- Biotechnology

- COVID-19 Saliva-based Screening Market

COVID-19 Saliva-based Screening Market Size, Share, and Growth Forecast 2026 - 2033

COVID-19 Saliva-based Screening Market by Product (Saliva Collection Kits, Saliva Nucleic Acid Purification Kits, Saliva-based Detection Kits [Rapid Test Kits, PCR-based Kits]), by Technology (Direct Sample to PCR, RT-qPCR, Lateral Flow Assays), by End User (Hospitals & Clinics, Diagnostic Laboratories, Research Institutes, Home/Self-Care Users, Workplaces & Long-Term Care Facilities), by Regional Analysis, 2026-2033

COVID-19 Saliva-based Screening Market Size and Trends Analysis

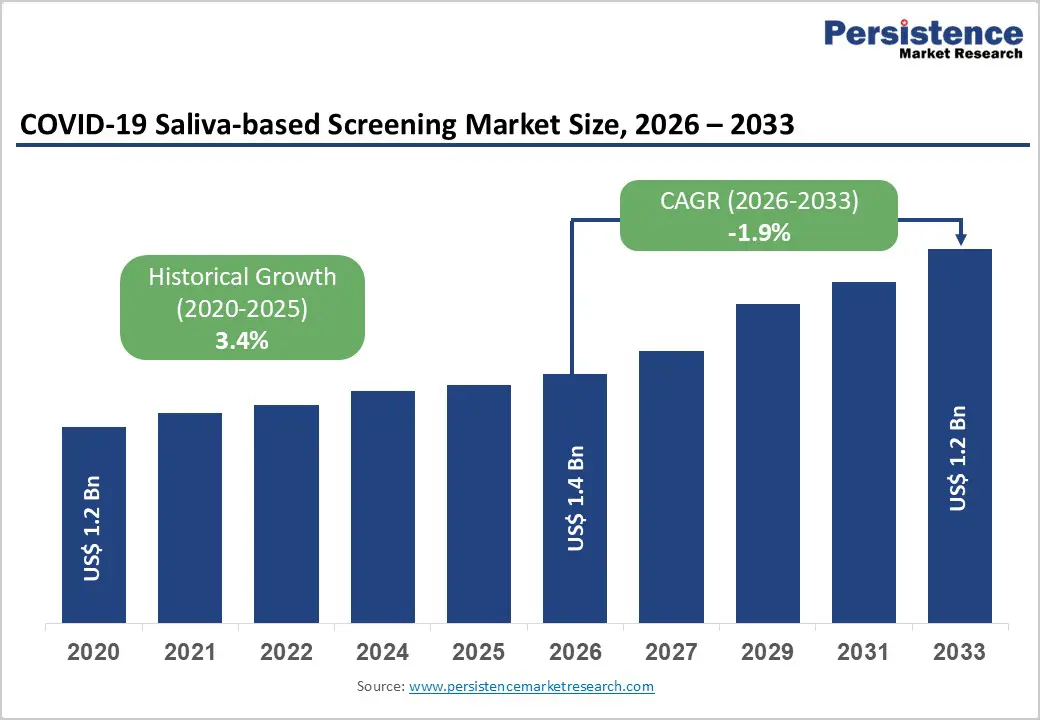

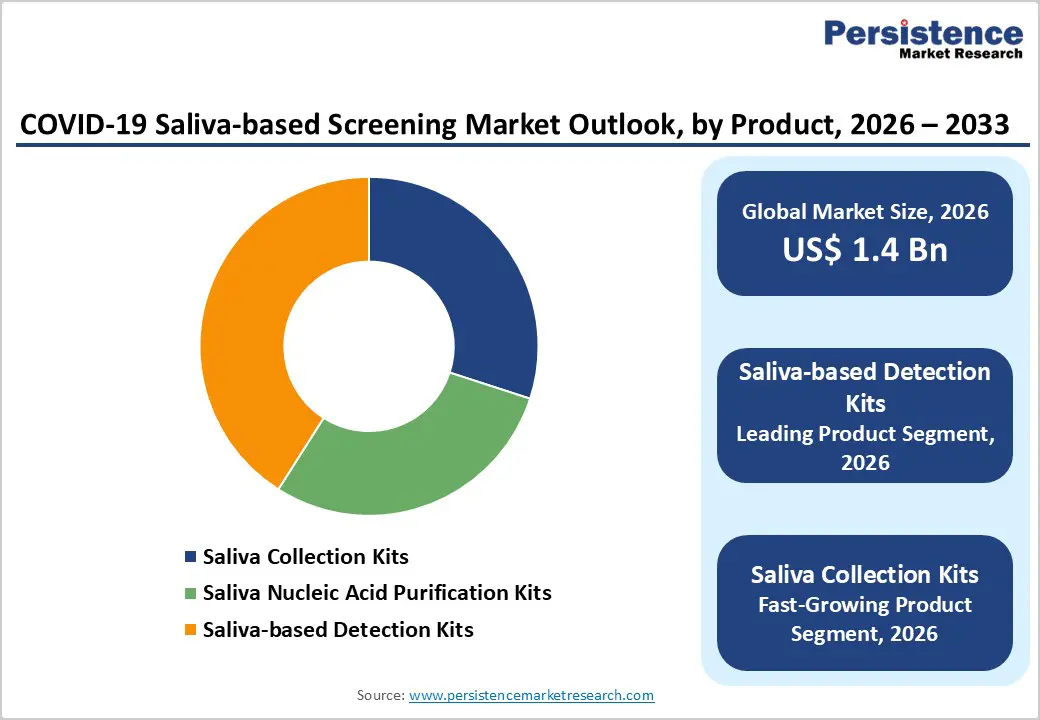

The global COVID-19 Saliva-based Screening Market is expected to be valued at US$ 1.4 billion in 2026 and projected to reach US$ 1.2 billion by 2033, declining at a CAGR of -1.9% between 2026 and 2033.

The market contraction reflects the transition from acute pandemic response to endemic disease management, characterized by reduced testing volumes and lower government procurement as immediate COVID-19 threats diminish. However, sustained demand from high-risk populations, workplace surveillance programs, and self-care initiatives continues to support market segments focused on non-invasive collection methods and rapid diagnostics.

The saliva-based screening market benefits from superior user experience and clinical advantages over nasopharyngeal swabs. According to research published in clinical microbiology journals, RT-qPCR tests using saliva specimens demonstrate sensitivity and specificity comparable to or exceeding nasopharyngeal swab-based methods, with sensitivity reaching 90% among symptomatic individuals. The FDA has authorized three saliva-based PCR tests for emergency use, including the SalivaDirect test developed by Yale School of Public Health, which enables pooling of up to five samples while maintaining clinical sensitivity equivalent to gold-standard RT-PCR testing. These regulatory approvals and clinical validations establish saliva-based screening as a credible diagnostic modality, particularly for surveillance applications in workplaces, schools, and home-based screening programs.

Key Market Highlights

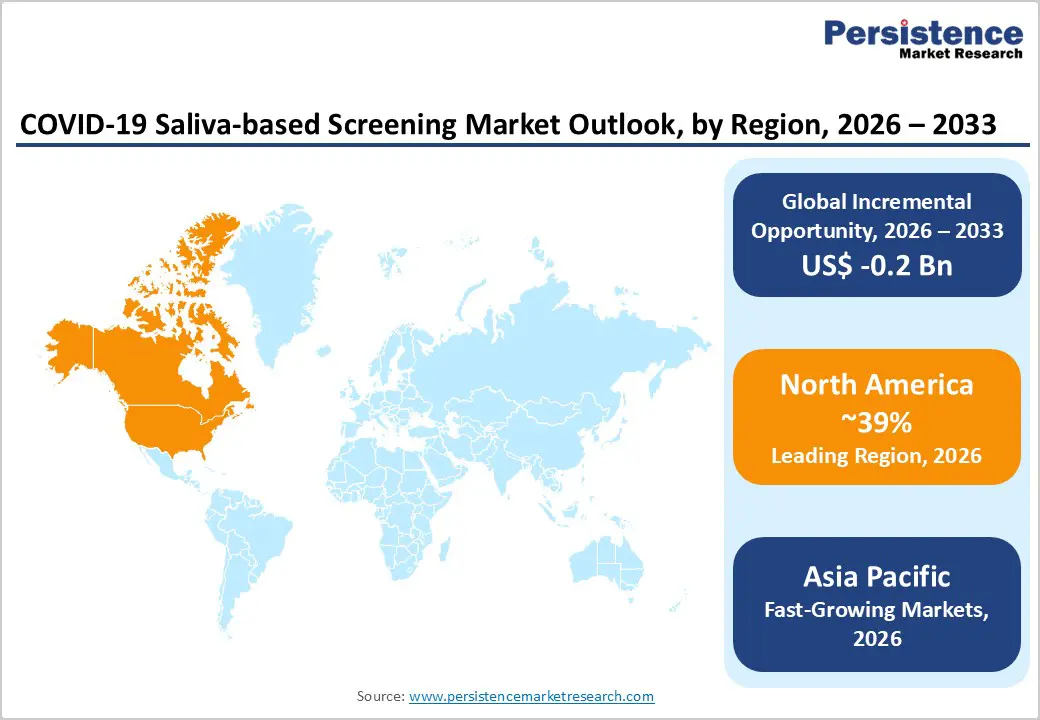

- North America maintains dominant regional position representing 39% of global saliva-based screening market share, driven by established regulatory frameworks, advanced healthcare infrastructure, and leading-edge diagnostic innovation from major manufacturers including FDA-authorized testing platforms.

- Asia Pacific emerges as fastest-growing region demonstrating significant growth potential through manufacturing industry expansion, regulatory framework evolution, and workplace-based testing program implementation across ASEAN economies and South Asian markets.

- Saliva-based Detection Kits represent dominant product segment with 41% market share, encompassing rapid test and PCR-based platforms that address diverse clinical and point-of-care requirements across diagnostic and surveillance applications.

- RT-qPCR technology leads within saliva-based screening markets supporting FDA-approved pooled testing of five samples, demonstrating analytical sensitivity of 10 copies per milliliter and sensitivity exceeding 90% among symptomatic populations.

| Global Market Attributes | Key Insights |

|---|---|

| Market Size (2026E) | US$ 1.4 billion |

| Market Value Forecast (2033F) | US$ 1.2 billion |

| Projected Growth CAGR (2026-2033) | -1.9% |

| Historical Market Growth (2020-2025) | 3.4% |

Market Dynamics

Market Growth Drivers

Shift Toward Home-Based and Workplace Screening Programs

The transition from clinical laboratory-centric testing to decentralized, home-based, and workplace screening models drives adoption of saliva-based collection kits. Self-testing strategies achieve high acceptability rates of 91%-98.7% across diverse populations, according to systematic reviews published in peer-reviewed medical literature. Implementation pilots in manufacturing industries demonstrate that 60% employee enrollment rates are achievable, with workforce participation enabling detection of community transmission and household clusters. Organizations including World Health Organization (WHO) recommend self-testing as a component of integrated COVID-19 response strategies, citing reduced healthcare system burden and empowerment of individuals for health self-management. Governments in multiple regions have integrated self-testing into workplace health policies, creating sustained procurement channels. The United States CDC reports that between August 2021 and March 2022, utilization of at-home tests increased significantly among American adults experiencing COVID-19-like symptoms, validating consumer acceptance of non-clinical testing pathways. Saliva-based collection kits address the comfort, accessibility, and compliance barriers associated with nasopharyngeal swabs, supporting expanded deployment in occupational health and community screening settings.

Superior Clinical Performance and Non-Invasive Collection Advantages

Saliva-based RT-qPCR assays offer clinical performance advantages that justify market positioning and pricing premiums. Clinical studies demonstrate that saliva specimens detect certain infections not captured by nasopharyngeal swabs, potentially reflecting superior sampling characteristics or viral load representation in oral secretions. Limit of detection for saliva-based assays reaches 10 copies per milliliter, compared to 100 copies per milliliter for nasopharyngeal specimens, suggesting enhanced sensitivity at low viral concentrations. Non-invasive collection eliminates discomfort associated with nasopharyngeal swabs, improves compliance in pediatric and sensitive populations, and reduces occupational exposure for healthcare workers and testing personnel. These clinical advantages maintain market traction despite declining testing volumes, particularly for serial screening applications requiring repeated sampling.

Market Restraints

Significant Decline in Testing Demand as COVID-19 Transitions to Endemic Phase

Pandemic-driven testing demand has substantially contracted as vaccination rates increase, population immunity strengthens, and acute COVID-19 threat perception diminishes globally. Government stockpiling programs have concluded, emergency procurement frameworks have been dismantled, and insurance reimbursement for routine COVID-19 testing has been curtailed in numerous jurisdictions. The FDA-authorized saliva-based testing market, concentrated in molecular diagnostics, experiences particular vulnerability as rapid antigen tests require high viral copy numbers and dominate point-of-care segments with lower cost structures. Reduced testing volume pressures pricing, particularly in molecular testing categories where saliva-based kits command higher per-test costs than nasal swab alternatives. Laboratory consolidation and automation investments made during pandemic peaks have excess capacity, limiting procurement of new testing kits. Organizational uncertainty regarding future pandemic severity and testing relevance discourages long-term commitments, shifting purchasing toward consumables with near-term replacement cycles rather than kit-based solutions requiring training and workflow integration.

Technical and Clinical Limitations in Performance Parameters

Saliva-based testing exhibits performance variability that constrains adoption in clinical diagnostic settings requiring maximum sensitivity. Sample collection timing, oral hygiene status, and patient factors including recent eating or drinking influence specimen quality and diagnostic accuracy. Lateral flow assays designed for saliva show sensitivity of 66.7% in certain applications, substantially lower than RT-qPCR sensitivity levels, limiting point-of-care applications requiring rapid turnaround. Clinical laboratories operating high-throughput diagnostics may prioritize nasopharyngeal swabs with established workflows and supplier relationships, delaying adoption of alternative collection methods despite acknowledged advantages. These technical limitations create regulatory and clinical barriers preventing universal displacement of conventional swab-based testing, particularly in diagnostic confirmation and clinical management pathways.

Market Opportunities

Expansion in Long-Term Care Facilities and Healthcare Worker Surveillance Programs

Long-term care facilities, including nursing homes and assisted living centers, represent a high-value market segment for saliva-based screening given infection prevention requirements and vulnerable resident populations. Regulatory agencies including PMDA have approved saliva as a specimen type for COVID-19 diagnostics, facilitating regulatory acceptance in institutional settings. Regular surveillance testing of healthcare workers, visitors, and residents requires serial sampling that imposes physical burden with conventional nasopharyngeal swabs; saliva-based methods eliminate discomfort barriers that discourage repeat testing. A 2024 study of COVID-19 self-testing in manufacturing settings demonstrated 69%-100% feasibility for serial testing implementation, with organizational adoption driven by workplace safety compliance mandates. Healthcare facilities managing long-term care residents facing infection risk can implement cost-effective saliva-based screening protocols as infection prevention measures, reducing outbreaks while maintaining operational continuity. The WHO guidance on self-testing in congregate settings explicitly mentions workplaces and healthcare facilities as prioritized deployment environments. Regulatory frameworks in multiple jurisdictions permit saliva-based diagnostics in occupational health settings, supporting procurement by large healthcare systems operating long-term care networks. As COVID-19 remains endemic, sustained surveillance in high-risk settings creates stable market demand for collection kits and detection assays, offsetting volumes lost in general population screening.

Development of Multiplex Diagnostics Combining COVID-19 with Influenza and RSV Detection

Multiplex respiratory pathogen diagnostics represent a significant growth opportunity in saliva-based testing markets. In September 2024, major manufacturers including Roche and Abbott expanded molecular testing portfolios with multiplex panels detecting COVID-19, Influenza A and B, and Respiratory Syncytial Virus (RSV) from single saliva samples, addressing clinical demand for comprehensive respiratory pathogen identification. Single-sample multiplex testing reduces operational costs, accelerates turnaround times to under four hours, and improves laboratory efficiency in high-volume settings. Clinical evidence supports multiplexed assays for emergency department triage, enabling rapid differentiation of viral illnesses during peak seasons. FDA marketing authorizations in 2024 for multiplex assays including the Hologic Panther Fusion SARS-CoV-2/Flu A/B/RSV Assay demonstrate regulatory feasibility and market validation of this approach. Saliva-based collection simplifies specimen handling in multiplex workflows compared to nasopharyngeal swabs requiring specialized transport media and processing protocols. Healthcare systems operating integrated respiratory pathogen panels can leverage existing laboratory infrastructure investments, reducing barriers to adoption. Public health agencies implementing respiratory surveillance programs utilize multiplex diagnostics for rapid pathogen identification, supporting epidemiological tracking and variant monitoring. This convergence of saliva-based collection with multiplex diagnostics creates market opportunities spanning clinical diagnostics, occupational health, and public health surveillance domains, potentially reversing market contraction in diagnostics segments integrating saliva specimens.

Category-wise Insights

Product Analysis

Saliva-based Detection Kits lead the product category with approximately 41% market share as of 2025, representing the primary revenue-generating segment within saliva-based screening markets. This dominance reflects the segment's encompassing rapid test kits and PCR-based detection platforms, addressing diverse clinical and point-of-care requirements. PCR-based detection kits command higher value per unit due to superior clinical sensitivity, supporting laboratory infrastructure and high-throughput processing environments. FDA-authorized saliva-based detection kits, including SalivaDirect and MicroGEM platforms, demonstrate validated diagnostic performance and established market presence in clinical laboratories across multiple United States regions, with deployed testing reaching over two million administered tests. Lateral flow assays within the detection kit category provide cost-effective rapid screening despite moderate sensitivity, supporting point-of-care deployments in clinics, workplaces, and home settings where turnaround time prioritization justifies reduced analytical sensitivity. The segment benefits from ongoing improvements in assay design, with manufacturers developing simplified protocols reducing sample preparation complexity and expanding applicability across laboratory settings. Saliva-based detection kits represent scalable revenue opportunities, particularly as regulatory frameworks continue accepting saliva as validated specimen type across additional diagnostic modalities and endpoints.

End User Analysis

Diagnostic Laboratories serve as a leading end-user segment, leveraging saliva-based testing capabilities to enhance operational capacity and accommodate patient preferences for non-invasive collection. Clinical laboratories processing high-volume molecular diagnostics integrate saliva-based RT-qPCR workflows with existing automation platforms, reducing marginal costs for incremental test volume. The segment benefits from established relationships with reference laboratories and accredited testing networks validating saliva-based diagnostic performance. Large diagnostic networks including Quest Diagnostics Incorporated operate national laboratory systems utilizing saliva-based testing for routine surveillance and diagnostic confirmation, providing market stability through institutional procurement patterns. Public health laboratories supporting COVID-19 surveillance programs maintain saliva-based testing capabilities aligned with epidemiological monitoring requirements and population screening mandates. Hospitals & Clinics represent secondary end-users maintaining saliva-based testing availability for patient accommodation and workflow flexibility, though concentrated testing volumes continue in laboratory facilities offering high-throughput processing infrastructure.

Regional Insights

North America COVID-19 Saliva-based Screening Market Trends and Insights

North America dominates global saliva-based screening markets with approximately 39% market share as of 2025, reflecting established regulatory frameworks, advanced healthcare infrastructure, and early technology adoption. The United States FDA has authorized three saliva-based PCR tests for COVID-19 detection, including SalivaDirect, establishing regulatory precedent for saliva specimen acceptance across diagnostic platforms. Major diagnostics manufacturers including Thermo Fisher Scientific Inc., Abbott Laboratories, Roche Diagnostics, and Hologic Inc. maintain active research and development programs advancing saliva-based multiplexed respiratory pathogen detection, with FDA approvals in 2024 for multiplex assays accelerating commercial deployment. Regional innovation ecosystems including academic medical centers at Yale University and University of California Irvine have pioneered open-source saliva-based protocols, contributing to widespread adoption and technology standardization.

Asia Pacific COVID-19 Saliva-based Screening Market Trends and Insights

Asia Pacific represents the fastest-growing region for saliva-based screening, driven by manufacturing capacity development, rising healthcare investments, and regulatory framework evolution across major economies. Japan's PMDA has authorized saliva as a specimen type for COVID-19 diagnostics, facilitating regulatory acceptance and market expansion across Japanese healthcare and occupational settings. China's regulatory authorities have approved multiple saliva-based diagnostic platforms, supporting both domestic consumption and regional distribution through multinational diagnostics manufacturers. India's healthcare systems are increasingly implementing workplace and community-based testing programs incorporating saliva-based methodologies, addressing occupational health requirements and population screening initiatives.

Implementation pilot studies conducted in Malaysia and South-East Asian manufacturing industries demonstrate feasibility of workplace-based self-testing programs, with over 60% employee enrollment rates and subsequent household member participation supporting transmission prevention and family safety. These implementation experiences establish operational models for expanding saliva-based testing infrastructure across the region. Manufacturing and export-oriented industries in multiple ASEAN member states have adopted occupational health surveillance incorporating saliva-based screening, creating sustained demand for collection kits and diagnostic platforms. Healthcare capacity development initiatives in South Asia increasingly emphasize non-invasive diagnostics compatible with varied laboratory infrastructure levels, supporting saliva-based testing as scalable solution. Regional regulatory harmonization efforts are gradually advancing, though national approval processes remain variable, requiring multinational diagnostics manufacturers to maintain country-specific submissions and compliance documentation. As COVID-19 surveillance persists and occupational health standards advance, Asia Pacific markets demonstrate strong potential for saliva-based screening adoption, potentially offsetting market contraction in mature North American and European regions.

Competitive Landscape

Market Structure Analysis

The COVID?19 saliva-based screening market is highly competitive, driven by rapid innovation in testing technologies and growing demand for non-invasive, point-of-care solutions. Companies are focusing on developing rapid, accurate, and easy-to-use tests to cater to hospitals, laboratories, workplaces, and at-home consumers. Technological advancements, such as RT-PCR, lateral flow assays, and emerging molecular methods, are intensifying market rivalry. Strategic initiatives like partnerships, collaborations, and regional expansions are common to capture market share.

Key Market Developments

- In August 2022, Penn State researchers developed an at-home, saliva-based testing platform that provided results in 45 minutes. In preliminary tests, the platform detected the COVID-causing virus with the same level of sensitivity as PCR tests.

Companies Covered in COVID-19 Saliva-based Screening Market

Thermo Fisher Scientific Inc., Abbott Laboratories, Quest Diagnostics Incorporated, F. Hoffmann-La Roche AG, Hologic Inc., PerkinElmer Inc., Quidel Corporation, Seegene Inc., ARUP Laboratories, Vatic Health Ltd., Fluidigm Corporation, DxTerity Diagnostics Inc.

Frequently Asked Questions

The global COVID-19 Saliva-based Screening Market is expected to be valued at US$ 1.4 billion in 2026.

Primary demand drivers include transition toward home-based and workplace screening programs with high acceptability rates of 91%-98.7%, superior clinical performance of saliva-based RT-qPCR assays with 90% sensitivity among symptomatic individuals, and expansion of multiplex respiratory pathogen diagnostics combining COVID-19, Influenza, and RSV detection from single saliva samples, addressing institutional laboratory efficiency requirements.

North America dominates global markets with approximately 39% market share as of 2025, reflecting FDA authorization for three saliva-based PCR tests, advanced healthcare infrastructure, active research and development by leading manufacturers, and established regulatory frameworks supporting saliva-based diagnostics deployment across clinical and occupational health settings.

Significant opportunities include expansion in long-term care facilities requiring serial surveillance testing, development of multiplex respiratory pathogen diagnostics enabling single-sample detection of COVID-19 alongside Influenza and RSV, and growth in occupational health surveillance programs , particularly in Asia Pacific manufacturing industries , demonstrating 60%+ employee enrollment rates in workplace-based self-testing initiatives.

Leading market participants include Thermo Fisher Scientific Inc., Abbott Laboratories, Roche Diagnostics, Quest Diagnostics Incorporated, Hologic Inc., PerkinElmer Inc., and Quidel Corporation, all maintaining FDA-authorized saliva-based diagnostic platforms and active research and development programs.