- Hardware & Software IT Services

- Bare Metal Cloud Market

Bare Metal Cloud Market Size, Share, and Growth Forecast 2026 – 2033

Bare Metal Cloud Market by Component (Bare Metal Cloud Servers, and Services), by Enterprise Size (Large Enterprises, Small & Medium-sized Enterprises, and Micro Businesses), by End User (BFSI, Manufacturing, Government, IT and Telecom, Media and Entertainment, Healthcare, and Others), by Regional Analysis, 2026–2033

Bare Metal Cloud Market Size and Trend Analysis

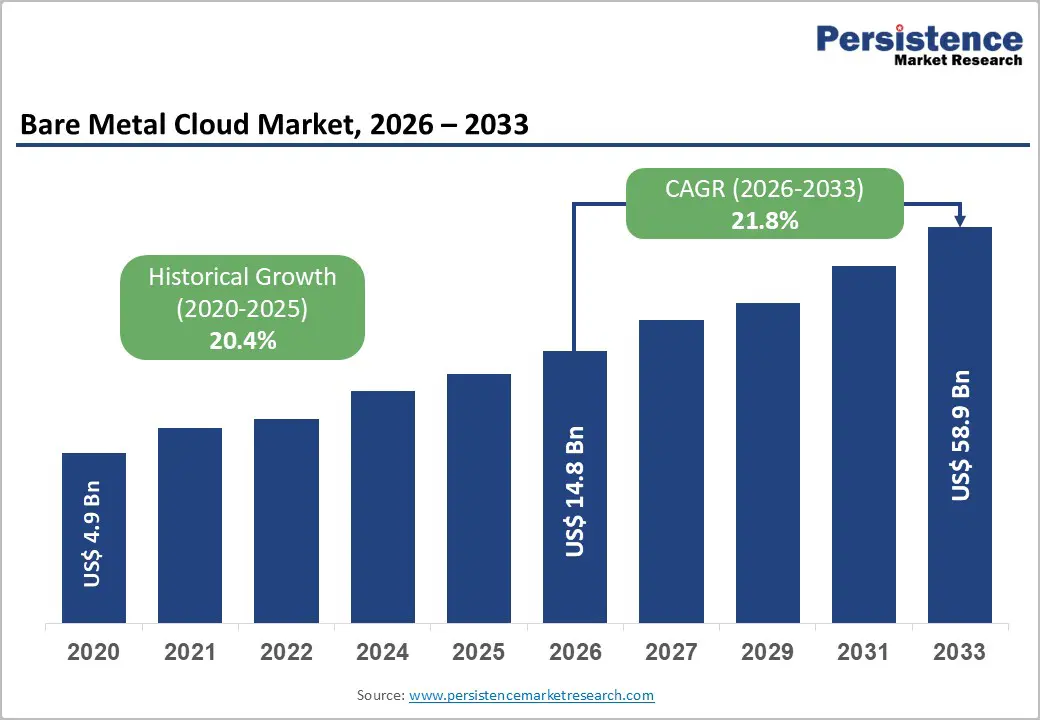

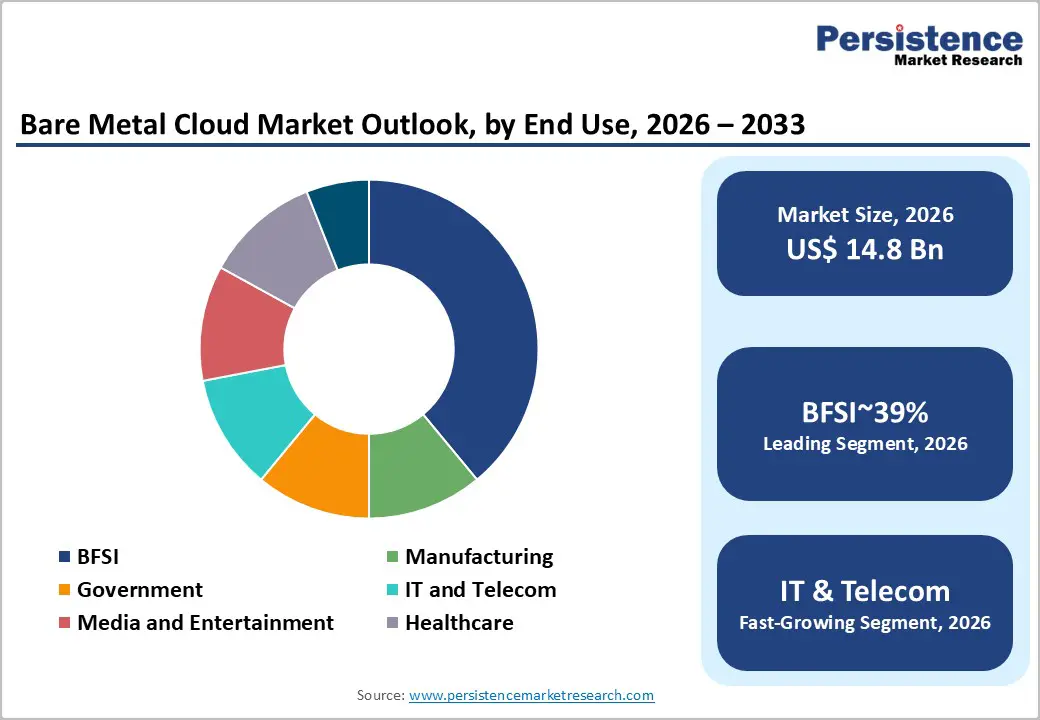

The global Bare Metal Cloud Market size is likely to be valued at US$ 14.8 Billion in 2026 and is expected to reach US$ 58.9 Billion by 2033, growing at a CAGR of 21.8% during the forecast period from 2026 and 2033. The market’s strong expansion is underpinned by surging adoption of high-performance computing, latency-sensitive applications, and AI/ML workloads that demand direct access to physical servers without virtualization overhead.

Key Market Highlights

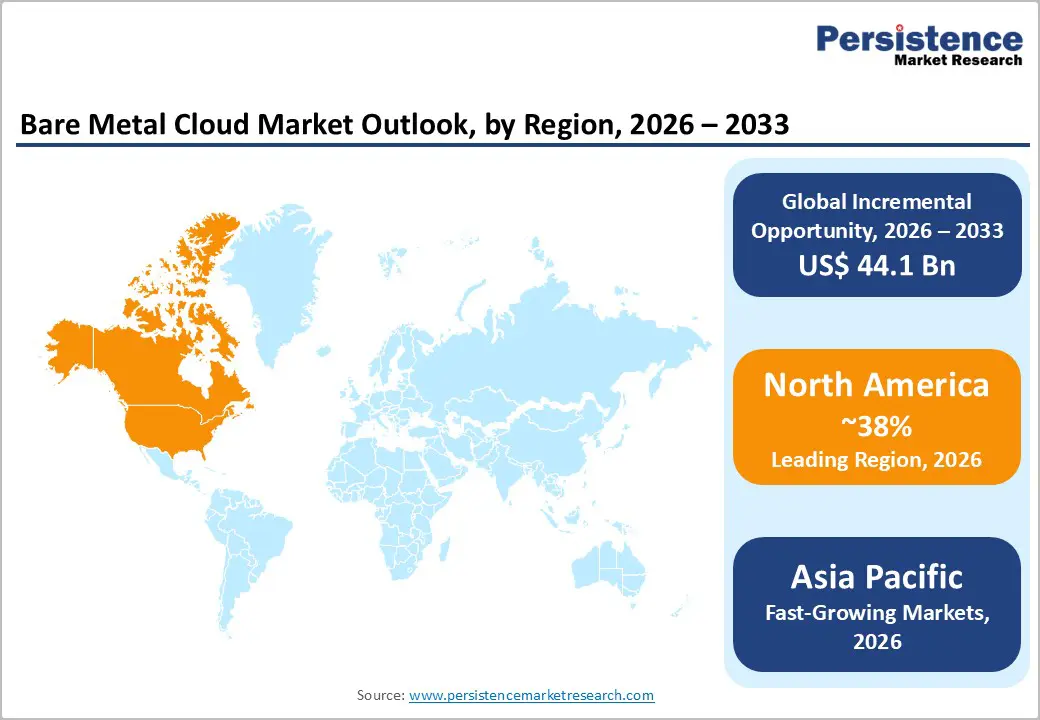

- Leading region: North America dominates the Bare Metal Cloud Market holding 38% share, supported by advanced cloud infrastructure, strong enterprise IT spending, and early adoption of AI, analytics, and latency-sensitive workloads across BFSI, media, and technology industries.

- Fastest-growing region: Asia Pacific is the fastest-growing regional market with rising CAGR of 24.5%, driven by rapid digitalization in China, Japan, India, and ASEAN, booming e-commerce and fintech ecosystems, and strong manufacturing-led adoption of high-performance cloud infrastructure.

- Dominant segment: By end user, BFSI is the leading segment, accounting for a 39% share of deployments as banks and insurers rely on dedicated bare metal servers for secure, low-latency transaction processing, real-time risk analytics, and stringent regulatory compliance.

- Fastest-growing segment: Within enterprise size, Small & Medium-sized Enterprises are emerging as the fastest-growing segment of 25.8% CAGR, supported by more affordable bare metal offerings, flexible pricing models, and managed services that lower skill barriers and enable enterprise-grade performance.

- Key market opportunity: Expanding AI/ML and edge computing ecosystems create major opportunities for providers offering GPU-optimized, edge-proximate bare metal platforms bundled with strong API Integration and Deployment and managed services tailored to industry-specific use cases.

| Key Insights | Details |

|---|---|

| Bare Metal Cloud Market Size (2026E) | US$ 14.8 Billion |

| Market Value Forecast (2033F) | US$ 58.9 Billion |

| Projected Growth CAGR (2026–2033) | 21.8% |

| Historical Market Growth (2020–2025) | 20.4% |

Market Dynamics

Market Growth Drivers

Rising High-Performance and Latency-Sensitive Workloads

Enterprises are rapidly deploying workloads such as AI/ML, real-time analytics, and high-frequency transaction processing that require deterministic performance and ultra-low latency. Bare metal cloud servers eliminate the hypervisor layer, reducing latency and improving throughput, making them ideal for such use cases. Industry analyses indicate that a growing share of cloud budgets is being allocated to performance-optimized infrastructure, with dedicated environments increasingly preferred for large databases and in-memory computing.

In BFSI, for instance, real-time risk analytics and fraud detection demand millisecond-level response times, which bare metal environments support more efficiently than shared virtualized instances. This structural shift toward performance-centric architectures strongly reinforces demand for Bare Metal Cloud Servers and associated Support and Maintenance services.

Growing Adoption in Regulated and Security-Sensitive Industries

Sectors handling sensitive data are turning to bare metal cloud to combine cloud agility with tighter control over physical resources. Financial institutions, healthcare providers, and government agencies must comply with stringent frameworks such as GDPR, PCI-DSS, and sector-specific cybersecurity regulations, which favor dedicated, single-tenant infrastructure. Bare metal cloud enables organizations to deploy custom security controls, dedicated firewalls, and encryption frameworks while retaining auditability at the hardware level.

In banking and insurance, dedicated servers reduce multitenancy risks and support secure connectivity to on-premise systems. Hospitals and healthcare networks leverage bare metal for clinical applications, medical imaging, and electronic health records that require predictable performance and robust data protection. This compliance-driven shift from traditional hosting and shared clouds toward dedicated cloud infrastructure significantly propels market growth.

Market Restraints

High Upfront Cost and Operational Complexity for Smaller Customers

Despite its benefits, bare metal cloud can involve higher minimum commitments and configuration complexity compared with commodity virtual instances. Small and micro businesses often lack in-house expertise to manage OS-level tuning, security hardening, and workload placement on dedicated hardware.

While managed Business Consulting and Support and Maintenance services are emerging, cost sensitivity among Small & Medium-sized Enterprises can slow adoption, especially in regions where generic public cloud instances are aggressively priced. This cost-to-complexity equation restrains penetration among price-conscious customers that do not yet require high-performance or compliance-grade environments.

Skill Gaps and Integration Challenges in Hybrid Architectures

The transition to bare metal cloud, particularly within hybrid and multi-cloud strategies, demands skilled teams capable of managing infrastructure automation, API Integration and Deployment, and network architecture. Many enterprises face shortages of cloud-native and DevOps skills, making it challenging to fully exploit bare metal capabilities such as infrastructure-as-code, advanced observability, and optimized workload scheduling.

Integration with legacy data centers, security tools, and compliance monitoring systems can further complicate deployments. These skill and integration hurdles can elongate implementation timelines and discourage risk-averse organizations from aggressively scaling their bare metal cloud footprint.

Market Opportunities

Expansion of AI/ML, HPC, and GPU-Optimized Bare Metal Platforms

Vendors are increasingly rolling out GPU-accelerated bare metal instances tailored to AI training, inference, and high-performance computing workloads. Hyperscalers and specialized providers are introducing configurations with the latest CPU and GPU architectures, high-bandwidth memory, and fast NVMe storage to support large language models, complex simulations, and scientific computing.

As AI investment continues to surge across industries, enterprises are seeking environments that provide predictable performance and efficient resource utilization at scale. Bare metal GPU clusters allow organizations to deploy tightly coupled compute nodes with minimal virtualization overhead, accelerating time-to-insight. This creates significant opportunity for providers that can bundle Bare Metal Cloud Servers with managed MLOps stacks, AI frameworks, and specialized Support and Maintenance services designed for data-intensive workloads.

Rising Edge Computing and Industry-Specific Bare Metal Solutions

The proliferation of IoT, 5G networks, and distributed applications is driving demand for edge-proximate compute infrastructure. Bare metal cloud deployed in regional and edge data centers enables low-latency processing for use cases such as real-time video analytics, smart manufacturing, connected vehicles, and digital retail experiences. Providers are increasingly offering industry-specific bare metal solutions, such as hardened platforms for Manufacturing environments or high-bandwidth configurations for Media and Entertainment streaming and content delivery.

As enterprises re-architect applications for edge and hybrid scenarios, tailored bare metal offerings, integrated via robust API Integration and Deployment frameworks, will capture a growing share of these new workloads, creating attractive long-term revenue pools for market participants.

Category wise Insights

Component Analysis

Within components, Bare Metal Cloud Servers account for an estimated around 60% share of total market revenues, reflecting the central role of dedicated compute infrastructure in this domain. Enterprises prioritize direct server access to run mission-critical databases, container platforms, and AI pipelines with full control over CPU, memory, and storage configurations. Industry data indicates that a rising proportion of performance-sensitive cloud spending is directed toward single-tenant servers to avoid noisy-neighbor effects and virtualization overhead.

This preference is particularly strong in BFSI, IT and Telecom, and Healthcare, where predictable performance and isolation are mandatory. Service layers such as API Integration and Deployment, Business Consulting, and Support and Maintenance are growing quickly, yet they are largely built around and dependent on the foundational demand for robust bare metal server platforms, reinforcing servers’ dominant revenue contribution.

Enterprise Size Analysis

By enterprise size, Large Enterprises represent the leading customer group, accounting for an estimated close to 60% market share. Large organizations typically manage complex application portfolios, global user bases, and stringent compliance obligations, all of which benefit from dedicated bare metal infrastructure. These enterprises are more likely to operate hybrid and multi-cloud strategies, using bare metal for performance-critical workloads while retaining virtualized capacity for general-purpose applications.

Their substantial IT budgets and mature DevOps capabilities enable them to exploit advanced configurations, automation frameworks, and Business Consulting engagements to optimize infrastructure usage. In sectors such as global banking, telecom carriers, and multinational manufacturers, large enterprises are standardizing on bare metal nodes as a core building block for high-performance private and public cloud architectures, cementing their leadership in overall market demand.

End User Analysis

BFSI as the Leading End-User Segment

Among end users, BFSI holds a leading share, estimated at approximately around 39% of the bare metal cloud demand. Financial institutions manage massive volumes of sensitive transaction data and rely on real-time processing for trading, payments, risk modeling, and fraud detection. These workloads require ultra-low latency, deterministic performance, and robust security—attributes strongly aligned with bare metal cloud infrastructure. Dedicated servers support compliance with financial regulations and data-residency obligations, while enabling banks and insurers to customize encryption, key management, and network segmentation.

The rapid adoption of advanced analytics and AI-driven services, such as algorithmic trading and personalized financial products, further pushes BFSI players toward high-performance bare metal environments. As digital banking and instant payment systems scale worldwide, BFSI is expected to remain the anchor vertical for bare metal cloud investments.

Regional Insights

North America Bare Metal Cloud Market Trends

North America represents the most mature Bare Metal Cloud Market, underpinned by strong cloud adoption, deep enterprise IT spending, and a dense ecosystem of data centers and interconnection hubs. The U.S. leads regional demand, with hyperscale providers and specialist bare metal vendors offering extensive footprints and advanced configurations for AI, big data, and SaaS workloads. Financial services, media streaming, and hyperscale internet platforms are among the earliest adopters of GPU-accelerated bare metal nodes for latency-sensitive and high-throughput use cases.

Regulatory frameworks emphasizing data protection and sector-specific compliance, particularly in BFSI and healthcare, reinforce the preference for single-tenant cloud infrastructure. The region’s strong innovation ecosystem—spanning silicon vendors, cloud-native software providers, and networking specialists—supports rapid iteration in bare metal offerings, including edge-proximate deployments and tightly integrated API Integration and Deployment toolchains. As enterprises in the U.S. and Canada deepen hybrid and multi-cloud strategies, North America is expected to retain its leadership position in both adoption scale and solution maturity.

Europe Bare Metal Cloud Market Trends

Europe’s Bare Metal Cloud Market is shaped by stringent data-protection regulations and growing emphasis on digital sovereignty. Countries such as Germany, the U.K., France, and Spain are witnessing rising demand for sovereign and regionally hosted bare metal infrastructure that complies with frameworks like GDPR and sector-specific guidelines in finance and public services. European cloud providers and global players operating local data centers increasingly position bare metal platforms as a secure, compliant alternative to multitenant public cloud for sensitive workloads.

Regulatory harmonization across the European Union, combined with initiatives around trusted and federated cloud infrastructures, encourages enterprises to adopt dedicated infrastructure for critical data and analytics. Manufacturing, automotive, and industrial companies in Germany and France are expanding use of high-performance bare metal environments to run digital twins, IoT analytics, and engineering simulations. Meanwhile, service providers in the U.K. and Spain focus on bare metal for media delivery, gaming, and edge services. This combination of compliance-centric demand and advanced industrial use cases is steadily expanding the European share of global bare metal deployments.

Asia Pacific Bare Metal Cloud Market Trends

The Asia Pacific Bare Metal Cloud Market is one of the fastest-growing, supported by strong digitalization, manufacturing advantages, and a rapidly expanding base of cloud-native enterprises. China, Japan, and India are at the forefront, with hyperscalers and regional providers investing heavily in new data centers and bare metal offerings to support e-commerce, fintech, gaming, and industrial applications. In China, large internet and fintech platforms deploy bare metal clusters for high-concurrency transaction systems and large-scale AI models. Japan leverages bare metal for low-latency financial trading, advanced manufacturing, and media delivery, while India is seeing increased adoption among IT services, digital payments, and SaaS providers.

Across ASEAN, governments and enterprises are modernizing infrastructure to support smart city projects, 5G rollouts, and Industry 4.0 initiatives in electronics, automotive, and consumer goods manufacturing. Bare metal cloud in regional hubs helps customers achieve low-latency access, comply with data-residency rules, and avoid cross-border data transfer bottlenecks. Cost-competitive data center construction and a skilled IT workforce in several Asia Pacific countries further enhance the region’s attractiveness as a production and service location for global bare metal cloud providers.

Competitive Landscape

Market Structure Analysis

The Bare Metal Cloud Market is moderately consolidated, with a mix of global hyperscalers, telecom-backed providers, and specialized bare metal hosting companies. Leading players such as IBM, Oracle, Amazon Web Services, Inc., Equinix, Inc., OVH SAS, and Lumen Technologies leverage extensive data center networks and deep enterprise relationships to deliver integrated bare metal, networking, and managed services.

Competition centers around performance differentiation, geographic coverage, ecosystem integration, and value-added services including Business Consulting, managed security, and lifecycle Support and Maintenance. Emerging business models focus on flexible consumption, edge-proximate deployments, and GPU-rich configurations for AI and graphics workloads. Partnerships with silicon vendors, software providers, and interconnection platforms are expanding, reinforcing a landscape where technology alliances and platform ecosystems are as critical as raw infrastructure scale.

Key Market Developments

- In March, 2025: IBM introduced enhanced bare metal servers featuring next-generation CPUs optimized for AI and analytics workloads, expanding performance options for enterprise customers.

- In April, 2025: Oracle expanded Oracle Cloud Infrastructure bare metal GPU instances to support larger AI models and high-performance computing, strengthening its competitive position in performance-intensive cloud services.

- In May, 2025: OVH SAS launched new high-grade bare metal servers with advanced cooling and energy-efficiency features, targeting intensive workloads such as AI, big data, and 3D rendering in Europe and North America.

Frequently Asked Questions

The global Bare Metal Cloud Market is projected to reach around US$ 58.9 Billion by 2033, growing from approximately US$ 14.8 Billion in 2026 at a robust CAGR of about 21.8% during 2026–2033.

Key demand drivers include rising adoption of AI/ML, high-performance computing, and latency-sensitive applications, as well as stringent regulatory and security requirements in sectors like BFSI, healthcare, and government, which favor dedicated, single-tenant cloud infrastructure.

The BFSI segment is the leading end-user, leveraging bare metal cloud for secure, low-latency transaction processing, real-time risk analytics, fraud detection, and regulatory compliance, making it the largest contributor to overall market revenues.

North America leads the global market, supported by mature cloud infrastructure, high enterprise IT spending, strong presence of leading providers such as IBM, Oracle, Amazon Web Services, Inc., and Equinix, Inc., and early adoption of performance-centric cloud architectures.

A major opportunity lies in delivering GPU-optimized and edge-proximate bare metal platforms tailored to AI, analytics, and IoT use cases, combined with robust API Integration and Deployment, managed security, and industry-specific solution stacks.

Key players include IBM, Oracle, Amazon Web Services, Inc., CenturyLink, Internap Corporation, RACKSPACE US, INC., Limestone Networks, Inc., BIGSTEP, Equinix, Inc., Hivelocity, Inc., Hetzner Online GmbH, HorizonIQ, Linode, LLC, Lumen Technologies, OVH SAS, along with regional providers such as Alibaba Cloud, Tencent Cloud, Huawei Technologies Co., Ltd., Fujitsu Limited, Leaseweb, and phoenixNAP.