- Industrial Machinery

- Brazil Conveyor Market

Brazil Conveyor Market Size, Share, and Growth Forecast, 2026 – 2033

Brazil Conveyor Market by Equipment Type (Sortation Conveyor, Others), Degree of Automation (Manual Conveyor Systems, Others), Industry Verticals (Mining, Logistics and Supply Chain, Other industries), and Country Analysis 2026 – 2033

Brazil Conveyor Market Size and Trends Analysis

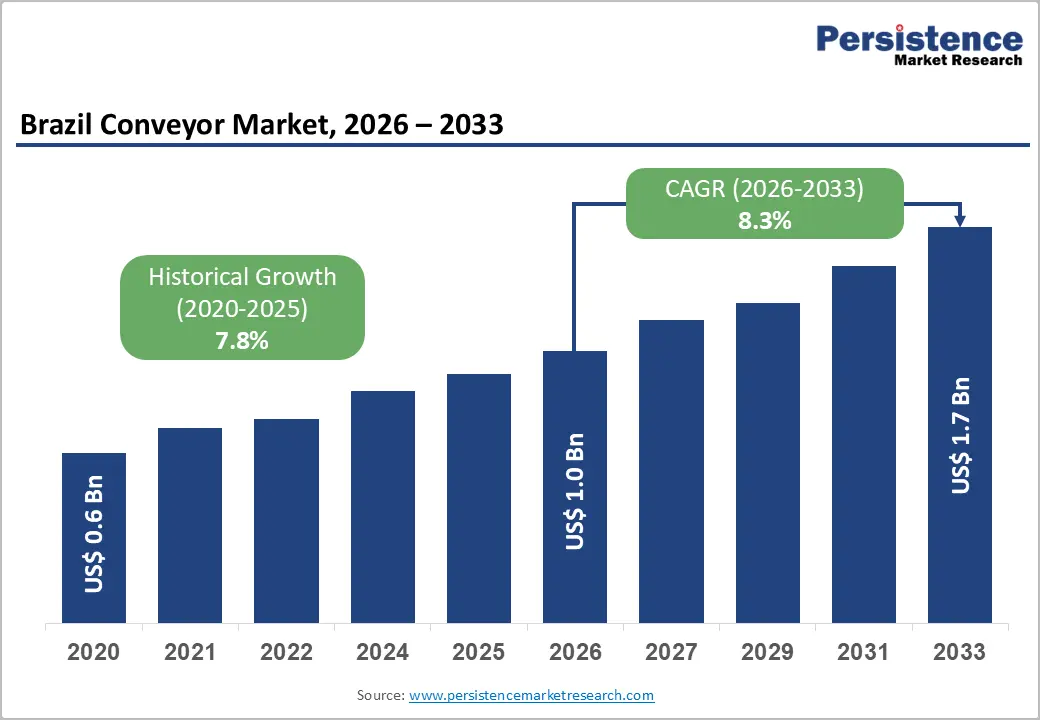

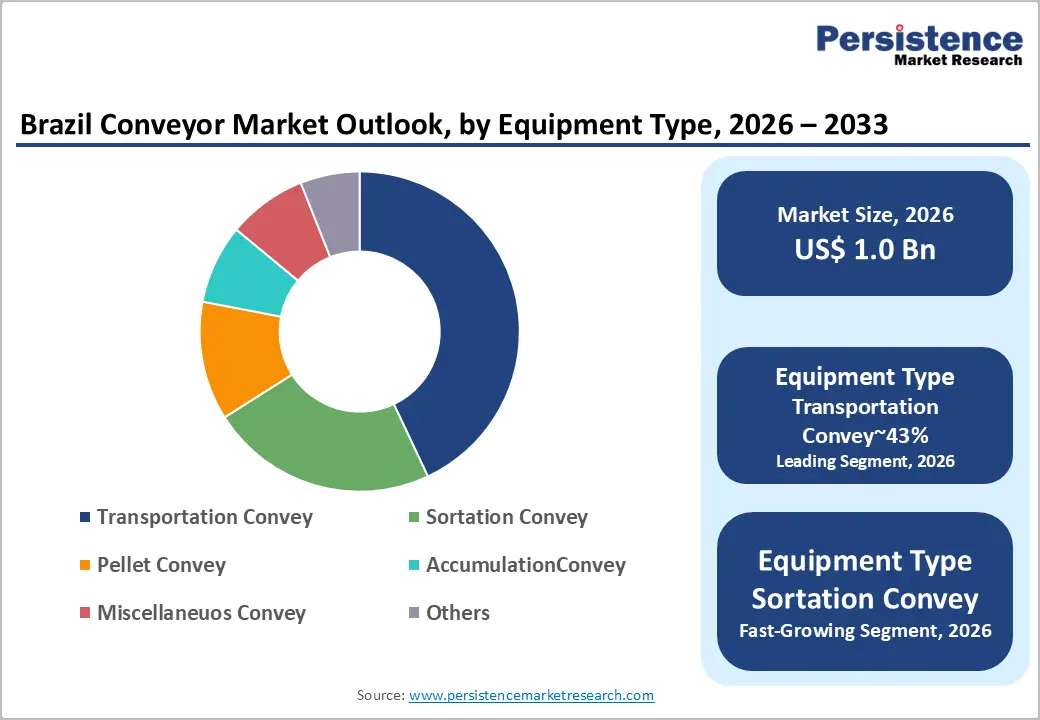

The Brazil conveyor market size is likely to be valued at US$1.0 billion in 2026 and is expected to reach US$1.7 billion by 2033, growing at a CAGR of 8.3% during the forecast period from 2026 to 2033, driven by the accelerating adoption of industrial automation, particularly as the mining and logistics sectors continue to expand across Brazil’s resource-rich regions. Increasing industrialization and ongoing mining developments are expected to boost demand for heavy-duty conveyor systems. Logistics companies are also likely to adopt automated solutions to enhance operational efficiency and throughput in urban distribution centers. Strategic infrastructure investments are set to further improve material handling capabilities, while manufacturers are anticipated to incorporate artificial intelligence to optimize conveyor performance and reduce energy consumption. Overall, these factors are expected to support steady growth in Brazil’s industrial equipment sector.

Key Industry Highlights:

- Leading Equipment Type: Transport conveyors are expected to lead, accounting for approximately 43% share in 2026 through heavy industrial adoption, high throughput, reliable quality, and high-value applications in mining and bulk material handling.

- Fastest-growing Equipment: Sortation conveyors are anticipated to grow the fastest due to on-demand production, hybrid workflows, and increasing adoption in logistics, e-commerce, and retail distribution centers.

- Leading Industry Vertical: Mining is expected to lead, holding approximately 32% share in 2026. This dominance is driven by Brazil’s status as a global iron ore leader, with massive investments in high-capacity belt systems.

- Fastest-growing End-user: Logistics and supply chain is anticipated to be the fastest-growing segment, fueled by urban delivery pressures, e-commerce expansion, and rapid fulfillment center deployment.

| Key Insights | Details |

|---|---|

| Brazil Conveyor Market Size (2026E) | US$1.0 Bn |

| Market Value Forecast (2033F) | US$1.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.8% |

DRO Analysis

Driver Analysis – E-commerce Proliferation Stimulating Warehouse Fulfillment Infrastructure

The rapid expansion of online retail platforms is expected to transform domestic logistics requirements significantly. Fulfillment centers are likely to require advanced sortation systems to manage high parcel volumes efficiently. Increased consumer demand for rapid delivery is anticipated to accelerate the adoption of automated conveyors. Logistics providers are projected to scale their distribution networks to reach secondary metropolitan areas faster. These shifts are expected to create a sustained demand for modular and scalable conveyor designs. Manufacturers are positioned to benefit from the ongoing digitalization of the national supply chain ecosystem.

Logistics efficiency is set to improve through Interroll with Small Wheel Vertical Crossbelt Sorter technology. This system is expected to optimize space utilization while providing high-speed sorting for small parcels. The compact design allows operators to maximize throughput within existing warehouse footprints across urban centers. Furthermore, Vanderlande with POSISORTER HC is anticipated to deliver reliable high-capacity sorting for diverse items. These technological deployments are expected to reduce manual labor costs while increasing order accuracy levels. Such advancements are projected to strengthen the competitive position of large-scale e-commerce market participants.

Government-Led Digital Transformation Incentives for Industrial Modernization

Federal initiatives focused on industrial digitalization are expected to accelerate the adoption of smart conveyors. Substantial investment plans are projected to support the integration of robotics within domestic manufacturing plants. These policies are estimated to encourage enterprises to upgrade legacy systems with intelligent automation features. Improved access to credit for technology procurement is anticipated to stimulate market activity across sectors. Modernization is set to improve the global competitiveness of Brazilian goods in international trade markets. The focus on Industry 4.0 is likely to drive long-term structural growth in hardware.

The push for smart systems is illustrated by Dematic with the FD Shuttle for warehouses. This automated storage solution is expected to integrate seamlessly with existing conveyor frameworks for efficiency. Its floor rail-free design is projected to offer flexibility for expanding distribution and manufacturing facilities. Honeywell Intelligrated, with conveying solutions, is highly skilled to provide integrated controls for better workflow. These platforms are anticipated to enable real-time monitoring of material flow across complex industrial environments. Government support is set to ensure a stable environment for such high-technology capital investments.

Mining Sector Bulk Handling Expansion

Rising ore extraction volumes propel conveyor adoption as Brazilian mines scale output to meet global commodity demands. Infrastructure upgrades in iron and bauxite operations necessitate robust transport systems for continuous material flow. This dynamic boosts market momentum by linking production surges to automation investments. Policy incentives for mineral exports further amplify procurement cycles across large-scale sites.

Intralox with AquaPruf Series and Habasit with Sanigard Hygiene Belt exemplify engineering tailored for mining durability and reduced downtime. These platforms integrate modular designs that enhance throughput while minimizing maintenance interruptions. Market participants gain a competitive edge as such innovations align with operational uptime mandates. Forward positioning strengthens as vendors scale local assembly to support regional project pipelines.

Restraint Analysis – High Capital Expenditure Requirements for Advanced Automation

Significant initial investment costs are expected to limit the adoption of fully automated conveyor systems. Small and medium enterprises face financial hurdles when upgrading their material handling. The high price of specialized components and software integration is projected to extend payback periods. Economic fluctuations in the region are anticipated to make long-term capital commitments more challenging today. High interest rates discourage firms from pursuing large-scale automation projects in the near-term. This financial barrier is set to maintain the dominance of more affordable semi-automated alternatives.

Cost pressures are often addressed by Mercurio with high-performance conveyor belts for cost-effective transport. While these products offer durability, the total system cost remains a hurdle for many operators. Procurement teams prioritize immediate operational needs over long-term technological advancement in hardware. Flexlink with X45 systems might also see restricted adoption due to specialized engineering cost structures. Manufacturers are expected to offer more flexible financing models to mitigate these high entry barriers. The preference for lower-cost manual or semi-automated solutions is projected to persist among smaller players.

Technical Skill Gaps in Advanced System Maintenance

A shortage of specialized labor is expected to hinder the maintenance of sophisticated conveyor systems. The integration of AI and IoT requires technicians with advanced digital and mechanical skill sets. Domestic firms are projected to struggle with recruiting personnel capable of managing complex automated hardware. This skills gap is anticipated to lead to longer downtime periods during equipment failure events. High training costs are projected to increase the operational expenditures for companies adopting new technologies. The lack of local expertise is set to slow the deployment of cutting-edge solutions.

Service requirements are being addressed by Metso with Life Cycle Services to support mining operators. These agreements are expected to provide the necessary expertise for maintaining critical material handling equipment. The reliance on external service providers is estimated to increase the long-term operational costs. Interroll with MCP PLAY also requires specific programming knowledge for optimal configuration and daily management. Companies are projected to invest in internal training programs to build a more resilient workforce. This human resource challenge is anticipated to influence the pace of technological transition significantly.

Opportunity Analysis – Integration of IoT and Predictive Analytics for Performance

The adoption of digital twins and sensor networks is expected to unlock significant efficiency gains. Real-time data monitoring is projected to allow operators to anticipate potential conveyor failures before they occur. Predictive maintenance is anticipated to reduce unplanned downtime and extend the lifespan of expensive hardware. These digital solutions are anticipated to improve the safety and reliability of heavy-duty mining operations. Manufacturers are positioned to offer software-as-a-service models to supplement their traditional conveyor equipment sales. The shift toward data-driven operations is set to become a major competitive differentiator soon.

Innovative monitoring is currently led by Continental AG with Conti+ 2.0 for belt management. This platform is expected to provide comprehensive insights into the health of steel cord belts. Operators are using these analytics to optimize the scheduling of maintenance and repairs. Furthermore, Vanderlande, with the Flow Sort Controller, is projected to enhance the precision of sorting operations. These tools are anticipated to enable more agile responses to changing throughput demands in warehouses. The integration of such technologies is anticipated to create new revenue streams for equipment vendors.

Rising Demand for Sustainable and Energy-Efficient Conveying

Environmental regulations and corporate sustainability goals are expected to drive demand for green conveyor solutions. Energy-efficient motors and low-friction materials are expected to become standard requirements for new system installations. Carbon reduction mandates are projected to encourage the replacement of diesel-powered machinery with electric alternatives. Sustainable practices are anticipated to improve the public image of mining and manufacturing enterprises domestically. These trends will favor manufacturers who prioritize environmental performance in their product development. Green technology is set to capture a growing share of industrial investment budgets.

Sustainability is a focus for Vanderlande with ADAPTO, which uses energy-efficient shuttle technology. This system is expected to minimize power consumption while maintaining high throughput in distribution centers. Manufacturers are projected to utilize recyclable materials in the construction of conveyor frames and rollers. Additionally, SEW-EURODRIVE with MOVIGEAR is progressing to provide decentralized drive solutions for energy savings. These components are anticipated to reduce the overall environmental footprint of large-scale material handling facilities. The market for eco-friendly systems is expected to expand as regulatory pressures increase.

Category–wise Analysis

Equipment Type Insights

Transport conveyors are expected to lead, accounting for approximately 43% share in 2026. This dominance is underpinned by the heavy reliance on bulk material handling in mining sectors. Belt systems are projected to remain the primary choice for transporting large volumes of ore. These conveyors are anticipated to provide the most cost-effective solution for long-distance material movement. The integration of Continental AG with Phoenix Phoenocord ST10000 illustrates the focus on high-capacity transport. Mercurio, with high-performance conveyor belts are supporting various industrial applications.

Sortation conveyors are expected to be the fastest-growing segment, driven by the explosive expansion of e-commerce and retail distribution networks. High-speed sorting is projected to become essential for managing the increasing volume of individual parcels. Technology from Interroll with the Small Wheel Vertical Crossbelt Sorter is set to drive efficiency. Vanderlande with POSISORTER HC is anticipated to meet the needs of large logistics hubs. The shift toward automated fulfillment is projected to accelerate the deployment of these systems.

Industry Vertical Insights

Mining is anticipated to lead, holding approximately 32% share in 2026. This dominance is driven by the country's status as a global leader in iron ore. Extraction projects in the Carajás region are projected to require massive investments in belt systems. The durability of Continental AG with Phoenix Phoenocord ST10000 is likely to satisfy these requirements. Additionally, Metso, with Life Cycle Services, is expected to ensure the longevity of mining hardware. High-capacity conveyors are set to remain critical for the profitability of large-scale mineral operations. The sector's demand is estimated to be sustained by rising global commodity prices.

The logistics and supply chain segment is expected to be the fastest-growing segment, driven by urban delivery pressures. The rise of digital marketplaces is projected to necessitate the build-out of new fulfillment centers. Modern distribution hubs are more likely to prioritize high-speed conveyors for rapid order processing and dispatch. Vanderlande with ADAPTO is anticipated to play a key role in the automation of warehouses. Dematic with Multishuttle is projected to improve the storage density of logistics facilities. The ongoing localization of supply chains is set to stimulate investments in advanced sorting hardware. This segment is expected to experience rapid technological adoption in metropolitan regions.

Competitive Landscape

The Brazil conveyor market is characterized by a fragmented structure with high competition among global and local players. Market leadership is often determined by the ability to provide integrated, high-reliability systems for mining. Procurement relationships and brand equity are likely to favor established vendors with extensive local service networks. Metso, with Life Cycle Services, establishes a benchmark for long-term operational support in the mining sector. These players are expected to drive the technological evolution of the domestic conveyor ecosystem.

Horizontal differentiation is expected to increase as manufacturers expand their portfolios to cover multiple industry segments. Premium innovators are anticipated to focus on AI integration and energy-efficient designs to maintain their margins. Vanderlande with ADAPTO and Dematic with Multishuttle represent high-end automated storage and retrieval benchmarks. In contrast, local competitors like Mercurio with high-performance conveyor belts offer value-positioned solutions for standard needs.

Key Industry Developments:

- In June 2025, Continental AG confirmed plans for the strategic carve-out and planned sale of its ContiTech group sector by 2026. This move positions the conveyor division as a more agile, independent entity, potentially attracting new investment specifically for Brazilian industrial growth.

- In May 2025, ContiTech celebrated the successful expansion and full operational integration of its conveyor belt plant in Ponta Grossa, Paraná. This expansion enables the local production of the world’s strongest belts (up to ST10000), drastically reducing shipping timelines for South American mining operations.

Companies Covered in Brazil Conveyor Market

- Dematic (KION Group)

- Vanderlande (Toyota Industries)

- Honeywell Intelligrated

- Daifuku

- Beumer Group

- Metso

- Interroll

- Continental AG (ContiTech)

- Flexlink (Coesia)

- Dorner

- Mercurio

- Bellt Correntes Transportadoras

- ConVeyBelts Michelin Group

- Derco do Brasil

- TM Schaefer Engenharia

- Bastian Solutions

Frequently Asked Questions

The Brazil conveyor market is projected to be valued at US$1.0 billion in 2026 and is expected to reach US$1.7 billion by 2033, driven by industrial automation in the mining and logistics sectors and strategic infrastructure investments.

Rapid growth in online retail platforms and urban delivery demands is boosting the adoption of automated and sortation conveyors, enabling faster fulfillment, higher throughput, and more efficient warehouse operations across Brazil.

The Brazil conveyor market is forecast to grow at a CAGR of 8.3% from 2026 to 2033, reflecting strong demand in mining, logistics, and industrial modernization initiatives.

The logistics and supply chain is anticipated to be the fastest-growing industry vertical, driven by the rapid deployment of modern fulfillment centers, urban delivery pressures, and digital marketplace expansion.

The Brazil conveyor market is highly competitive, with major players including Dematic (KION Group), Vanderlande (Toyota Industries), Honeywell Intelligrated, Metso, Interroll, Continental AG (ContiTech), Mercurio, and Flexlink (Coesia), competing through technology integration, service networks, and energy-efficient solutions.