- Automotive Components & Materials

- Diesel Particulate Filter (DPF) Cleaner Market

Diesel Particulate Filter (DPF) Cleaner Market Size, Share, and Growth Forecast, 2026 - 2033

Diesel Particulate Filter (DPF) Cleaner Market by Material Type (Silicon Carbide, Ceramic Fiber, Others), Vehicle Type (Passenger Vehicles, Commercial Vehicles, Others), Sales Channel (Original Equipment Manufacturers (OEMs), Aftermarket), and Regional Analysis for 2026 - 2033

Diesel Particulate Filter (DPF) Cleaner Market Share and Trends Analysis

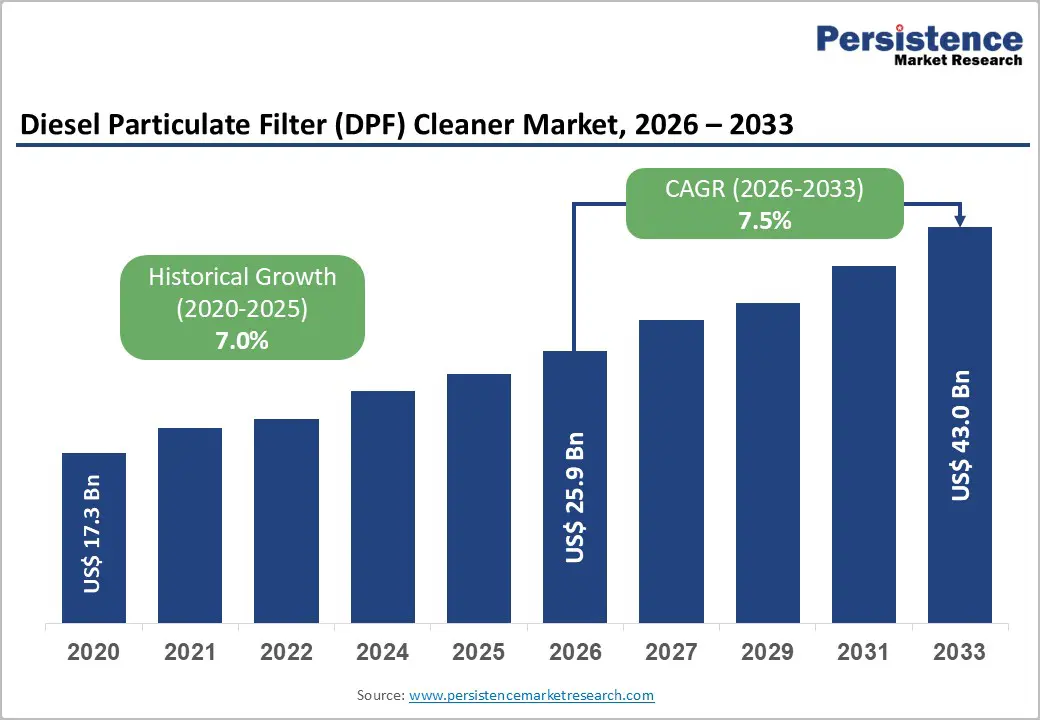

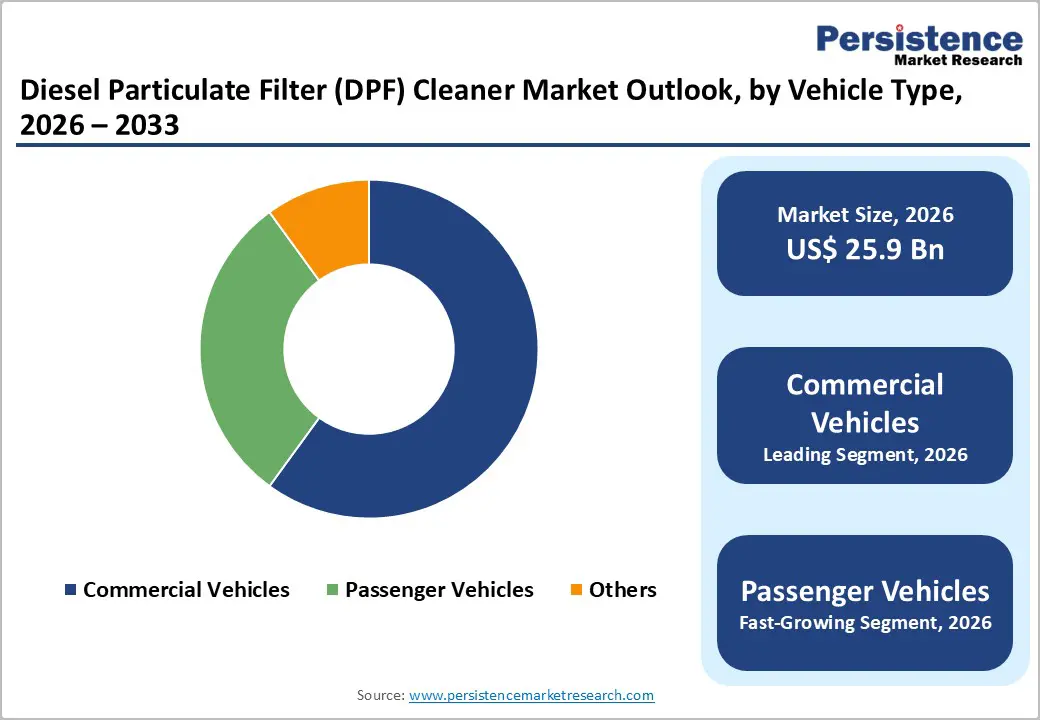

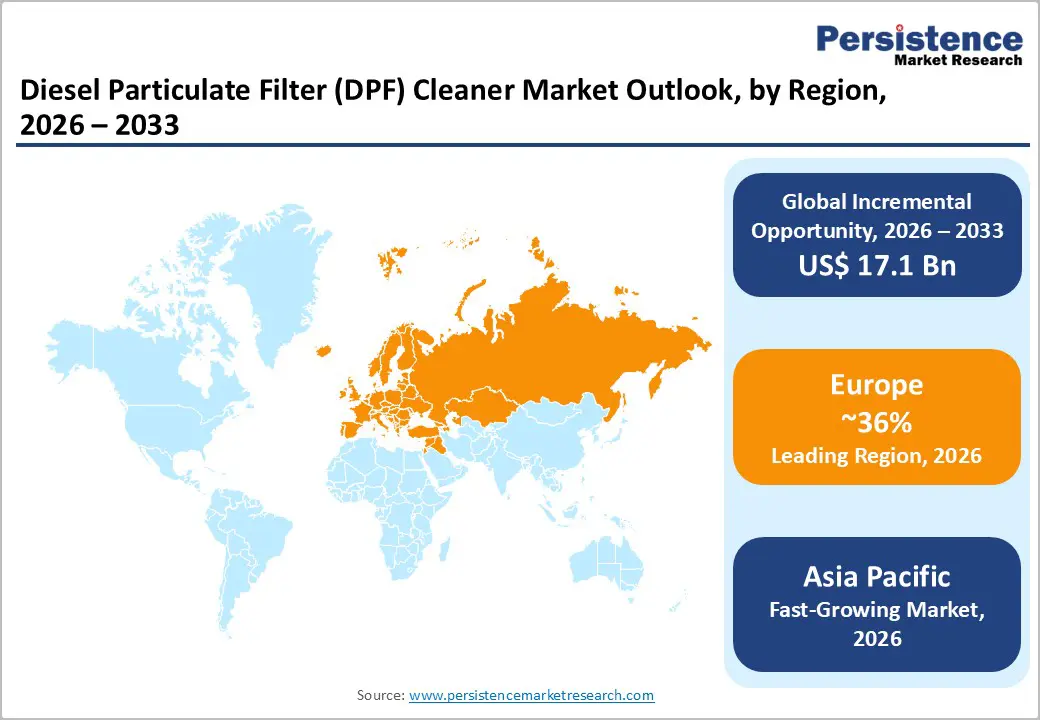

The global diesel particulate filter (DPF) cleaner market size is likely to be valued at US$ 25.9 billion in 2026, and is projected to reach US$ 43.0 billion by 2033, growing at a CAGR of 7.5% during the forecast period 2026-2033. This forecast reflects the systematic expansion of emission-control maintenance solutions driven by stringent global emission standards, rising diesel-vehicle fleets, and heightened awareness of vehicle performance longevity.

The market expansion is anchored on regulatory mandates, increasing diesel vehicle penetration in emerging economies, and heightened fleet maintenance priorities in commercial transport. The ongoing implementation of advanced cleaning technologies and the growth of aftermarket service networks continue to drive steady demand. Markets with stringent environmental regulations and dense populations of diesel vehicles are experiencing particularly robust adoption rates.

Key Industry Highlights

- Dominant Material Type: Silicon carbide is projected to account for approximately 36% of the market value in 2026, while ceramic fiber is likely to be the fastest-growing segment, with a CAGR of 8.1% through 2033, driven by its lightweight properties.

- Vehicle Type Trends: Commercial vehicles are expected to hold around 60% share in 2026, whereas passenger vehicles are set to grow fastest with a CAGR of 7.9% during 2026–2033, supported by a large population of legacy diesel cars.

- Sales Channel Dynamics: The aftermarket segment is anticipated to lead with an estimated 47% share in 2026, while OEM channels are projected to expand fastest at a CAGR of 8.3% through 2033, owing to integrated service programs and factory-recommended maintenance.

- Regional Leadership: Europe is poised to lead with an estimated market share of 36% in 2026, while Asia Pacific is projected to be the fastest-growing market, with a 2026-2033 CAGR of 9.2%, fueled by emerging fleet growth and stricter emission norms.

- November 2025: Ford announced that its 2026 Ford F-150 will feature a gasoline particulate filter on popular trims, aligning with stricter emissions standards while potentially impacting exhaust sound and maintenance considerations.

| Key Insights | Details |

|---|---|

|

Diesel Particulate Filter Cleaner Market Size (2026E) |

US$ 25.9 Bn |

|

Market Value Forecast (2033F) |

US$ 43.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Intensifying Stringency of Emission Compliance Norms

The strengthening of on-road and in-use emission compliance checks across major automotive markets has led to a measurable increase in demand for diesel particulate filter cleaning services. Several European cities expanded real-world emission checks and roadside inspections, where partially clogged DPFs led to immediate non-compliance notices for commercial vehicles operating under Euro VI norms. Similarly, under Bharat Stage VI enforcement in India, fleet operators faced registration and permit risks when onboard diagnostics detected abnormal backpressure due to soot accumulation. These developments have made periodic DPF cleaning a mandatory operational step rather than a preventive maintenance step, driving steady demand across both OEM-authorized service networks and independent aftermarket providers.

Vehicle operators are increasingly prioritizing cost control and asset utilization, strengthening the preference for professional DPF cleaning over full filter replacement. Replacing a clogged DPF involves high capital expense and extended vehicle downtime, whereas cleaning restores filtration performance at a significantly lower cost. The adoption of durable cleaning materials, such as silicon carbide and ceramic fiber, allows filters to withstand multiple service cycles without loss of efficiency. This practical focus on minimizing maintenance disruption while extending component life has positioned DPF cleaning as a core operational strategy across commercial transport, public transit, and other high-usage diesel applications.

High Entry Barriers and Structural Decline in Diesel Passenger Vehicles

Significant setup and compliance requirements constrain the adoption of professional diesel particulate filter cleaning solutions. Capital investment in advanced cleaning systems can exceed US$100,000 per facility, limiting adoption among small workshops, particularly in developing regions. Beyond equipment costs, service providers must invest in certified materials, technician training, and process standardization to meet regulatory and OEM-aligned service expectations. These structural barriers slow the formalization and geographic expansion of organized DPF cleaning services, especially in price-sensitive markets where informal maintenance practices are still prevalent.

Against this backdrop, long-term demand visibility is affected by the gradual contraction in diesel passenger vehicle usage. According to the International Energy Agency (IEA), diesel passenger vehicle sales in Europe declined by over 35% between 2018 and 2023, driven by electrification policies and urban diesel restrictions. This shift reduces the addressable market for DPF cleaning in passenger applications over time. While commercial and high-utilization diesel segments continue to support demand, the declining passenger base constrains volume growth and forces market participants to increasingly rely on commercial vehicles and aftermarket services to sustain revenue.

Expansion of Aftermarket Networks and OEM-Integrated Service Models

The opportunities in the diesel particulate filter cleaner market are broadening due to tighter in-use emission enforcement and urban air-quality initiatives. A clear example emerged in 2025 in Bangkok, where authorities introduced stricter limits on exhaust smoke from diesel vehicles as part of a broader climate and pollution-control strategy. Under the revised norms, diesel vehicles exceeding lowered opacity thresholds face penalties and operational restrictions. Such measures shift the focus from one-time compliance to continuous emissions performance, encouraging vehicle operators to adopt regular DPF cleaning as a practical and compliant maintenance solution rather than risking fines or service disruption.

This regulatory environment is accelerating the evolution of structured aftermarket and OEM-aligned service ecosystems. Vehicle operators increasingly prefer authorized or certified cleaning programs that ensure regulatory compliance while preserving aftertreatment system integrity. OEMs and service partners are responding by embedding DPF cleaning into scheduled maintenance contracts and warranty-linked service offerings. These stricter urban emission controls and the formalization of service frameworks are transforming DPF cleaning into a repeatable, policy-supported opportunity, particularly in high-density cities and regions prioritizing air-quality improvement.

Category-Wise Analysis

Material Type Insights

Silicon carbide is expected to lead the DPF cleaner market revenue at roughly 38% in 2026 due to the high thermal resistance, durability, and ability of the material to endure repeated regeneration cycles. Its performance under high exhaust temperatures and heavy particulate loads makes it ideal for trucks, buses, and other intensive-duty vehicles. Independent tests show silicon carbide maintains over 95% filtration efficiency after multiple cycles, enhancing filter longevity and lowering lifecycle costs for operators. Increasing emission compliance in high-usage segments reinforces its dominance in commercial applications.

Ceramic fiber is poised to be the fastest-growing material, with an approximate CAGR of 8.1% between 2026 and 2033, driven by its lightweight design, lower production complexity, and suitability for compact filters in passenger and light commercial vehicles. Advances in thermal stability and particulate capture efficiency make it competitive with traditional substrates. Its adoption is strongest in urban regions with strict emissions monitoring, where cost-efficient, lightweight solutions are favored. The combination of operational performance and regulatory readiness supports rising uptake in Europe and Asia.

Vehicle Type Insights

Commercial vehicles are expected to dominate in 2026, accounting for nearly 60% of the diesel particulate filter cleaner market revenue share. High utilization and continuous operation of these vehicles accelerate soot accumulation, making regular DPF cleaning essential for emission compliance, fuel efficiency, and engine performance. Scheduled maintenance is increasingly routine, with examples such as Indian state transport authorities implementing organized DPF cleaning for interstate bus fleets to meet Bharat Stage-VI standards. Regulatory oversight and operational intensity sustain consistent demand in this segment.

Passenger vehicles are expected to be the fastest-growing segment, with a CAGR of around 7.9% through 2033, driven by the widespread presence of legacy diesel cars across Europe and Asia that require periodic maintenance. Concerns about urban air quality and stricter local emission rules drive DPF servicing among private vehicle owners. Technological improvements in compact DPFs and cost-efficient cleaning methods for smaller engines facilitate broader adoption. Off-highway and industrial vehicles maintain a stable demand tied to heavy-duty usage and compliance standards.

Sales Channel

The aftermarket is slated to remain the leading sales channel, accounting for over 47% of the revenue share in 2026. Its leadership is bolstered by a broad network of regional service providers, independent garages, franchise chains, and mobile cleaning operators capable of servicing diverse diesel fleets. Operators often choose aftermarket cleaning due to cost efficiency, faster turnaround, and accessibility, especially in regions where OEM service centers are less prevalent. Local emission testing programs such as enhanced roadside compliance checks implemented across several Southeast Asian and Middle Eastern transport corridors have increased the frequency of required maintenance, further strengthening demand for aftermarket services. These inspection initiatives encourage timely filter servicing, which aftermarket providers are well-positioned to deliver.

The original equipment manufacturer channel is predicted to be the fastest-growing, at an approximate 8.3% CAGR from 2026 to 2033, as OEMs incorporate certified cleaning solutions into authorized service schedules and extended warranty offerings. This approach reinforces customer confidence by aligning cleaning protocols with vehicle design specifications and regulatory requirements. OEM service packages often include scheduled DPF cleaning at defined mileage intervals, providing structured maintenance planning and improved long-term emission performance. Manufacturers also leverage digital service reminders and integrated diagnostic support to enhance adherence to compliance. The rising prominence of OEM channels reflects a broader industry shift toward formalized maintenance ecosystems.

Regional Market Insights

North America Diesel Particulate Filter (DPF) Cleaner Market Trends

The North America DPF cleaner market growth is primarily driven by the U.S. commercial trucking sector, which, with over 3.5 million trucks, sustains strong demand under the Tier 4 particulate emission standards of the Environmental Protection Agency (EPA). Extensive fleet utilization and robust maintenance infrastructure support the widespread adoption of professional DPF services. Regulatory enforcement ensures compliance, making periodic cleaning a critical operational practice. Technological focus is shifting toward automated cleaning systems and AI-enabled diagnostic tools, enhancing efficiency and reducing downtime. Investments increasingly target mobile cleaning solutions, providing convenient access for dispersed fleets. The strong alignment of regulations, vehicle density, and service capabilities maintains North America’s leading position in the global market.

The OEM-certified programs are gaining traction, particularly among larger fleet operators who prefer structured service schedules for warranty compliance. Regional competition is driven by service quality, turnaround speed, and technological integration. Urban delivery networks and long-haul trucking operations are prioritizing preventive maintenance to minimize operational disruptions. The aftermarket and OEM channels complement each other, with OEMs providing certified solutions and aftermarket providers offering flexible access to smaller operators. Continuous innovation in cleaning materials and processes reinforces the reliability of DPF systems. North America’s mature regulatory framework and advanced infrastructure underpin sustained market stability and moderate growth.

Europe Diesel Particulate Filter (DPF) Cleaner Market Trends

Europe is expected to capture nearly 36% of the diesel particulate filter cleaner market share in 2026, led by Germany, the U.K., France, and Spain, where harmonized Euro VI emission standards ensure consistent demand. Germany continues to advance OEM-certified DPF programs for heavy-duty trucks. At the same time, France recently launched a nationwide urban diesel emission inspection initiative for city buses and light commercial vehicles, emphasizing real-time particulate monitoring. Urban low-emission zones in multiple European cities have accelerated the adoption of professional cleaning services. Competitive intensity remains high, with a strong focus on energy-efficient cleaning technologies, transparency in emission reporting, and fleet optimization strategies. Regulatory oversight and urban air quality targets continue to reinforce service adoption across both passenger and commercial diesel fleets. These developments highlight Europe’s structured approach to combining compliance with operational efficiency.

Aftermarket services dominate in dense metropolitan regions, whereas OEM-certified programs are more prominent in commercial fleets requiring warranty-backed maintenance. Investments focus on advanced cleaning equipment, technician training, and digital service management to optimize performance and regulatory compliance. Continuous technological improvements in filter materials and regeneration processes improve durability and reduce service frequency. European operators increasingly integrate DPF cleaning into preventive maintenance schedules. The strong regulatory framework, well-established service networks, and effective operational practices continue to support its market leadership and drive consistent growth across the region.

Asia Pacific Diesel Particulate Filter Cleaner Market Trends

Asia Pacific is projected to be the fastest-growing regional market for DPF cleaners, with a projected 2026-2033 CAGR of 9.2%, driven by China, India, and Japan. The large diesel vehicle populations and tightening emission norms have accelerated DPF adoption in commercial and passenger segments. In China, municipal transport authorities implemented mandatory in-use DPF checks for urban buses to ensure compliance with stricter PM2.5 emission limits. Emerging ASEAN countries, including Indonesia and Vietnam, show growing uptake due to expanding logistics, mining, and construction sectors. The lower manufacturing costs and improved service infrastructure enhance regional competitiveness. Rapid urbanization and industrial growth further elevate demand for reliable DPF maintenance solutions. These factors establish Asia Pacific as the global market’s fastest-expanding region.

Commercial and light commercial vehicles are the primary drivers of demand, with operators prioritizing maintenance strategies that ensure emission compliance and operational efficiency. OEM-certified service programs are gradually introduced to complement aftermarket coverage in high-density urban corridors. Investments focus on mobile cleaning units, technician training, and process standardization, enabling rapid scaling of DPF services. Innovation emphasizes cost-effective cleaning processes and durable substrates for high-utilization vehicles. The growth trajectory of the Asia Pacific DPF cleaner market demonstrates the region’s strategic importance in DPF cleaning services, balancing regulatory enforcement with accessible service infrastructure.

Competitive Landscape

The global diesel particulate filter cleaner market has been demonstrating a moderately consolidated structure, led by prominent organizations such as Bosch, Cummins Inc., Tenneco Inc., Faurecia SE, and Donaldson Company Inc. These firms have been securing substantial revenue shares through enduring partnerships with OEMs, deep regulatory knowledge, and comprehensive service ecosystems. Heavy investments in research and development have been targeting cutting-edge cleaning methods, resilient substrate compositions, and automated regeneration mechanisms to deliver superior performance, extended lifespan, and adherence to tightening emission regulations. Industry observers will have noted how such strategic focus enables these leaders to command pricing authority while preempting compliance shifts across major automotive regions.

Regional specialists including Hengst GmbH & Co. KG, MAHLE GmbH, and WABCO Holdings Inc. have been carving positions through targeted solutions for aftermarket demands and bespoke applications. Formidable barriers comprising certification mandates, specialized machinery needs, and regulatory hurdles have been shielding incumbents from disruptive entrants. Innovations such as portable cleaning stations and OEM-endorsed maintenance protocols have been empowering smaller operators to seize segment-specific growth. Market leaders pursuing geographic expansion and collaborative technology alliances will have accelerated consolidation trends, creating pathways for sustained differentiation amid rising electrification pressures and sustainability imperatives.

Key Industry Developments

- In November 2025, Marelli won the Society of Automotive Engineers (SAE) Innovations in Lightweighting Award for its LeanExhaust platform, a compact exhaust system for internal combustion engine (ICE) vehicles. It delivers 16 kilograms of weight reduction, 52% lower carbon emissions during production, and 85 kilograms of CO2 savings per vehicle through dual-layer converters and micro-hole mufflers, eliminating non-recyclable materials.

- In June 2025, Lubrizol launched MF9145V, a diesel additive specifically engineered for China's diverse driving conditions that reduces diesel particulate matter formation at the source, cutting DPF regeneration frequency by 25%, improving system flow efficiency by 28%, and enhancing fuel economy while minimizing operational downtime.

- In January 2025, the DieselWise Indiana program announced $750,000 in DERA funding for clean diesel projects, including DPF retrofits. The initiative targets fleets in high-pollution areas, promoting emission reductions and accelerating the adoption of retrofit DPF and exhaust technologies.

Companies Covered in Diesel Particulate Filter (DPF) Cleaner Market

- Robert Bosch GmbH

- Tenneco Inc.

- FORVIA

- Eberspächer Group

- Donaldson Company

- Clean Diesel Specialists

- Dinex Group

- HJS Emission Technology

- Mann+Hummel

- Cummins Inc.

- BASF SE

- Blue Devil Products

Frequently Asked Questions

The global diesel particulate filter (DPF) cleaner market size is projected to reach US$ 25.9 billion in 2026.

The key market drivers are increasingly stringent emission regulations, widespread deployment of commercial diesel vehicles, introduction of advanced cleaning technologies, and cost-efficient maintenance strategies favoring cleaning over replacement.

The market is poised to witness a CAGR of 7.5% between 2026 and 2033.

Major opportunities include the expansion of aftermarket cleaning services and the growth of OEM-certified cleaning programs integrated into vehicle maintenance packages.

Bosch, DENSO, Marelli, NGK Insulators, Continental, and Tenneco, among others, are some of the key players in the market.