- HVAC

- Cleanroom Air Filter Market

Cleanroom Air Filter Market Size, Share, and Growth Forecast, 2026 – 2033

Cleanroom Air Filter Market by Product Type (HEPA Filters, ULPA Filters, Pre-Filters, Others), Application (Pharmaceutical, Biotechnology, Medical Device, Electronics & Semiconductor, Food & Beverage, Others), Filter Type (Fan Filter Units, HVAC Systems, Terminal Diffusers, Others), and Regional Analysis for 2026-2033

Cleanroom Air Filter Market Share and Trends Analysis

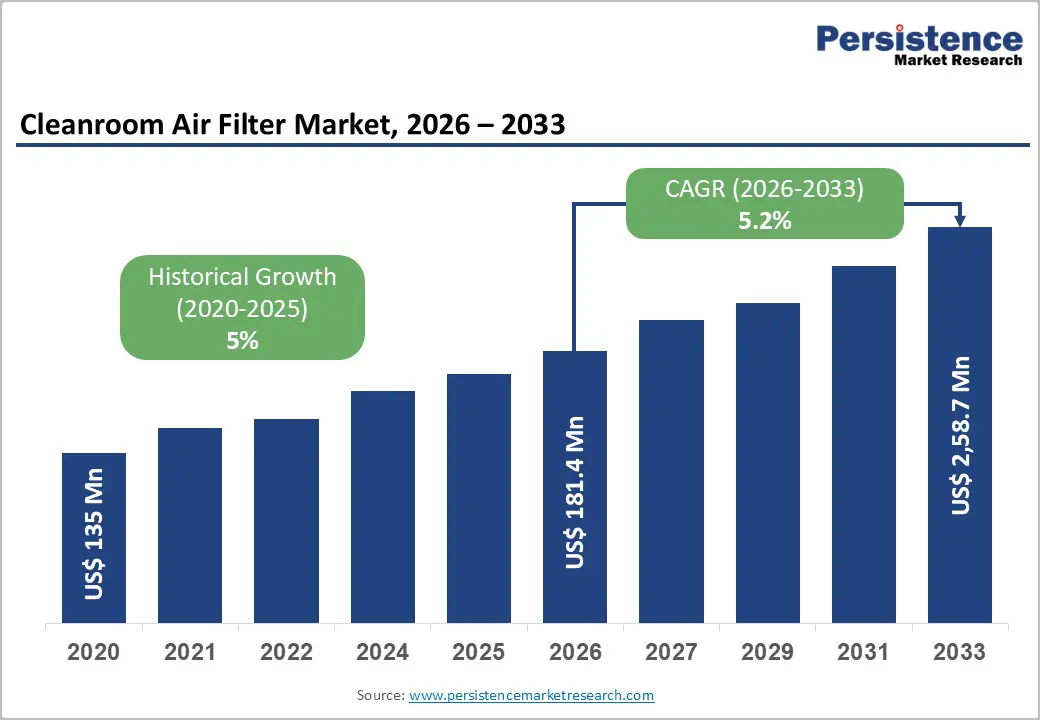

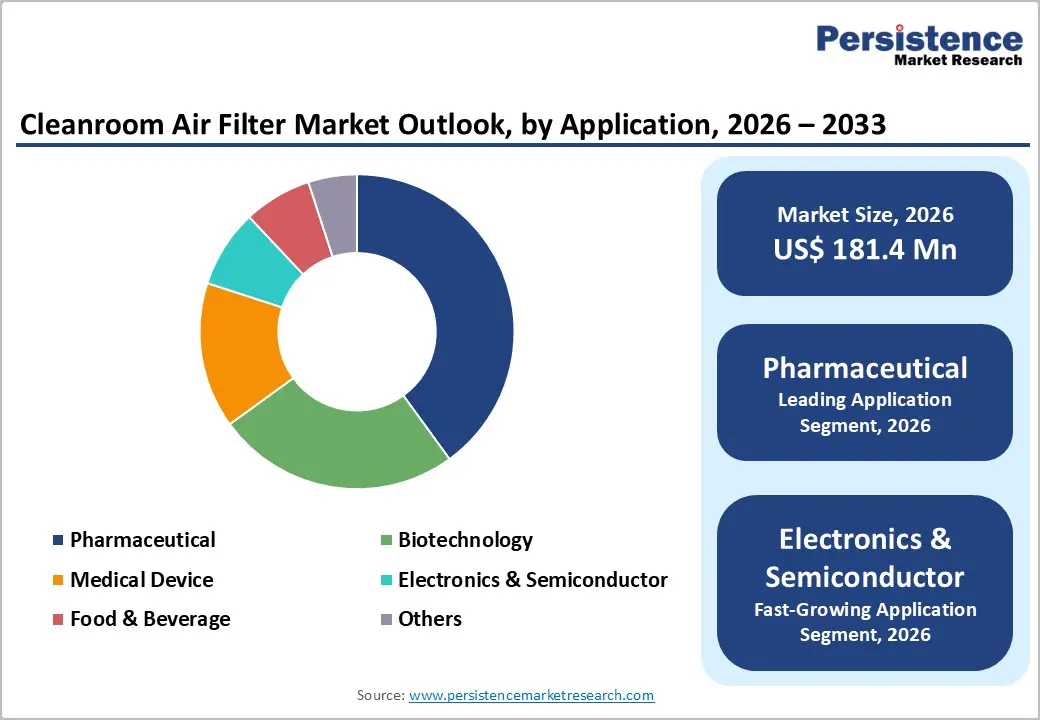

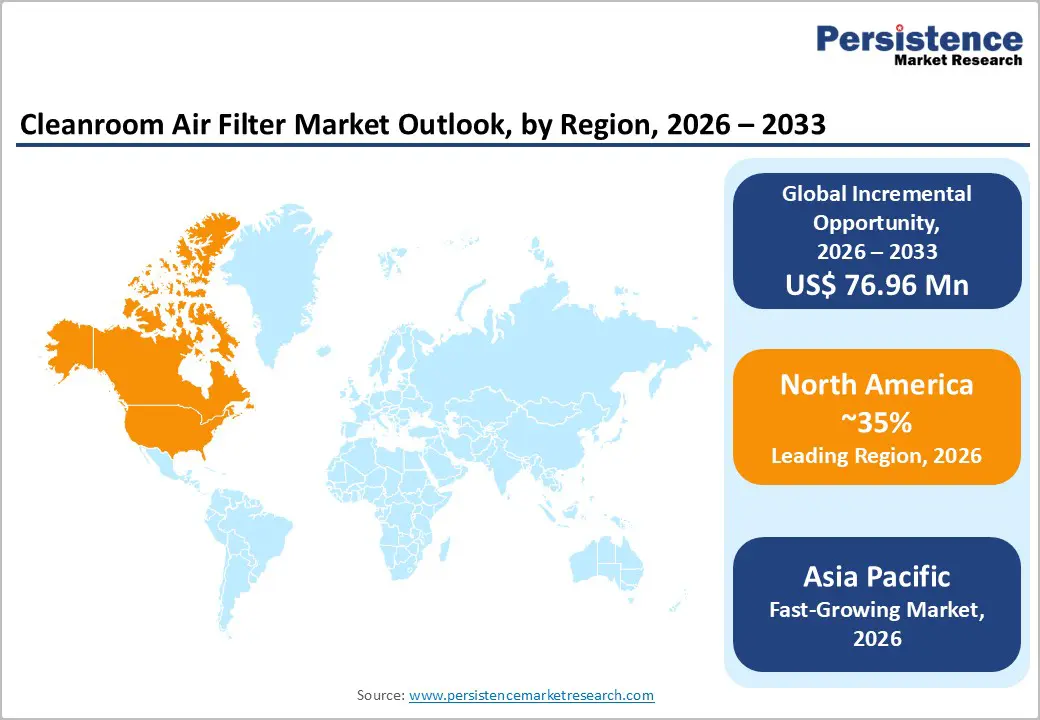

The global cleanroom air filter market size is likely to be valued at US$ 181.4 million in 2026, and is projected to reach US$ 258.7 million by 2033, growing at a CAGR of 5.2% during the forecast period 2026−2033.

Rising industrial demand for controlled environments is driving investments in air filtration technologies across pharmaceuticals, biotechnology, and electronics sectors. Regulatory mandates for contamination control, including ISO 14644 standards, enforce stringent cleanroom air quality levels, creating steady demand for advanced filters. Technological integration, such as high-efficiency particulate air (HEPA) and ultra-low particulate air (ULPA) systems, improves operational reliability and energy efficiency, enhancing adoption. The expansion of healthcare infrastructure in emerging economies increases the need for sterile environments in pharmaceutical manufacturing and medical device production. Industrial automation and process digitalization allow real-time monitoring and predictive maintenance of filtration systems, boosting operational efficiency.

Key Industry Highlights

- Dominant Region: North America is expected to dominate with an estimated 35% market share in 2026, supported by strong biopharmaceutical and advanced manufacturing infrastructure and stringent regulatory enforcement.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, propelled by semiconductor fabrication expansion and pharmaceutical manufacturing scale-up.

- Leading Application: Pharmaceutical applications are projected to lead with 40% market share in 2026, driven by strict regulatory compliance and tight contamination control requirements.

- Fastest-growing Application: Electronics and semiconductor applications are projected to register the fastest growth through 2033, on account of expanding microchip fabrication capacity and increasing capital investment in advanced wafer fabrication facilities.

- November 2025: AAF International introduced the AstroScan® M system to improve safety and efficiency in HEPA filter leak testing, enabling in-situ validation of bag-in/bag-out containment systems.

| Report Attribute | Details |

|---|---|

|

Cleanroom Air Filter Market Size (2026E) |

US$ 181.4 Mn |

|

Market Value Forecast (2033F) |

US$ 258.7 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Heightening Demand for Contamination Control in Healthcare and Research Facilities

Air quality control in healthcare and research settings plays a pivotal role in reducing airborne pathogen transmission and ensuring aseptic conditions for patients and sensitive biological work. Regulatory guidance from the Centers for Disease Control and Prevention (CDC) emphasizes that filtration is a core component of environmental infection control in health-care facilities, and that proper heating, ventilation, and air conditioning systems must be designed to remove contaminated air and minimize the risk of spreading airborne pathogens to both patients and healthcare personnel. Filtration systems with high efficiency, such as HEPA filters, are recommended for areas with a high risk of airborne contamination, including isolation rooms and areas housing infectious patients, as they physically remove particulate matter and pathogens from circulated air, thereby supporting safer care environments.

Healthcare-associated infections (HAIs) remain a major patient safety concern, as highlighted in the 2024 CDC National and State Healthcare-Associated Infections Progress Report, which found that approximately 1 in 31 hospital patients in the United States has at least 1 HAI on any given day. This prevalence underscores the ongoing challenge of controlling infection spread within clinical environments and the need for robust air quality management as part of infection prevention strategies. Effectively managing airborne contaminants through engineered filtration and ventilation can lower the concentration of infectious particles circulating in critical spaces, protect immunocompromised individuals, and support broader public health goals for reducing HAIs.

Technological Advancements in Filter Design

Rapid improvements in air filtration technology reshaped expectations for particulate removal efficiency and operational performance in critical contamination-sensitive environments. Government standards such as the U.S. Department of Energy (DOE)’s HEPA definition, which requires filters to capture at least 99.97% of particles 0.3 micrometers in diameter, set a baseline for high performance in industrial and laboratory applications and drive engineers to pursue even higher efficiency and lower pressure drop designs. Innovations in filament materials, media structuring, and rigorously tested configurations enhance the likelihood that process-sensitive zones maintain stable environmental conditions with less energy overhead, supporting stringent air quality thresholds mandated in regulated production zones where even nano-scale contaminants disrupt outcomes.

Pushing beyond basic efficiency targets, advanced filtration designs incorporate digitally enabled monitoring, adaptive airflow control, and hybrid media blends that expand performance parameters without fundamentally increasing system complexity. These technological enhancements directly influence uptime, predictive maintenance forecasting, and lifecycle cost models, giving quantifiable performance improvements to engineering and facility managers. Digital sensor feedback mechanisms reduce unscheduled filter change events by enabling condition-based servicing, aligning with broader industrial digitalisation strategies. Integrating mechanically optimised designs with smart control layers enables facilities to balance quality assurance commitments with escalating energy costs and compliance obligations across sensitive operations, from pharmaceutical production to precision manufacturing.

Long Service Life Reducing Replacement Frequency

High-efficiency filtration systems in controlled environments are designed to maintain optimal air quality for extended periods. According to the U.S. CDC, HEPA filters used in healthcare and laboratory settings can operate effectively for up to 10 years when supported by prefiltration and regular monitoring. This extended operational lifespan ensures consistent particulate control, reducing replacement frequency and minimizing operational interruptions in sensitive environments such as hospitals, research laboratories, and semiconductor facilities.

From a business perspective, extended service life affects replacement cycles and revenue generation. Longer-lasting filters reduce the demand for recurring purchases, lowering the frequency of aftermarket sales that typically contribute to predictable revenue streams. Maintenance schedules shift from periodic replacements to condition-based monitoring, potentially limiting service contract opportunities. Firms may respond by offering value-added services such as real-time monitoring, predictive maintenance, and installation support to maintain customer engagement.

Shortage of Skilled Cleanroom Professionals

The shortage of skilled cleanroom professionals results from a structural gap in workforce capabilities relative to industry requirements for highly specialized roles requiring expertise in contamination control, heating, ventilation, & air conditioning (HVAC) systems, regulatory compliance, and precision equipment operation. National policies on skill development indicate persistent challenges in aligning vocational and technical education with industrial needs, particularly for technology-intensive sectors. Training programs often fail to equip candidates with the practical knowledge and certifications required to manage cleanroom environments effectively. Government data highlight that a substantial portion of the labor force lacks the necessary technical skills and experience to operate under strict cleanliness standards. Limited availability of trained professionals affects operational efficiency and compliance with regulatory standards, forcing companies to extend onboarding and supervision periods, thereby increasing costs and reducing productivity.

This workforce gap creates significant operational and financial pressures for organizations dependent on high-performance air filtration and controlled environments. Cleanroom operations demand rigorous adherence to contamination-prevention protocols, where even minor errors can result in costly product losses and regulatory penalties. According to the India Skills Report 2025, only 54.8% of graduates are considered employable in industry-aligned roles, highlighting the insufficiency of trained personnel for specialized applications. Organizations must invest in extensive in-house training, continuous upskilling, and external consulting support to fill capability gaps, which increases operational expenditures and delays project timelines.

Development of Eco-friendly and Sustainable Filtration Solutions

A stronger emphasis on sustainable, energy-efficient filtration solutions aligns with broader government environmental and energy-efficiency policies that influence technology adoption and regulatory compliance. Programs managed by agencies such as the U.S. Environmental Protection Agency (EPA) set performance and energy-use benchmarks for air-cleaning devices and filters, guiding industrial and commercial buyers in their procurement decisions. Compliance with these guidelines ensures operational efficiency, reduces energy consumption, and supports long-term cost management.

Governmental focus on indoor air quality and energy conservation standards reinforces the relevance of eco-friendly filtration. Agencies continue to promote healthier indoor environments through high-efficiency filtration, ventilation improvements, and source control strategies. Products that meet these standards benefit from reduced operational costs, enhanced regulatory compliance, and improved workplace safety. From a business perspective, sustainable filtration solutions also strengthen corporate environmental, social, & governance (ESG) positioning, which influences stakeholder perception and supports long-term strategic growth.

Integration of Smart IoT and Sensor-Enabled Filters

Data-driven monitoring via smart IoT and sensor networks transforms traditional cleanroom operations by providing continuous, real-time insights into environmental conditions, including particulate levels, temperature, and humidity. These systems enable immediate corrective action when parameters deviate from required standards, reducing contamination risks and improving operational reliability. According to the U.S. National Institute of Standards and Technology (NIST), IoT-enabled environmental monitoring enables centralized data analysis, visualization, and automated alerts, enhancing responsiveness compared to manual inspections and fixed maintenance schedules.

Operational efficiency and energy optimization are significantly enhanced through predictive maintenance and dynamic control of ventilation systems. U.S. DOE studies indicate that sensor-driven HVAC and filtration systems can improve energy efficiency while maintaining strict environmental conditions. Automated logging of system performance supports regulatory compliance and minimizes downtime, while real-time adjustments to airflow and filtration reduce unnecessary energy consumption.

Category-wise Analysis

Product Type Insights

HEPA filters are poised to lead with nearly 45% of the cleanroom air filter market revenue share in 2026, owing to their high particle removal efficiency and widespread regulatory acceptance. Industries such as pharmaceuticals and biotechnology require HEPA filters to maintain ISO class-compliant cleanrooms. HEPA filters demonstrate proven performance in removing submicron particles, ensuring sterility in sensitive production environments. Adoption is further reinforced by established supply chains, standardized specifications, and compatibility with automated HVAC systems. Operational reliability and compliance alignment position HEPA filters as the preferred solution across diverse industrial segments. Their strong validation history, global certification recognition, and consistent filtration efficiency across varying airflow conditions support long-term deployment in mission-critical facilities. Maintenance protocols are well defined, enabling predictable lifecycle management and cost planning.

ULPA filters are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by increasing demand for ultra-clean environments in semiconductor fabrication and high-precision electronics manufacturing. Their enhanced particulate capture efficiency addresses stringent contamination control requirements. Adoption is supported by technological advancements enabling energy-efficient operation and reduced pressure drops. Integration with smart monitoring systems further accelerates adoption in industries prioritizing precision and compliance. The growth trajectory is underpinned by expanding production facilities and the need for next-generation filtration capabilities in critical manufacturing processes. Advanced membrane materials and improved pleat design enhance airflow uniformity while sustaining ultra-low penetration levels. The ongoing miniaturization of electronic components increases sensitivity to airborne particles, elevating performance expectations.

Application Insights

Pharmaceutical applications are likely to dominate, with a projected 40% share of the cleanroom air filter market in 2026, driven by stringent regulatory mandates and the continuous production of sterile drugs. Contamination control is critical in drug formulation, compounding, and packaging. Cleanroom filtration ensures product safety and compliance with U.S. Food and Drug Administration (FDA) and European Medicines Agency (EMA) guidelines. High adoption rates are driven by facility expansion, process standardization, and operational audits. Reliability and performance of air filtration systems remain key considerations for maintaining uninterrupted pharmaceutical production. Validation protocols, batch traceability requirements, and Good Manufacturing Practice (GMP) compliance frameworks reinforce the importance of controlled airflow systems. Increasing biologics manufacturing and vaccine production further elevate sterility standards.

Electronics and semiconductor applications are expected to grow the fastest during the 2026-2033 forecast period, driven by expanding microchip fabrication and nanotechnology development. Industry-specific contamination control thresholds necessitate high-efficiency air filtration. Adoption is stimulated by investment in precision manufacturing, automated assembly lines, and technology-intensive cleanroom designs. The growth potential is amplified by regional manufacturing hubs and increasing global demand for semiconductor components. Digital integration of filtration systems enhances operational monitoring, accelerating adoption. Shrinking circuit geometries and higher wafer densities increase sensitivity to airborne molecular contamination. Capital expenditure in advanced fabrication facilities supports demand for ultra-clean production zones.

Regional Insights

North America Cleanroom Air Filter Market Trends

North America is expected to dominate with an estimated 35% of the cleanroom air filter market value in 2026, reflecting concentration of high-value, contamination-sensitive manufacturing ecosystems. Leadership is anchored in large-scale biopharmaceutical production, advanced therapy medicinal product facilities, aerospace engineering, and defense electronics manufacturing operating under stringent environmental control protocols. Regulatory enforcement by the U.S. FDA and Health Canada sustains recurring validation, certification, and replacement cycles, creating predictable demand patterns. High compliance intensity within current Good Manufacturing Practice environments necessitates continuous airflow integrity testing and documented performance verification.

Dominance is further supported by capital-intensive research and development infrastructure and early adoption of automation-driven facility management systems. Federal semiconductor manufacturing incentives accelerate the development of advanced fabrication plants requiring ultra-controlled particulate environments. Elevated labor costs encourage predictive maintenance models and sensor-enabled filtration monitoring to minimize downtime risks. Institutional procurement frameworks prioritize validated, performance-certified components, reinforcing premium product adoption

Europe Cleanroom Air Filter Market Trends

Europe represents a technologically advanced and regulation-intensive landscape for cleanroom air filtration deployment, characterized by strong alignment with harmonized quality and environmental standards. Pharmaceutical manufacturing clusters in Germany, Switzerland, France, Ireland, and Belgium sustain consistent demand for validated contamination control infrastructure, particularly in biologics, vaccine production, and advanced therapy medicinal products. Compliance with European Medicines Agency guidelines and European Union Good Manufacturing Practice frameworks requires documented airflow validation, particulate monitoring, and periodic integrity testing, reinforcing structured replacement cycles. The expansion of sterile injectables manufacturing and contract development activities underscores the need for high-efficiency filtration systems.

Sustainability policy frameworks strongly influence purchasing decisions, with emphasis on energy-efficient Heating, Ventilation, and Air Conditioning configurations and reduced lifecycle carbon intensity. Adoption of low-pressure-drop filters and recyclable filtration media aligns with European Union climate objectives and industrial decarbonization strategies. Advanced research infrastructure and public funding support innovation in nanotechnology, life sciences, and aerospace engineering, all of which depend on contamination-controlled production spaces. Cross-border supply chain integration within the European Union enables standardized technical specifications and procurement practices.

Asia Pacific Cleanroom Air Filter Market Trends

Asia Pacific is forecasted to be the fastest-growing market for cleanroom air filters between 2026 and 2033, propelled by accelerated semiconductor fabrication expansion, pharmaceutical manufacturing scale-up, and strategic electronics supply chain localization initiatives. Large capital investments in wafer fabrication plants, biosimilar production units, and medical device manufacturing clusters across China, Taiwan, South Korea, and India are intensifying demand for advanced contamination control systems. Production-linked incentive programs and industrial modernization policies are strengthening domestic output of integrated circuits, specialty chemicals, and sterile formulations. Increasing design complexity in microelectronics and biologics processing increases sensitivity to microscopic contaminants, underscoring the need for high-efficiency filtration technologies capable of maintaining stringent particulate control thresholds.

Growth momentum is further supported by competitive manufacturing economics that attract multinational greenfield investments and capacity relocation strategies. The expansion of robotics-enabled precision assembly lines increases reliance on validated environmental control infrastructure. Development of large industrial corridors enables integrated cleanroom planning at the construction stage, streamlining adoption of high-performance airflow management systems. Rising domestic consumption of consumer electronics, diagnostic devices, and injectable therapeutics sustains the continuous scaling of production. Strengthening export compliance standards and quality certification frameworks accelerate deployment of advanced air filtration systems across critical manufacturing ecosystems.

Competitive Landscape

The global cleanroom air filter market structure demonstrates moderate consolidation, with leading multinational filtration manufacturers sustaining competitive influence through technology depth, global distribution networks, and vertically integrated production capabilities. Key participants include Camfil AB, Parker Hannifin Corp., Daikin Industries Ltd., Freudenberg and Co. KG, TROX GmbH, 3M Co., Atlas Copco AB, MANN HUMMEL International GmbH and Co. KG, and Ahlstrom Holding 3 Oy. These organizations compete through high-efficiency particulate technologies, engineered airflow management systems, and advanced media innovation designed for critical manufacturing environments. Strong research and development investments enable continuous enhancement of filter media performance, energy efficiency optimization, and compliance validation capabilities.

Competitive intensity is shaped by technological differentiation, regional manufacturing presence, and the ability to deliver customized contamination control solutions aligned with industry-specific regulatory frameworks. Larger participants leverage economies of scale, integrated Heating, Ventilation, and Air Conditioning system compatibility, and digital monitoring integration to secure high-value contracts in pharmaceutical, semiconductor, and advanced manufacturing facilities. Mid-sized and specialized suppliers contribute to selective fragmentation through niche expertise in modular cleanroom configurations and application-specific filtration media. Strategic collaborations, mergers, and technology licensing agreements are used to expand geographic reach and accelerate product innovation.

Key Industry Developments

- In January 2026, Cleanova acquired U.S.-based Airflotek and TES-Clean Air Systems to enter ultra-clean controlled-environment markets and strengthen its capabilities in advanced cleanroom and high-efficiency air filtration solutions.

- In November 2025, Freudenberg expanded its filtration portfolio with next-generation fan filter units (FFUs), integrated bag-in/bag-out (BIBO) containment systems, and N-Methyl-2-Pyrrolidone (NMP) resistant filters designed for semiconductor, pharmaceutical, and lithium-ion battery manufacturing environments, improving safety and energy efficiency.

- In September 2025, Camfil AB announced the expansion of HEPA and ULPA filter production at its Manesar plant to boost supply capacity for hospitals, pharmaceutical cleanrooms, biotechnology laboratories, and other containment facilities, enhancing compliance with EN 1822 and ISO 29463 standards and reinforcing critical air-quality support for key sectors.

Companies Covered in Cleanroom Air Filter Market

- Camfil AB

- Parker Hannifin Corp.

- Daikin Industries Ltd.

- Freudenberg and Co. KG

- TROX GmbH

- 3M Co.

- Atlas Copco AB

- MANN HUMMEL International GmbH and Co. KG

- Ahlstrom Holding 3 Oy

- Lindab AB

- Filtration Group Corp.

- Airtech Japan Ltd.

- Labconco Corp.

- Kalthoff Luftfilter und Filtermedien GmbH

- KOWA Air Filter Industry Ltd

- Daesung Industrial Co. Ltd.

- Aerospace America Inc.

- CleanAir Solutions Inc.

- E.L. Foust

- Airex Filter Corp.

Frequently Asked Questions

The global cleanroom air filter market is projected to reach US$ 181.4 million in 2026.

Rising semiconductor fabrication, expanding sterile pharmaceutical manufacturing, stringent regulatory compliance requirements, and increasing demand for contamination-controlled production environments are driving the market.

The market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Expansion of semiconductor fabrication facilities, growth in biologics and vaccine manufacturing, adoption of smart sensor-enabled filtration systems, retrofit demand in aging cleanrooms, and sustainability-driven energy-efficient filter innovation represent key market opportunities.

Some of the key market players include Camfil AB, Parker Hannifin Corp., Daikin Industries Ltd., Freudenberg and Co. KG, TROX GmbH, 3M Co., and Atlas Copco AB.