- Agrochemicals

- Amino Acid Fertilizer Market

Amino Acid Fertilizer Market Size, Share, and Growth Forecast 2026 - 2033

Amino Acid Fertilizer Market by Source (Natural, Synthetic), Form (Liquid, Solid, Powder), Application (Crop, Horticulture, Gardening, Other), and Regional Analysis for 2026 - 2033

Amino Acid Fertilizer Market Size and Trend Analysis

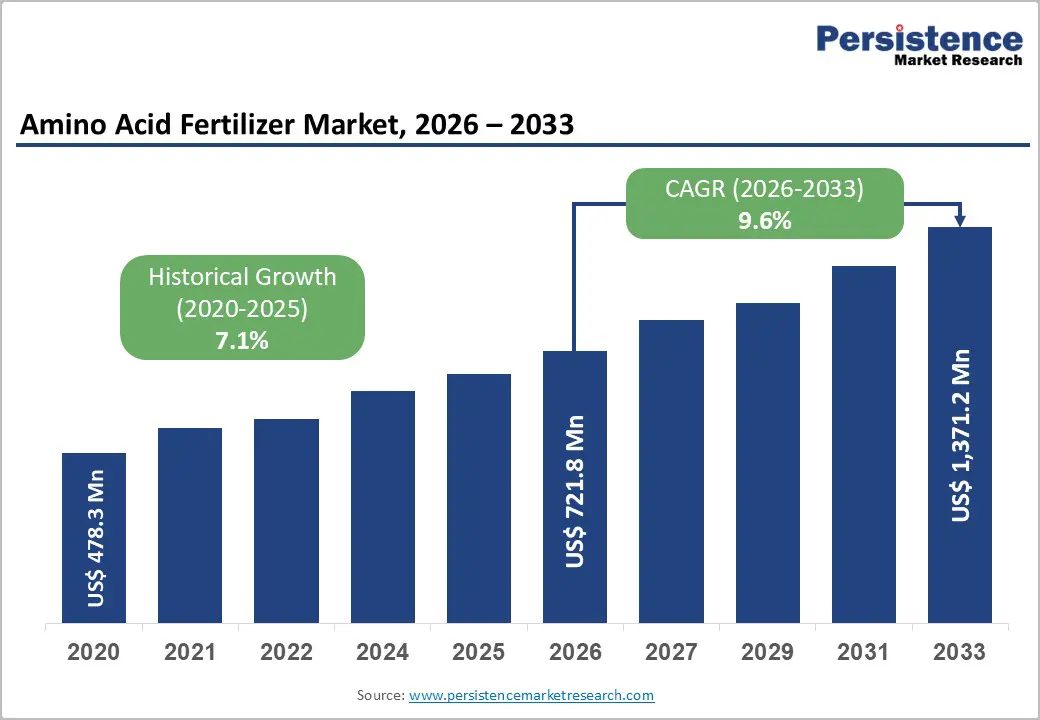

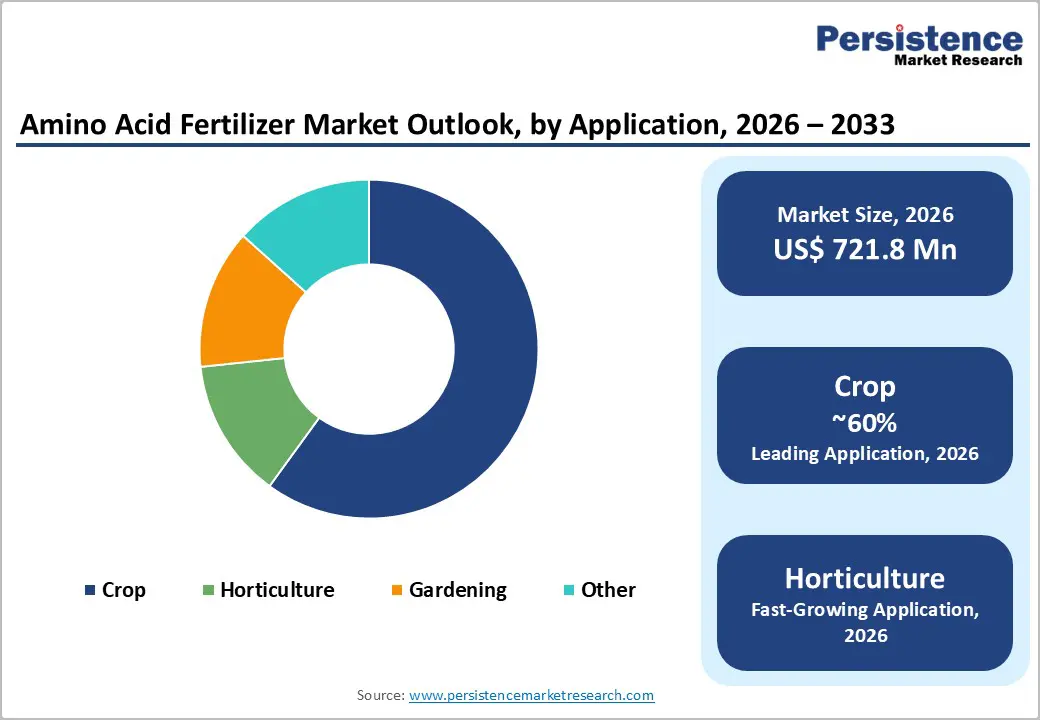

The global amino acid fertilizer market size is estimated at US$ 721.8 million in 2026 and is projected to reach US$ 1,371.2 million by 2033, growing at a CAGR of 9.6% between 2026 and 2033. This robust expansion is primarily driven by accelerating global adoption of organic and sustainable farming practices, escalating demand for high-yield crop solutions amid a rising world population, and increasing regulatory pressure on synthetic fertilizers across key agricultural economies.

According to the Food and Agriculture Organization (FAO), global food production must rise by approximately 70% by 2050 to feed a projected population of nearly 10 billion people, creating sustained demand for nutrient-efficient inputs such as amino acid fertilizers. Complementing this, the USDA reported that the U.S. organic market reached USD 62.5 billion in 2021, underlining expanding market receptivity toward bio-based agricultural products.

Key Industry Highlights:

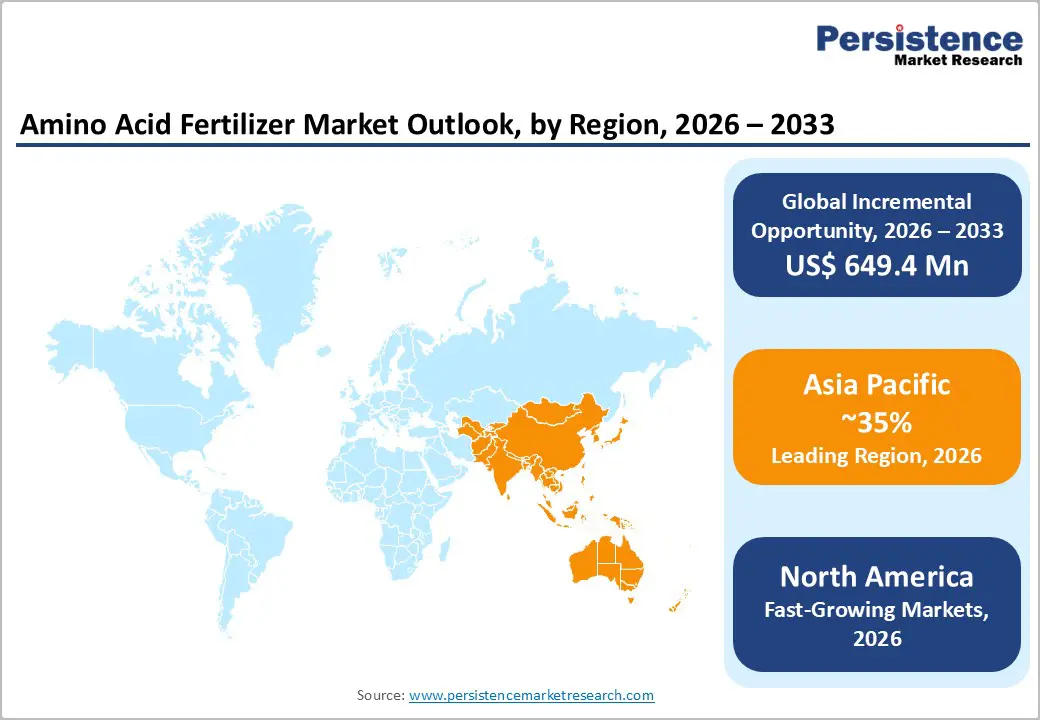

- Leading Region: Asia Pacific dominates the global amino acid fertilizer market with approximately 35% share, driven by China and India's large-scale agricultural bases, government modernization programs, and cost-competitive manufacturing infrastructure.

- Fastest Growing Region: North America is the fastest-growing region, propelled by the United States, which remains the primary contributor, supported by a strong regulatory foundation led by the EPA and USDA, which promote sustainable agricultural inputs through programs such as the Environmental Quality Incentives Program (EQIP).

- Dominant Segment: The Crop application segment leads with approximately 60% market share, supported by the critical role of amino acid fertilizers in improving yield and stress tolerance of staple cereals, wheat, rice, and maize, which underpin global food security.

- Fastest Growing Segment: The Horticulture application sub-segment is the fastest-growing category, driven by rising consumer demand for pesticide-residue-free produce and strict retailer sustainability mandates across EU supermarket chains and premium export markets.

- Key Market Opportunity: Government-backed precision agriculture adoption and the emergence of nano-encapsulated amino acid formulations present a significant opportunity, with 20-30% of global farmers already utilizing precision hardware, enabling targeted, data-driven amino acid application that maximizes crop yield while minimizing environmental impact.

| Key Insights | Details |

|---|---|

|

Amino Acid Fertilizer Market Size (2026E) |

US$ 721.8 Mn |

|

Market Value Forecast (2033F) |

US$ 1,371.2 Mn |

|

Projected Growth CAGR (2026–2033) |

9.6% |

|

Historical Market Growth (2020–2025) |

7.1% |

Market Dynamics

Drivers - Rising Global Adoption of Organic and Sustainable Agriculture

The global transition toward organic farming has emerged as a significant structural catalyst for the amino acid fertilizer market. According to the Research Institute of Organic Agriculture (FiBL) and IFOAM Organics International, organic agriculture is practiced in 188 countries, encompassing more than 96 million hectares managed by over 4.5 million farmers as of 2022. Global sales of organic food and beverages reached nearly EUR 135 billion in the same year, underscoring the sector’s accelerating momentum.

Amino acid fertilizers, produced from plant- and animal-derived hydrolysates, align naturally with organic certification standards, reinforcing their preference among environmentally conscious growers. Their proven ability to enhance nutrient uptake, strengthen root development, and improve plant stress tolerance reduces dependence on synthetic inputs and supports sustainability directives established by the European Commission’s Farm to Fork Strategy and the USDA’s Environmental Quality Incentives Program (EQIP).

Population-Driven Food Security Imperative and Precision Farming Expansion

Rising global food demand is prompting governments and agribusinesses to prioritize advanced nutrient solutions that enhance crop yield efficiency. The FAO projects that global food production must increase by nearly 70% by 2050, underscoring the urgency for high-performance, environmentally responsible fertilizers. Precision agriculture is simultaneously transforming input management practices, with the 2024 McKinsey Global Farmer Survey indicating that 20–30% of farmers worldwide have adopted precision hardware, and an additional 5% plan to adopt it within two years.

Amino acid fertilizers align well with these technologies, supporting data-driven, variable-rate applications that improve nutrient utilization and minimize waste. Moreover, approximately 20% of farmers have already incorporated biostimulants, including amino acid hydrolysates, into their practices, with a further 6% intending to do so, highlighting a rapidly expanding addressable market.

Restraints - High Production Costs Limiting Smallholder Adoption

A major constraint on the amino acid fertilizer market is the substantially higher production cost compared with conventional synthetic fertilizers. Their manufacturing requires advanced enzymatic or chemical hydrolysis processes, high-quality raw materials, and specialized fermentation facilities. Industry assessments indicate that establishing such production units demands initial investments of USD 50–100 million, creating significant entry barriers and limiting supply-side competition.

Consequently, the elevated pricing restricts adoption among smallholder and subsistence farmers, who represent the majority of the agricultural workforce in many developing regions. This cost burden slows market penetration in high- potential areas, particularly across sub-Saharan Africa and South and Southeast Asia.

Regulatory Complexity and Certification Barriers

The fragmented global regulatory environment governing bio-based fertilizers presents a significant challenge for amino acid fertilizer manufacturers. Divergent certification requirements across jurisdictions, particularly those related to organic labeling, necessitate substantial investments in compliance documentation, third-party audits, and product reformulation.

Although the European Union’s Regulation (EU) 2019/1009 harmonizes standards for fertilizing products, it also introduces rigorous testing and registration protocols that extend time-to-market cycles. Navigating differing regulatory frameworks in North America, Asia-Pacific, and Latin America further increases compliance expenditure, limiting operational agility and slowing the cross-border commercialization of new amino acid fertilizer formulations.

Opportunity - Precision Nanotechnology and Smart Formulation Innovation

The integration of nanotechnology with amino acid fertilizer formulation represents a significant opportunity for advanced product differentiation. Nano-encapsulated and micro-encapsulated formulations allow precise, controlled nutrient release aligned with specific plant growth stages, thereby enhancing nutrient-use efficiency and minimizing leaching losses. Research institutions are increasingly developing bio-stimulant-enhanced blends that incorporate amino acids, humic and fulvic acids, and beneficial microbial inoculants, resulting in improved soil microbial activity and greater crop resilience.

Nearly 35% of current innovation efforts are concentrated on enzymatic hydrolysis methods, controlled-release delivery systems, and integration with precision agriculture platforms. Companies that successfully commercialize these next-generation formulations are positioned to command premium prices and establish strong intellectual-property advantages, thereby reinforcing their competitive standing in the global market.

Asia-Pacific Government-Backed Agricultural Modernization Programs

Government-sponsored agricultural modernization programs across the Asia-Pacific region are generating substantial growth opportunities for amino acid fertilizer suppliers. China’s Ministry of Agriculture and Rural Affairs has allocated RMB 156 billion in 2024 to advance agricultural modernization, with a strong emphasis on the adoption of organic inputs and soil management, as well as health improvement initiatives that directly support amino acid fertilizer utilization.

In India, the Pradhan Mantri Krishi Sinchai Yojana promotes efficient fertilizer management and sustainable farming practices. Research by the Indian Council of Agricultural Research (ICAR) demonstrates that amino acid applications improved crop yields by 18-25% across multi-state trials, reinforcing the case for broader adoption. With Asia-Pacific accounting for roughly 35% of the global market and an agricultural workforce of over 1 billion people, the region presents unparalleled expansion potential for companies with robust, localized distribution networks.

Category-wise Insights

By Source

The Natural segment remains the leading source category in the global amino acid fertilizer market, representing approximately 62% of total market share. Naturally derived amino acid fertilizers, produced from both plant-based and animal-based hydrolysates, are widely favored in organic farming due to their full compliance with certification frameworks established by organizations such as IFOAM Organics International and the USDA National Organic Program (NOP). Their high bioavailability, capacity to enhance soil microbial activity, and function as effective chelating agents for essential trace minerals reinforce their agronomic advantage over synthetic alternatives.

As highlighted by FiBL, global organic farmland now exceeds 96 million hectares, sustaining strong structural demand for naturally sourced amino acid inputs. This continued expansion further solidifies the Natural segment’s dominance within the market.

By Form

The liquid form segment dominates the global amino acid fertilizer market, accounting for approximately 45% of the total share due to its practical advantages and broad agronomic applicability. Liquid formulations enable rapid absorption through both foliar and soil application methods, ensure uniform distribution during irrigation or fertigation, and blend easily with complementary plant nutrition inputs. Their strong compatibility with modern drip and sprinkler irrigation systems, widely adopted under precision agriculture initiatives, further reinforces their market leadership.

According to the McKinsey Global Farmer Survey 2024, precision agriculture hardware adoption stands at 20-30% worldwide, with liquid inputs being the preferred format for these systems. Meanwhile, the Powder sub-segment is projected to grow fastest, supported by reduced logistics costs, extended shelf life, and high nutrient concentration, making it especially suitable for price-sensitive emerging markets.

By Application

The crop application segment holds the largest share of the amino acid fertilizer market at approximately 60%, reflecting the central role of staple crops such as wheat, rice, maize, and soybeans in global food systems. Amino acid fertilizers applied to cereals and grains improve chlorophyll synthesis, enhance nitrogen metabolism, and strengthen resistance to abiotic stresses, including drought and salinity, attributes of increasing importance amid growing climate variability.

According to the FAO, cereals account for over 50% of global caloric intake, underscoring the segment’s critical agricultural relevance. The Horticulture sub-segment is the fastest-growing application, driven by rising demand for residue-free fruits and vegetables, stringent sustainability requirements across markets such as the European Union, and higher returns on investment for producers adopting specialized amino acid nutrient programs.

Regional Insights

North America Amino Acid Fertilizer Market Trends

North America represents a mature and innovation-oriented market for amino acid fertilizers, accounting for roughly 23% of global demand. The United States remains the primary contributor, supported by a strong regulatory foundation led by the EPA and USDA, which promotes sustainable agricultural inputs through programs such as the Environmental Quality Incentives Program (EQIP). In 2024, EQIP allocated USD 2.8 billion, with significant funding directed toward the adoption of organic and eco-friendly fertilizers. USDA data indicate that American farmers applied amino acid-based products across 12.8 million acres in 2023, reflecting a 15% year-over-year increase and growing confidence in their effectiveness.

Canada’s expanding organic farmland and rising demand for clean-label food products further reinforce regional growth. Additionally, integration with IoT-enabled precision agriculture, AI-driven crop management, specialty horticulture, and controlled-environment farming is broadening application potential beyond traditional row crops.

Europe Amino Acid Fertilizer Market Trends

Europe accounts for approximately 20% of global amino acid fertilizer demand and operates under one of the most comprehensive bio-fertilizer regulatory frameworks worldwide. The European Union’s Regulation (EU) 2019/1009 standardizes fertilizing product requirements across member states, while the Farm to Fork Strategy aims to reduce fertilizer use by 20% and expand organic farmland by 25% by 2030, strengthening the shift toward amino acid-based alternatives. Germany’s 2020 Fertilizer Ordinance imposes strict nitrogen limits in water-protection zones, encouraging adoption of slow-release organic nutrients.

France, the region’s second-largest market, benefits from strong agroecological policies and leads Europe in organic fruit and wine production. Spain’s horticulture sector, especially in Murcia, drives demand for amino acid foliar applications, supported by studies indicating up to 25% reduced irrigation needs. Post-Brexit, the United Kingdom has maintained alignment with EU organic standards, ensuring regulatory continuity, while industry data shows a 49% reduction in Scope 1 and 2 emissions from 2005 to 2020, with bio-based fertilizers increasingly contributing to this progress.

Asia Pacific Amino Acid Fertilizer Market Trends

Asia Pacific is the largest regional market for amino acid fertilizers, accounting for nearly 35% of global revenue. China remains the principal growth driver, supported by the Ministry of Agriculture and Rural Affairs’ RMB 156 billion (USD 21.8 billion) allocation in 2024 to advance agricultural modernization, with a strong emphasis on soil health and the adoption of organic inputs. China’s extensive amino acid manufacturing base, leveraging fermentation infrastructure originally developed for food and pharmaceutical applications, provides notable cost advantages and fuels export-driven supply expansion across Southeast Asia.

In India, the Indian Council of Agricultural Research (ICAR) reports 18–25% yield improvements from the application of amino acids, while programs such as the Pradhan Mantri Krishi Sinchai Yojana continue to promote adoption. ASEAN countries, including Indonesia, Vietnam, and Thailand, are experiencing rising demand driven by stringent export requirements, growing preference for organic produce, and ongoing FAO-supported soil sustainability initiatives. Japan further strengthens regional innovation through advanced R&D focused on precision formulations for specialty crops and greenhouse cultivation.

Competitive Landscape

The global amino acid fertilizer market is characterized by a moderately fragmented competitive landscape, with leading companies collectively accounting for approximately 55–60% of total market share. These firms pursue assertive strategies focused on product innovation, geographic expansion, and strategic acquisitions to strengthen their competitive positions. Differentiation is primarily driven by advancements in hydrolysis and fermentation technologies, extensive portfolios of organic certifications, and comprehensive agronomic support services. An emerging industry trend involves the development of multifunctional bio-stimulant formulations that integrate amino acids with humic substances and microbial inoculants. Mid-tier and specialized players increasingly target high-value niches such as horticulture and controlled-environment agriculture, while investment in digital agronomy platforms represents a growing competitive frontier.

Key Developments:

- April 2025: BASF Professional & Specialty Solutions (P&SS) has launched its latest nitrification inhibitor, Ampliqan®, to the global fertilizer industry. The innovation protects nitrogen against losses due to nitrate leaching and nitrous oxide emissions and will be available across Asia-Pacific and other regions globally by 2026.

- October 2024: Omex expanded its distribution network to South America, broadening its market reach into key agricultural economies, including Brazil and Argentina, two of the world's most significant crop production markets, as part of its strategy to grow its amino acid foliar fertilizer business in emerging regions.

- December 2023: Yara International ASA announced a strategic partnership to expand sustainable bio-stimulant and amino acid fertilizer solutions across Southeast Asia, targeting integration with precision agriculture platforms for rice and vegetable crops.

Top Companies in Amino Acid Fertilizer

Yara International ASA (Oslo, Norway) is the market's foremost participant by revenue scale and global distribution reach, operating in over 160 countries. The company's integrated crop nutrition portfolio spans conventional and organic fertilizers, with its amino acid and bio-stimulant segment gaining accelerating commercial momentum. Yara's deep investment in digital farming solutions and its strategic partnerships with agri-tech firms position it at the intersection of precision agriculture and sustainable nutrition, enabling data-driven amino acid dosing recommendations for farmers at scale.

Haifa Group (Haifa, Israel) is a global leader in specialty plant nutrition, with a particularly strong presence in the drip-irrigation and foliar fertilizer segments that are ideally suited for liquid amino acid products. The company's robust R&D capabilities, evidenced by its pioneering work in nano-encapsulation and micronutrient chelation technology, enable it to deliver premium amino acid formulations with demonstrably superior crop performance outcomes.

BASF SE (Ludwigshafen, Germany) brings formidable R&D and regulatory expertise to the amino acid fertilizer market through its Agricultural Solutions division. BASF's commitment to innovation, underpinned by annual R&D spending exceeding EUR 2 billion across its chemicals business, enables continuous development of next-generation amino acid formulations tailored to diverse crop and climate conditions.

Companies Covered in Amino Acid Fertilizer Market

- Yara International ASA

- Haifa Group

- BASF SE

- SQM SA

- Evonik Industries AG

- Nutrien Ltd.

- ICL Fertilizers

- Ajinomoto Co., Inc.

- Omex Agrifluids

- NutriAg Ltd.

- Acadian Seaplants Limited

- Biolchim S.p.A.

- EuroChem Group

- Futureco Bioscience S.A.

- Humintech GmbH

Frequently Asked Questions

The global Amino Acid Fertilizer Market is estimated at US$ 721.8 Mn in 2026 and is projected to reach US$ 1,371.2 Mn by 2033, growing at a CAGR of 9.6% over the 2026–2033 forecast period.

The market is primarily driven by the global transition to organic and sustainable farming practices, with organic agriculture now covering over 96 million hectares in 188 countries per FiBL and IFOAM data, combined with the FAO's mandate that food production must increase by 70% by 2050 to meet population demand.

The Crop application segment holds the dominant position with approximately 60% market share, driven by extensive use of amino acid fertilizers in staple cereals and grains, including wheat, rice, and maize, which collectively account for over 50% of global human caloric intake according to the FAO.

Asia-Pacific is the leading region, accounting for approximately 35% of global amino acid fertilizer demand, driven by China's USD 21.8 billion agricultural modernization investment in 2024, India's documented yield improvements of 18–25% from amino acid trials conducted by ICAR, and expanding organic farming policies across ASEAN nations. The region is simultaneously the market's fastest-growing geography.

The most compelling growth opportunity lies in the convergence of precision agriculture and advanced amino acid formulation technology. With 20–30% of farmers globally already using precision agriculture hardware (McKinsey Global Farmer Survey 2024) and nano-encapsulation enabling controlled, targeted nutrient delivery, manufacturers that develop smart, high-performance formulations compatible with digital farming platforms can unlock premium-priced market segments and build durable competitive advantages in both developed and emerging markets.