- Beverages

- Aromatic Bitters Market

Aromatic Bitters Market Size, Share, and Growth Forecast, 2026 - 2033

Aromatic bitters market by Source (Herbs, Spices, Fruit Peels), Application (Beverages, Whiskey, Cocktail, Rum, Tequila, Household), Distribution Channel (Direct, Indirect), and Regional Analysis for 2026 – 2033

Aromatic Bitters Market Size and Trends Analysis

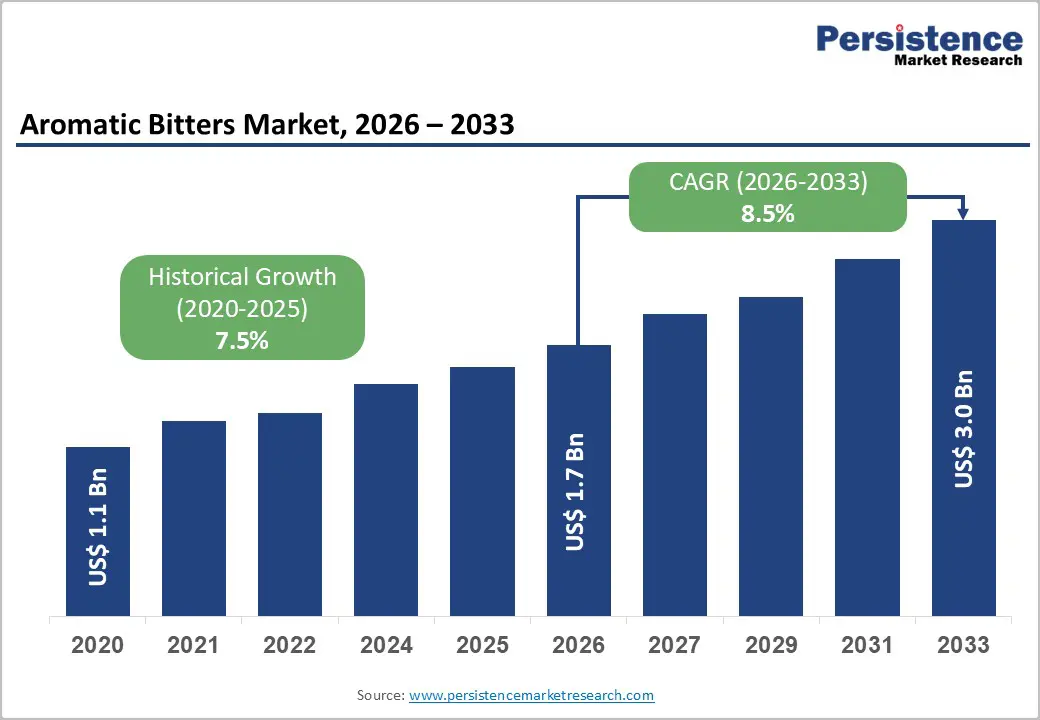

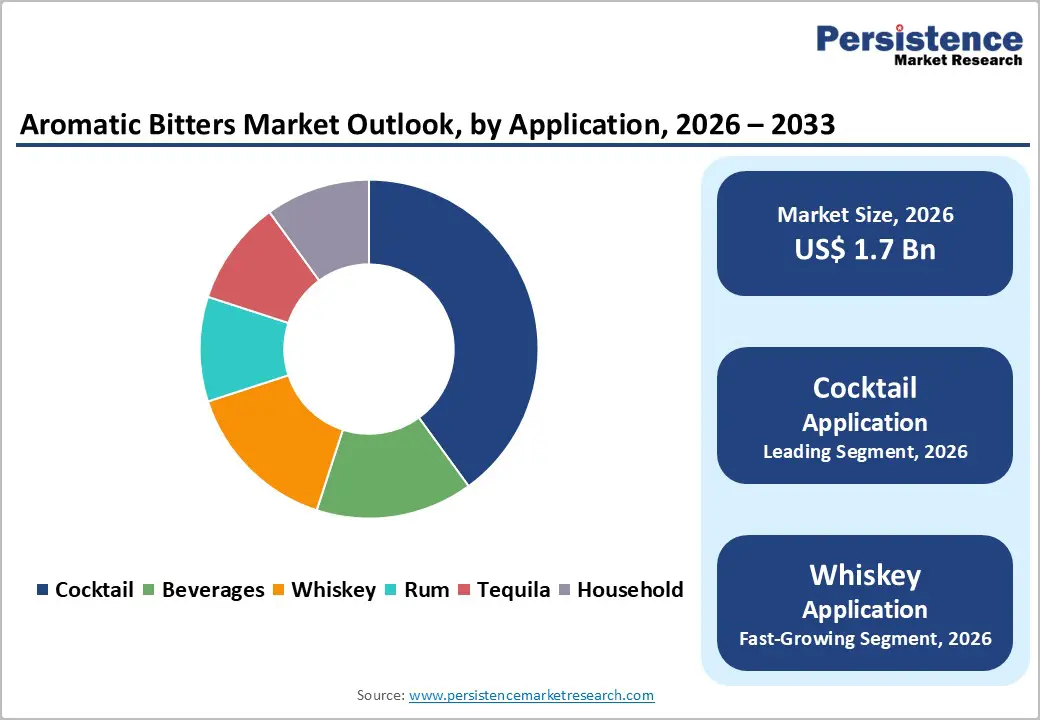

The global aromatic bitters market size is likely to be valued at US$1.7 billion in 2026, and is expected to reach US$3.0 billion by 2033, growing at a CAGR of 8.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of craft cocktail culture, rising home bartending trends, and growing demand for premium flavor-enhancing bitters in whiskey, rum, and tequila-based drinks.

The growing demand for high-quality, small-batch aromatic bitters, particularly herb- and spice-based varieties, is driving adoption in both on-premise and off-premise channels. Advances in natural extract concentration and clean-label formulations are enhancing aroma intensity and regulatory compliance. The increasing recognition of bitters as essential for cocktail complexity and flavor balance is fueling market growth, particularly in premium mixology and spirits markets.

Key Industry Highlights:

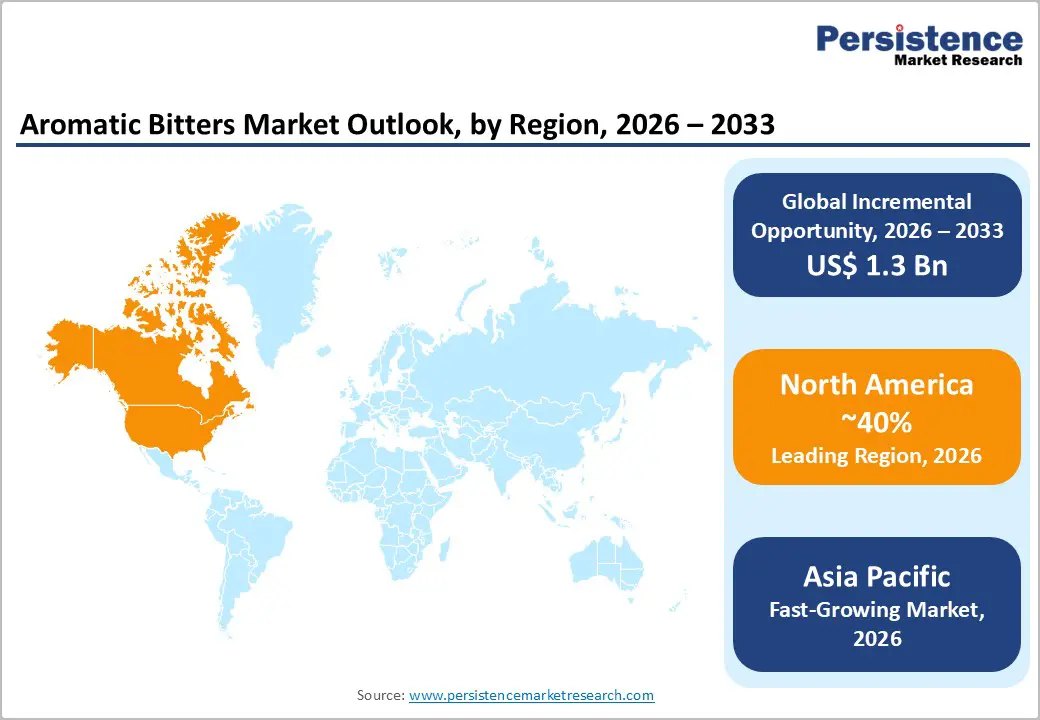

- Leading Region: North America, anticipated to account for a 40% market share in 2026, driven by a dominant craft cocktail scene, high whiskey & cocktail consumption, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by a rapid rise in western-style cocktail bars, expanding premium spirits consumption, and growing mixology culture in China, India, and Japan.

- Dominant Source: Herbs, to hold approximately 48% of the market share, as herb-based bitters remain the core of classic cocktail profiles.

- Leading Application: Cocktail, to contribute nearly 52% of the market revenue, due to the highest usage in bar and home mixology.

| Key Insights | Details |

|---|---|

| Aromatic Bitters Market Size (2026E) | US$1.7 Bn |

| Market Value Forecast (2033F) | US$3.0 Bn |

| Projected Growth CAGR (2026-2033) | 8.5% |

| Historical Market Growth (2020-2025) | 7.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Surge in Craft Cocktail Culture and Home Bartending

The surge in craft cocktail culture and home bartending reflects a broader shift toward personalized, experience-driven consumption. Consumers are no longer satisfied with standard mixed drinks; instead, they are exploring complex flavor profiles, premium spirits, artisanal mixers, and fresh, locally inspired ingredients. Social media, digital recipe platforms, and video tutorials have played a major role in demystifying cocktail preparation, encouraging experimentation and skill-building at home. Home bartending has evolved from a casual hobby into a creative ritual, where presentation, glassware, and technique matter as much as taste.

This trend has also been fueled by changing social dynamics. Smaller gatherings and at-home entertaining have increased the appeal of crafting high-quality drinks without relying on bars or restaurants. Consumers are investing in bar tools, specialty bitters, syrups, and infused spirits, treating cocktails as an extension of culinary expression. There is also growing interest in low-alcohol and alcohol-free craft cocktails, aligning with wellness-focused lifestyles while preserving the sophistication of mixology.

Rising Premium Spirits Consumption in Emerging Markets

Rising premium spirits consumption in emerging markets is driven by a combination of economic, cultural, and social shifts. As disposable incomes grow in countries across Asia, Latin America, and Africa, more consumers are trading up from basic, low-cost alcoholic beverages to higher-quality, well-branded spirits. This reflects not just greater spending power, but also a desire for status, sophistication, and new experiences. Premium spirits often symbolize modernity and success, and choosing them can be a way for emerging-market consumers to signal personal achievement or global awareness.

Urbanization and exposure to global lifestyles through travel, media, and digital platforms are expanding tastes and expectations around drinks. Younger adult consumers are increasingly curious about varietals, provenance, and the craftsmanship behind spirits, whether that’s a single-malt whisky, artisanal rum, or a boutique gin. This elevated interest is further supported by more dynamic hospitality sectors, high-end bars, lounges, and restaurants that curate premium spirit offerings and educate patrons through tasting events and creative cocktails.

Barrier Analysis – Regulatory Complexity and Alcohol-Content Restrictions

Regulatory complexity and alcohol-content restrictions significantly shape how alcoholic beverages are produced, marketed, and consumed, often creating both challenges and unintended outcomes for consumers and businesses alike. Governments impose varied rules around alcohol content, labeling, advertising, taxation, and distribution to address public health concerns, cultural norms, and safety priorities. In many regions, especially where alcohol carries social or religious sensitivities, authorities set strict limits on the allowable percentage of alcohol in beverages or prohibit certain products altogether. These restrictions can fragment markets, forcing producers to tailor formulations and packaging to meet local thresholds, which increases complexity and cost.

Compliance with diverse regulations, such as mandatory health warnings, age verification requirements, or limits on where and when alcohol can be sold, adds layers of administrative burden. Small and medium producers often find it especially difficult to navigate overlapping rules across jurisdictions, slowing product rollouts and innovation. For consumers, regulatory patchwork can lead to inconsistencies in product availability and price disparities, influencing purchasing behavior and sometimes driving demand toward informal or unregulated alternatives.

Intense Competition from Low-Cost Private-Label and Counterfeit Products

Intense competition from low-cost private-label and counterfeit products has reshaped the beverage landscape, pressured established brands, and shifted consumer behavior. Retailers and supermarkets increasingly promote private-label alcoholic beverages as value alternatives, often priced significantly lower than mainstream brands. These products appeal especially during economic uncertainty, when consumers prioritize affordability without wanting to forego social drinking occasions. Because private-label offerings typically have lower marketing and distribution costs, they can undercut branded products on price while still delivering acceptable taste and quality, making them attractive for cost-conscious buyers.

Counterfeit spirits and illicit alcohol have proliferated in some regions, fueled by gaps in enforcement and high tax and regulatory burdens that make legitimate products expensive. Counterfeiters mimic packaging and branding to deceive buyers, which can erode trust in authentic products and damage brand equity. Beyond financial losses for legitimate producers, counterfeit alcohol poses significant health risks, as unregulated production often lacks safety controls.

Opportunity Analysis – Growth in Low- & Non-Alcoholic Bitters and Clean-Label Formulations

Growth in low- and non-alcoholic bitters and clean-label formulations reflects a broader shift in consumer values around health, transparency, and sensory exploration. Bitters, once a niche ingredient primarily used in traditional cocktails, are being reinvented to serve modern lifestyles that emphasize moderation without sacrificing complexity of flavor. Producers are crafting bitters and cocktail enhancers that deliver botanical depth, nuanced bitterness, and aromatic lift while keeping alcohol content minimal or nonexistent. This trend allows home bartenders and hospitality venues to create sophisticated drinks that cater to guests who are sober curious, reducing intake, or simply seeking refreshing alternatives.

Clean-label formulations amplify this movement by foregrounding recognizable, natural ingredients and streamlined production processes. Consumers are scrutinizing labels more than ever, rejecting artificial colors, synthetic flavors, and preservatives in favor of products with clear origins and straightforward ingredient lists. Bitters made with herbs, roots, spices, and citrus peels not only fit this aesthetic but also align with wellness-oriented narratives around plant-derived botanicals and functional benefits, such as digestive support.

Expansion in Asia Pacific Cocktail Culture and Premium Spirits

Expansion in Asia Pacific cocktail culture and premium spirits reflects a dynamic blend of economic growth, evolving tastes, and cultural exchange. Rapid urbanization and rising disposable incomes have empowered a growing middle class to explore beyond traditional beverages, seeking out elevated drinking experiences. Instead of sticking to standard local liquors or inexpensive mixed drinks, many consumers, especially in major cities such as Shanghai, Singapore, Seoul, and Mumbai, are embracing craft cocktails as a symbol of modernity and leisure. This curiosity has encouraged bars and lounges to innovate, blending regional ingredients with global techniques to create drinks that feel both locally rooted and cosmopolitan.

Exposure to international travel, digital media, and social platforms has familiarized consumers with cocktail trends from around the world, inspiring local bartenders to adopt and reinterpret styles such as molecular mixology, barrel-aged serves, and artisanal infusions. These experiences, shared online, reinforce cocktail culture as something trendy, expressive, and socially shareable.

Category-wise Analysis

Source Insights

Herbs are anticipated to dominate the market, accounting for approximately 48% of the market share in 2026. Its dominance is driven by its versatility, natural appeal, and strong alignment with evolving consumer preferences. Herbal ingredients are widely valued for their ability to deliver complex flavors, aromas, and functional benefits without relying on artificial additives. Their deep roots in traditional remedies and culinary practices enhance consumer trust and acceptance across regions. In addition, growing demand for clean-label, plant-based, and wellness-oriented products has accelerated the use of herbs in beverages, food, and personal care applications. Wong Lo Kat is one of China’s best-selling herbal tea brands. Founded in the 19th century, Wong Lo Kat’s products are formulated primarily from a blend of traditional herbal ingredients such as chrysanthemum, licorice, and other botanicals, and are widely consumed for both taste and perceived health benefits.

Spices represent the fastest-growing source, due to tapping into rising consumer interest in bold, diverse, and culturally inspired flavors. Unlike traditional ingredients, spices bring distinctive sensory profiles such as heat from chili, warmth from cinnamon, or earthiness from turmeric that enhance complexity without adding sugar or artificial additives. Their association with culinary authenticity and global cuisines makes them especially appealing in beverages, snacks, and wellness products. Lahori Zeera, an Indian beverage brand by Archian Foods Pvt. Ltd., which has built a 300 + crore (over US$3.6 billion) business around a spiced soft drink. The company’s flagship Lahori Zeera drink incorporates traditional spices such as cumin (zeera), black pepper, ginger, and rock salt into a fizzy beverage, differentiating it from regular sodas and resonating strongly with health- and flavor-oriented consumers.

Application Insights

Cocktails are expected to dominate the market, contributing nearly 52% of revenue in 2026, as consumer preferences continue to shift toward premium, experience-led drinking occasions. Cocktails offer versatility in flavor, format, and presentation, allowing brands and venues to cater to diverse tastes, from classic recipes to innovative, ingredient-driven creations. The rise of home bartending, social media influence, and cocktail-focused bars has further amplified demand. In addition, cocktails enable the use of premium spirits, botanicals, and mixers, increasing average spend per serving. ready-to-drink (RTD) cocktail portfolio from Bacardi Limited. Bacardi has been actively expanding its premixed cocktail offerings under brands such as BACARDÍ Real Rum Canned Cocktails, which are positioned as convenient, premium spirit-based beverages that appeal to consumers seeking bar-quality drinks without the preparation work. This strategy has helped Bacardi capture a significant share of the growing RTD cocktail segment, which is already a dominant revenue driver within overall cocktail sales globally.

Whiskey represents the fastest-growing application, reflecting its widening appeal across demographics, cultures, and consumption occasions. Consumers are increasingly drawn to whiskey for its rich flavor complexity, premium image, and diverse styles from smooth Irish and bourbon to smoky Scotch and innovative single malts. Whiskey also lends itself well to both traditional and contemporary cocktails, increasing its versatility in bars and at home. As disposable incomes rise in key markets, buyers are trading up to aged and craft expressions. Indri–Trini single malt whisky by Piccadilly Agro Industries. After its launch, Indri quickly became one of the fastest-growing single malt whisky brands globally, selling around 170,000 cases worldwide and expanding into major export markets such as the U.S., the U.K., and Australia.

Regional Insights

North America Aromatic Bitters Market Trends

North America is projected to dominate, account for nearly 40% revenue in 2026, driven by the region’s dominant craft cocktail culture, strong whiskey & spirits consumption, and high public awareness of premium mixology benefits. Distribution systems in the U.S. and Canada provide extensive support for aromatic bitters programs, ensuring wide accessibility across herb-based, cocktail, and indirect populations. Increasing demand for small-batch, convenient, and easy-to-use forms is further accelerating adoption, as these formats improve flavor complexity and reduce barriers associated with basic bitters.

Innovation in aromatic bitters technology, including stable spice-forward, improved clean-label delivery, and targeted whiskey enhancement, is attracting significant investment from both public and private sectors. Government initiatives and TTB campaigns continue to promote use against flavor risks, cocktail creativity concerns, and emerging premiumization threats, creating sustained market demand. The growing focus on tequila grades and specialty uses, particularly for cocktails and others, is expanding the target applications for aromatic bitters.

Europe Aromatic Bitters Market Trends

Europe is increasing awareness of cocktail heritage and premium spirits benefits, strong regulatory systems, and government-led gastronomy programs. Countries such as the U.K., Germany, France, and Italy have well-established bar and spirits frameworks that support routine aromatic bitters use and encourage adoption of innovative flavor delivery methods, including herb- and spice-based solutions. These high-quality formulations are particularly appealing for cocktail populations, regulation-conscious bars, and whiskey users, improving complexity and coverage rates.

Technological advancements in aromatic bitters development, such as enhanced botanical extraction, application-targeted delivery, and improved two-toned grades, are further boosting market potential. European authorities are increasingly supporting research and trials for bitters against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, authentic options is aligned with the region’s focus on preventive flavor enhancement and cocktail tourism. Public awareness campaigns and promotion drives are expanding reach in both on-premise and off-premise segments, while suppliers are investing in production and novel variants to increase efficacy.

Asia Pacific Aromatic Bitters Market Trends

Asia Pacific is likely to be the fastest-growing market for aromatic bitters in 2026, driven by rising cocktail culture awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting bitters campaigns to address Western drinking growth and emerging mixology needs. Aromatic bitters are particularly attractive in these regions due to their cost-effective administration, ease of integration, and suitability for large-scale cocktail and whiskey drives in both urban and semi-urban populations.

Technological advancements are supporting the development of stable, effective, and easy-to-use aromatic bitters, which can withstand challenging storage conditions and minimize flavor dependence. These innovations are critical for reaching domestic bars and improving overall cocktail coverage. Growing demand for herb-based, cocktail, and indirect applications is contributing to market expansion. Public-private partnerships, increased premium spirits expenditure, and rising investment in bitters research and distribution capacity are further accelerating growth. The convenience of bitters delivery, combined with improved complexity and reduced risk of flat drinks, positions it as a preferred choice.

Competitive Landscape

The global aromatic bitters market is shaped by intense competition between long-established heritage brands and fast-growing craft producers, creating a dynamic and innovation-driven landscape. In North America and Europe, brands such as House of Angostura and The Bitter Truth maintain leadership through deep-rooted brand recognition, extensive distribution networks, and long-standing relationships with professional bartenders and hospitality groups. Their market position is further reinforced by continuous innovation in herb- and spice-based formulations, which preserve classic flavor profiles while supporting modern cocktail creativity.

In the Asia Pacific region, emerging and regional players are gaining momentum by introducing localized flavor solutions that reflect regional palates, botanicals, and cultural preferences. This localization strategy improves consumer accessibility and accelerates adoption in both on-trade and home-mixology channels. Herb-based delivery formats remain central to the category, as they enhance authenticity, reduce formulation risk, and allow seamless integration across a wide range of classic and contemporary cocktails.

Key Industry Developments

- In July 2025, Australia’s first locally produced cocktail bitters brand announced the official launch of its Aromatic and Orange Bitters in London, with the two award-winning flavors introduced to both on-trade and off-trade channels during the month. The launch followed successful entries in the U.S., where brand visibility was strengthened through workshops held at Tales of the Cocktail in New Orleans, hosted by bar entrepreneur and London Cocktail Club founder JJ Goodman. After expansion into several global markets, the U.K. debut was positioned as a strategic move, marking the brand’s entry into one of the world’s most influential beverage markets.

- In January 2025, Dan Leese, CEO of Hotaling & Co, stated that Hotaling’s first-ever line of bitters was launched in partnership with Luxardo, a long-established pioneer in cocktail culture, with the collaboration positioned to strengthen both companies’ leadership in the cocktail segment. It was highlighted that the bitters were introduced as a low-ABV option, featuring five distinct variations of Bitters and Soda drinks, designed to meet growing demand for flavorful yet lower-alcohol beverage choices.

Companies Covered in Aromatic Bitters Market

- House of Angostura

- Strongwater LLC

- Hella Cocktail Co.

- Fee Brothers

- Peychaud's Bitters

- Dashfire Bitters

- The Bitter Truth

- Wild Turkey

- Jack Daniel's

- Noilly Prat

Frequently Asked Questions

The global aromatic bitters market is projected to reach US$1.7 billion in 2026.

Growing interest in craft cocktails, premium spirits, and experiential drinking is driving demand for high-quality bitters and flavor enhancers across bars, restaurants, and home bartending.

The aromatic bitters market is poised to witness a CAGR of 8.5% from 2026 to 2033.

Increasing demand for mindful drinking and convenience opens opportunities for alcohol-free bitters, low-ABV formulations, and ready-to-drink bitters-based beverages targeting both home consumers and on-trade channels.

House of Angostura, The Bitter Truth, Fee Brothers, Peychaud's Bitters, and Hella Cocktail Co. are the key players.