- Specialty & Fine Chemicals

- Acetylated Distarch Adipate Market

Acetylated Distarch Adipate Market Size, Share, and Growth Forecast 2026 - 2033

Acetylated Distarch Adipate Market by Source (Corn-based, Tapioca-based, Potato-based, Wheat-based, Others), by Application (Food, Pharmaceutical, Textile, Paper & Pulp, Others), by Grade (Food Grade, Pharmaceutical Grade, Industrial Grade), by Regional Analysis, 2026 - 2033

Acetylated Distarch Adipate Market Size and Trend Analysis

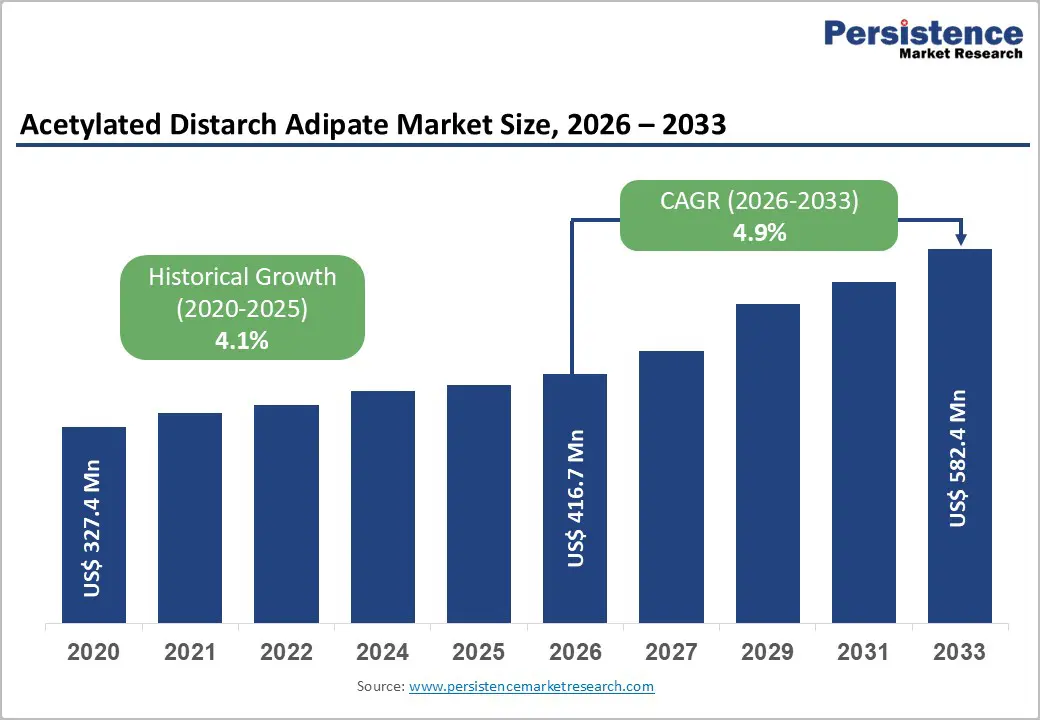

The global acetylated distarch adipate market size is expected to be valued at US$ 416.7 million in 2026 and projected to reach US$ 582.4 million by 2033, growing at a CAGR of 4.9% between 2026 and 2033.

This growth is driven by rising demand for processed and convenience foods, in which acetylated distarch adipate (E1422) functions as a reliable stabilizer and thickener that is resistant to heat, acid, and freeze-thaw cycles. Further expansion of the pharmaceutical and food sectors further fuels adoption, supported by regulatory approvals from EFSA and the FDA. Historical growth of 4.1% CAGR from 2020 - 2025 highlights steady market expansion amid urbanization and clean-label trends.

Key Industry highlights:

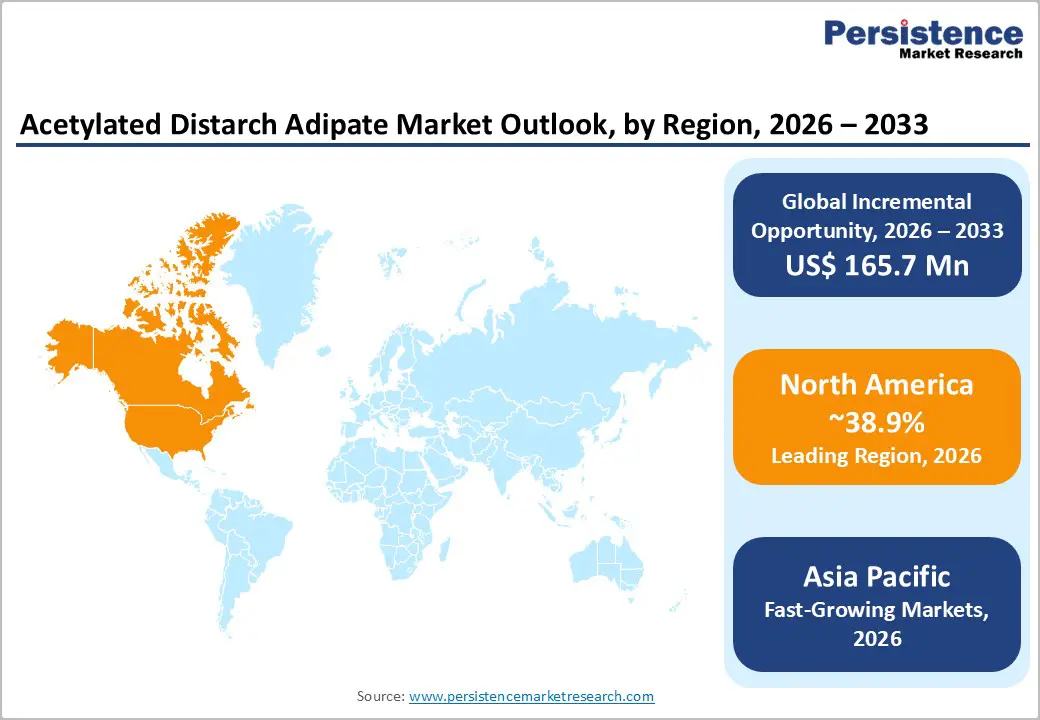

- Leading Region: North America leads the market with 38.9% share in 2025, supported by strong U.S. food processing capabilities, regulatory clarity, and widespread adoption of modified starches across food, pet food, and pharmaceutical applications.

- Fastest-Growing Region: Asia Pacific, with a 35.8% share in 2025, remains the fastest-growing region, driven by rapid urbanization, expanding food manufacturing in China and India, and cost-effective raw material availability.

- Leading Application Category: Food applications dominate, with a 65% market share in 2025, reflecting essential use in frozen, canned, and processed foods that require high stability under heat, acid, and freeze–thaw conditions.

- Fastest-Growing Category: Pharmaceutical-grade acetylated distarch adipate is the fastest-growing segment, supported by rising demand for binders and stabilizers in tablet and solid dosage formulations amid global pharmaceutical expansion.

- Key Growth Opportunity: Sustainable textiles and paper applications present strong opportunities, as eco-friendly policies and the adoption of biodegradable materials drive demand for starch-based alternatives to synthetic binders and coatings.

| Key Insights | Details |

|---|---|

| Acetylated Distarch Adipate Size (2026E) | US$ 416.7 million |

| Market Value Forecast (2033F) | US$ 582.4 million |

| Projected Growth CAGR (2026 - 2033) | 4.9% |

| Historical Market Growth (2020 - 2025) | 4.1% |

Market Dynamics

Drivers - Rising Demand for Processed and Convenience Foods Accelerates Market Adoption

The growing global consumption of convenience and ready-to-eat foods is increasing demand for reliable stabilizers such as acetylated distarch adipate (E1422). Its ability to maintain texture and viscosity in frozen, canned, and high-heat processed products makes it indispensable. FAO data indicates robust growth in processed food production, with E1422 ensuring stability in sauces, bakery goods, and dairy under shear stress and acidic conditions.

This functionality not only enhances product shelf life but also preserves sensory appeal, critical for consumer satisfaction. Urbanization and busier lifestyles in emerging economies further increase demand for ready-to-eat meals, thereby driving adoption of E1422 across both mass-market and premium processed food segments and supporting steady market expansion.

Growing Consumer Preference for Clean-Label and Functional Foods Supports Market Growth

Shifting consumer trends toward natural, plant-derived ingredients are favoring acetylated distarch adipate, sourced from corn or tapioca. Its compatibility with clean-label requirements allows manufacturers to formulate products without synthetic preservatives. Regulatory approvals, including EFSA safety endorsements and FDA GRAS status, reinforce confidence in its safe use at GMP levels.

Beyond safety, E1422 provides functional benefits, including anti-retrogradation in frozen dough and improved stability in bakery and pet foods. These performance attributes enhance product quality, texture, and longevity, thereby driving adoption of health-focused and functional food products while supporting broader global market growth for modified starches.

Restraints - High Regulatory Compliance Costs Pose Challenges for Manufacturers

Acetylated distarch adipate production is subject to stringent regulatory standards from agencies like EFSA and FDA, including strict residue limits (adipic acid ≤0.135%, acetyl ≤2.5%). Meeting these standards requires extensive testing and documentation, significantly increasing production costs. Such compliance complexities often delay new product launches, particularly in the pharmaceutical sector, where purity and stability criteria are critical for scalability.

Smaller manufacturers face disproportionate barriers due to these costs and operational requirements, limiting their market entry. Variations in global regulatory approvals further complicate production planning and distribution, thereby constraining market growth despite rising demand for processed and functional foods, particularly in regions with the strictest food and drug safety regulations.

Consumer Shift Toward Natural and Unmodified Starches Restrains Growth

Despite E1422 being plant-derived, growing consumer aversion to chemically modified starches is shifting demand toward native starch alternatives. Clean-label trends, fueled by health consciousness, have led surveys to indicate that over 30% of new food products prioritize unmodified ingredients. This changing preference creates adoption challenges for acetylated distarch adipate in sensitive segments such as infant and baby foods.

The perception of “natural” ingredients as safer or healthier continues to influence product formulation decisions. Manufacturers must navigate this consumer-driven restraint while balancing functionality and regulatory compliance, which can limit the penetration of E1422 in certain markets, particularly in premium and health-focused food categories.

Opportunity - Expansion of Pharmaceutical Applications Creates Significant Growth Opportunities

The rapid expansion of the pharmaceutical sector presents promising opportunities for acetylated distarch adipate, which functions as a reliable binder and stabilizer in tablets and withstands high-shear manufacturing processes. Increasing global pharmaceutical output, driven by WHO-reported demand for generic drugs in aging populations, is fueling this trend. Food-grade ADA currently dominates, but pharmaceutical-grade variants are growing at a higher CAGR, reflecting rising adoption.

Clean-label and safety-conscious formulations further support its integration in pharmaceutical products, enabling improved tablet stability, controlled disintegration, and consistent performance. Manufacturers can leverage this growth by developing tailored pharmaceutical-grade ADA solutions that meet regulatory standards while addressing functional needs in both emerging and mature pharmaceutical markets worldwide.

Rising Demand in Sustainable Textiles and Paper Industries Boosts Industrial Use

Industrial applications in textiles and paper, particularly in Asia Pacific manufacturing hubs, offer strong growth prospects for acetylated distarch adipate. It serves as a biodegradable adhesive and pulp stabilizer, reducing reliance on synthetic chemicals. Government policies that promote eco-friendly materials, including initiatives such as the EU Green Deal, further accelerate adoption and align with sustainability goals across industries.

Tapioca-based ADA, derived from renewable and sustainable sources, is emerging as the fastest-growing segment of raw materials. Its use in eco-conscious manufacturing processes supports significant projected volume gains, enabling companies to capitalize on both industrial growth and sustainability trends while differentiating products in a competitive market.

Category-wise Analysis

Source Insights

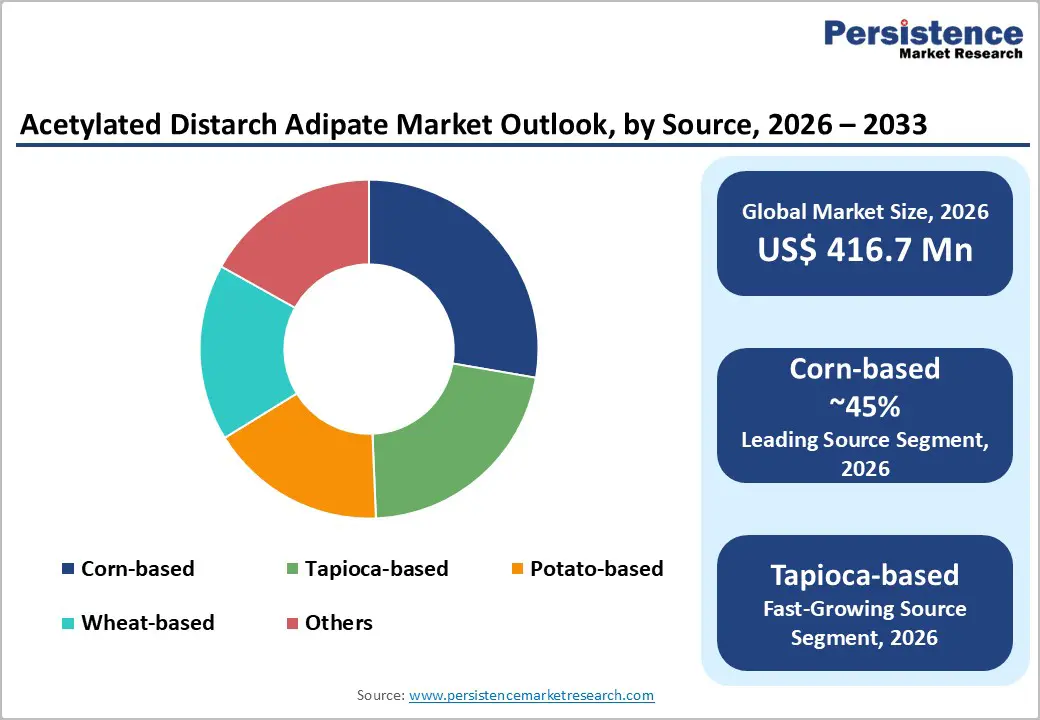

Corn-based acetylated distarch adipate leads the market with a 45% share in 2025, driven by abundant availability and cost-efficiency from major US corn-producing regions. FAO data highlights corn’s dominance in modified starch production, offering high amylopectin content for superior viscosity, texture, and stability in diverse food applications. Its versatility across food, pharmaceutical, and industrial grades reinforces its leadership position globally.

Tapioca-based starch is emerging as the fastest-growing source, favored for its clean-label appeal and sustainable sourcing. Tapioca offers excellent functional properties in freeze-thaw applications, bakery, and convenience foods. Its renewable nature and alignment with eco-conscious and plant-based trends make it increasingly attractive for manufacturers seeking both functional performance and sustainability credentials.

Application Insights

Food applications account for 65% of the market in 2025, reflecting the essential role of ADA in frozen foods, bakery items, and canned products requiring freeze-thaw stability. Regulatory approvals from EFSA and FDA enable safe usage in emulsions, sauces, and ice cream, ensuring consistent texture and preventing breakdown during processing. Rising processed food consumption strengthens the dominance of food applications.

Beyond traditional applications, pharmaceutical and industrial uses are witnessing rapid growth. ADA’s functionality as a binder and stabilizer in tablets, along with its use in biodegradable adhesives, paper coatings, and textile sizing, drives adoption. Manufacturers are increasingly leveraging these sectors for expansion, benefiting from clean-label trends and regulatory acceptance in functional formulations.

Grade Insights

Food-grade acetylated distarch adipate holds a 70% share in 2025, supported by regulatory safety approvals and high demand across bakery, pet food, and canned goods. Listings under FDA GRAS and Codex GSFA confirm its suitability, while superior gelling and stability in high-acid products reinforce its market dominance and broad applicability across processed food segments.

Pharmaceutical-grade ADA is emerging as the fastest-growing segment, driven by its use as a binder and stabilizer in solid dosage forms. With increasing demand for controlled-release tablets and functional pharmaceutical formulations, this grade is gaining traction. Its high purity, thermal and shear stability, and regulatory compliance make it a preferred choice in global pharmaceutical manufacturing.

Regional Insights

North America Acetylated Distarch Adipate Market Trends

North America holds a leading position in the global acetylated distarch adipate market, accounting for approximately 38.9% share in 2025, supported by advanced food processing infrastructure and strong innovation ecosystems in the U.S. FDA regulatory frameworks enable widespread use of E1422 in ready meals, frozen foods, and microwavable products. Clean-label reformulation trends further accelerate adoption across sauces, dairy, and convenience foods.

Beyond food, strong demand from pet food and pharmaceutical industries provides market stability. Pharmaceutical applications benefit from ADA’s binder and stabilizing properties, while pet food manufacturers rely on texture retention and shelf stability. Continuous R&D investments and regulatory clarity support product innovation, reinforcing North America’s leadership in both consumption and technological development.

Europe Acetylated Distarch Adipate Market Trends

Europe represents a mature yet steadily expanding market, driven by harmonized EFSA regulations across major economies such as Germany, the U.K., France, and Spain. The region is projected to grow at a CAGR of around 4.5% during the forecast period, supported by rising demand for processed foods and frozen bakery products. Strong compliance standards ensure consistent quality and widespread acceptance of E1422.

Sustainability initiatives, including the EU Green Deal, are driving adoption in paper, packaging, and biodegradable industrial applications. Additionally, growth in frozen dough and premium bakery products supports demand, while confectionery manufacturers leverage ADA to meet strict texture and quality benchmarks, reinforcing Europe’s balanced food and industrial demand profile.

Asia Pacific Acetylated Distarch Adipate Market Trends

Asia-Pacific is the fastest-growing regional market, accounting for approximately 35.8% of the market in 2025, driven by large-scale manufacturing capabilities in China, India, Japan, and the ASEAN countries. Rapid urbanization and changing dietary habits are driving demand for convenience and ready-to-eat foods, significantly increasing the need for stabilizers such as acetylated distarch adipate. China’s food processing expansion remains a key growth engine.

India’s cost-effective production of tapioca starch strengthens regional supply and export competitiveness. Government incentives supporting food technology, processing infrastructure, and industrial starch applications further boost adoption. Rising pharmaceutical manufacturing and increasing use in paper and textile industries position Asia Pacific as a long-term growth hub for the market.

Competitive Landscape

The global acetylated distarch adipate market is moderately consolidated, characterized by the presence of large multinational producers with strong vertical integration across raw material sourcing, processing, and distribution. Competitive positioning is shaped by advanced R&D capabilities, enabling the development of customized grades tailored for food, pharmaceutical, and industrial applications. Manufacturers focus on performance enhancement, regulatory compliance, and consistent quality to maintain long-term supply relationships.

Strategic expansion remains a key competitive approach, particularly through capacity additions and manufacturing footprints in Asia Pacific to leverage cost advantages and proximity to high-growth markets. Increasing emphasis on clean-label formulations, sustainable sourcing, and collaborative partnerships for pharmaceutical applications is shaping competitive differentiation across the market.

Key Developments:

- In January 2025, Ingredion launched a new food-grade E1422 specifically designed for frozen dough applications, improving freeze–thaw stability and extending shelf life, supported by internal research validating enhanced texture retention during cold storage and reheating cycles.

- In October 2024, Tate & Lyle expanded its corn-based acetylated distarch adipate production capacity in Europe to meet rising bakery demand, focusing on clean-label formulations that deliver consistent viscosity, improved processing tolerance, and compliance with regional regulatory standards.

- In March 2024, ADM introduced a tapioca-sourced acetylated distarch adipate variant tailored for pet food applications, delivering improved texture, binding efficiency, and moisture stability, with industry tests confirming better palatability and processing performance in dry and wet formulations.

Companies Covered in Acetylated Distarch Adipate Market

- Cargill, Incorporated

- Ingredion Incorporated

- Archer Daniels Midland Company (ADM)

- Tate & Lyle PLC

- Roquette Frères

- AGRANA Beteiligungs-AG

- Emsland Group

- Avebe U.A.

- Grain Processing Corporation

- Südstärke GmbH

- Global Bio-Chem Technology Group

- Qingdao Cerealchem Co., Ltd.

- Shandong Fuyang Biotechnology Co., Ltd.

- SPAC Starch Products (India) Ltd.

- Universal Starch-Chem Allied Ltd.

Frequently Asked Questions

The global acetylated distarch adipate market is projected to reach US$ 416.7 million in 2026, supported by steady demand from food and pharmaceutical industries.

Rising consumption of processed, frozen, and convenience foods drives demand, as E1422 provides critical heat, acid, and freeze-thaw stability in food formulations.

North America leads the market with a 38.9% share in 2025, driven by strong U.S. food processing infrastructure and supportive regulatory frameworks.

Growing use as pharmaceutical binders and expanding applications in sustainable textiles and paper offer significant long-term growth opportunities.

Leading players include Ingredion, Tate & Lyle, ADM, and Roquette Frères.