- Medical Devices

- Arthroscopic Devices Market

Arthroscopic Devices Market Size, Share, and Growth Forecast 2026 - 2033

Arthroscopic Devices Market by Product (Arthroscopic Implants, Arthroscopies, Shoulder Implants, Arthroscopic Radio Frequency Devices, Arthroscopic Radio Frequency Systems, Other), by End User, by Regional Analysis, 2026-2033

Arthroscopic Devices Market Size and Trend Analysis

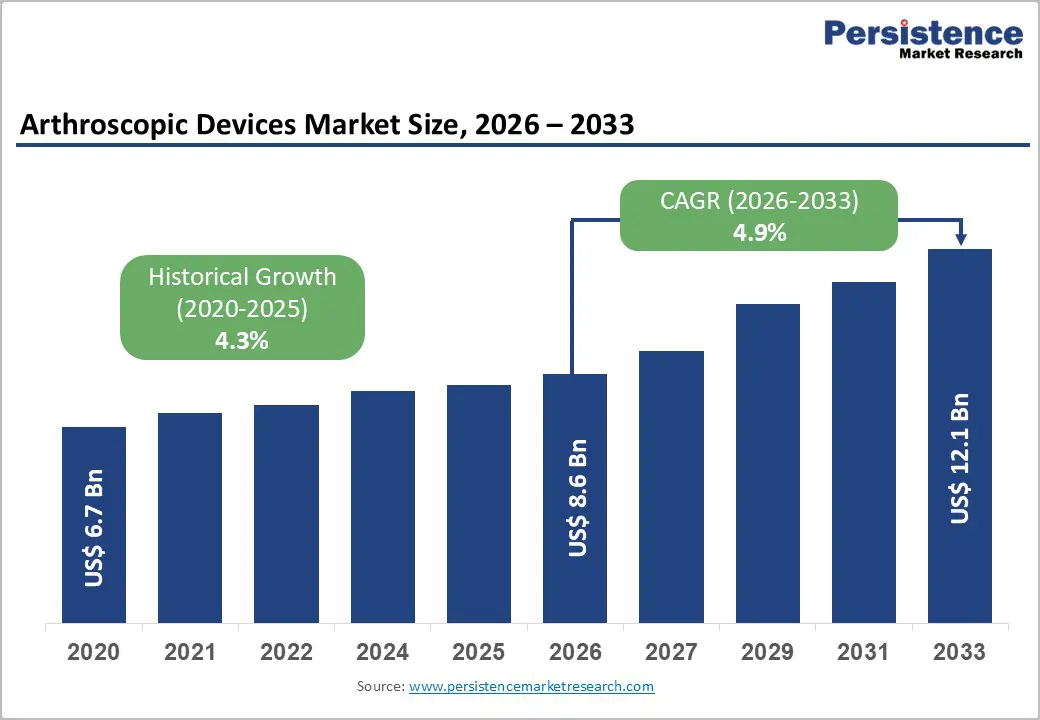

The global arthroscopic devices market size is expected to be valued at US$ 8.6 billion in 2026 and projected to reach US$ 12.1 billion by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

The arthroscopy devices market is progressing steadily, supported by rising orthopedic case volumes, increasing preference for minimally invasive surgeries, and continuous technological improvements in joint visualization and repair systems. Growing incidences of sports injuries, osteoarthritis, and traumatic joint disorders are boosting procedural demand worldwide. Surgeons favor arthroscopy for its reduced postoperative pain, shorter hospital stays, and quicker recovery, driving higher utilization across orthopedic and sports-medicine departments. Advancements in high-definition arthroscopes, imaging platforms, and precision-guided instruments further enhance surgical accuracy and broaden clinical applications across multiple joints.

Looking ahead, market expansion will be influenced by higher knee-procedure volumes, growing use of bioabsorbable implants, and hospital investments in digitally integrated operating rooms. Improved healthcare access in emerging economies is also expected to support sustained long-term growth.

Key Market Highlights

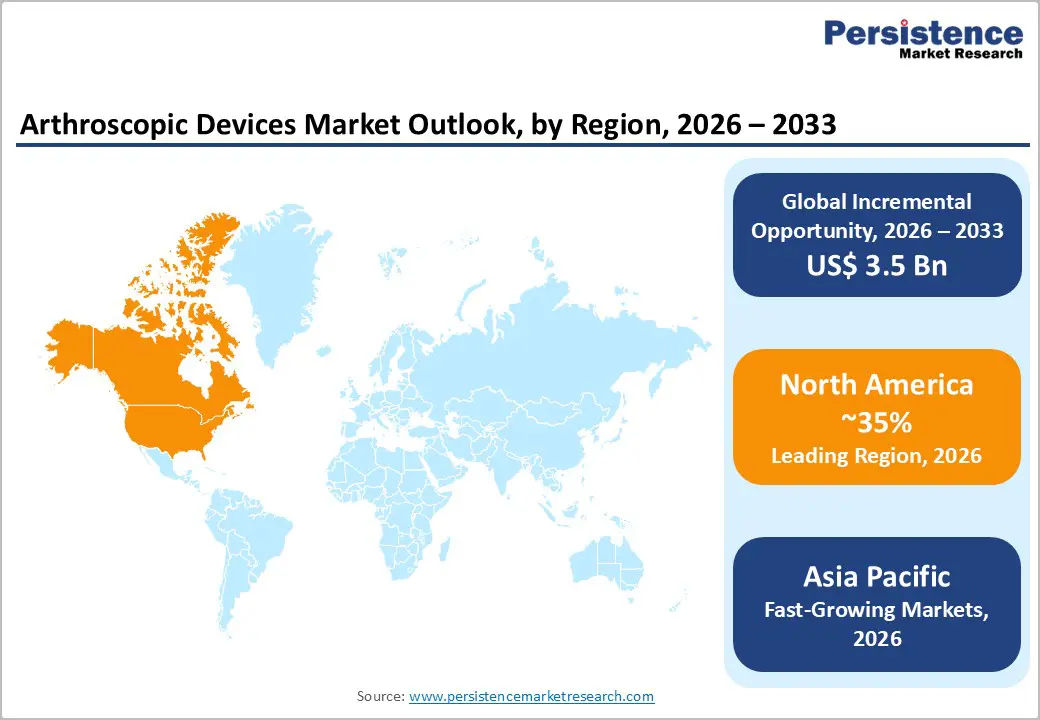

- North America dominates the arthroscopic devices market, supported by advanced surgical infrastructure, high orthopedic procedure volumes, strong reimbursement coverage, and rapid adoption of new technologies.

- Asia Pacific is the fastest-growing region, driven by expanding healthcare access, rising sports injuries and osteoarthritis prevalence, government hospital investments, and local manufacturing initiatives.

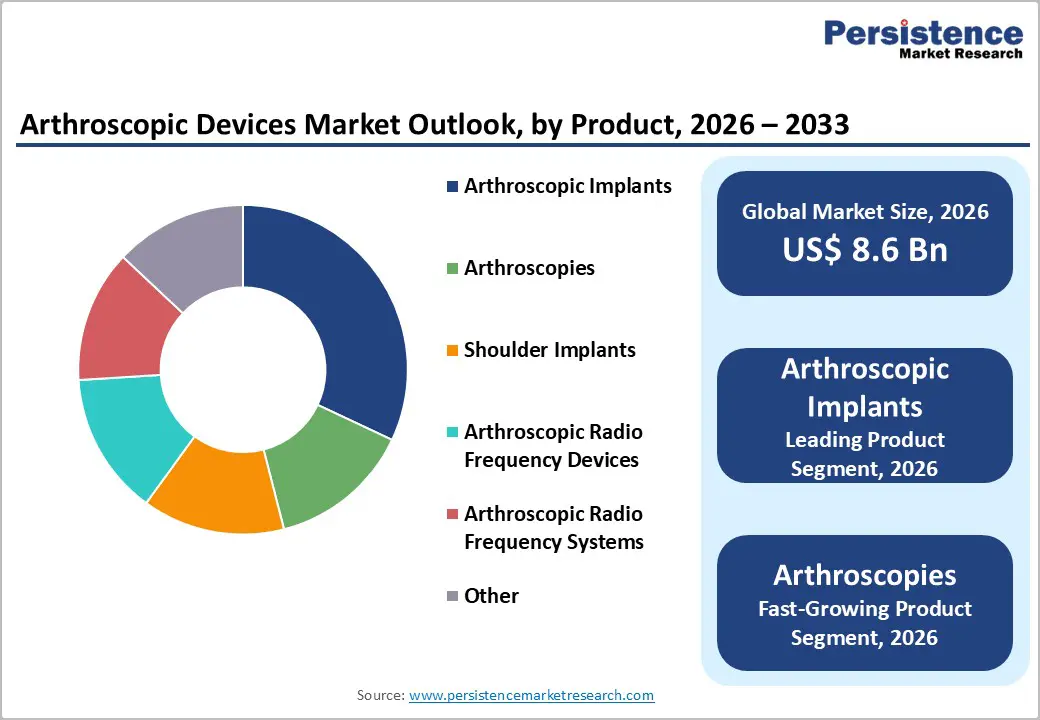

- Arthroscopic implants hold the largest product share due to frequent use in ligament reconstruction, rotator cuff repair, meniscal fixation, and rising adoption of bioabsorbable materials.

- Ambulatory surgical centers and outpatient orthopedic clinics are the fastest-growing end users, supported by payer shifts toward same-day surgeries, lower procedure costs, faster recovery expectations, and compact arthroscopy system adoption.

| Global Market Attributes | Key Insights |

|---|---|

| Arthroscopic Devices Market Size (2026E) | US$ 8.6 billion |

| Market Value Forecast (2033F) | US$ 12.1 billion |

| Projected Growth CAGR (2026-2033) | 4.9% |

| Historical Market Growth (2020-2025) | 4.3% |

Market Dynamics

Driver: Increasing Geriatric Population and High Frequency of Joint Replacement Surgery

The arthroscopy devices market is expanding due to the rising demand for joint replacement surgeries. Furthermore, the growing geriatric population is a significant factor driving growth of the global arthroscopy devices market, leading to an increase in knee and joint problems among the older population. According to the World Health Organization, there were 1 billion people aged 60 and more in 2019, and that number is anticipated to rise to 1.4 billion by 2030 and 2.1 billion by 2050. As the number of people suffering from musculoskeletal diseases rises, so will the demand for arthroscopy devices in the near future.

Rising frequency of sports injuries

The arthroscopy devices market is dominated by sports and the other physical activities in which injuries are frequent. Arthroscopy is turning out to be favored over traditional operations due to benefits such as reduced muscle injury, faster recovery, and faster rehabilitation. Arthroscopic devices for treating sports injuries are expected to present significant opportunities to key players in the market. The rising number of cases of sports injuries will fuel the growth of the arthroscopy devices market throughout the forecast period.

Restraint: High Cost and Lack of Skilled Professionals

Arthroscopic devices are very expensive and out of reach for people with average and poor incomes. Another factor impeding the growth of the arthroscopic devices market is the high costs associated with arthroscopic devices, which include infrastructure and training expenditures. In addition, a scarcity of skilled professionals will be a big problem for the growth of the global arthroscopic devices market.

Stringent Rules and Manufacturing Issues

One of the primary factors impeding the growth of the arthroscopic devices market is the strict FDA rules and regulations. The increasing frequency of recalls by the US FDA due to product failures, component inconsistencies, or compromised sterility concerns is impeding the market growth. Apart from that, serious flaws in manufacturing processes uncontrolled and inadequate storage conditions, increase the risk of contamination and may result in patient infection. As a result, manufacturing issues or product failures are projected to hamper the growth of the arthroscopic devices market.

Opportunity: Increased Preference for Minimally Invasive Treatment Procedures

The growing preference for minimally invasive (MI) treatment procedures is a major factor accelerating adoption of arthroscopy devices across orthopedic practices worldwide. Patients increasingly favor arthroscopic surgery over open techniques because it involves smaller incisions, less muscle damage, reduced postoperative pain, and shorter hospital stays. These clinical advantages translate into faster rehabilitation and earlier return to daily activities, making arthroscopy particularly attractive for sports injuries and degenerative joint conditions. Surgeons also benefit from improved visualization, precise instrumentation, and enhanced procedural control, which contribute to consistent outcomes and broader clinical acceptance across knee, shoulder, hip, and ankle interventions.

Healthcare systems and payers further support the shift toward minimally invasive approaches by encouraging outpatient care and cost-efficient treatment pathways. Hospitals and ambulatory surgical centers are investing in advanced arthroscopy suites to meet rising procedural volumes. As awareness of MI benefits continues to grow and training programs expand, arthroscopic techniques are expected to remain central to orthopedic care, sustaining long-term market growth globally.

Category-wise Insights

Product Analysis

The Arthroscopic Implants segment is projected to contribute a substantial portion of arthroscopy-device revenues in 2025, supported by rising volumes of ligament repairs, rotator-cuff reconstructions, and meniscal procedures. Surgeons increasingly rely on fixation anchors, interference screws, suture-passing systems, and graft-support devices to stabilize joints while minimizing tissue trauma. Manufacturers continue to expand portfolios with both metal and bioabsorbable implants, aiming to shorten operating times, improve pull-out strength, and promote biological healing. Refinements in anchor geometry, knotless technologies, and pre-loaded suture systems have improved workflow efficiency inside operating rooms and reduced complication risks. Clinical studies and real-world feedback consistently report favorable functional outcomes and lower revision rates with newer implant designs, strengthening physician confidence. As minimally invasive orthopedic approaches become standard practice across major joints, sustained investment in implant innovation is expected to keep this category central to arthroscopic procedure growth worldwide.

End user Analysis

Hospitals remain the largest end users of arthroscopic devices, driven by high surgical throughput, access to advanced imaging suites, and multidisciplinary orthopedic teams capable of managing complex reconstructions. Large tertiary centers frequently adopt premium visualization systems, powered instruments, and implant portfolios, supported by capital budgets and reimbursement coverage for minimally invasive procedures. Ambulatory surgical centers (ASCs), however, are emerging as a rapidly expanding end-user segment as payers encourage same-day orthopedic surgeries and patients seek faster recovery pathways. ASCs favor compact, efficient arthroscopy platforms that enable high case turnover while maintaining clinical quality. Specialty orthopedic clinics also contribute steadily, particularly in sports-medicine-focused practices performing knee and shoulder interventions. Across all settings, demand is shaped by surgeon preference, procedure mix, and economic efficiency. Continued migration of routine arthroscopies toward outpatient environments is expected to reshape purchasing patterns and stimulate competition for cost-effective, high-performance device systems.

Regional Insights

North America Arthroscopic Devices Market Trends and Insights

North America continues to lead the global arthroscopy devices market, commanding the largest share of revenues due to a mature healthcare ecosystem, advanced surgical infrastructure, and high procedural volume. The region’s strong adoption of minimally invasive orthopedic procedures particularly knee, shoulder, and elbow arthroscopies is driven by high incidences of sports injuries, osteoarthritis, and degenerative joint disorders. With healthcare facilities equipped with cutting-edge visualization systems and powered instruments, arthroscopy has become a routine intervention across hospitals and ambulatory surgical centers. North America’s leadership is further reinforced by robust reimbursement frameworks that support same-day outpatient surgery, enhancing access and efficiency for patients choosing minimally invasive solutions over traditional open surgeries. Major growth contributors include the U.S., which accounts for a significant portion of regional procedure volumes, and Canada, which benefits from comprehensive public healthcare investment and rising orthopedic care demand. Innovation partnerships between device makers and clinical centers also sustain competitive momentum and technology diffusion.

Asia Pacific Arthroscopic Devices Market Trends and Insights

The Asia Pacific arthroscopic devices market is the fastest-growing regional segment globally, propelled by expanding healthcare infrastructure, rising orthopedic disease burden, and increasing adoption of minimally invasive surgical techniques. Countries like China, India, and Japan are central growth drivers, with significant investments in modern surgical suites and arthroscopy training programs that widen access to advanced joint repair procedures. China holds a leading share within the region, supported by healthcare modernization and rising public demand for orthopedic interventions. India exhibits strong momentum with robust CAGR figures, bolstered by favourable healthcare policies, local manufacturing growth, and increasing surgical volumes. Japan’s technologically sophisticated hospitals enhance demand for high-definition visualization and energy-based arthroscopic instruments. Across Asia Pacific, rising sports participation, a growing aging population prone to joint conditions, and greater outpatient care penetration are accelerating procedural uptake. As healthcare spending increases and surgical capabilities expand in Tier-1 and Tier-2 cities, the region offers significant opportunities for device companies targeting mid- to long-term growth.

Competitive Landscape

Market Structure Analysis

The arthroscopic devices market is highly competitive, featuring several multinational and regional manufacturers competing on technology, pricing, and clinical outcomes. Leading companies are expanding manufacturing facilities to enhance production capacity, ensure supply reliability, and reduce costs. Market participants increasingly focus on launching advanced products, including high-definition visualization systems, innovative implants, and energy-based instruments for orthopedic procedures. Strategic collaborations with hospitals and sports-medicine centers, along with geographic expansion into emerging markets, are also common. Continuous R&D investment and regulatory approvals remain critical to sustaining differentiation, strengthening global footprints, and capturing rising demand for minimally invasive orthopedic surgeries worldwide.

Key Market Developments

- In April 2025, Medtronic plc, a global healthcare technology company, received U.S. Food and Drug Administration approval for its Inceptiv™ closed-loop rechargeable spinal cord stimulator designed to treat chronic pain.

- In April 2025, Zimmer Biomet Holdings, Inc., a leading medical technology firm, announced the successful completion of the world’s first robotic-assisted shoulder replacement surgery using its ROSA® Shoulder System.

Companies Covered in Arthroscopic Devices Market

- Smith & Nephew plc

- Medtronic plc

- Zimmer Biomet Holdings, Inc

- Conmed Corporation

- Johnson & Johnson

- Henke Sass Wolf GmbH

- Stryker Corporation

- Karl Storz GmbH & Co. KG

- Arthrex, Inc

- Richard Wolf GmbH

- Other

Frequently Asked Questions

The global arthroscopic devices market is valued at US$ 8.6 billion in 2026.

Increasing prevalence of joint disorders, sports injuries, aging population, rising demand for minimally invasive procedures, and expanding outpatient surgical centers.

North America leads with 35% share in 2025.

Expand into emerging markets and outpatient settings with innovative, cost-effective, minimally invasive arthroscopic solutions and AI/robotics-enabled technologies.

Leaders include Smith & Nephew plc, Medtronic plc, Zimmer Biomet Holdings, Inc, Conmed Corporation, and Johnson & Johnson.