- Technology

- Actuator Sensor Interface Market

Actuator Sensor Interface Market Size, Share, and Growth Forecast, 2025 - 2032

Actuator Sensor Interface Market by Component (AS-i Master, AS-i Cable, AS-i Node, AS-i Power Supply, Repeater, and Others), by Application (Material Handling, Building Automation, Drive Control, Process Automation, and Others), by Industry, and Regional Analysis for 2025 - 2032

Actuator Sensor Interface Market Share and Trends Analysis

The global actuator sensor interface market size is projected to rise from US$ 2,019.3 Mn in 2025 to US$ 2,965.1 Mn to witness a CAGR of 5.7% by 2032. Actuator sensor interface (ASI) is primarily designed to streamline the communication between control systems and field devices, such as sensors and actuators. Lesser wiring complexity reduces installation time, lowers costs, and minimizes transmission errors. ASI supports high-speed data transfer, enabling manufacturers to achieve greater operational efficiency, faster production cycles, and reduced downtime.

Key Industry Highlights

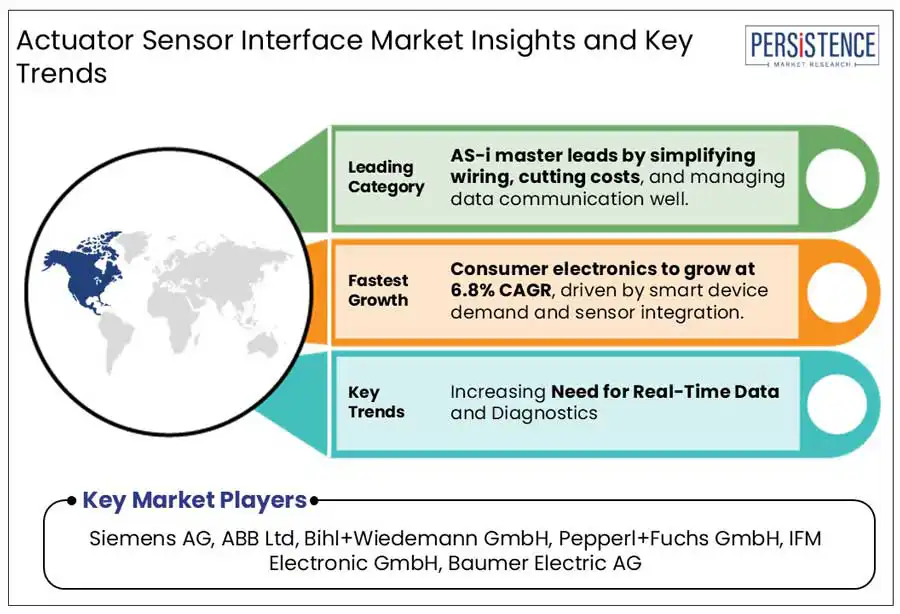

- North America is estimated to account for a 31.7% share in 2025, with strong adoption of industrial automation and smart manufacturing technologies.

- AS-i master is projected to generate a 36.9% share in 2025 due to their ability to simplify wiring, reduce installation costs, and efficiently manage data communication.

- The automotive sector is expected to account for a 29.5% share in 2025 due to the rising adoption of automation, advanced driver-assistance systems (ADAS), and electric vehicles.

- Demand for compact devices is rising, encouraging the development of smaller AS-interface components without compromising performance.

- The push for timely decision-making in process control boosts demand for fast and reliable communication networks.

|

Global Market Attribute |

Key Insights |

|

Actuator Sensor Interface Market Size (2025E) |

US$ 2,019.3 Mn |

|

Market Value Forecast (2032F) |

US$ 2,965.1 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

5.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.1% |

Market Dynamics

Driver - Increased focus on predictive maintenance

Predictive maintenance leverages advanced technologies to proactively identify potential equipment failures, thus improving operational efficiency and minimizing downtime. By using real-time data, predictive maintenance algorithms anticipate failures before they occur, allowing for timely interventions. AS-i, a communication system designed for industrial automation, plays a critical role by facilitating seamless communication between sensors and actuators, providing the essential data required for monitoring equipment conditions. For example, in the automotive sector, ASI systems enable manufacturers to monitor the health of production line equipment in real time, allowing for the prediction of potential failures and the proactive scheduling of maintenance. This approach reduces unexpected downtimes and significantly improves overall production efficiency.

Restraint - Interoperability and data accuracy challenges

The lack of uniformity in communication protocols and data formats creates interoperability challenges, making it difficult for devices from different manufacturers to work together seamlessly. This fragmentation increases both the costs and complexity for system integrators and end-users, complicating the deployment and management of IoT solutions.

The effectiveness of sensors and actuators is heavily reliant on the accuracy and reliability of the data they collect and transmit. In critical applications, such as healthcare, inaccurate or unreliable data can lead to suboptimal system performance and pose significant safety risks. For example, wearable IoT devices monitoring vital signs must provide precise data to ensure accurate diagnostics and timely interventions, as any deviation in data accuracy could compromise patient safety and the efficacy of medical treatments.

Opportunity - Rise of electric vehicles and autonomous vehicles

The global electric vehicle (EV) market is witnessing significant growth, with electric and plug-in hybrid vehicle sales rising by 29% year-on-year in March 2025. This surge is primarily driven by strong momentum in China and Europe, supported by government incentives and stringent emissions regulations. As EV adoption increases, the demand for actuator sensor interface (ASi) systems is growing to manage the complex networks of sensors and actuators required in modern vehicles.

The Indian automotive market is showing early interest in autonomous vehicle (AV) technologies, with plans to launch new EV models in 2025 featuring advanced functionalities such as adaptive cruise control and lane-keeping assistance. These capabilities depend on real-time data processing and control facilitated by ASi systems, which are critical for seamless communication between sensors and actuators. By enabling precise control over essential functions like braking, steering, and battery management, ASi systems enhance safety, performance, and energy efficiency key pillars in the global shift toward electrification and automation.

Actuator Sensor Interface Market Key Trend

Impact of Wireless Actuator Sensor Interfaces on Industrial Automation

Wireless actuator sensor interface (ASI) solutions are driving significant growth in the market, particularly in industrial automation and smart manufacturing. By enabling seamless, cable-free communication between sensors and actuators, it offers enhanced operational flexibility, reduces installation costs, and supports scalable automation architectures. This shift is closely aligned with the principles of Industry 4.0, where the emphasis is on real-time connectivity and data-driven decision-making to improve operational efficiency.

Wireless AS-i solutions are especially advantageous in environments where traditional wiring is impractical or hazardous. For example, in the oil and gas industry, it enables remote monitoring and control in explosive or hard-to-reach areas, enhancing both safety and operational efficiency. As industries continue to embrace Industry 4.0 innovations, wireless AS-i solutions are expected to expand, delivering greater operational agility, cost savings, and scalability across diverse sectors.

Category-wise Analysis

By Component

Based on component, the industry is divided into AS-i master, AS-i cable, AS-i node, AS-i power supply, repeater, and others. Among these, AS-i master is projected to generate a share of 36.9% in 2025. It offers a cost-effective and simplified wiring solution which significantly reduces installation time and maintenance costs. Its ability to support fast and flexible communication makes it particularly suitable for dynamic industrial environments such as manufacturing, automotive, and logistics. The AS-i master also ensures scalability and efficiently manages complex sensor networks, which further drives its adoption across various applications.

AS-i nodes, on the other hand, are estimated to show decent growth in the forecast period due to their ability to provide simple, cost-effective communication between sensors, actuators, and controllers in automation systems. The increasing adoption of industrial automation, smart factories, and the need for seamless data exchange between devices are key factors fueling this growth.

By Industry

Based on industry, the market is segregated into automotive, food & beverages, pharmaceuticals, manufacturing, chemicals, energy & utilities, aerospace & defense, consumer electronics, and others. Out of these, the automotive sector is expected to account for 29.5% share in 2025. This growth is attributed to the increasing integration of advanced driver-assistance systems (ADAS), electric vehicles (EVs), and automation technologies. These applications require precise monitoring and control of critical functions such as braking, steering, and engine management, all of which rely heavily on actuators and sensors. Furthermore, the rising demand for vehicle safety, performance optimization, and emission control is accelerating the adoption of actuator-sensor interfaces in modern vehicles.

The consumer electronics industry is expected to experience significant growth, driven by the rising demand for advanced technologies and smart devices, including wearables, smart home appliances, and automotive systems. To meet the evolving needs of these devices, precise and efficient actuator-sensor interfaces are becoming increasingly essential. These interfaces play a critical role in enhancing user experience and optimizing device functionality.

Regional Insights

North America Actuator Sensor Interface Market Trends

North America is projected to account for approximately 31.7% of the actuator sensor interface market share in 2025, driven by its strong industrial base in sectors such as automotive, aerospace, and manufacturing. The region's adoption of advanced manufacturing technologies, supported by initiatives like those from the U.S. Department of Energy, has played a key role in promoting smart sensors and actuators, boosting market growth.

The rise of the Internet of Things (IoT) and Industry 4.0 technologies has further propelled the demand for actuator sensor interfaces, essential for enhancing connectivity and operational efficiency. North America's leadership in digital transformation, coupled with its access to cutting-edge manufacturing capabilities and research institutions, positions it to remain a dominant player.

Asia Pacific Actuator Sensor Interface Market Trends

In China, the government's initiatives are fostering the adoption of automation and smart technologies, including AS-i systems, to enhance manufacturing productivity. The country's vast manufacturing sector, combined with advancements in industrial automation, positions China as a major player in the market, with an increased demand for actuator-sensor interfaces to support smart cities and industrial automation.

South Korea's strong presence in the semiconductor and automotive industries is also driving adoption. The government's support for smart factory initiatives, alongside the growing automation needs in manufacturing contributes to the market's growth. Meanwhile, in India, initiatives such as Make in India and Digital India accelerate the adoption of industrial automation. As industries seek cost-effective and efficient solutions, the demand for AS-i networks in India is rising further fueling the expansion.

Europe Actuator Sensor Interface Market Trends

In Europe, Germany leads in industrial automation through Industry 4.0 strategy, which emphasizes the integration of cyber-physical systems, IoT, and smart factories. The German Federal Ministry for Economic Affairs and Energy (BMWi) plays a pivotal role in supporting research and development in automation technologies, fostering a favorable environment for the adoption. This strategic focus drives Germany's continued dominance in industrial digitization and automation.

In the UK, the government's focus on automation and robotics aims to enhance productivity, thereby supporting the adoption of cutting-edge technologies. Meanwhile, France is heavily investing in industrial digitization, particularly within sectors like aerospace, automotive, and pharmaceuticals, with actuator sensor interfaces playing a key role. Through its Industrie du Futur program, France is driving the digital transformation of its manufacturing sector, with the Ministry for the Economy and Finance promoting the integration of smart technologies to boost productivity and competitiveness.

Competitive Landscape

The global Actuator Sensor Interface (ASI) market is fragmented, with a mix of small to medium-sized players and larger multinational corporations. Manufacturers are focusing on developing compact, energy-efficient, and IoT-compatible AS-Interface modules, while the seamless integration of AS-i with industrial Ethernet and fieldbus systems is enhancing communication between field-level devices and higher-level systems.

Key Industry Developments

- In November 2024, SPX FLOW introduced the CU4plus ASi-5 control unit, a next-generation solution built on the advanced Actuator Sensor Interface 5 (ASi-5) standard. Designed for APV and Waukesha Cherry-Burrell sanitary valves, it enhances connectivity, speeds up installation, and boosts operational performance. With integrated IoT capabilities, the unit maximizes uptime, efficiency, and system interoperability, setting a new benchmark in valve management.

- In November 2024, Bihl + Wiedemann introduced the ASi-5 motor module (BWU4974) for the Lenze i550 motec frequency inverter, offering a compact and cost-effective solution for installation in cable ducts without the need for an AUX line. Leveraging ASi-5 technology, the module enables fast, cyclical adjustments to ramps and motor speed, while also providing comprehensive motor feedback, including current consumption and error flags.

- In January 2024, ABB launched Ability Field Information Manager (FIM) 3.0, a digital solution that enhances connectivity and interoperability for industrial field instruments, supporting both current and future smart factory devices. Featuring a client/server architecture, FIM 3.0 enables efficient, multi-user device management, and now supports ASi-5 device integration via FIM Bridge PROFINET, streamlining operations and boosting productivity in industrial automation.

Companies Covered in Actuator Sensor Interface Market

- Siemens AG

- ABB Ltd

- Bihl+Wiedemann GmbH

- Pepperl+Fuchs GmbH

- IFM Electronic GmbH

- Baumer Electric AG

- Schneider Electric SE

- Valmet

- symestic GmbH

- Murrelektronik GmbH

- Christian Bürkert GmbH & Co. KG

- EUCHNER GmbH + Co. KG

Frequently Asked Questions

The global market is projected to be valued at US$ 2,019.3 Mn in 2025.

The need for real-time data and monitoring in industrial processes is the key market driver.

The market is poised to witness a CAGR of 5.7% from 2025 to 2032.

The transition toward smart factories that integrate IoT and advanced sensors is the key market opportunity.

Siemens AG, ABB Ltd, and Bihl+Wiedemann GmbH are among the leading key players.