- Automotive Components & Materials

- Automotive Actuators Market

Automotive Actuators Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Actuators Market by System Location (Transmission Actuators, Driveline Actuators, and Brake Actuators), by Component (Electric, Pneumatic, Hydraulic, and Electromagnetic), by Application (Passenger Car, LCV, HCV), and Regional Analysis for 2025 - 2032

Automotive Actuators Market Size and Trends Analysis

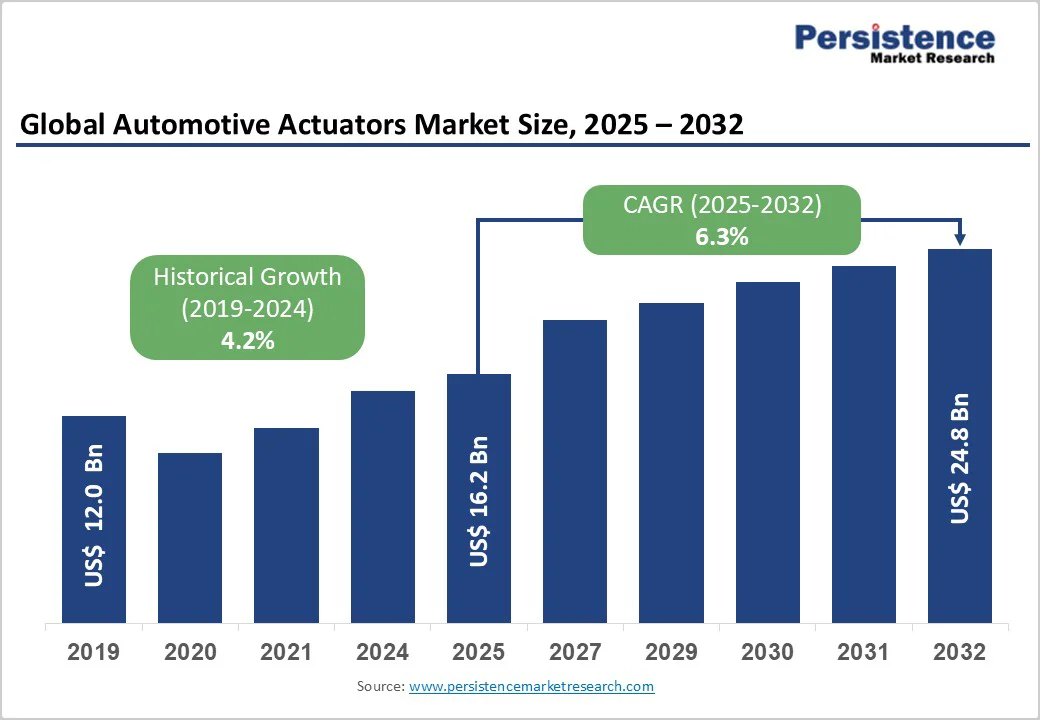

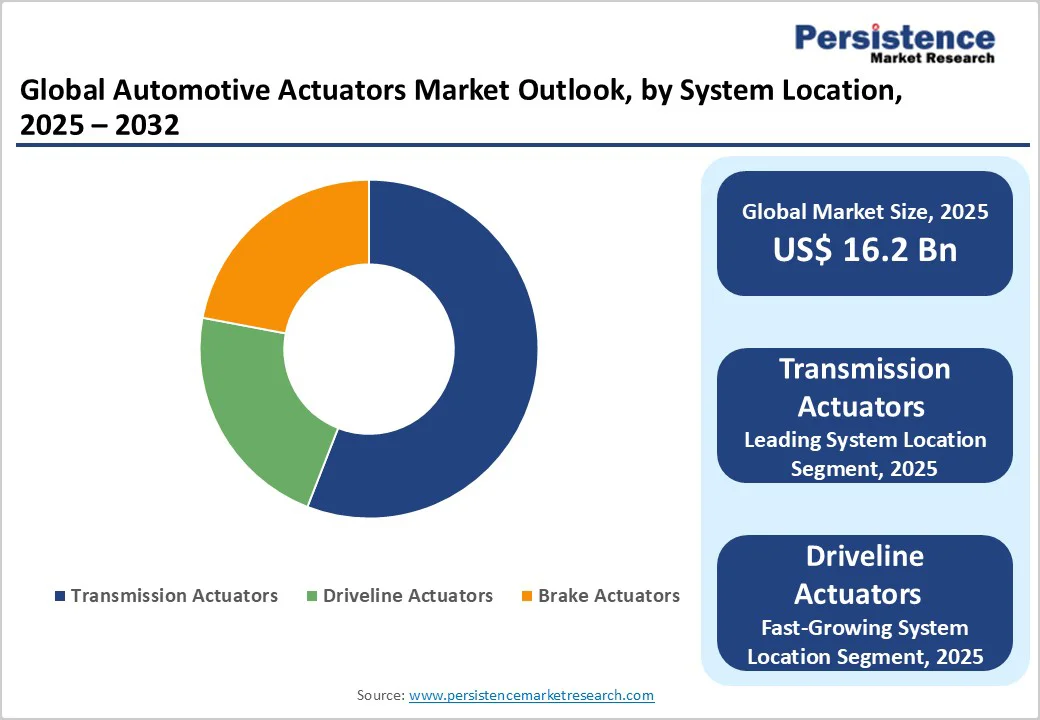

The global automotive actuators market size is valued at US$ 16.2 billion in 2025 and is projected to reach US$ 24.8 billion by 2032, growing at a CAGR of 6.3% between 2025 and 2032.

This market expansion is driven by the accelerating adoption of advanced driver assistance systems (ADAS), increasing penetration of electric vehicles requiring sophisticated actuation technologies, and stringent global automotive safety regulations mandating ISO 26262 compliance for critical electrical and electronic systems.

Key Industry Highlights:

- Transmission actuators dominate system location segments with above 40% revenue share, while driveline actuators represent the fastest-growing category fueled by AWD/4WD system adoption and electric vehicle dual-motor configurations

- Electric actuators lead component segments commanding above 35% market share, with pneumatic actuators experiencing fastest growth in commercial vehicle high-force applications including advanced braking systems

- Passenger cars maintain application segment leadership exceeding 45% revenue share, while light commercial vehicles demonstrate highest growth velocity driven by e-commerce logistics and urban delivery service expansion

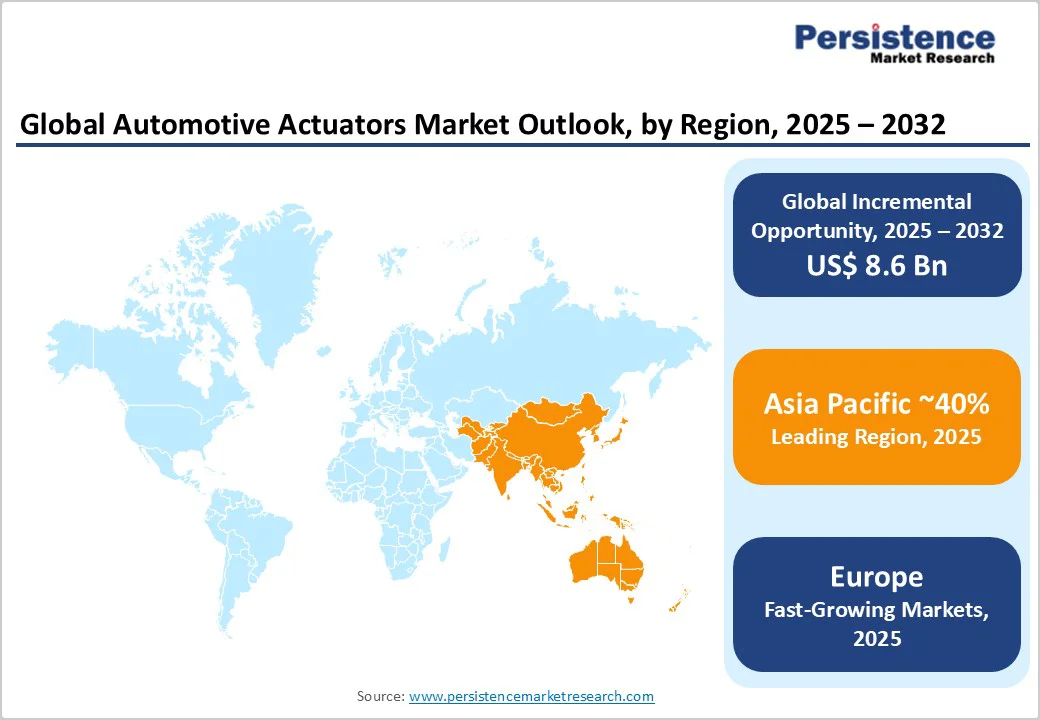

- Asia Pacific region dominates with above 40% global revenue share supported by China's NEV market exceeding 9.5 million annual units, while Europe exhibits strong growth at 6.10% CAGR through 2032 driven by stringent GSR safety mandates

- ADAS penetration reached 8.3% in India's H1 2025 market, representing 33% year-over-year growth, with Level 2 systems expanding 70.8% and electric vehicles achieving 36.4% ADAS integration rates

- Strategic product innovations, including Renesas RL78 microcontrollers for actuator control and Continental's Ac2ated Sound technology, achieving 90% weight reduction, demonstrate industry evolution toward multifunctional, software-enabled actuator solutions

| Key Insights | Details |

|---|---|

| Automotive Actuators Market Size (2025E) | US$ 16.2 Bn |

| Market Value Forecast (2032F) | US$ 24.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.2% |

Market Dynamics

Drivers - Rapid Proliferation of Advanced Driver Assistance Systems (ADAS

The global automotive industry is witnessing unprecedented integration of ADAS technologies, which fundamentally rely on precision actuators for operational effectiveness.

According to JATO Dynamics research, ADAS penetration in India's passenger vehicle market reached 8.3% in H1 2025, representing 33% year-over-year growth from 6.2% in H1 2024. Electric vehicles demonstrate significantly higher ADAS integration rates, with 36.4% penetration compared to conventional vehicles, as EV platforms facilitate seamless hardware-software integration for autonomous features.

Key ADAS functionalities, including adaptive cruise control, lane-keeping assist, autonomous emergency braking, and collision avoidance systems, require sophisticated actuators for throttle response, steering adjustment, and brake modulation.

The Indian government's mandate for Advanced Emergency Braking Systems (AEBS), Lane Departure Warning Systems (LDWS), and Driver Drowsiness and Attention Warning (DDAWS) in commercial vehicles, targeting a 50% reduction in road fatalities by 2030 from current levels of 180,000 annual deaths, exemplifies regulatory drivers accelerating actuator demand.

This regulatory momentum, combined with consumer expectations for enhanced safety features, positions actuators as critical enablers of next-generation vehicle intelligence.

Implementation of Functional Safety Standards and Regulatory Compliance

The automotive industry's adoption of ISO 26262 functional safety standards for electrical and electronic systems has created mandatory requirements for actuator design, testing, and validation throughout the automotive safety lifecycle.

This international standard, titled "Road vehicles - Functional safety," establishes Automotive Safety Integrity Levels (ASIL) ranging from A to D with ASIL D representing the most safety-critical applications requiring the strictest testing protocols.

Actuators deployed in brake-by-wire systems, electronic stability control (ESC), anti-lock braking systems (ABS), and autonomous driving functions must demonstrate compliance with rigorous fault tolerance, reliability, and performance standards.

The standard's "proven in use" clause allows components deployed in millions of vehicles without incident to achieve compliance, while new actuator technologies undergo comprehensive hazard analysis and risk assessment. Manufacturing facilities increasingly incorporate Tool Confidence Level (TCL) qualification processes, ranging from TCL1 to TCL4, to ensure software tools used in actuator development meet safety requirements.

This regulatory framework, combined with consumer safety expectations and liability considerations, compels automotive manufacturers to invest substantially in advanced actuator technologies that satisfy functional safety requirements, thereby driving market growth through quality and performance differentiation.

Restraint - Integration and Calibration Complexity in Multi-System Architectures

Modern vehicles incorporate increasingly complex electrical and electronic architectures, where the integration of diverse actuator systems spanning powertrain, chassis, body control, and safety applications presents formidable technical challenges.

The requirement for precise synchronization between numerous actuators, sensors, and electronic control units demands sophisticated software algorithms and extensive calibration procedures to ensure optimal system performance. Automotive manufacturers must reconcile compatibility across multiple vehicle platforms, regional specifications, and evolving technology standards while maintaining reliability and safety.

The complexity is amplified in electric and autonomous vehicles, where actuators must interface with battery management systems, motor controllers, vehicle-to-everything (V2X) communication networks, and artificial intelligence-based decision algorithms.

Calibration requirements vary significantly across different operating conditions, including temperature ranges from -40°C to +150°C for transmission-mounted actuators, creating substantial engineering overhead. These integration challenges extend development timelines, increase validation costs, and create barriers for smaller manufacturers lacking comprehensive testing infrastructure, thereby constraining market growth velocity.

Opportunity - Emerging Demand for Lightweight, Energy-Efficient Actuator Solutions

The automotive industry's pursuit of improved fuel efficiency and extended electric vehicle range creates substantial opportunities for next-generation actuator technologies emphasizing weight reduction and energy optimization.

Traditional hydraulic and pneumatic actuators are progressively being replaced by electric alternatives offering 90% reduction in weight and volume, as demonstrated by Continental's Ac2ated Sound system introduced in partnership with Sennheiser in January 2020.

Electric actuators provide superior energy efficiency through elimination of hydraulic pumps, reduced parasitic losses, and integration with vehicle energy management systems. The development of brushless DC motor technologies, regenerative energy capture mechanisms, and low-power microcontroller units enables actuators to minimize battery drain, a critical consideration for electric vehicle range anxiety mitigation.

Manufacturers investing in compact actuator designs use advanced materials such as carbon fiber composites, high-strength aluminum alloys, and thermoplastic components can capture market share in the rapidly expanding EV segment, projected to account for 15% annual growth in actuator demand.

This opportunity extends to retrofit markets, where vehicle electrification conversions require space-efficient actuation solutions compatible with existing mechanical architectures.

Category-wise Analysis

System Location Insights

Transmission actuators dominate the global automotive actuators market, securing over 40% of revenue share by 2025 through their essential function in facilitating seamless gear shifts, optimizing engine performance across diverse driving scenarios, and boosting vehicle drivability in manual and automatic systems.

The rise of dual-clutch transmissions (DCT), continuously variable transmissions (CVT), and sophisticated automatic setups has escalated actuator integration, with modern vehicles featuring up to 8-12 units for clutch control, gear selection, valve operations, and torque converter lockup.

Innovations from companies like Getrag, Hyundai, and Honda, including advanced software and electromechanical systems, have slashed shift times to under 100 milliseconds while elevating fuel efficiency via precise gear ratios.

Complementing this, driveline actuators represent the fastest-growing segment, fueled by the surging popularity of all-wheel drive (AWD) and four-wheel drive (4WD) in SUVs and crossovers. These actuators, encompassing torque vectoring, transfer case mechanisms, and differential locks, dynamically distribute power to enhance stability, traction, and off-road prowess.

The shift toward electric vehicles with dual-motor setups further accelerates demand, as independent actuators for front and rear motors integrate with stability and terrain control systems, delivering premium driving experiences that justify higher costs and strengthen brand appeal. Together, these segments underscore the industry's push toward electrification and performance optimization.

Application Insights

Passenger cars dominate the actuator market, capturing over 45% of revenue due to massive global production exceeding 70 million units annually and the integration of advanced comfort, convenience, and safety features.

These vehicles rely on actuators across powertrain management (such as throttle and variable valve timing), chassis control (including electronic power steering and adaptive suspension), body functions (like power windows and latches), and thermal systems (such as HVAC blend doors).

Consumer demand for premium features and regulatory mandates encompassing electronic stability control in over 60 countries, backup cameras in North America, and automatic emergency braking in the EU drive adoption, while software-defined vehicles with over-the-air updates enable programmable actuators for evolving functionalities.

In contrast, light commercial vehicles (LCV) represent the fastest-growing segment, fueled by booming urban logistics, e-commerce, and last-mile delivery services exemplified by fleets from Amazon and JD.com.

LCVs require actuators for automated transmissions, electronic braking in stop-and-go operations, and cargo management, with accelerating electric adoption in zero-emission zones necessitating specialized solutions for electric powertrains, regenerative braking, and battery thermal management.

Shorter replacement cycles (5-7 years versus 10-15 for heavy trucks) accelerate technology integration, bolstered by government incentives for electrification and safety mandates, positioning LCVs as a key growth driver in the actuator landscape.

Regional Insights and Trends

Asia Pacific Region Dominates the Global Automotive Actuators Market, Driven by China and India's Rapid Growth

Asia Pacific dominates the global automotive actuators market, holding over 40% revenue share in 2025 with a valuation exceeding US$6.5 billion, and stands as the fastest-growing segment worldwide. This prominence stems from China's position as the world's largest automotive market, producing over 26 million vehicles annually, bolstered by its comprehensive manufacturing ecosystem, supportive policies, and expanding middle class.

Initiatives like "Made in China 2025" drive investments in intelligent vehicles, connected infrastructure, and New Energy Vehicles (NEVs), with the NEV market surpassing 9.5 million units in 2024, fueling demand for actuators in electric powertrains, battery management, and autonomous systems.

Japan leads in technological innovation through companies like Denso, Hitachi Astemo, and Aisin, focusing on electromagnetic actuators and precision motors. Toyota and Honda's hybrid technologies, such as hybrid synergy drive and i-MMD systems, require specialized actuators for power-split devices and seamless transitions.

India emerges as the region's fastest-growing market, with passenger vehicle production rising over 8% annually and two-wheeler electrification creating opportunities for cost-effective actuators, supported by Production-Linked Incentive schemes.

Southeast Asian nations, including Thailand, Indonesia, Vietnam, and Malaysia, are key manufacturing hubs attracting investments from global automakers. Thailand, producing over 1.8 million vehicles yearly with strong pickup and eco-car segments, demands durable, cost-effective actuators for diesel engines. Expanding logistics and e-commerce sectors boost light commercial vehicles, while EV incentives in Indonesia and Thailand ensure sustained leadership through 2032.

The European Automotive Actuators Market Flourishes Amid Stringent Regulations and Technological Advancements

The European automotive actuators market represents a highly sophisticated and regulation-driven landscape. The European market is projected to grow with a 6.8% CAGR.

This regional market demonstrates the highest regulatory stringency globally, with European Union mandates including Euro 7 emission standards (effective 2025), General Safety Regulation (GSR) requirements for advanced emergency braking, lane-keeping assistance, and intelligent speed assistance in all new vehicles, and ambitious carbon neutrality targets driving automotive electrification.

Germany, the region's largest automotive market, hosts major manufacturers including Volkswagen Group, BMW, Mercedes-Benz, and premium actuator suppliers such as Continental, Bosch, and ZF Friedrichshafen, creating a concentrated innovation ecosystem emphasizing premium vehicle technologies and high-performance actuator solutions.

Competitive Landscape

The global automotive actuators market demonstrates moderate concentration with fragmented regional characteristics, where leading international suppliers command significant market shares through comprehensive product portfolios, global manufacturing footprints, and established relationships with major automotive OEMs, while numerous specialized manufacturers serve niche applications, regional markets, or specific actuator technologies.

Denso Corporation holds an estimated 12-14% global market share, leveraging its position as Toyota Group's primary supplier and extensive presence across electromechanical, electromagnetic, and pneumatic actuator categories. Robert Bosch GmbH maintains comparable market share at 11-13%, distinguished by comprehensive automotive technology portfolio spanning powertrain, chassis, and body control systems.

Continental AG commands approximately 9-11% market share, emphasizing electric actuators and advanced driver assistance applications. Other significant players, including BorgWarner Inc. (6-8% share, focusing on powertrain actuators), Hitachi Astemo (5-7% share, strong in Asian markets), and ZF Friedrichshafen (4-6% share, chassis and transmission specialization) complete the leading tier.

Key Industry Developments

- In October 2025, Nexteer Automotive company announced its Direct Drive Hand Wheel Actuator (DD-HWA) as the company’s latest advancement in Steer-by-Wire (SbW) technologies. DD-HWA establishes a new benchmark for steering feel, system integration and vehicle design flexibility enabling automakers to deliver next-generation driving experiences across software-defined vehicles and all levels of assisted and automated driving

- In May 2023, HELLA GmbH & Co. KGaA secured a number of series orders in the electromobility sector, focusing on highvoltage battery management systems, electronic valve actuators, and intelligent battery sensors.

- In May 2023, HELLA GmbH & Co. KGaA launched an electronic valve actuator (eVA) to its existing electrification portfolio. In thermal management systems, it controls valves precisely and helps ensure that the coolant is directed as required.

- In January 2023, Robert Bosch acquired eesy-ic GmbH to expand its semiconductor activities for the automotive market. Integrated circuits developed by eesy-ic are used in electronic control units (ECUs) for vehicles and other mobile solutions.

Companies Covered in Automotive Actuators Market

- Denso Corporation

- Hitachi, Ltd.

- Actus Manufacturing, Inc.

- Ansei Corporation

- ZF Friedrichshafen AG

- Nidec Corporation

- Magna International, Inc.

- Minebea Mitsumi, Inc.

- Mitsubishi Heavy Industries Ltd.

- Brose Fahrzeugteile GmbH & Co KG

- CTS Corporation

- DURA Automotive Systems

- EFI Automotive

- HELLA GmbH & Co. KGaA

- Johnson Electric Holdings Limited

- Kongsberg Automotive

- Robert Bosch GmbH

- SNT Motiv Co., Ltd.

- Stabilus GmbH

- Stoneridge Inc.

- Vitesco Technologies

- Mahle GmbH

- Other Market Players

Frequently Asked Questions

The Automotive Actuators market is estimated to be valued at US$ 38.8 Bn in 2025.

The key demand driver for the Automotive Actuators market is the rising adoption of Advanced Driver Assistance Systems (ADAS), autonomous driving technologies, and the broader shift toward vehicle electrification (including electric and hybrid vehicles).

In 2025, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global Automotive Actuators market.

Among applications, passenger car has the highest preference, capturing beyond 45% of the market revenue share in 2025, surpassing other applications.

Denso Corporation, Hitachi, Ltd., Actus Manufacturing, Inc., Ansei Corporation, and ZF Friedrichshafen AG are a few leading players in the Automotive Actuators market.