- Oil & Gas

- Cryogenic Storage Tanks Market

Cryogenic Storage Tanks Market Size, Share, and Growth Forecast, 2026-2033

Cryogenic Storage Tanks Market by Raw Material (Steel, Nickel Alloy, Aluminum Alloy, Others), Cryogenic Liquid (LNG, LPG, Nitrogen, Oxygen, Argon, Others), End-Use (Food Freezing, De-Flashing Plastic/Rubber, Preserve Biological Sample, Metal Treating, Pulverization, Others), and Regional Analysis for 2026-2033

Cryogenic Storage Tanks Market Share and Trends Analysis

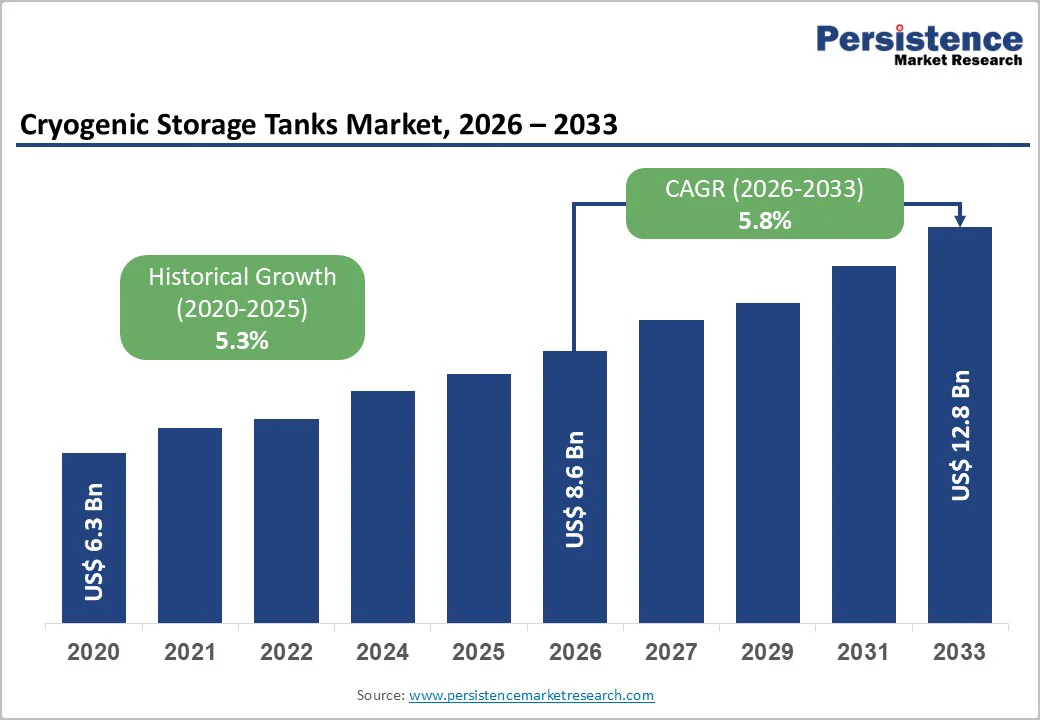

The global cryogenic storage tanks market size is likely to be valued at US$ 8.6 billion in 2026, and is projected to reach US$ 12.8 billion by 2033, growing at a CAGR of 5.8% during the forecast period 2026-2033. Liquefied natural gas (LNG) infrastructure buildout has created substantial equipment requirements for advanced storage solutions across the supply chain. Core sectors are increasingly relying on contained gases for precision manufacturing and process control. For example, healthcare facilities require reliable vessels for medical gases such as oxygen and nitrogen, while hydrogen economy projects depend heavily on cryogenic solutions for fuel storage and distribution. Material science breakthroughs and insulation system improvements enhance tank efficiency, durability, and safety profiles. Organizations across the value chain should align their strategies with these dynamics, with manufacturers channeling R&D investments in hydrogen-ready designs and investors targeting opportunities in Asia Pacific.

Key Industry Highlights

- Dominant Liquid: LNG is projected to lead with approximately 45% share in 2026, while liquid nitrogen is expected to grow the fastest at 7% CAGR through 2033, driven by industrial, healthcare, and food freezing applications.

- Leading Raw Material: Steel is anticipated to hold nearly 50% in 2026 due to its structural reliability and cost efficiency, whereas aluminum alloy is likely to be the fastest-growing material at 8% CAGR through 2033, reflecting strong demand for lightweight, corrosion-resistant cryogenic tanks.

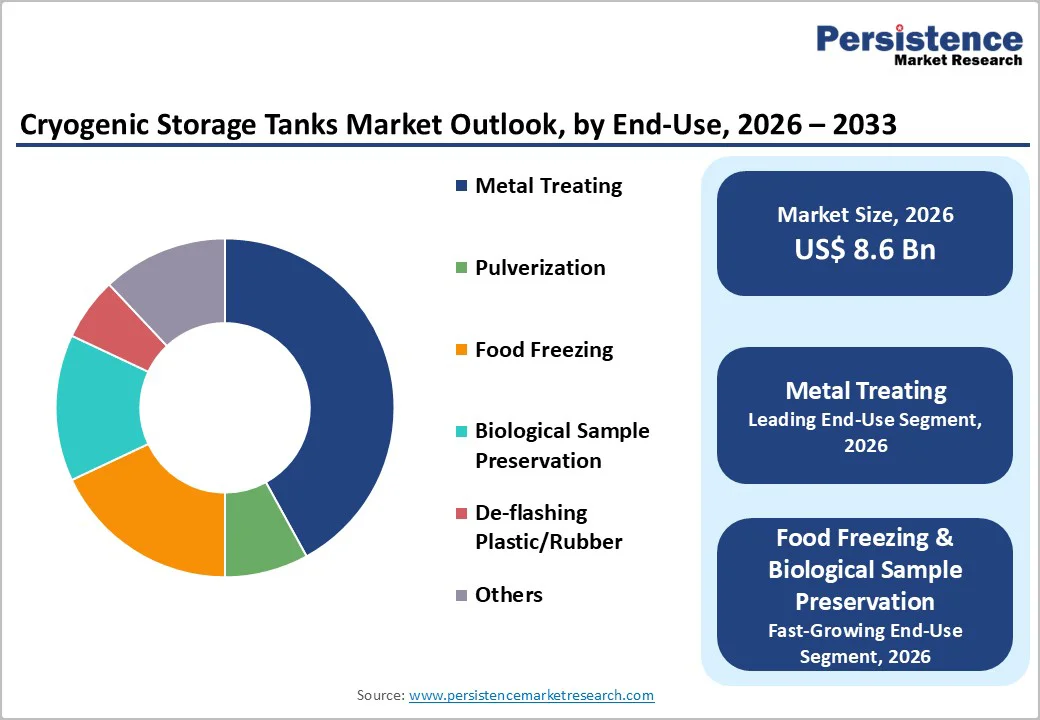

- Dominant End-Use: Metal treating segment is likely to lead with 42% share in 2026, driven by metallurgy and cryogenic grinding.

- Fastest-growing End-Use: Food freezing and biological preservation are projected to exhibit the highest 2026-2033 CAGR of about 6%, boosted by cold-chain expansion and biopharma demand.

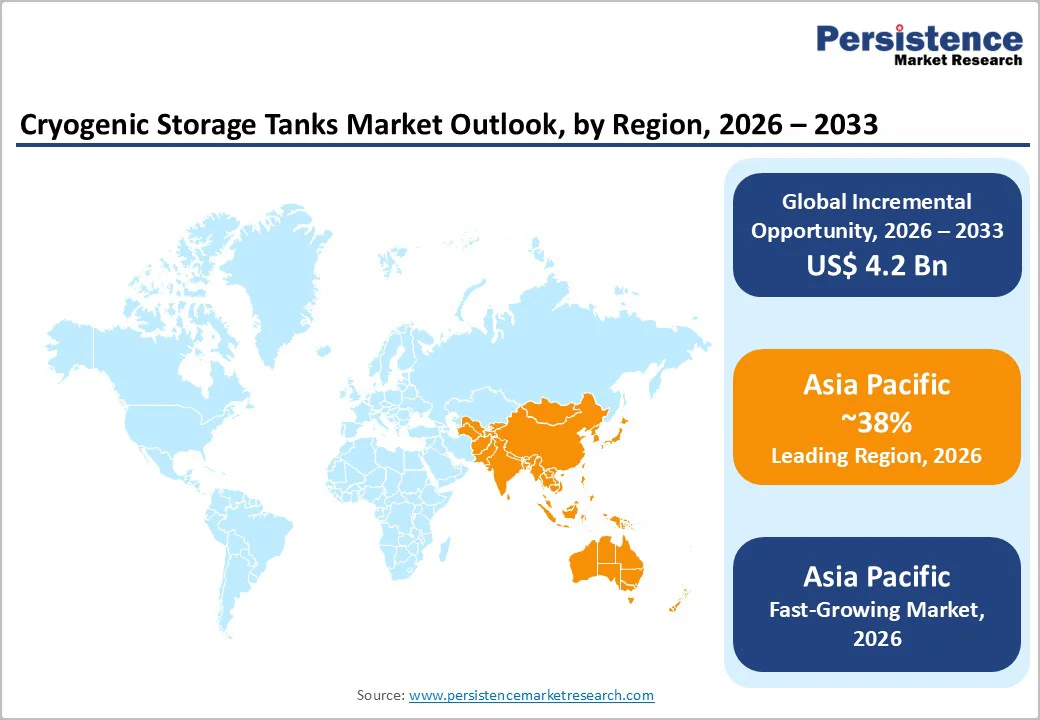

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 38% share in 2026 and register the fastest CAGR 8% through 2033, driven by rapid industrialization and supportive clean energy policies.

- Competitive Environment: Strategic developments include product innovations in hydrogen storage and IoT-enabled cryogenic solutions, as well as mergers and geographic expansions.

- January 2025: Lloyd’s Register, along with KR, DNV, and ABS, granted Approval in Principle (AiP) to HD Korea Shipbuilding & Offshore Engineering for a vacuum-insulated, large-scale liquid hydrogen tank system.

| Key Insights | Details |

|---|---|

| Cryogenic Storage Tanks Market Size (2026E) | US$ 8.6 Bn |

| Market Value Forecast (2033F) | US$ 12.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Energy Infrastructure Growth and Policy Support Catalyzing Cryogenic Storage Demand

The cryogenic storage tanks market growth is anticipated to receive strong momentum from government-led clean energy initiatives, particularly in the hydrogen and LNG sectors. India’s National Green Hydrogen Mission, for example, has an initial total outlay of INR 19,744 crore (approximately US$ 2.4 billion) until the 2029-30 fiscal year to build a comprehensive green hydrogen ecosystem. The funding supports infrastructure development, storage technologies, and pilot projects for transport and distribution, directly increasing the demand for cryogenic tanks capable of safely storing ultra-low temperature hydrogen. Similar investments in LNG terminals and industrial gas storage across Asia Pacific are reinforcing the adoption of large-scale cryogenic storage systems for energy and industrial applications.

Private and public sector collaborations have expanded hydrogen and LNG storage capacity, such as planned electrolyzer and hydrogen production facilities backed with multi-million-dollar capital deployments, reflecting broader commitment to decarbonization and secure energy supply chains. India’s green hydrogen production projects with integrated storage and transport infrastructure signal growing industrial reliance on cryogenic systems for temperature-critical applications. For example, in July 2025, Andhra Pradesh announced plans to establish India's largest green hydrogen ecosystem in Amaravati by 2030, partnering with industry and academia for production and derivatives. Key targets include 5 GW electrolyzer capacity and 1.5 MMTPA hydrogen production by 2029, plus INR 500 crore for 50 startups and local manufacturing of 60% components.

Escalating Compliance Requirements and Cost Pressures Constrain Adoption

The cryogenic storage tank deployment faced escalating costs due to stricter safety and design standards. The upgrades such as thicker vacuum insulation and dual O-ring seals increased the per tank prices, while mandatory advanced leak detection and monitoring systems increased operational expenses. Lead times for stainless steel and high-grade alloys extended to 14–18 weeks, raising procurement costs and delaying project schedules. These cost pressures particularly affect small and mid-sized operators, limiting their ability to invest in new tanks. Despite rising demand from LNG, hydrogen, and industrial gas sectors, high capital and operational expenditures are restraining broader adoption, especially in emerging and cost-sensitive markets.

Alongside manufacturing cost escalation, regulatory compliance has intensified in key markets. Frameworks such as the 2025 amendment to India’s Gas Cylinders Rules now mandate stricter traceability, valve testing, and digital identification for hydrogen and cryogenic storage equipment, increasing administrative and technical overhead. Compliance with comprehensive safety protocols and international alignment requirements adds complexity and expense, particularly for small and mid-tier manufacturers seeking global market entry. These cost and regulatory hurdles are constraining broader adoption of cryogenic storage solutions in price-sensitive and emerging regions.

Energy Transition and Infrastructure Expansion Accelerating Cryogenic Storage Adoption

Asia Pacific remains the most dynamic opportunity region for cryogenic storage tanks, driven by sustained LNG infrastructure expansion and accelerating clean-energy transition policies. China continues to rank as the world’s largest LNG importer, supporting ongoing additions of LNG receiving terminals and on-site cryogenic storage to secure fuel supply for power generation and heavy industry. Across Southeast Asia, new LNG terminals and gas distribution networks are being developed to replace coal and fuel oil in electricity and industrial applications. These infrastructure shifts are directly increasing demand for large-capacity, high-integrity cryogenic tanks capable of supporting baseload energy and industrial consumption.

Beyond energy, industrial and healthcare sectors are diversifying cryogenic applications. In 2025, multiple industrial players in Asia Pacific commissioned cryogenic storage solutions supporting LNG terminals, hydrogen processing, and maritime fuel applications, demonstrating real-world market uptake. For example, INOX India deployed cryogenic tanks for LNG infrastructure and China’s CNOOC expanded its LNG storage facilities in mid-2025, underpinning tangible market expansion. As manufacturing, healthcare, and clean fuel projects proliferate, the need for scalable, high-performance cryogenic storage systems, especially for LNG, liquid hydrogen, and industrial gases, is expected to grow steadily through the forecast period.

Category-wise Analysis

Raw Material Insights

Steel is expected to remain the leading raw material, accounting for an estimated 50% of the cryogenic storage tank market revenue share in 2026, supported by its structural strength and suitability for large stationary installations. Steel continues to be the preferred material for LNG terminals and bulk industrial gas storage where long service life and compliance with pressure vessel standards are critical. In 2025, companies such as Chart Industries and McDermott International continued supplying steel-based full-containment cryogenic tanks for LNG terminals and industrial gas facilities, reinforcing steel’s dominance. These tanks are engineered to withstand extreme thermal stress while enabling large-volume storage, sustaining steel’s leadership across energy and industrial end uses.

Aluminum alloy is projected to be the fastest-growing segment, showcasing an estimated CAGR of 8% through 2033, driven by the rising demand for lighter tanks used in modular, mobile, and decentralized cryogenic applications. Aluminum alloys offer superior corrosion resistance and lower tare weight compared to steel, making them suitable for transportable liquid nitrogen and oxygen systems. These tanks are widely used in healthcare and life-science settings where ease of handling and space efficiency are critical. Aluminum’s thermal performance also supports reduced boil-off losses in smaller-scale deployments. As decentralized gas usage grows, aluminum alloy adoption continues to accelerate.

Cryogenic Liquid Insights

LNG is likely to be the dominant liquid, representing approximately 45% of cryogenic storage tank market demand in 2026. This leadership reflects continued LNG terminal development and regulatory-driven increases in reserve storage capacity. A clear example is Petronet LNG and other terminal operators expanding on-site LNG storage infrastructure in 2025 to meet higher safety and supply security requirements. LNG storage tanks require large diameters, thick insulation, and high mechanical integrity, making them the largest revenue contributors within the cryogenic liquid segment. LNG’s central role in power generation and industrial fuel switching continues to anchor its market leadership.

Liquid hydrogen is poised to be the fastest-growing cryogenic liquid, expected to grow at a CAGR of around 7% through 2033. Momentum increased in 2025 as companies such as Air Liquide and Linde advanced liquid hydrogen storage systems to support hydrogen mobility and industrial decarbonization projects. Cryogenic hydrogen storage is essential for achieving higher energy density and long-distance transport. Equipment suppliers are introducing advanced insulation and boil-off control technologies to address hydrogen’s ultra-low temperature requirements, positioning liquid hydrogen as the most rapidly expanding cryogenic liquid category.

End-Use Insights

Metal treating is expected to represent the largest end-use segment, accounting for an estimated 42% share of cryogenic storage tank demand in 2026. These applications rely heavily on liquid nitrogen for cryogenic hardening, shrink fitting, controlled cooling, and fine material pulverization across metals, minerals, and specialty chemicals. Continued expansion in automotive manufacturing, heavy engineering, and advanced materials processing sustained high consumption of bulk cryogenic liquids at industrial facilities. Cryogenic storage tanks are essential in these settings to ensure uninterrupted supply, process stability, and precise temperature control. The scale and continuity of these operations reinforce their dominance within the end-use landscape.

Food freezing and biological sample preservation form the fastest-growing end-use segment, forecast to grow at approximately 6% CAGR between 2026 and 2033. This growth is supported by rising demand for frozen and processed foods, expansion of temperature-controlled logistics, and increasing reliance on cryogenic preservation for vaccines, cell cultures, and biological samples. Investments in food processing capacity and biopharma research infrastructure increased demand for on-site liquid nitrogen storage systems. These applications require stable ultra-low temperatures and high system reliability, directly supporting adoption of dedicated cryogenic storage tanks. As regulatory standards for food safety and biological integrity tighten, cryogenic storage becomes increasingly critical.

Regional Insights

North America Cryogenic Storage Tanks Market Trends

North America represents a mature and technology-intensive market, supported by its role as a major LNG exporter and a well-established industrial gas ecosystem. The U.S. Federal Energy Regulatory Commission (FERC) has been approving multiple LNG terminal expansions along the Gulf Coast, directly increasing the demand for large-scale cryogenic storage tanks at export facilities. The region also benefits from sustained demand for liquid oxygen and nitrogen across metals, chemicals, and healthcare infrastructure. Regulatory oversight by ASME Boiler and Pressure Vessel Code (BPVC) and OSHA safety standards mandates high-specification tank designs. These regulations raise system costs but ensure consistent replacement and upgrade demand.

From a growth standpoint, the North America market is expected to expand at roughly 5% CAGR through 2033, reflecting infrastructure maturity rather than capacity saturation. Public funding under the U.S. Department of Energy’s hydrogen and clean fuel programs supported pilot-scale cryogenic hydrogen storage projects. Healthcare-driven oxygen storage upgrades also continued following post-pandemic preparedness mandates. Competitive intensity remains high, with suppliers focusing on engineered-to-order tanks and lifecycle service contracts. While compliance costs remain elevated, regulatory clarity supports long-term capital planning. The region prioritizes reliability and safety over rapid volume expansion.

Europe Cryogenic Storage Tanks Market Trends

Europe presents a structurally attractive environment for cryogenic storage investments, as coordinated energy security policies, environmental regulations, and common infrastructure frameworks create predictable demand conditions. LNG import terminals, high industrial gas usage in sectors such as aerospace and automotive, and the expansion of biopharmaceutical cold-chain networks together support sustained utilization of stationary storage assets. The European Union (EU) has introduced gas security rules that encourage member countries to maintain higher LNG reserves ahead of winter, which in turn promotes additional capacity at terminals and distribution hubs. For project developers and operators, it is therefore essential to align tank sizing, siting, and contracting strategies with evolving import patterns, industrial gas offtake needs, and the tightening of storage obligations across key European corridors.

The market in Europe is expected to grow steadily through 2033, supported by national hydrogen roadmaps in Germany, France, Spain, and other early adopters. Public funding programmes and green-transition subsidy schemes continue to lower risk on large capital projects, while manufacturers prioritize R&D that improves thermal performance and reduces product losses. At the same time, lengthy permitting cycles and high upfront costs can slow execution, so stakeholders should plan for phased deployments, robust stakeholder engagement, and early regulatory consultation. To capture value in this environment, suppliers and asset owners can focus on compliance-ready designs that meet the EU Pressure Equipment Directive (PED), flexible footprints that serve both LNG and emerging hydrogen demand, and long-term service models that help industrial and healthcare users manage reliability and total cost of ownership.

Asia Pacific Cryogenic Storage Tanks Market Trends

Asia Pacific stands out as the dominant and most dynamic regional market for cryogenic storage tanks, expected to capture about 38% of the cryogenic storage tanks market share in 2026. Rapid energy infrastructure projects and rising industrial gas needs fuel this leadership. New LNG import terminals, such as Taiwan’s Guantang facility near Taoyuan City set for completion in 2025, add receiving and storage capacity to diversify imports and meet surging energy requirements. Developers should prioritize scalable tank designs that integrate with these hubs, while end-users benefit from localized supply chains that cut lead times and logistics costs.

The regional market is also forecast to display the highest 2026-2033 CAGR of roughly 8%. LNG build-out continues, alongside industrialization and broader gas applications in manufacturing. Progress on Indonesia’s Abadi LNG project Front-End Engineering Design (FEED) activities in 2025 signals massive future storage demands for production scaling. Local manufacturers and original equipment manufacturers (OEMs) expand footprints to boost responsiveness. Evolving regulations speed infrastructure rollout. Stakeholders gain by targeting joint ventures for onshoring, investing in modular tanks for quick deployment, and aligning with national energy security goals to secure long-term contracts.

Competitive Landscape

The global cryogenic storage tanks market leaders, such as Linde plc, Air Liquide, INOXCVA, Chart Industries, and Messer Group, command significant revenue share through established industrial gas networks and engineering prowess. These companies deliver integrated solutions and channel investments into R&D, superior insulation materials, IoT-powered monitoring systems, and ultra-low temperature designs tailored for industrial processes, LNG, and healthcare needs. Stakeholders should evaluate partnerships with these frontrunners to access proven technologies that minimize downtime and operational risks.

Regional specialists, including Cryofab, Technovap, and SHI Cryogenics Group, have carved niches in mobile units, biopharmaceutical storage, and small-scale LNG setups. Elevated capital requirements, stringent regulatory hurdles, and intricate fabrication processes deter fresh competitors. Consolidation will accelerate via mergers, technology alliances, and production scale-ups, while smaller firms hone localized offerings. Buyers gain by diversifying suppliers for agility, prioritizing vendors with compliance certifications, and scouting emerging players for cost-effective customizations in high-growth areas such as Asia Pacific hydrogen hubs.

Key Industry Developments

- In October 2025, Tiger Logistics (India) Limited signed a Memorandum of Understanding (MoU) with H2 Invest to bring cryogenic hydrogen transport technology to India. The partnership supports emerging hydrogen supply chains and facilitates safe, large-scale distribution of liquid hydrogen, strengthening India’s readiness for clean energy adoption and hydrogen mobility.

- In August 2025, Asyad Group successfully transported a 115-ton LNG cryogenic tank from Northern India to Dammam, Saudi Arabia, over a 1,500km route combining overland and maritime segments. The operation required specialized handling, precise temperature and pressure control, and detailed engineering planning.

- In January 2025, CB&I was awarded a multi-hundred-million-dollar EPC contract by the TJN Ruwais Joint Venture to construct two 180,000m³ full-containment LNG cryogenic tanks in Abu Dhabi. The project significantly enhances Abu Dhabi’s LNG storage capacity and its position as a global gas exporter.

Companies Covered in Cryogenic Storage Tanks Market

- Chart Industries, Inc.

- Linde plc

- Air Products and Chemicals, Inc.

- INOX India Pvt. Ltd. (INOXCVA)

- Cryofab, Inc.

- Taylor‑Wharton International LLC

- Wessington Cryogenics Ltd.

- FIBA Technologies, Inc.

- Cryolor (Asia Pacific Private Ltd.)

- VRV S.p.A.

- Air Water, Inc.

- Cryoquip LLC

- Gardner Cryogenics, Inc.

- Suretank Group Ltd.

- CIMC Enric Holdings Ltd.

Frequently Asked Questions

The global cryogenic storage tanks market is projected to reach US$ 8.6 billion in 2026.

Expansion of LNG and industrial gas infrastructure, rising energy storage and hydrogen adoption, and growing biopharma and cold-chain requirements globally are key market drivers.

The market is poised to witness a CAGR of 5.8% from 2026 to 2033.

The opportunities exist in emerging markets in Asia Pacific, modular and mobile cryogenic tank adoption, hydrogen fuel storage, and healthcare/biopharma cold-chain expansion.

Chart Industries, Inc., Linde plc, Air Products and Chemicals, INOX India Pvt. Ltd. (INOXCVA), and Cryofab, Inc. are some of the key players in the market.