- Semiconductor Materials & Components

- Amplifier and Comparator IC Market

Amplifier and Comparator IC Market Size, Share, and Growth Forecast, 2026 – 2033

Amplifier and Comparator IC Market by Product Type (Operational Amplifiers, Comparator ICs, Instrumentation Amplifiers, Others), Technology (Low-Power Amplifiers, High-Speed Amplifiers, High-Accuracy Comparators, Programmable Configurable ICs), Application (Consumer Electronics, Automotive Electronics, Industrial Electronics, Medical Devices, Telecommunication Systems), and Regional Analysis for 2026-2033

Amplifier and Comparator IC Market Share and Trends Analysis

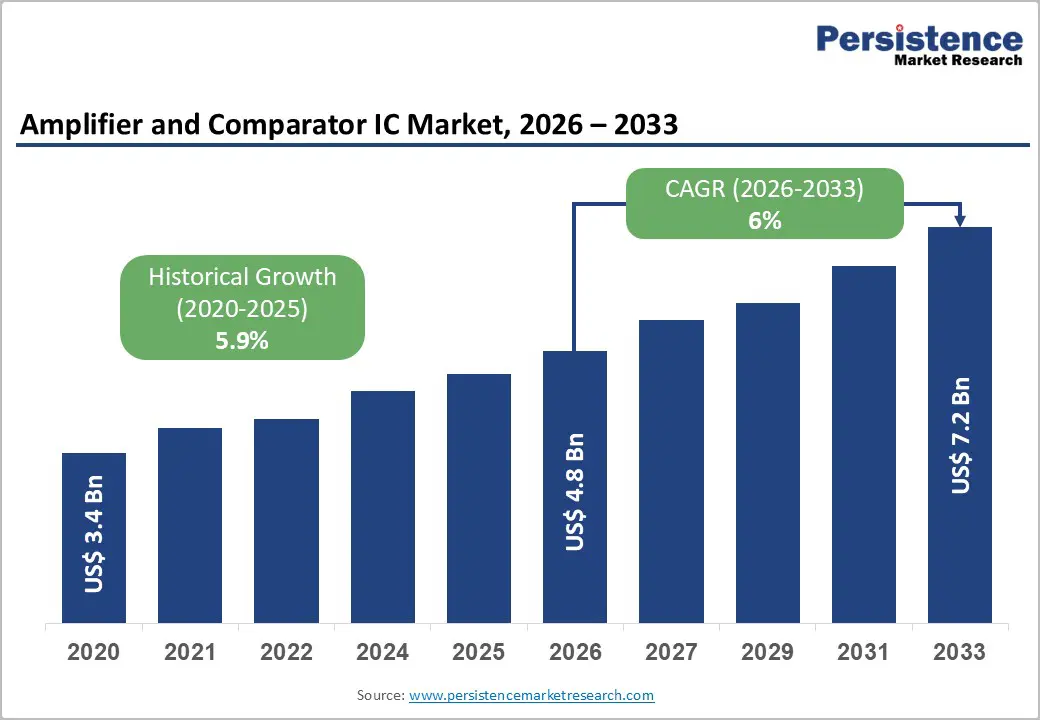

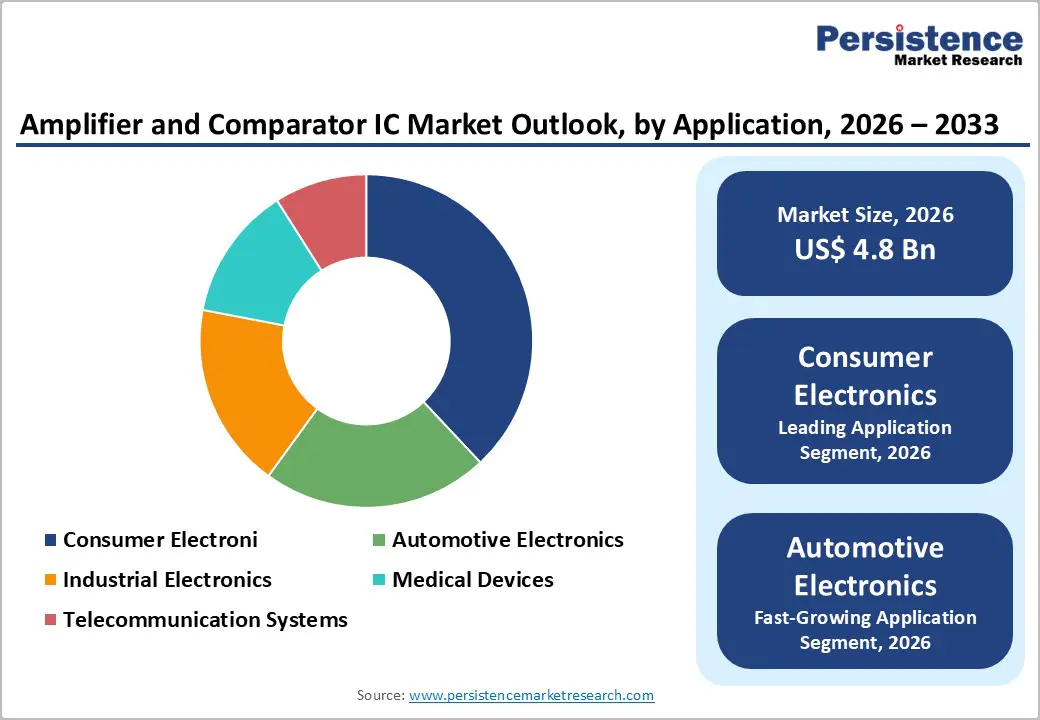

The global amplifier and comparator IC market size is likely to be valued at US$ 4.8 billion in 2026, and is projected to reach US$ 7.2 billion by 2033, growing at a CAGR of 6% during the forecast period 2026−2033.

Rising adoption of consumer and industrial electronics is driving the demand for efficient amplification and comparison solutions, stimulating the cross-sectoral incorporation of integrated circuits (ICs). Technological advancements in low-power and high-speed designs have enabled scalable deployment in automotive and telecommunication systems, enhancing operational efficiency and energy optimization. Expansion of digital infrastructure and connectivity has increased the need for high-accuracy signal processing, promoting IC penetration. Emerging automotive electronics applications, including electric vehicles and driver-assist systems, are increasing IC utilization. Industrial automation adoption fosters demand for reliable instrumentation and programmable ICs in factory and process environments.

Key Industry Highlights

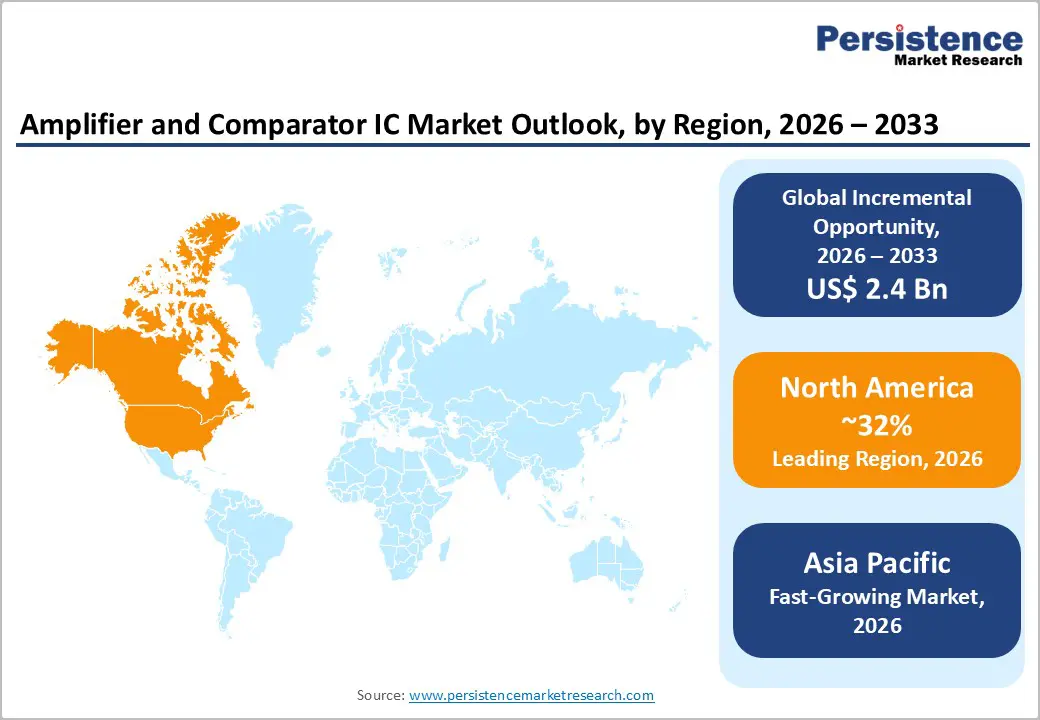

- Dominant Region: North America is projected to lead the market in 2026 with about 32% share, driven by strong analog semiconductor leadership of the U.S. and Canada.

- Fastest-growing Market: The Asia Pacific market is forecasted as the fastest-growing through 2033, owing to semiconductor expansion across China, Taiwan, South Korea, and Japan.

- Leading Application: Consumer electronics are expected to lead in 2026 with about 38% share, on account of strong IC integration and soaring smart device demand.

- Fastest-growing Application: Automotive electronics is projected as the fastest-growing segment during 2026–2033, fueled by skyrocketing electric vehicle (EV) adoption.

| Key Insights | Details |

|---|---|

| Amplifier and Comparator IC Market Size (2026E) | US$ 4.8 Bn |

| Market Value Forecast (2033F) | US$ 7.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of Automotive Electronics

Integration of advanced electronics across modern vehicles elevates demand for precision analog components that regulate signal conditioning, sensing accuracy, and power stability. Government analysis indicates semiconductor content per car is projected to rise from US$ 600 in 2022 to US$ 1,200 by 2030, reflecting rapid penetration of intelligent safety and connectivity systems. Such architecture relies on amplifiers for sensor signal amplification and comparators for voltage-level detection within driver-assistance platforms, battery management units, infotainment modules, and powertrain controls. Electrification trends replace mechanical subsystems with electronic control frameworks, creating higher circuit density and stricter performance thresholds. Vehicles increasingly function as software-defined platforms integrating artificial intelligence, cloud connectivity, and high-resolution interfaces, raising requirements for stable analog front-end processing and precise threshold monitoring across multiple electronic domains.

Regulatory safety mandates, electrified propulsion programs, and connected-mobility initiatives reinforce design complexity within automotive electrical architectures, strengthening procurement volumes for signal-processing integrated circuits. Public policy projections show 40% of global light-vehicle sales expected to be electric by 2030, signaling structural transition toward electronics-centric vehicle platforms. Electric propulsion eliminates numerous mechanical parts yet introduces advanced sensing, thermal monitoring, and voltage supervision requirements, each dependent on analog conditioning and comparison circuitry. High-level driver assistance features, digital cockpits, and remote diagnostics platforms require continuous voltage validation and real-time signal amplification to maintain system integrity and operational reliability.

Advancements in Consumer Electronics

Rapid product innovation cycles across smartphones, AI-enabled laptops, wearables, and smart home devices intensify demand for precision analog signal processing components that regulate voltage, filter noise, and convert signals for real-time responsiveness. High-performance audio, imaging, sensing, and wireless communication functions require stable amplification and accurate voltage comparison to maintain fidelity and power efficiency within compact architectures. Rising device complexity increases component density per unit, raising integration needs for low-power analog chips that ensure reliable performance across temperature variation, battery constraints, and miniaturized circuit layouts. According to Government of India data cited by the Union Electronics and IT Minister, electronics exports surpassed INR 4 lakh crore in 2025, indicating strong production expansion that correlates with rising component consumption across manufacturing supply chains.

Premiumization trends reinforce this demand pattern through feature-rich designs such as high-resolution displays, advanced camera modules, immersive audio systems, biometric authentication, and AI processing blocks. Each function depends on precise signal conditioning and threshold detection to maintain operational stability, driving higher unit usage of analog interface chips per device. Manufacturing incentives, semiconductor ecosystem initiatives, and domestic production programs strengthen supply resilience while encouraging localized sourcing of electronic subsystems, further elevating component requirements. Integration of sensors, power-management circuits, and mixed-signal architectures within compact boards expands reliance on specialized analog control elements that sustain accuracy, efficiency, and electromagnetic compatibility across multi-functional electronic platforms.

Pricing Pressures Fueled by Intense Market Competition

Rivalry across analog semiconductor suppliers creates sustained pricing pressure, limiting revenue expansion potential for amplifier and comparator IC vendors. Large electronics manufacturers employ multi-vendor sourcing policies, which strengthen buyer negotiation leverage and compress average selling prices. Standardized design architectures and widely accessible fabrication partnerships reduce technical differentiation, leading suppliers to compete primarily on cost efficiency, delivery reliability, and support services. Public policy initiatives encouraging domestic semiconductor production increase participant density in several regions. Guidance published by the U.S. Department of Commerce indicates that national incentive programs continue to stimulate new fabrication ventures and supplier entry, reinforcing competitive intensity across component categories.

Technology overlap between analog, mixed-signal, and system-on-chip solutions further intensifies rivalry. Device manufacturers integrate multiple signal-conditioning functions into single packages, reducing standalone component demand and shifting competition toward bundled solutions. Capital-intensive validation requirements and qualification standards encourage firms to pursue large-volume contracts, prompting aggressive bidding behavior that reshapes pricing benchmarks across supply tiers. Frequent product refresh cycles raise research expenditure obligations, placing smaller firms under financial strain while larger firms leverage scale advantages. Globalized distribution networks enable regional producers to access international customers, expanding supplier pools within procurement platforms and increasing substitution risk among functionally comparable devices.

Supply Chain Volatility

Volatility across semiconductor logistics networks creates structural constraints for analog component segments such as amplifier and comparator integrated circuits, where production continuity depends on synchronized wafer fabrication, packaging, and testing flows. Fragmented sourcing models amplify exposure to geopolitical policy shifts, export controls, and transportation interruptions, which alter lead-time predictability and contract pricing stability. A U.S. government supply chain assessment indicates firms report limited visibility into upstream chip origin and sourcing pathways, a condition that complicates procurement planning and raises operational risk exposure. Strategic planners therefore face difficulty aligning inventory buffers with real demand signals, resulting in procurement inefficiencies, delayed product launches, and cost volatility across downstream electronics manufacturing ecosystems.

Risk intensity increases when critical fabrication stages rely on geographically concentrated foundry clusters. Government cybersecurity research highlights semiconductor supply chains as vulnerable to coordination threats and structural security weaknesses across lifecycle stages, reinforcing concerns regarding reliability of component availability. Manufacturing firms responding to such uncertainty often shift toward conservative sourcing contracts, dual-vendor qualification programs, and higher safety stock targets, actions that raise operational expenditure and compress margin profiles. Capital allocation decisions within device producers therefore prioritize supply assurance investments over design innovation budgets, influencing competitive positioning, technology refresh cycles, and long-term product roadmap execution.

Growth in Industrial Automation and Smart Manufacturing

Industrial transformation initiatives across manufacturing economies generate structural demand for precision analog components used in sensing, signal conditioning, and decision circuitry. Automated production environments rely on real-time voltage comparison, current monitoring, and noise-filtered amplification to maintain accuracy in robotics, machine vision, and predictive maintenance architectures. Expansion of smart factory infrastructure increases integration of control loops, programmable logic systems, and Industrial Internet of Things nodes, all of which depend on stable signal interpretation layers. Public-sector industrial acceleration programs reinforce this transition. A 2025 Government of India National Statistics Office release reported manufacturing output growth of 3.4% year-on-year in April 2025, confirming expansion of factory activity that supports adoption of precision electronic control hardware.

Smart manufacturing frameworks emphasize digital feedback, autonomous adjustment, and energy optimization, creating technical environments where signal integrity determines production stability. IoT-enabled factory systems demonstrate measurable operational gains, including 18% lower energy consumption, 22% reduction in machine downtime, and 15% improvement in resource utilization, highlighting dependence on accurate measurement and comparison circuitry that translates physical variables into actionable data. Advanced production lines therefore integrate multiple sensing layers, each requiring amplification and threshold evaluation prior to controller response. Industrial strategies focusing on robotics, artificial intelligence, and adaptive control platforms intensify this requirement since machine learning algorithms rely on high-fidelity analog input for calibration and fault detection.

Proliferation of IoT Devices

Rapid expansion of connected sensors, wearables, industrial nodes, and smart infrastructure is creating strong demand for precision analog signal chains. Each IoT endpoint relies on amplification, filtering, and voltage comparison to translate real-world inputs into digital data for microcontrollers. Amplifier ICs strengthen weak sensor outputs from temperature, pressure, or motion elements, while comparator ICs enable threshold detection for event-driven processing. Rising deployment across smart cities, logistics tracking, healthcare monitoring, and factory automation is increasing unit shipments of compact, low-power components. Design priorities across device manufacturers emphasize energy efficiency, miniaturization, and accuracy, directing procurement toward advanced analog integrated circuits optimized for battery-operated environments. Supply chains are aligning production strategies with high-volume IoT hardware cycles.

Market dynamics indicate that distributed intelligence architectures depend on localized analog decision capability rather than centralized processing. Comparator circuits support instant signal evaluation within edge modules, reducing latency and data transmission load, which strengthens system responsiveness in safety, predictive maintenance, and environmental sensing applications. Amplifiers tailored for ultra-low quiescent current enable extended device lifespan in remote installations where maintenance access remains limited. Semiconductor vendors are investing in specialized product lines, reference designs, and integration platforms aligned with wireless modules and microcontrollers. Competitive differentiation is shifting toward noise performance, thermal stability, and package density, shaping procurement strategies across consumer electronics, automotive electronics, and industrial automation sectors.

Category-wise Analysis

Product Type Insights

Operational amplifiers are poised to lead with a forecasted 35% share in 2026, owing to their widespread applicability across consumer electronics, automotive modules, and industrial instrumentation. Their versatility in signal amplification and filtering enables integration in a diverse range of electronic devices. High adoption in automotive safety and telecommunication systems reinforces sustained utilization. Provider preference for standardization and modular designs supports operational amplifier dominance. Manufacturing processes benefit from mature production techniques, ensuring reliability and scalability. Broad design compatibility with analog and mixed-signal circuits strengthens deployment across multiple platforms. Demand from portable electronics and medical devices sustains shipment volumes. Long product lifecycles improve inventory planning for component distributors and original equipment manufacturers.

Comparator ICs are anticipated to be the fastest-growing segment between 2026 and 2033, fueled by increasing deployment in sensor interfaces, battery management systems, and high-accuracy measurement applications. The rise of electric vehicles and industrial automation elevates demand for precise threshold detection and signal comparison. Technological improvements, including low-power designs and high-speed operation, enhance integration into compact electronic systems. Expanding telecommunication networks and connected devices require real-time monitoring capabilities, further driving comparator IC adoption. Industrial digitization initiatives stimulate procurement across manufacturing environments. Growth in renewable energy systems increases reliance on monitoring circuits.

Application Insights

The consumer electronics segment is slated to hold a dominant position, with an anticipated 38% market share in 2026, driven by widespread integration of operational amplifiers and comparator ICs in smartphones, laptops, and wearable devices. High adoption is influenced by accessibility, scalability, and modular design preferences. The expansion of digital content consumption and connected devices promotes IC utilization. Efficient power management and device miniaturization reinforce consumer electronics reliance on integrated circuit solutions. Technology-enabled service delivery, including remote monitoring and control, supports continuous growth. Rising product refresh cycles sustain component demand across global manufacturing hubs. Increasing penetration of smart home ecosystems strengthens semiconductor procurement. Supply chain optimization and contract manufacturing partnerships enhance volume distribution across regional consumer markets.

The automotive electronics segment is forecasted to be the fastest-growing end-user segment between 2026 and 2033, boosted by electric vehicle adoption, autonomous driving technologies, and infotainment system enhancements. High-accuracy and low-power ICs are crucial for battery management, sensor interfacing, and adaptive control systems. Provider referrals and regulatory requirements for vehicle safety accelerate technology deployment. Integration in connected vehicle ecosystems enhances real-time monitoring and predictive functionality. Expansion of advanced driver assistance systems is strengthening reliance on precision analog components. Electrification platforms require stable signal conditioning across thermal environments.

Regional Insights

North America Amplifier and Comparator IC Market Trends

North America is expected to dominate with an estimated 32% of the amplifier and comparator IC market share in 2026, reflecting strong concentration of analog design leaders, defense electronics procurement, and high value system manufacturing. Industrial demand from aerospace platforms, medical diagnostics equipment, and hyperscale computing infrastructure sustains premium component pricing and stable order visibility. Presence of major fabrication facilities across United States and Canada strengthens localized supply reliability for critical signal chain components used in mission sensitive applications.

Technology leadership derives from deep collaboration between semiconductor architects, cloud hardware firms, and autonomous platform developers seeking precision analog performance. Capital availability through advanced financial markets supports rapid prototyping, niche process experimentation, and specialized wafer agreements. Government backed manufacturing incentives and secure supply mandates encourage domestic sourcing for sensitive infrastructure programs. Design ecosystems aligned with universities and national laboratories accelerate validation cycles and commercialization timelines. High analog content in artificial intelligence servers and advanced communication networks increases revenue contribution per device shipped.

Europe Amplifier and Comparator IC Market Trends

Europe presents a stable growth environment with high adoption of energy-efficient and precision ICs across automotive and industrial sectors. Demand is supported by advanced manufacturing bases in Germany, France, Italy, and Netherlands, where automation systems, electric mobility platforms, and smart grid equipment require accurate signal conditioning components. Industrial equipment producers emphasize reliability, thermal stability, and low power consumption, driving procurement of high-performance amplifiers and comparators. Regulatory frameworks aligned with sustainability and safety standards encourage integration of precision analog circuits within machinery, transportation electronics, and power control units. Strong engineering traditions and structured certification processes support consistent component quality across manufacturing supply networks.

Innovation momentum is reinforced through collaborative semiconductor programs funded by European Union initiatives focused on microelectronics development and technology sovereignty. Research centers and design laboratories coordinate with automotive system integrators and industrial automation firms to refine analog architectures suited for harsh operating environments. Demand is expanding in renewable energy converters, rail signaling controls, and aerospace instrumentation requiring stable voltage comparison and noise suppression performance. Supply infrastructure benefits from geographic proximity between fabrication facilities, packaging providers, and end-equipment manufacturers, enabling rapid validation cycles.

Asia Pacific Amplifier and Comparator IC Market Trends

Asia Pacific is forecasted to be the fastest-growing market for amplifier and comparator ICs between 2026 and 2033, propelled by expanding semiconductor fabrication capacity, dense electronics production networks, and strong regional demand for precision analog components. Large-scale manufacturing investments across China, Taiwan, South Korea, and Japan are strengthening localized supply chains for signal-conditioning integrated circuits. High output of smartphones, electric vehicles, telecommunications hardware, and factory automation systems is increasing consumption of amplifiers and comparators. Competitive production economics and vertically coordinated component ecosystems are improving delivery timelines and strengthening export competitiveness for analog semiconductor manufacturers.

Growth acceleration is supported by expanding electronics assembly corridors and rising system integration activity across India and Southeast Asian economies. Demand for precision analog components is rising within power regulation modules, sensor interfaces, and industrial control architectures. Regional policy initiatives focused on semiconductor self-reliance are encouraging capital deployment into fabrication plants, packaging facilities, and circuit design centers. Close proximity between wafer production, testing infrastructure, and end-device assembly reduces operational lead cycles and supports rapid commercialization.

Competitive Landscape

The global amplifier and comparator IC market demonstrates a moderately consolidated competitive structure in which established semiconductor firms retain strong influence over pricing, technology standards, and supply continuity. Major participants such as MediaTek, ABB, Microchip Technology, BONN Elektronik, and MACOM Technology control substantial revenue shares through diversified product portfolios and strong distribution networks. Market concentration is shaped by long qualification cycles, strict reliability requirements, and high design validation costs that create entry barriers for new participants. Smaller suppliers, therefore concentrate on specialized applications such as high-frequency amplification, aerospace electronics, or custom analog modules, allowing differentiation without direct competition against large-volume manufacturers.

Competitive dynamics emphasize technological refinement, integration capability, and performance optimization rather than price competition alone. Leading suppliers allocate significant capital toward analog architecture research, process node adaptation, and packaging innovation to enhance noise suppression, thermal stability, and signal precision. Strategic collaborations with automotive, telecommunications, and industrial equipment producers strengthen design win rates and long-term procurement agreements. Global supply chain management remains a critical strategic lever, ensuring component availability across multiple production regions and reducing disruption risk.

Key Industry Developments

- In December 2025, Toshiba Electronic Devices & Storage Corporation announced the launch of its TC75W71FU CMOS dual comparator featuring high-speed response, rail-to-rail input/output range, and rapid overcurrent detection capability for industrial equipment, with propagation delays as low as 30–45 ns and low-voltage operation starting at 1.8 V.

- In November 2025, NOVOSENSE introduced its NSCSA240-Q bidirectional current-sense amplifier series designed for automotive and industrial high-voltage PWM systems, featuring up to 80 V input range, ±5 μV offset, and 135 dB CMRR to improve transient immunity and monitoring accuracy.

- In June 2025, Filtronic unveiled its Prometheus V-band high-frequency amplifier system at the International Microwave Symposium (IMS) 2025, featuring gallium nitride (GaN) technology and scalable solid-state power amplifiers delivering up to 500 W output for long-range satellite communications and mission-critical applications.

Companies Covered in Amplifier and Comparator IC Market

- MediaTek Inc.

- ABB Ltd.

- Microchip Technology Inc.

- BONN Elektronik GmbH

- MACOM Technology Solutions Holdings Inc.

- Fuji Electric Co. Ltd.

- Analog Devices Inc.

- Infinite Electronics Inc.

- Broadcom Inc.

- Linearized Amplifier Technologies and Services Pvt. Ltd.

- Electronics and Innovation Ltd.

Frequently Asked Questions

The global amplifier and comparator IC market is projected to reach US$ 4.8 billion in 2026.

Rising demand for precision signal conditioning across automotive electronics, industrial automation, telecommunications infrastructure, and consumer devices is driving the expansion of the market.

The market is poised to witness a CAGR of 6% from 2026 to 2033.

Key opportunities arise from expanding electric vehicle electronics, industrial IoT (IIot) deployment, renewable energy control systems, and increasing integration of precision analog components in miniaturized smart devices.

Some of the key market players include MediaTek Inc., ABB Ltd., Microchip Technology Inc., BONN Elektronik GmbH, and MACOM Technology Solutions Holdings Inc.