- Food Ingredients & Additives

- Bitter Blocker Market

Bitter Blocker Market Size, Share, and Growth Forecast, 2026 - 2033

Bitter Blocker Market by Product Type (Natural Bitter Blockers, Synthetic Bitter Blockers, Others), Application (Food & Beverage, Pharmaceuticals, Others), End-user (Industrial, Non-Industrial, Consumer), and Regional Analysis for 2026 - 2033

Bitter Blocker Market Size and Trends Analysis

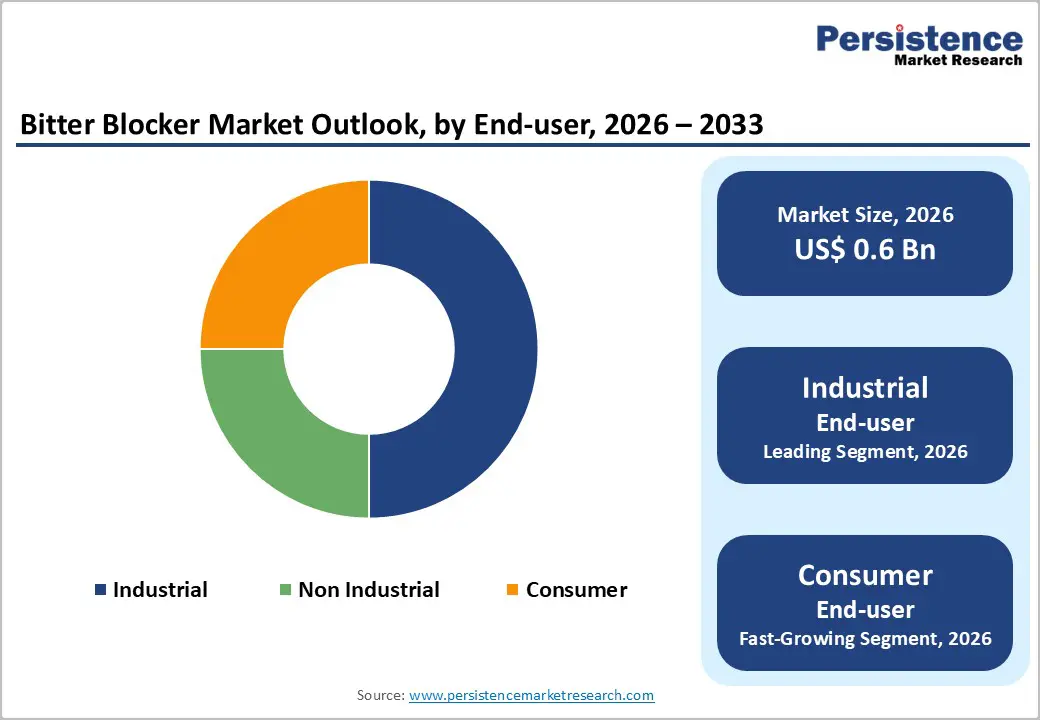

The global bitter blocker market size is likely to be valued at US$0.6 billion in 2026, and is expected to reach US$1.0 billion by 2033, growing at a CAGR of 8.7% during the forecast period from 2026 to 2033, driven by the increasing prevalence of functional food innovation, rising demand for taste-modifying agents in low-sugar products, and advancements in natural bitter masking technologies.

Growing demand for effective, clean-label bitter blockers, especially in food & beverage and pharmaceuticals, is accelerating adoption across end-uses. Advances in natural and synthetic formulations are further boosting uptake by offering more potent, versatile options. Increasing recognition of bitter blockers as critical for consumer acceptance in bitter-active compounds remains a major driver of market growth.

Key Industry Highlights:

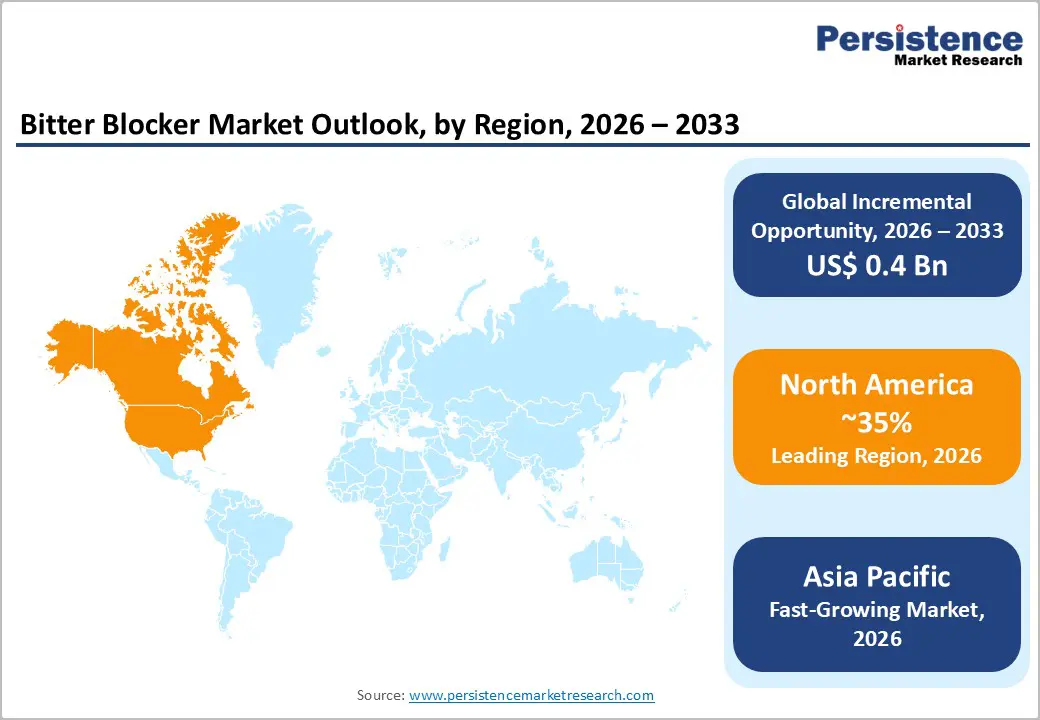

- Leading Region: North America, anticipated to account for a 35% market share in 2026, driven by advanced food R&D, high demand for low-sugar beverages, and strong innovation in the U.S.

- Fastest-growing Region: Asia Pacific, likely to be driven by rapid food processing growth, rising health-conscious consumers, and growing investments in taste enhancement in China and India.

- Dominant Product Type: Natural bitter blockers, to hold approximately 55% of the revenue share, as they provide clean-label appeal and consumer preference for plant-derived options.

- Leading Application: The food & beverage segment accounts for over 60% of the market revenue in 2026, due to masking needs in functional drinks, supplements, and low-calorie products.

- Leading End-user: The industrial segment, to contribute nearly 50% of the market revenue, due to high-volume usage in large-scale manufacturing.

| Key Insights | Details |

|---|---|

| Bitter Blocker Market Size (2026E) | US$0.6 Bn |

| Market Value Forecast (2033F) | US$1.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Functional Food Innovation and Demand for Taste-Modifying Agents

The rising preference for functional food innovation is quickly becoming a major opportunity for bitter blocker suppliers, driven by growing consumer demand for palatable, health-focused products and reduced sugar intake. Traditional bitter actives often create off-tastes, especially in low-calorie beverages and supplements, leading to lower acceptance and sales. Taste-modifying technologies, including natural blockers, synthetic agents, protein-based masks, and flavor-modulating compounds, address these concerns by offering a neutral, effective alternative. These formats simplify recipes, reduce the need for sweeteners, and are particularly effective during functional trends or clean-label markets where sensory balance is critical.

Bitter blockers significantly lower the risk of product rejection, formulation complexity, and waste, which remain major concerns in food settings. They also support improved shelf life and easier blending, especially for natural and synthetic grades, making them ideal for high-volume or premium products. As global nutrition organizations push for wider functional coverage and user-friendly agents, demand continues to expand across pharmaceuticals and other sectors.

High Development and Sensory Testing Costs

High development and sensory testing costs present a significant barrier for companies advancing next-generation bitter blockers and novel masking systems. Developing innovative grades such as natural protein blockers, synthetic high-potency agents, or multi-sensory modulators requires extensive research, specialized chemistry, and advanced flavor technologies that are far more expensive than basic additives. Sensory is an even greater challenge: many refined variants, taste-neutral lots, and stability-enhanced products are sensitive to pH, heat, and matrix interactions, requiring rigorous optimization to ensure they remain effective throughout storage and consumption. Achieving long-term performance often involves costly panel trials, sophisticated GC-MS testing, and the use of high-grade precursors, which significantly increase R&D expenditures.

Meeting stringent regulatory expectations for GRAS status, allergen declarations, and batch consistency requires multiple validation studies under various conditions and across several production batches. This adds both time and financial burden to development timelines. Scaling up manufacturing requires controlled reactors, specialized blending lines, and quality-assurance systems, further driving up overall costs. For smaller formulators, these challenges can limit innovation or delay commercialization.

Advancements in Natural and Multi-Sensory Delivery Platforms

Advancements in natural and multi-sensory bitter-blocker delivery platforms are transforming the global taste landscape by addressing two major challenges: synthetic dependence and off-taste persistence. Natural platforms are engineered to achieve plant-derived masking, reducing reliance on chemicals and enabling clean-label claims in beverages. Innovations, such as peptide blockers, enzyme inhibitors, aroma modulation, and hybrid extracts, significantly improve neutrality and reduce bitterness, lowering reformulation costs for brands and consumer campaigns.

Progress in multi-sensory platforms, including encapsulated blockers, flavor synergies, texture modifiers, and timed-release systems, supports more comprehensive masking by stimulating overall perception, the product’s first line of defense against rejection. These formats eliminate lingering aftertaste, enhance acceptance, and allow versatile use without additional sweeteners, making them highly suitable for mass functional programs. New technologies such as nano-encapsulation, bio-adhesive coatings, and VLP-based carriers further enhance efficacy and response.

Category-wise Analysis

Product Type Insights

Natural bitter blockers are anticipated to dominate the market, accounting for approximately 55% of the market share in 2026. Their dominance is driven by clean-label appeal, consumer trust, and regulatory advantages, making it preferred for functional foods. Natural bitter blockers provide effective masking, ensure safety, and contribute to premium positioning, making it suitable for large-scale beverage campaigns. TastesNatural™, which offers all-natural bitter-blocker and masking solutions for clean-label food and beverage innovations. Their proprietary natural bitter blocker technology is used to improve taste profiles of products containing caffeine, botanicals, or plant proteins, further demonstrating industry adoption of natural bitter masking solutions in premium and health-focused products.

Synthetic bitter blockers represent the fastest-growing segment, due to their potency and expanding use in pharmaceuticals. Its high-efficiency profile makes it ideal for targeted bitterness reduction, reducing dosage needs. Continuous innovations in synthesis are further strengthening their precision, driving rapid adoption across North America and Europe, where demand for economical, high-performance blockers is accelerating. DSM-Firmenich, which launched a new portfolio of taste-modulation solutions for pharmaceutical formulations that includes bitter blockers designed to target bitter taste receptors at the molecular level, helping pharmaceutical manufacturers improve palatability across dosage forms. This type of synthetic taste-blocking innovation supports rapid adoption in North America and Europe, where demand for economical, high-performance bitter-masking solutions is accelerating.

Application Insights

The food and beverage segment is expected to dominate the market, accounting for approximately 60% of revenue in 2026. This growth is driven by the need for taste modification, large-scale functional programs, and strong global demand for palatable products. The segment’s leadership continues as brands expand low-sugar product lines. Increasing adoption of pharmaceutical masking and other multi-sector initiatives underscores the growing focus on diverse applications. For instance, Symrise AG offers bitterness-blocking solutions specifically for plant-based beverages, a rapidly growing category where flavors such as pea and soy can have strong off-notes. Their specialized formula reduces bitterness, enhancing consumer taste perception and enabling the launch of low-sugar, functional drinks without compromising flavor.

The pharmaceutical segment is the fastest-growing sector, driven by increasing focus on medicine palatability and the expanding use of taste blockers in oral medications. The shift toward patient-friendly drug formulations, combined with improved adherence, is accelerating adoption. Advances in synthetic purity and the ongoing development of natural blends entering clinical trials further support market growth. For example, Senopsys, a specialist in pharmaceutical taste-masking, collaborates with major pharma companies to create palatable drug products using advanced bitter-blocking and masking technologies, such as its FlavorOpt™ Taste Masking System. These technologies are applied in both clinical and commercial formulations to mask the bitterness of challenging APIs, enhancing patient compliance, particularly in oral sprays and other dosage forms where taste is a critical barrier.

End-user Insights

The industrial segment is projected to lead the market, accounting for nearly 50% of revenue in 2026. This dominance is driven by its role as the primary hub for large-scale formulations, high-volume programs, and the management of diverse products requiring consistent taste masking. Industrial players benefit from strong integration, skilled chemists, and the capacity to handle complex or high-throughput blends. They are at the forefront of natural-ingredient rollouts and emerging synthetic-trial efforts. For example, Givaudan’s TasteSolutions® masking platforms are widely used by multinational food and beverage companies to address off-flavors in functional beverages and high-protein formulations, ensuring consistent taste profiles at scale. These industrial-grade solutions are supported by extensive R&D and formulation expertise, enabling efficient product launches in global markets.

The consumer segment is expected to be the fastest-growing, fueled by its strong DIY presence and use in direct-to-consumer products. These solutions offer convenient, quick, and accessible taste masking, appealing to users in home or low-effort settings. Expanded outreach, health-focused initiatives, and broader availability of routine and premium blockers are accelerating adoption in urban and semi-urban areas. For instance, Nexxus Foods’ Bitter Masking System - NX 0611, available in small 150 g samples, allows home formulators and hobbyists to reduce bitterness in homemade beverages or food products without industrial expertise, serving as a clear example of direct-to-consumer bitter blockers for everyday use.

Regional Insights

North America Bitter Blocker Market Trends

North America is expected to lead the global bitter blocker market, representing nearly 35% of revenue in 2026. This leadership is supported by the region’s advanced food infrastructure, strong R&D capabilities, and high public awareness of functional benefits. Processing systems in the U.S. and Canada facilitate extensive taste-masking programs, ensuring broad accessibility of bitter blockers across food and beverage, pharmaceutical, and other applications. Rising demand for natural, convenient, and easy-to-use formats is further driving adoption, as these solutions enhance consumer acceptance and reduce barriers associated with bitter-active ingredients.

Advancements in bitter blocker technology, such as stable natural extracts, enhanced synthetic delivery systems, and targeted multi-sensory solutions, are driving significant investments from both public and private sectors. Government initiatives and clean-label campaigns are promoting their use to address sugar reduction, off-flavors, and emerging health concerns, sustaining strong market demand. Increased focus on pharmaceutical-grade and specialty applications, particularly for consumer products and other niches, is further expanding the range of uses for bitter blockers.

Europe Bitter Blocker Market Trends

Europe’s bitter blocker market is supported by increasing awareness of taste benefits, robust food systems, and government-led health initiatives. Countries such as Germany, France, and the U.K. have well-established nutrition frameworks that encourage routine taste masking and adoption of innovative blocker delivery methods. These formulations are particularly valued by food manufacturers, health-conscious consumers, and pharmaceutical users, improving compliance and coverage.

Technological advancements, such as higher-potency natural extracts, application-specific delivery systems, and improved synthetic grades, are further enhancing market potential. European authorities are actively supporting research and trials for both routine and specialized applications, strengthening market confidence. The rising demand for convenient, clean-label solutions aligns with the region’s emphasis on preventive nutrition and sugar reduction. Public awareness campaigns and promotional initiatives are expanding reach across urban and rural areas, while suppliers continue to invest in novel chemistries and formulation variants to improve efficacy.

Asia Pacific Bitter Blocker Market Trends

Asia Pacific is expected to be the fastest-growing market for bitter blockers, driven by rising health awareness, expanding government initiatives, and broader application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting blocker campaigns to support the growth of functional products and emerging pharmaceutical needs. Bitter blockers are particularly appealing in these markets due to their versatile administration, scalability, and suitability for large-scale beverage programs in both urban and rural areas.

Technological advancements are enabling the development of stable, effective, and user-friendly bitter blockers that can withstand challenging production conditions while minimizing off-flavors. These innovations are essential for reaching remote facilities and enhancing overall acceptance. Increasing demand across food and beverage, pharmaceutical, and other applications is fueling market expansion. Public-private partnerships, higher health expenditure, and growing investments in masking research and manufacturing capacity are also accelerating growth. The combination of convenient delivery, improved palatability, and reduced risk of rejection positions bitter blockers as a preferred solution in the region.

Competitive Landscape

The global bitter blocker market features competition between established flavor leaders and emerging taste modulators. In North America and Europe, ADM and BASF lead through strong R&D, distribution networks, and industry ties, bolstered by innovative grades and masking programs. In Asia Pacific, Givaudan SA advances with localized solutions, enhancing accessibility. Multi-sensory delivery boosts acceptance, cuts rejection risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Natural formulations solve synthetic issues, aiding penetration in clean-label areas.

Key Industry Developments

- In July 2025, Biospringer by Lesaffre advanced flavor innovation through its yeast-based ingredients to manage intense sensory profiles in foods. Its fermentation-derived Springer Mask 102 was developed to block bitterness and neutralize off-notes in alternative sweeteners, while Maxarome Prime yeast extract was designed to enhance flavors by boosting umami, meaty, and salty notes in savory applications.

- In March 2024, Symrise AG announced a partnership with a leading pharmaceutical company to develop taste-masking solutions for pediatric medications. The collaboration focuses on improving patient compliance by creating palatable formulations that address the challenges of bitter-tasting drugs.

Companies Covered in Bitter Blocker Market

- ADM

- BASF

- Blue California

- Cargill, Inc.

- Döhler

- dsm-firmenich

- DuPont de Nemours, Inc.

- Givaudan SA

- Kerry Group plc

- Symrise AG

- Tate & Lyle PLC

- Sensient Technologies Corporation

Frequently Asked Questions

The global bitter blocker market is projected to reach US$0.6 billion in 2026.

The rising prevalence of functional food innovation and demand for taste-modifying agents are key drivers.

The bitter blocker market is poised to witness a CAGR of 8.7% from 2026 to 2033.

Advancements in natural and multi-sensory delivery platforms are key opportunities.

ADM, BASF, Cargill, Inc., DSM-Firmenich, and Givaudan SA are the key players.