- Medical Devices

- Handheld Arthroscopic Instruments Market

Handheld Arthroscopic Instruments Market Size, Share, and Growth Forecast, 2026 – 2033

Handheld Arthroscopic Instruments Market by Product Type (Disposable, Reusable), Instrument (Knives, Graspers, Scissors, Others), Application (Knee Surgery, Shoulder Surgery, Hip Surgery, Others), End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics), and Regional Analysis for 2026-2033

Handheld Arthroscopic Instruments Market Share and Trends Analysis

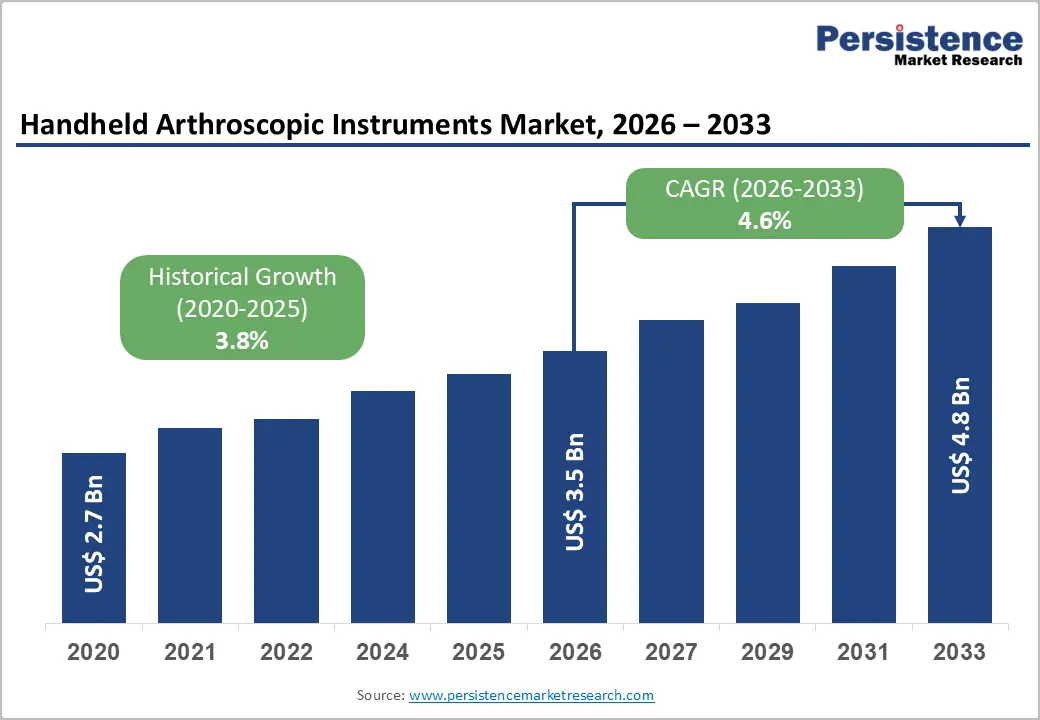

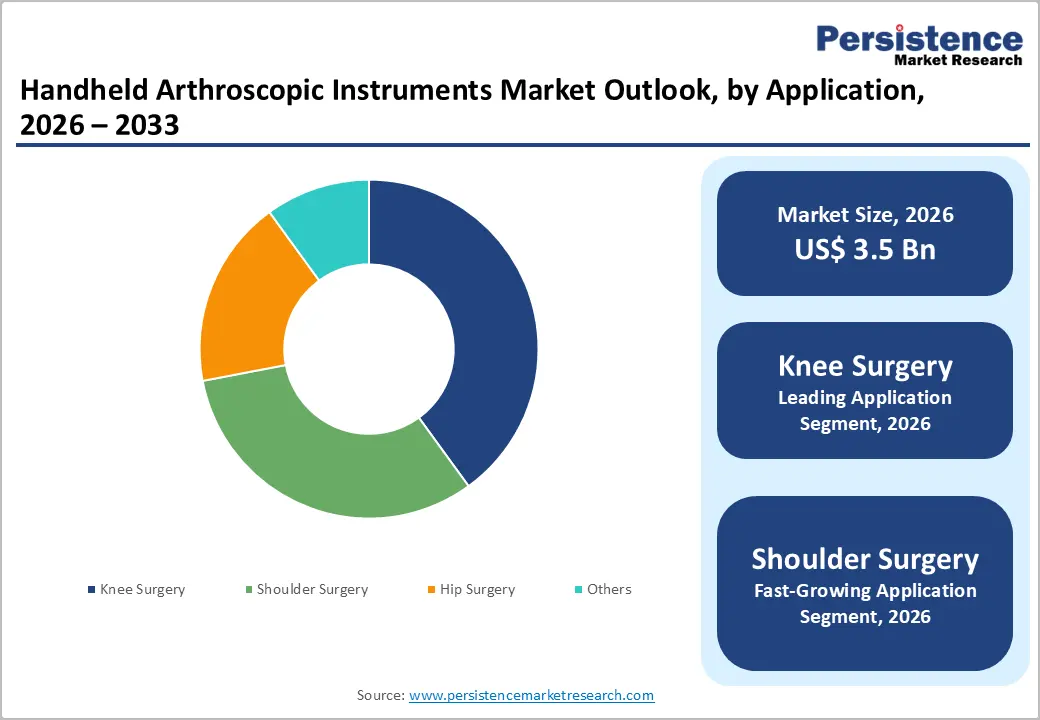

The global handheld arthroscopic instruments market size is likely to be valued at US$ 3.5 billion in 2026, and is projected to reach US$ 4.8 billion by 2033, growing at a CAGR of 4.6% during the forecast period 2026−2033. Rising prevalence of musculoskeletal disorders among aging populations directly expands the demand for minimally invasive procedures.

Enhanced clinical awareness and adoption of arthroscopic interventions drive consistent market utilization across orthopedic departments. Integration of advanced imaging and precision instrumentation increases surgical accuracy, reducing complications and shortening recovery times, which incentivizes providers to adopt handheld solutions.

Healthcare infrastructure expansion in emerging economies ensures accessibility to specialized procedures and supports instrument procurement. Technological innovations in ergonomics and sterilization processes strengthen provider confidence in handheld devices. Insurance coverage improvements and reimbursement policies facilitate affordability and broader patient access.

Key Industry Highlights

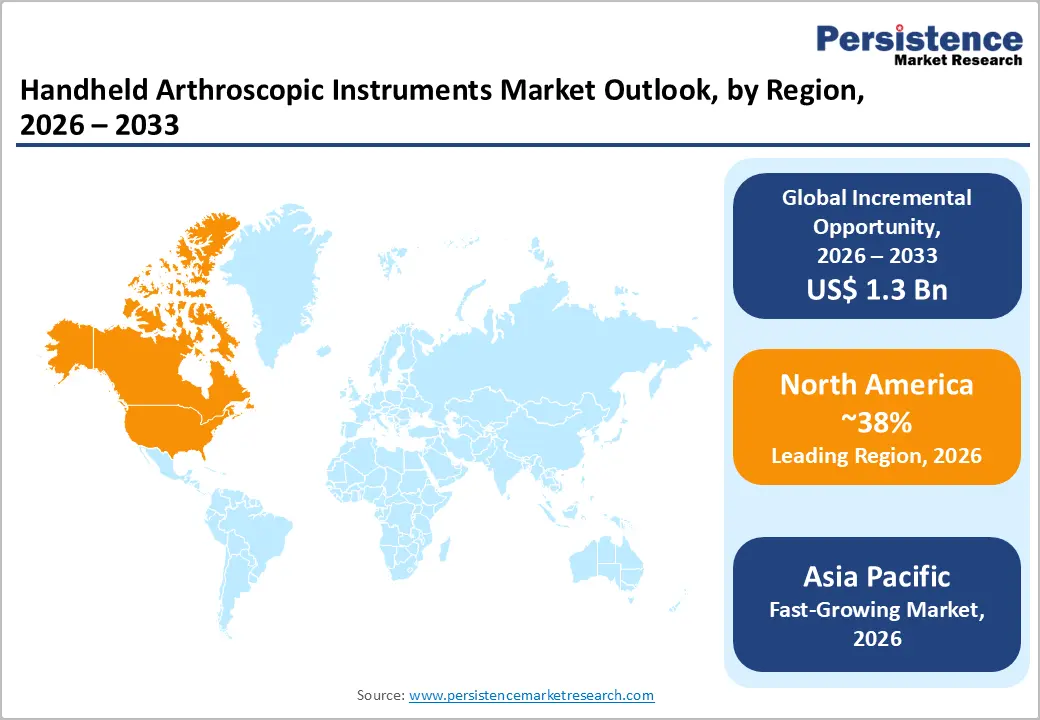

- Dominant Region: North America is expected to hold around 38% market share in 2026 due to high arthroscopy procedure volumes.

- Fastest-growing Regional Market: Asia Pacific is projected to be the fastest-growing market during 2026–2033, driven by expanding orthopedic infrastructure.

- Leading Application: Knee surgery is expected to secure 40% revenue share in 2026, stimulated by high prevalence of degenerative joint conditions and sports-related injuries.

- Fastest-growing Application: Shoulder surgeries are slated to be the fastest-growing segment between 2026 and 2033, fueled by rising rotator cuff injuries.

| Key Insights | Details |

|---|---|

|

Handheld Arthroscopic Instruments Market Size (2026E) |

US$ 3.5 Bn |

|

Market Value Forecast (2033F) |

US$ 4.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Orthopedic Disorders

Escalating incidence of orthopedic conditions across adult and elderly populations increases clinical demand for minimally invasive joint evaluation and repair procedures. Degenerative joint diseases, ligament injuries, cartilage damage, and sports-related trauma frequently require arthroscopic visualization and precision manipulation inside confined joint spaces. Handheld surgical tools enable accurate tissue cutting, grasping, and suturing through small portals, supporting effective treatment of shoulder, knee, hip, and ankle disorders. Expansion of orthopedic patient volumes leads healthcare providers to prioritize surgical technologies that support faster procedural workflows and improved operative precision.

Clinical burden data reinforces the expanding requirement for orthopedic interventions. A 2025 update from the U.K. government musculoskeletal health profile indicates that 17.9% of adults reported a long-term musculoskeletal condition in England during 2024, demonstrating the widespread presence of chronic joint and bone disorders requiring ongoing medical management. Large patient populations affected by osteoarthritis, ligament tears, and chronic joint pain create sustained demand for arthroscopic surgical pathways that reduce hospital stay and support functional recovery. Hospitals and orthopedic centers increasingly integrate minimally invasive joint repair programs in response to disability associated with these disorders.

Technological Advancements in Arthroscopic Tools

Continuous innovation in arthroscopic surgical technology strengthens clinical precision, efficiency, and safety in joint repair procedures. Modern handheld instruments incorporate high-definition visualization, micro-precision cutting tools, and ergonomic designs that support accurate manipulation within confined joint spaces. Advanced imaging integration enables surgeons to identify tissue structures clearly and perform targeted interventions through small incisions. Surgical teams benefit from improved dexterity and control during procedures such as ligament reconstruction and cartilage repair, leading to optimized surgical workflow and reduced procedural complexity. Digital navigation systems and sensor-enabled tools deliver real-time feedback that guides instrument movement and improves intra-operative decision making.

Rising clinical demand for joint treatment reinforces the importance of advanced surgical instruments in orthopedic care delivery. Government health data indicate that around 1.71 billion people globally live with musculoskeletal conditions, many of which require diagnostic or therapeutic interventions involving joint repair procedures. Growing prevalence of osteoarthritis, ligament injuries, and sports-related trauma increases surgical workload across orthopedic departments. Modern handheld arthroscopic tools support efficient management of these cases through minimally invasive approaches that reduce tissue damage and shorten recovery periods. Surgeons gain improved visualization and instrument control, enabling complex procedures to be completed with greater procedural accuracy and shorter operating time.

Limited Skilled Workforce and Training Requirements

Clinical application of arthroscopic tools requires advanced surgical precision, strong spatial awareness, and extensive procedural training. Orthopedic and sports medicine procedures rely on surgeons capable of operating through small incisions while interpreting camera-guided visualization displayed on monitors. Skill development involves long training cycles that include medical education, orthopedic residency, subspecialty fellowships, and repeated exposure to complex joint repair procedures. Training pathways often extend over many years, limiting the number of specialists entering clinical practice within a given period.

Operational complexity further intensifies this restraint. Arthroscopic procedures involve coordinated handling of cameras, probes, graspers, and cutting instruments within confined joint spaces. Surgical teams require specialized simulation laboratories, cadaver-based learning environments, and structured mentorship programs to develop proficiency. Many healthcare institutions lack advanced training infrastructure, restricting hands-on exposure for residents and reducing procedural confidence among early-career surgeons. Workforce distribution across regions remains uneven, leaving rural hospitals and smaller surgical centers with limited access to experienced orthopedic specialists.

High Development and Procurement Costs

Substantial investment requirements across research, engineering, and manufacturing processes create financial pressure within the surgical device ecosystem. Precision handheld instruments demand advanced medical-grade materials, micro-level machining, and strict quality control to meet clinical performance standards. Development phases involve extensive product testing, sterilization validation, and regulatory compliance procedures defined by public health authorities such as the U.S. Food and Drug Administration (FDA). These processes extend development timelines and raise production expenditures for manufacturers. High technical complexity also increases design costs related to ergonomic handling, durability under repeated sterilization cycles, and compatibility with arthroscopic visualization systems.

Healthcare providers face comparable financial considerations during equipment acquisition and operational deployment. Hospitals and ambulatory surgical facilities require comprehensive arthroscopy infrastructure that includes visualization units, specialized surgical tools, sterilization systems, and ongoing maintenance support. Procurement teams evaluate long-term equipment utilization, surgeon training requirements, and reimbursement conditions before approving purchases. Budget limitations within public healthcare systems further restrict investment capacity, particularly in developing regions where infrastructure modernization progresses gradually.

Development of Single-Use Instruments

Rising emphasis on infection prevention in surgical environments strengthens the strategic relevance of disposable surgical instruments. Reusable tools require complex reprocessing procedures that include cleaning, disinfection, packaging, and sterilization before the next procedure. Each stage introduces operational variability and contamination risk when protocols experience deviation or equipment performance declines. Sterile, single-use instruments eliminate reprocessing steps and enter the operating room in sealed packaging prepared for immediate clinical use. Surgical teams gain consistent instrument condition and predictable sterility, supporting strict infection-control protocols enforced in modern healthcare facilities.

Operational efficiency within orthopedic surgical centers further strengthens adoption potential. Reprocessing reusable instruments requires dedicated sterilization units, trained technical staff, and extended turnaround cycles between procedures. High procedural volumes in sports medicine and joint repair create scheduling pressure when instrument sets remain unavailable during sterilization phases. Disposable tools remove this constraint through immediate availability for every procedure, enabling streamlined surgical workflow and improved operating room utilization. Standardized packaging formats also simplify inventory management and traceability within hospital supply chains.

Integration of Smart Technologies

Continuous digital transformation within orthopedic surgery creates strong opportunity for intelligent surgical tools equipped with sensors, data analytics, and imaging integration. Smart-enabled handheld instruments provide real-time feedback on tissue interaction, instrument position, and procedural progress, allowing surgeons to perform complex joint procedures with higher accuracy and improved visualization. Advanced technologies such as artificial intelligence (AI), augmented reality (AR), and high-definition (HD) imaging platforms support precise navigation within small joint spaces, improving diagnostic clarity and procedural efficiency. Intelligent systems analyze surgical images during procedures and assist decision-making through pattern recognition and predictive analytics, reducing variability associated with manual surgical techniques.

Increasing prevalence of joint disorders strengthens the importance of advanced surgical technologies capable of delivering accurate and minimally invasive interventions. Government health statistics indicate that about 21.4% of adults in the United States reported diagnosed arthritis in 2024, reflecting a substantial clinical burden associated with joint degeneration and musculoskeletal conditions. Rising patient volumes for orthopedic procedures create demand for technologies that improve surgical consistency, reduce procedural time, and support faster recovery. Smart instruments equipped with imaging sensors, navigation tools, and digital connectivity enable surgeons to operate with improved spatial awareness and procedural control during joint repair or reconstruction.

Category-wise Analysis

Instrument Category Insights

Graspers are poised to lead with a forecasted 35% of the handheld arthroscopic instruments market revenue share in 2026, powered by critical usage across knee, shoulder, and hip arthroscopic procedures. High clinical trust and consistent performance in tissue manipulation drive surgeon preference. Hospital procurement emphasizes device reliability, sterilization compatibility, and ergonomic handling. Retail and distribution networks support widespread availability, ensuring procedural consistency in high-volume centers. Integration with training programs and clinical guidelines reinforces adoption. Provider confidence in graspers contributes to operational efficiency and patient safety, sustaining dominant market positioning.

Scissors is estimated to be the fastest-growing segment from 2026 to 2033, fueled by innovation in cutting-edge materials, improved blade precision, and enhanced ergonomic design. Surgical procedures increasingly require minimally invasive tissue dissection, promoting the use of advanced scissors instruments. Adoption is supported by digital integration, clinical trials demonstrating reduced complication rates, and hospital preference for high-precision devices.

Expansion of outpatient surgical facilities and specialty orthopedic clinics creates a scalable addressable base for scissors adoption. Regulatory approval for advanced designs accelerates market penetration. Growth reflects the intersection of surgical innovation, operational efficiency, and provider preference.

Application Insights

Knee surgery is likely to be the leading segment with a projected 40% of the handheld arthroscopic instruments market share in 2026, due to high prevalence of degenerative joint conditions and sports-related injuries. Established clinical guidelines recommend arthroscopic intervention as standard care for meniscal tears, ligament reconstruction, and cartilage repair. Hospitals and specialty clinics prioritize precision instruments for consistent outcomes. Digital imaging, real-time monitoring, and procedural standardization support widespread adoption.

Provider referrals and high procedure volumes reinforce market leadership. Cost efficiency and instrument reliability contribute to sustained utilization in high-demand clinical environments.

Shoulder surgeries are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by rising incidence of rotator cuff injuries and degenerative shoulder conditions among active populations. Technological advancements in instrument design, including improved reach, flexibility, and visualization, enhance procedural effectiveness. Expansion of sports medicine clinics and outpatient surgical centers increases accessibility to specialized arthroscopic procedures.

Clinical credibility and digital integration facilitate adoption among orthopedic surgeons. Economic investment in advanced instrumentation supports efficient workflow and patient throughput. Growth is driven by innovation, clinical need, and accessibility of specialized care.

Regional Insights

North America Handheld Arthroscopic Instruments Market Trends

North America is expected to lead with an estimated 38% of the handheld arthroscopic instruments value in 2026, supported by a highly developed orthopedic surgery ecosystem and consistent procedure demand across the United States and Canada. Extensive integration of arthroscopy in knee, shoulder, and hip interventions drives sustained instrument utilization within hospitals and ambulatory surgical centers. High procedure volumes related to ligament reconstruction, rotator cuff repair, and cartilage restoration generate continuous demand for precision handheld surgical tools.

Centers such as Cleveland Clinic and Mayo Clinic in the United States illustrate large-scale orthopedic procedure environments where minimally invasive joint surgery represents a standard clinical approach.

Another critical factor supporting dominance involves strong healthcare expenditure and structured reimbursement coverage for orthopedic procedures. The United States maintains one of the highest healthcare spending levels globally, enabling hospitals to adopt advanced surgical equipment and maintain large inventories of specialized instruments. Private insurance providers, Medicare programs, and employer-sponsored health plans frequently cover arthroscopic interventions for ligament injuries, meniscal tears, and degenerative joint conditions, ensuring stable procedural demand. Canada contributes through publicly funded healthcare systems that support orthopedic surgical services in major hospitals across provinces such as Ontario, British Columbia, and Alberta.

Europe Handheld Arthroscopic Instruments Market Trends

Europe represents a mature environment for advanced orthopedic surgery supported by well-established public healthcare systems and strong clinical specialization. Countries such as Germany, France, the United Kingdom, Italy, and Spain maintain extensive hospital networks equipped with modern arthroscopy systems used for knee, shoulder, and hip procedures. Germany demonstrates strong procedure capacity through a large number of orthopedic clinics and university hospitals that focus on sports injury treatment and joint reconstruction.

France shows consistent demand for minimally invasive orthopedic surgery through structured national healthcare coverage that supports joint repair procedures within public hospitals and private clinics.

Another defining characteristic involves a strong medical device innovation ecosystem supported by research collaboration between universities, hospitals, and technology companies. Switzerland, Sweden, and the Netherlands host advanced biomedical engineering programs that contribute to development of surgical tools, imaging systems, and orthopedic implants used in arthroscopic procedures. Clinical research institutions and teaching hospitals conduct studies that refine minimally invasive surgical techniques and improve instrument design for enhanced surgeon control and visualization.

Italy and Spain demonstrate growth in outpatient orthopedic procedures within ambulatory surgical facilities, reflecting a broader transition toward shorter hospital stays and efficient surgical workflows. Regulatory frameworks under the European Union Medical Device Regulation (MDR) strengthen quality standards and safety validation for surgical instruments entering healthcare systems.

Asia Pacific Handheld Arthroscopic Instruments Market Trends

Asia Pacific is forecasted to be the fastest-growing market for handheld arthroscopic instruments between 2026 and 2033, propelled by rapid expansion of orthopedic surgical infrastructure and increasing adoption of minimally invasive joint procedures across several high-population economies. China demonstrates strong growth momentum through continuous expansion of tertiary hospitals and orthopedic specialty centers in cities such as Beijing, Shanghai, and Guangzhou.

Large patient volumes affected by osteoarthritis and ligament injuries generate sustained demand for arthroscopic procedures. India shows rising adoption of arthroscopy within private healthcare networks such as Apollo Hospitals and Fortis Healthcare, where minimally invasive knee and shoulder procedures are increasingly preferred for faster recovery and reduced hospitalization time.

Japan represents a technologically advanced healthcare environment where orthopedic departments operate with sophisticated imaging systems and high-precision surgical tools. Hospitals in Tokyo and Osaka maintain strong focus on minimally invasive orthopedic surgery supported by advanced clinical training and research programs. South Korea demonstrates steady growth through expansion of specialized orthopedic hospitals and sports medicine clinics in Seoul and Busan.

Strong medical technology manufacturing capabilities and collaboration with international device developers support availability of advanced surgical instruments within operating rooms. Medical tourism expansion in Thailand, Singapore, and Malaysia further strengthens regional procedure volumes, with hospitals such as Bumrungrad International Hospital and Gleneagles Hospital performing large numbers of minimally invasive orthopedic interventions for international patients.

Competitive Landscape

The global handheld arthroscopic instruments market structure exhibits moderate fragmentation, with major multinational medical technology companies maintaining a strong presence through advanced surgical product portfolios and global distribution capabilities. Key participants include Smith+Nephew, Zimmer Biomet, Stryker, Medtronic, CONMED Corporation, and Johnson & Johnson. Combined operations of these organizations account for approximately 45% of total industry revenue, reflecting strong influence through product innovation, surgeon training programs, and well-established hospital relationships. Market leadership stems from extensive orthopedic portfolios that include arthroscopy visualization systems, powered surgical instruments, and specialized handheld tools designed for ligament repair, cartilage treatment, and joint reconstruction.

Competitive positioning increasingly focuses on ergonomic engineering, precision control, and integration with digital surgical platforms. Manufacturers are investing heavily in research and development to improve instrument durability, surgeon handling comfort, and procedural accuracy during minimally invasive joint surgeries. Development of lightweight materials, improved grip mechanisms, and modular instrument designs contributes to improved surgical performance and reduced operating room fatigue for orthopedic specialists. Strategic partnerships with hospitals, research institutions, and orthopedic training centers support clinical validation of new technologies and strengthen adoption among surgeons.

Key Industry Developments

- In March 2026, Stryker introduced new additions to the Triathlon Total Knee System and expanded the Mako SmartRobotics portfolio, including the Triathlon Gold femoral component and advanced robotic and power tool technologies, showcased at the American Academy of Orthopaedic Surgeons (AAOS) annual meeting to enhance precision and surgical workflow in orthopedic procedures.

- In March 2026, Orthoscan announced the launch of the TAU MVP, a next-generation mini C-arm imaging platform combining fluoroscopy and arthroscopy into a single mobile system, unveiled at the American Academy of Orthopaedic Surgeons annual meeting to enhance real-time surgical visualization and procedural precision.

- In September 2025, Arthrex announced the first successful clinical procedure using the NanoNeedle™ Scope 2.0, a next-generation ultra-small arthroscopic imaging device designed to support minimally invasive joint visualization and improve procedural precision in orthopedic surgery.

Companies Covered in Handheld Arthroscopic Instruments Market

- Smith+Nephew.

- Zimmer Biomet.

- Stryker

- Medtronic

- CONMED Corporation.

- Johnson & Johnson

- DJO, LTD

- B. Braun Medical (India) Pvt. Ltd.

- Integra LifeSciences Corporation.

- Richard Wolf GmbH.

Frequently Asked Questions

The global handheld arthroscopic instruments market is projected to reach US$ 3.5 billion in 2026.

Rising prevalence of sports injuries and degenerative joint disorders, along with increasing adoption of minimally invasive orthopedic procedures, is driving the market.

The market is poised to witness a CAGR of 4.6% from 2026 to 2033.

Integration of smart surgical technologies, expansion of ambulatory surgical centers, and rising healthcare infrastructure investment in emerging economies create key market opportunities.

Some of the key market players include Smith+Nephew, Zimmer Biomet, Stryker, Medtronic, CONMED Corporation, and Johnson & Johnson.