III standards requiring a 80% reduction in NOx emissions for new ships operating in designated Emission Control Areas. These multifaceted regulatory pressures across automotive, industrial, power generation, and marine sectors have created robust demand for selective catalytic reduction systems, diesel particulate filters, and flue gas desulfurization units, driving sustained market expansion.

Rapid Industrialization and Urbanization in Emerging Economies

The accelerating pace of industrialization and urbanization in the Asia-Pacific, particularly in China, India, and Southeast Asian nations, has intensified the need for emission-control solutions across the manufacturing, power generation, and transportation sectors. China’s manufacturing base, which accounts for over 40% of global industrial equipment production, combined with the country’s aggressive environmental policies, has created substantial demand for emission-control technologies.

India’s National Clean Air Programme, launched in January 2019, targets a 20-30% reduction in particulate matter concentrations in 131 cities by 2024, with revised targets aiming for up to a 40% reduction by 2025-2026. This comprehensive air quality improvement initiative has driven capital investments in emission control systems across power plants, cement factories, steel mills, and chemical processing facilities. The region’s expanding vehicle population, projected to account for over 56% of global vehicle production, combined with increasing environmental awareness among consumers and stricter enforcement of emission norms, has accelerated the adoption of catalytic converters, selective catalytic reduction systems, and diesel particulate filters, thereby expanding the market at an accelerated pace.

Restraints - Electric Vehicle Transition and Internal Combustion Engine Phase-Out

The global automotive industry’s transition toward electrification presents a significant long-term challenge to the traditional emission control systems market, particularly for vehicle-based applications. Fully electric vehicles eliminate the need for conventional exhaust aftertreatment systems such as catalytic converters and diesel particulate filters, which have historically represented a substantial revenue segment.

While plug-in hybrid vehicles and mild hybrids continue to require emission control systems, the accelerating adoption of battery-electric vehicles in developed markets, supported by government incentives and regulatory mandates, is expected to reduce the addressable market for automotive emission control technologies over the forecast period. This technological shift requires manufacturers to diversify their product portfolios and explore alternative applications in stationary sources and hybrid powertrains.

Volatile Precious Metal Prices and Supply Chain Disruptions

The selective catalytic reduction systems and catalytic converter market faces significant challenges stemming from volatile prices of platinum group metals, including platinum, palladium, and rhodium, which are essential catalytic materials. Geopolitical tensions, mining constraints, and supply chain disruptions have created price volatility that increases production costs and limits market competitiveness.

The scarcity of these precious metals, coupled with their critical role in achieving stringent emission standards, forces manufacturers to invest in expensive recovery and recycling technologies or develop low-precious-metal and zero-precious-metal catalyst formulations. Supply chain disruptions experienced since 2020 have constrained manufacturing capacity and extended delivery timelines, creating inventory challenges for original equipment manufacturers and aftermarket suppliers.

Opportunity - Retrofit Installation Programs and Aftermarket Expansion in Developing Nations

Significant opportunities exist in retrofitting existing equipment and vehicles in developing economies, where older, high-emission machines continue to operate due to limited replacement capital. Retrofit emission control systems, particularly diesel particulate filters and selective catalytic reduction units, have achieved remarkable market traction as cost-effective alternatives to equipment replacement. The retrofit segment commanded a dominant market share in 2024, driven by government incentives, corporate sustainability commitments, and enforcement actions targeting non-compliant equipment.

India’s push to retire non-BS VI vehicles and China’s aggressive phase-out of heavy-polluting commercial vehicles have created substantial retrofit opportunities worth billions of dollars. European retrofit programs have demonstrated successful implementation models, with VERT-approved retrofit technologies achieving 98% particle reduction efficiency and 97% solid particle number reduction, encouraging similar initiatives across the Asia Pacific and Latin American markets.

Advanced Emission Control Technologies for Industrial and Power Generation Sectors

Emerging opportunities in the industrial and power generation sectors present substantial growth potential as governments implement stricter air quality standards for stationary sources. Flue gas desulfurization systems, electrostatic precipitators, and fabric filter baghouse systems are experiencing accelerated demand from coal-fired thermal power plants, cement manufacturers, steel mills, and waste incineration facilities. India’s mandate to install flue gas desulfurization systems in thermal power plants by December 2025 has created a multi-billion-dollar market opportunity for emission-control equipment suppliers.

The U.S. EPA’s finalized updates to emissions standards for commercial and industrial solid waste incinerators, effective December 29, 2025, introduce stricter controls on fine particulate matter and regulated pollutants, requiring retrofitting or installation of advanced scrubber and baghouse systems. Additionally, the development of innovative technologies such as selective catalytic reduction systems for stationary diesel engines, regenerative thermal oxidizers for industrial volatile organic compounds treatment, and advanced sorbent injection systems for acid gas control is creating new market segments with significant growth potential in the industrial sector.

Category-wise Insights

Device Type Analysis

Catalytic converters represent the dominant device type segment, commanding approximately 28% market share in 2025 due to their widespread application across automotive platforms and stringent global emission standards. Catalytic converters have become the preferred technology for meeting Euro VI and Tier 3 emission standards, which mandate 95% reduction in nitrogen oxide and particulate matter emissions. The global automotive catalytic converter market is estimated at US$ 121.74 Bn in 2025. It is predicted to rise at a CAGR of 7.2% through the assessment period to reach a value of US$ 198.06 Bn by 2032.

Automotive OEMs including Toyota, Volkswagen, and General Motors have integrated advanced catalytic converter systems with real-time monitoring sensors and predictive maintenance capabilities into their powertrains. The catalytic converter market benefits from strong aftermarket demand, as fleet operators and individual vehicle owners seek replacement units to meet evolving standards, particularly in Asia Pacific markets where vehicle ownership continues to expand.

End-user Insights

The transportation sector, encompassing on-road vehicles, off-road equipment, railway, marine, and aviation applications, leads the market with approximately 47% market share in 2025, driven by regulatory mandates and technological advancements in automotive emission control. On-road vehicle applications represent the largest sub-segment, accounting for over 65% of transportation sector demand, as stringent automotive emission standards have become mandatory in virtually all developed and emerging markets.

Heavy-duty commercial vehicle applications, including trucks and buses, have emerged as high-growth segments following the implementation of Euro VI standards and equivalent regulations in China and India. Marine shipping represents a rapidly expanding segment driven by IMO MARPOL Annex VI regulations, with selective catalytic reduction systems and liquefied natural gas propulsion technologies becoming standard on new vessels operating in Emission Control Areas. The aviation sector presents emerging opportunities as regulatory bodies develop stricter nitrogen oxide emissions standards for aircraft engines, creating demand for advanced afterburner and catalytic oxidation technologies.

Installation Type Insights

Retrofit installations have established market dominance, capturing approximately 58% market share in 2025, reflecting the cost-effectiveness and rapid deployment advantages of retrofitting existing equipment over complete system replacement. Retrofit emission control technologies, including diesel oxidation catalysts, diesel particulate filters, and selective catalytic reduction units, have been successfully deployed across on-road vehicles, construction equipment, locomotives, and stationary industrial sources.

Government retrofit programs in Europe, North America, and increasingly in Asia Pacific regions have created sustained demand for certified retrofit systems meeting stringent durability and emissions performance requirements. Retrofit installations offer compelling value propositions for fleet operators seeking to extend equipment lifecycles while achieving compliance with evolving emission standards.

Regional Insights

North America Emission Control Systems Market Trends and Insights

North America remains the largest regional market for emission control systems, sustained by rigorous federal and state regulatory frameworks enforced by U.S. EPA and regional authorities. The United States accounts for nearly 72% of total North American market value, reflecting stringent Tier 3 and California LEV III regulations that require major reductions in NOx and particulate matter by 2025. These standards have accelerated deployment of three-way catalytic converters, diesel particulate filters, and selective catalytic reduction in light- and heavy-duty vehicles.

Market growth is further supported by adherence requirements across refineries, waste incineration, and industrial boilers. Updated EPA standards for commercial and industrial waste combustors finalized in June 2025 are projected to stimulate several billion dollars in retrofit and system upgrade demand. North America benefits from a well-established automotive supply chain, high regulatory enforcement capability, and investments in digital and predictive monitoring technologies to optimize aftertreatment performance and lifecycle cost.

Europe Emission Control Systems Market Trends and Insights

Europe represents a global leader in emission control innovation, reinforced by stringent EU regulatory policies and concentrated automotive manufacturing capacity. The EU’s Euro VI standards mandate up to 95% reduction in NOx and particulate emissions, establishing one of the strictest compliance thresholds worldwide. Germany, France, and the UK remain major adopters of advanced aftertreatment solutions across automotive and industrial systems.

The European Green Deal and target of 55% greenhouse gas reduction by 2030 encourage parallel electrification and emissions compliance for remaining internal combustion and industrial assets. Post-Brexit, the UK maintains alignment through the Environment Act 2021, sustaining long-term market demand. Industrial and municipal waste treatment facilities across Europe increasingly install hybrid baghouse-electrostatic precipitator configurations and advanced acid gas scrubbers. The region’s mature regulatory governance, strong innovation ecosystem, and investments in circular, low-precious-metal catalyst technologies position Europe among the fastest-growing emission control markets between 2026 and 2033.

Asia Pacific Emission Control Systems Market Trends and Insights

Asia Pacific is the fastest-growing regional market, projected to expand at 4.8% CAGR between 2026 and 2033, supported by accelerating environmental regulation, urbanization, and industrial output. China, producing nearly 30% of global vehicles, is a core demand center, supported by enforcement of China VI standards and decommissioning of older high-emission vehicles, boosting uptake of catalytic converters and SCR systems. India’s automotive sector is growing 7-8% annually, with Bharat Stage VI norms and the National Clean Air Programme driving investments in industrial SOx/NOx control and waste incineration systems.

Japan and South Korea maintain mature markets with high penetration of fabric filters and scrubbers across semiconductor, waste-to-energy, and chemical processing. ASEAN economies including Vietnam, Thailand, and Indonesia show rising adoption, supported by tightening compliance frameworks, rapid power capacity additions, and industrialization-led increases in stationary emissions control requirements.

Competitive Landscape

The emission control systems market displays a moderately consolidated competitive structure, with a limited number of large multinational suppliers supported by extensive R&D capabilities, global manufacturing footprints, and long-term supply agreements with automotive and industrial OEMs. These players focus on sustained technological leadership, including advancements in catalyst formulations, digital exhaust monitoring, and integrated system architectures that improve efficiency and regulatory compliance. Alongside them, a wide base of regional manufacturers and niche technology firms competes in localized markets, often emphasizing cost-competitive solutions or application specialization.

Competitive strategies increasingly revolve around vertical integration, backward linkages for raw materials security, and capacity expansion in high-growth emerging economies. Mergers, acquisitions, and technology licensing remain prevalent as firms strengthen product portfolios and secure access to proprietary designs. Participants are also prioritizing sustainability initiatives, particularly precious-metal recovery and circular material flows, while collaborating closely with OEMs and regulatory bodies to co-develop systems aligned with tightening emissions standards across transportation and stationary industrial applications.

Key Market Developments

- November 2025: Mitsubishi Heavy Industries announced completion of successful combustion testing for ammonia single-fuel burners capable of complete stable combustion with reduced nitrogen oxide emissions relative to coal firing, positioning the company for significant opportunities in the emerging clean ammonia fuel combustion market.

- June 2025: United States Environmental Protection Agency finalized updated emissions standards for commercial and industrial solid waste incineration units, introducing stricter controls on fine particulate matter and regulated pollutants including carbon monoxide and nitrogen oxides, effective December 29, 2025, creating substantial retrofit and new installation opportunities.

- December 2024: US EPA agreed to delay the final update of air pollution regulations for large municipal waste combustors until December 22, 2025, providing clarity to facility operators regarding upcoming compliance requirements and creating opportunities for emission control system providers to develop compliant solutions.

Companies Covered in Emission Control Systems Market

- DuPont de Nemours Inc.

- Tenneco Inc.

- GEA Group Aktiengesellschaft

- MAN

- Cummins Inc.

- Faurecia SE

- Denso Corporation

- Mitsubishi Heavy Industries Group

- Nett Technologies Inc.

- Anguil Environmental Systems Inc.

- DCL International Inc.

- Catalytic Products International

- Thermax Global Limited

- Ducon Technologies Inc.

- Bosal Group

- Johnson Matthey

- BASF SE

- Umicore

- Eberspächer

- Magna International

- Marelli Holdings Co. Ltd.

- Delphi Technologies

- Yutaka Giken Co. Ltd.

- Corning Incorporated

- Continental AG

Frequently Asked Questions

The emission control systems market is projected to reach approximately US$ 31.7 billion in 2026.

Demand is driven mainly by stringent emission regulations, rapid industrialization, and rising air pollution concerns.

North America is expected to hold the largest share, accounting for around 38% of the market.

Major opportunities lie in retrofit installations, tightening industrial emission norms, and new regulatory mandates.