- Nutraceuticals & Functional Foods

- Dietary Supplements Ingredients Market

Dietary Supplements Ingredients Market Size, Share, and Growth Forecast, 2025 - 2032

Dietary Supplements Ingredients Market by Ingredients Type (Vitamin, Botanicals, Minerals), Form (Tablets, Capsules, Powder), Health Application (General Health and Wellness, Bone and Joint Health, Energy and Weight Management, Gastrointestinal and Gut Health, Immunity Enhancement, Cardiovascular Health), and Regional Analysis for 2025 - 2032

Dietary Supplements Ingredients Market Size and Trends Analysis

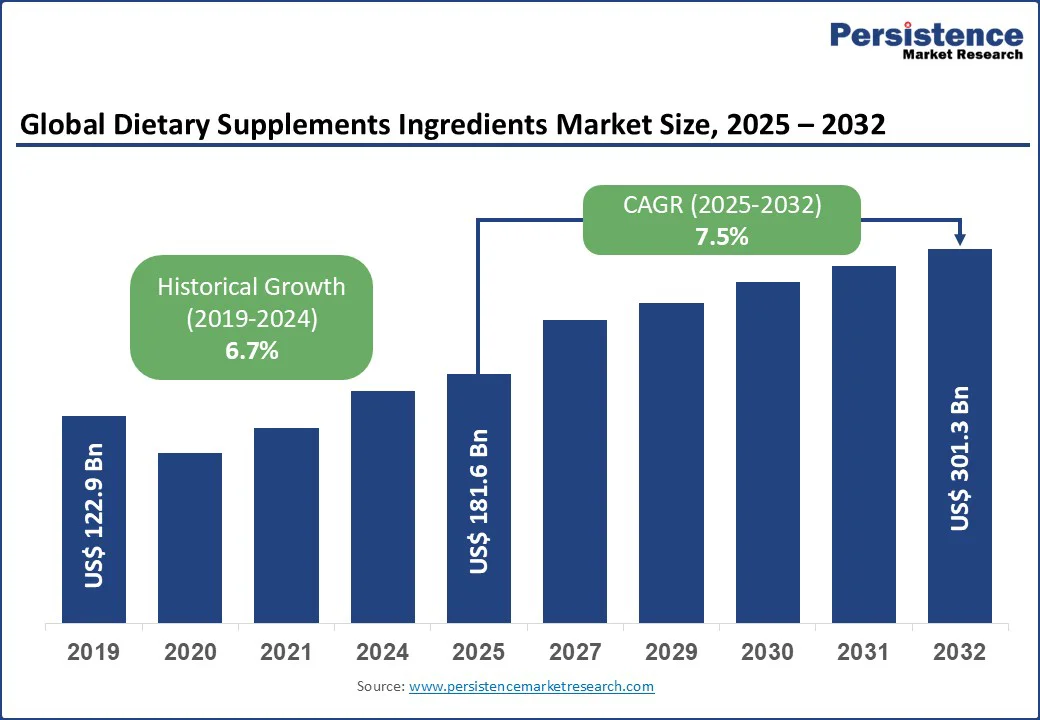

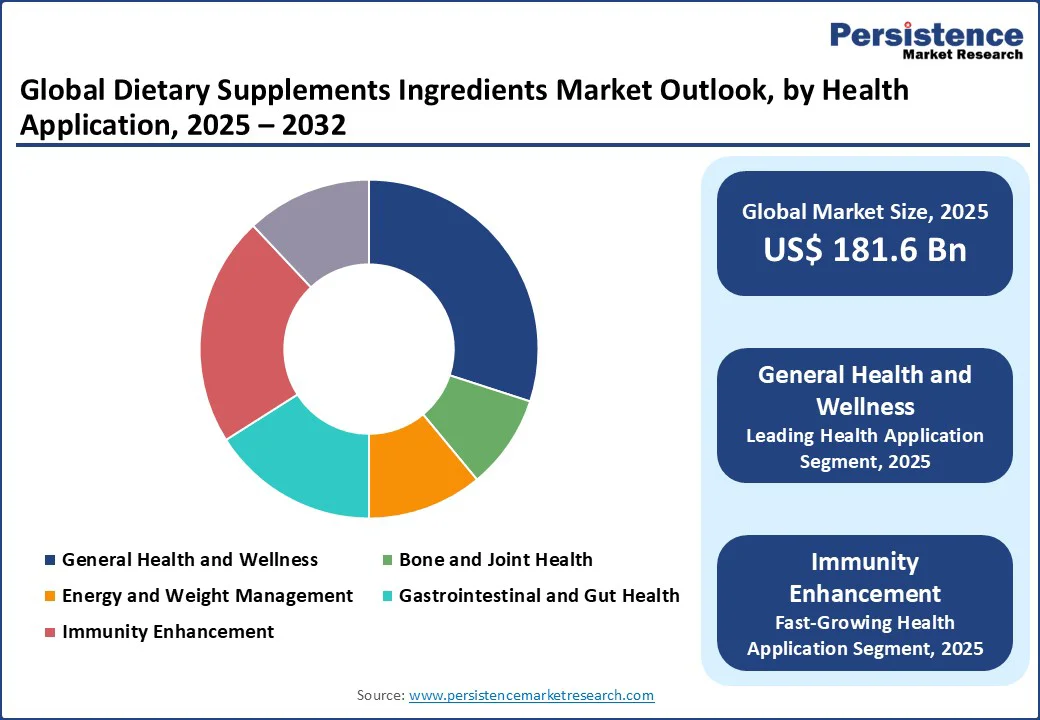

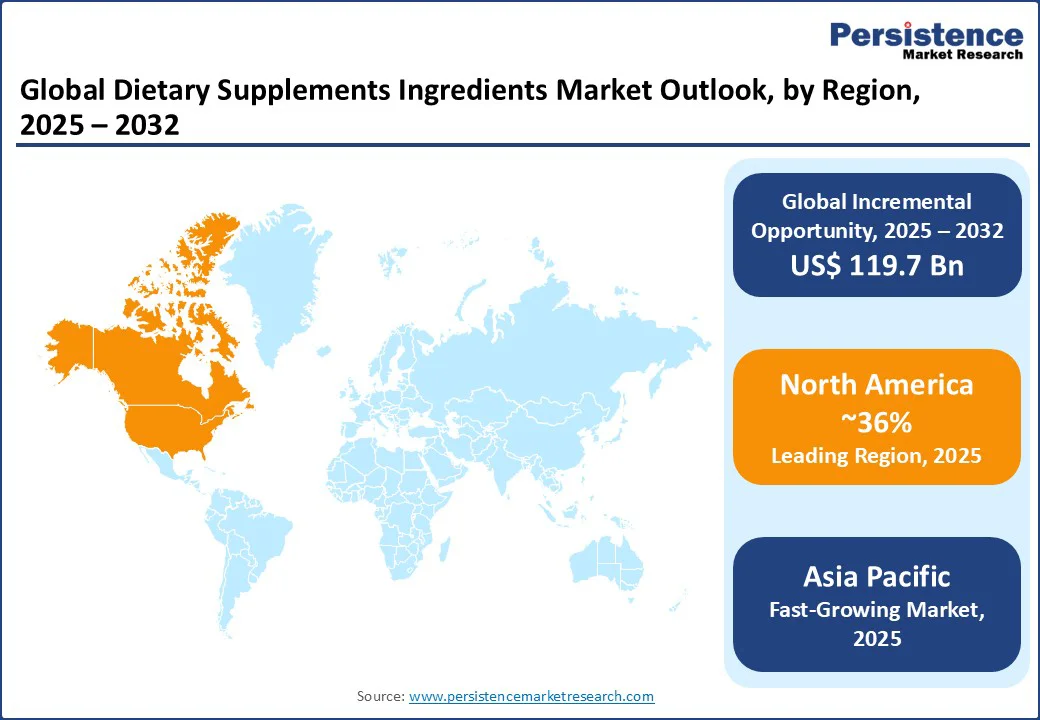

The global dietary supplements ingredients market size is likely to be valued at US$181.6 Bn in 2025 and is estimated to reach US$301.3 Bn by 2032, registering a CAGR of 7.5% during the forecast period from 2025 to 2032.

The dietary supplements ingredients market has experienced steady growth, driven by increasing health consciousness, advancements in supplement formulations, and rising demand for natural and functional ingredients. The growing focus on preventive healthcare and wellness trends further propels market expansion across retail, pharmaceutical, and e-commerce channels.

Key Industry Highlights:

- Leading Region: North America holds a 36% market share in 2025, driven by advanced healthcare infrastructure, high consumer awareness, and strong adoption of innovative supplement ingredients in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rising health investments, increasing lifestyle disease prevalence, and expanding wellness facilities in countries such as China and India.

- Dominant Ingredients Type: Vitamin accounts for 29% of the global dietary supplements ingredients market share, driven by its critical role in essential nutrient supplementation.

- Leading Form: Tablets lead with a 30% share, reflecting high global demand for convenient supplement formats.

|

Global Market Attribute |

Key Insights |

|

Dietary Supplements Ingredients Market Size (2025E) |

US$181.6 Bn |

|

Market Value Forecast (2032F) |

US$301.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.7% |

Market Dynamics

Driver - Rising Health Consciousness and Wellness Trends Push Demand

The global surge in health-conscious consumers and the adoption of preventive healthcare are key drivers of the dietary supplements ingredients market. The World Health Organization estimates that the prevalence of non-communicable diseases (NCDs) accounts for 74% of all deaths worldwide, with over 41 million deaths each year from diseases such as cancer, diabetes, and cardiovascular disease.. The rising incidence of these conditions, particularly in urban population, drives demand for nutrient-rich supplement ingredients, such as vitamins and minerals.

Technological advancements in ingredient extraction and formulation continue to propel significant market growth, as companies introduce products designed for higher efficacy and consumer appeal. For instance, DuPont’s bioavailable vitamin formulations are engineered to deliver improved absorption and greater effectiveness, enhancing overall consumer satisfaction and trust in dietary supplements. Supporting this trend, recent studies highlight that fortified supplements play an important role in reducing nutrient deficiencies, offering a more reliable alternative compared to traditional diets. The rising integration of natural botanicals, clean-label ingredients, and sustainable sourcing practices further accelerates adoption across wellness-focused consumer groups who increasingly prioritize transparency and eco-friendly solutions.

In parallel, government initiatives and rising investments in wellness infrastructure are boosting demand. In India, national nutrition programs such as POSHAN Abhiyaan have expanded access to affordable supplements, addressing gaps in public nutrition. Meanwhile, in North America, supportive policies promoting dietary wellness are encouraging retailers to diversify product portfolios, resulting in expanded shelf space and growing consumer engagement.

Restraint - High Costs and Supply Chain Challenges Restrict Adoption of dietary supplements

The high costs of dietary supplement ingredients continue to hinder widespread adoption, particularly in emerging markets. These products, often made with premium ingredients such as organic botanicals and bio-engineered vitamins, command high prices. Beyond the initial purchase cost, ongoing expenses for sourcing sustainable raw materials, such as non-GMO minerals, and certification requirements add to the total cost. For consumers in resource-limited regions, such as parts of Latin America and rural India, these financial burdens are difficult to justify, even with growing demand for health supplements. Premium ingredients are often priced significantly higher than conventional options, limiting accessibility.

The need for stable supply chains to source supplement ingredients also restricts market growth. Volatile commodity prices for botanicals such as herbs and minerals require specialized logistics, and industry reports highlight shortages of organic suppliers in the Asia Pacific regions. This supply gap, combined with high transportation costs, further limits the adoption of innovative products in developing regions, where logistics expenses can substantially increase retail prices.

Opportunity - Innovation in Functional Ingredients and Sustainable Sourcing Boosts Consumption

The development of functional and bioavailable supplement ingredients is creating substantial growth opportunities, particularly within wellness-oriented markets, personalized nutrition, and health-specific segments. These advanced formulations are designed to overcome the limitations of traditional supplements by offering improved absorption and targeted benefits, making them highly effective for lifestyle management, preventive care, and specific health needs. As consumer preferences continue shifting toward personalized wellness solutions, the demand for functional products is accelerating, especially in regions where dietary restrictions or nutrient deficiencies are more prevalent.

Alongside personalization, the growing emphasis on sustainability and clean-label trends is shaping product innovation. Plant-based, organic, and eco-friendly variants are gaining traction, requiring advanced formulations with precise nutrient balancing to meet consumer expectations. Clinical research supports this movement, with studies showing that functional ingredients such as probiotics can significantly improve gut health compared to conventional approaches, further driving adoption. For instance, the National Center for Complementary and Integrative Health (NCCIH), part of the U.S. National Institutes of Health, provides detailed information on probiotics. These are defined as live microorganisms that can confer health benefits when consumed in adequate amounts.

Additionally, the rapid expansion of e-commerce platforms is reshaping market accessibility. Direct-to-consumer sales, subscription-based models, and digital engagement are strengthening consumer connections. Companies such as Amway Corp. are leveraging digital tools to provide personalized recommendations and streamline distribution, reducing reliance on traditional retail. This digital transformation, combined with rising online supplement ingredient sales, is fueling broader market expansion by improving accessibility, convenience, and consumer engagement.

Category-wise Insights

Ingredients Insights

The global dietary supplements ingredients market is segmented into vitamins, botanicals, and minerals. Vitamin dominates, holding approximately 29% of the dietary supplements ingredients market share in 2025, due to their critical role in providing essential nutrients for general health. Advanced vitamin products, such as Bayer AG’s bioavailable formulations, are widely used for their efficacy and benefits.

Botanicals are the fastest-growing segment, driven by increasing demand for natural, plant-based supplements. Innovations in herbal extracts, such as GlaxoSmithKline plc.’s options, enhance value and appeal, boosting adoption in wellness applications.

Form Insights

The global dietary supplements ingredients market is divided into Tablets, Capsules, and Powder. Tablets lead with a 30% share in 2025, driven by their convenience and high global popularity, with millions of units consumed annually for their ease of use and dosage accuracy.

Powder is emerging as the fastest-growing supplement segment, driven by consumer demand for customizable, convenient, and easily mixable formats. Its versatility supports applications across sports nutrition, wellness, and functional foods, fueling widespread adoption and expanding opportunities in global markets.

Health Application Insights

By type, the market is segmented into general health and wellness, bone and joint health, energy and weight management, gastrointestinal and gut health, immunity enhancement, and cardiovascular health. General health and wellness dominates with a 30% share in 2025, driven by broad consumer demand for daily supplements.

Immunity Enhancement is the fastest-growing segment, driven by heightened post-pandemic health awareness and strong demand for immune-boosting ingredients. Continuous innovations in formulations, including botanicals, vitamins, and probiotics are accelerating adoption, making it a key growth driver.

Regional Insights

North America Dietary Supplements Ingredients Market Trends

In North America, the U.S. is dominant , and expected to account for 36% market share in 2025, driven by high health awareness and advanced wellness infrastructure. Demand for vitamins and botanical ingredients is accelerating, driven by the rising emphasis on preventive and personalized nutrition. Consumers are increasingly seeking supplements that align with individual health goals, prompting leading players such as Amway Corp. and Abbott to introduce innovative product lines tailored to evolving needs. This shift highlights a strong preference for sustainable and functional supplement systems, with companies such as Pfizer Inc. adopting advanced natural extraction techniques to maximize nutritional value and product efficacy.

Health consciousness remains the primary purchase driver, reinforced by stringent FDA regulations that ensure safety, transparency, and the use of clean-label ingredients. Additionally, supportive government policies that encourage wellness initiatives and nutritional awareness are fostering industry expansion. These developments are boosting production capacity and shaping a highly dynamic, competitive market landscape where innovation, sustainability, and compliance are central to growth.

Europe Dietary Supplements Ingredients Market Trends

Europe’s dietary supplements ingredients market is strongly led by Germany, the U.K., and France, supported by strict regulatory frameworks and rising consumer preference for natural and functional supplements. Germany commands a significant share, with established brands such as Bayer AG and Glanbia plc driving sales of vitamins, minerals, and fortified products that align with preventive health trends. The EU’s comprehensive Food Safety Regulations foster compliance, innovation, and consumer trust.

In the U.K., growth is fueled by functional supplement blends, with companies such as NU SKIN meeting demand for personalized wellness solutions. France demonstrates increasing adoption of botanical-based supplements, supported by companies such as GlaxoSmithKline plc. Government policies encouraging sustainable nutrition and eco-conscious formulations further reinforce market prospects across the region.

Asia Pacific Dietary Supplements Ingredients Market Trends

Asia Pacific is projected to be the fastest-growing region owing tostrong contributions from China, India, and Japan. In India, the increasing prevalence of lifestyle-related diseases, coupled with government-led initiatives such as POSHAN Abhiyaan, is boosting demand for affordable vitamin and mineral ingredients. Companies such as RBK Nutraceuticals Pty Ltd are capitalizing on this by offering cost-effective, high-quality solutions to address nutritional deficiencies. China’s market expansion is fuelled by rapid retail development, urbanization, and rising middle-class demand for functional and personalized supplements.

Global leaders such as DuPont de Nemours, Inc. are actively tailoring product portfolios to suit local consumer preferences. Meanwhile, Japan emphasizes premium, high-nutrition ingredients, with brands such as XanGo, LLC gaining strong traction among health-conscious consumers. The rapid penetration of e-commerce platforms across the region further accelerates accessibility and growth, enabling direct-to-consumer sales and strengthening overall market potential.

Competitive Landscape

The dietary supplements ingredients market is intensely competitive, with global and regional players emphasizing innovation, sustainability, and strict regulatory compliance. The growing demand for functional and natural ingredients is heightening rivalry as companies strive to meet evolving health standards. Strategic partnerships, product launches, and regulatory approvals remain central to sustaining growth and competitive positioning.

Industry Developments:

- In February 2025, GetHealthy and Vitaboom announced a strategic alliance aimed at revolutionizing the personalized nutrition sector. The partnership intends to provide consumers with personalized supplement recommendations and wellness plans by fusing GetHealthy's cutting-edge digital health platform with Vitaboom's knowledge of nutritional supplements. The collaboration makes it simpler for people to reach their health objectives by using AI-driven insights and user data to develop customized nutrition solutions.

- In October 2025, higher concentration VitaCholine was introduced by Vantage Nutrition in clear liquid capsules. These capsules contain 275–550 mg of free choline each, making them a distinctive and aesthetically pleasing dosage. The new capsules will be on display at Supply Side West in Las Vegas, demonstrating Vantage Nutrition's dedication to quality, innovation, and quick market delivery.

Companies Covered in Dietary Supplements Ingredients Market

- Amway Corp.

- Abbott

- Bayer AG

- Glanbia plc

- Pfizer Inc.

- Archer Daniels Midland

- NU SKIN

- GlaxoSmithKline plc.

- Herbalife Nutrition Ltd.

- Nature's Sunshine Products, Inc.

- XanGo, LLC

- RBK Nutraceuticals Pty Ltd

- American Health

- DuPont de Nemours, Inc.

- Others

Frequently Asked Questions

The dietary supplements ingredients market is projected to reach US$181.6 Bn in 2025.

Rising health consciousness, technological advancements, and government health initiatives are key drivers.

The dietary supplements ingredients market is poised to witness a CAGR of 7.5% from 2025 to 2032.

Innovation in functional ingredients and sustainable sourcing presents significant growth opportunities.

Amway Corp., Bayer AG, and Glanbia plc are among the key players.