ID: PMRREP13987| 192 Pages | 11 Sep 2025 | Format: PDF, Excel, PPT* | Chemicals and Materials

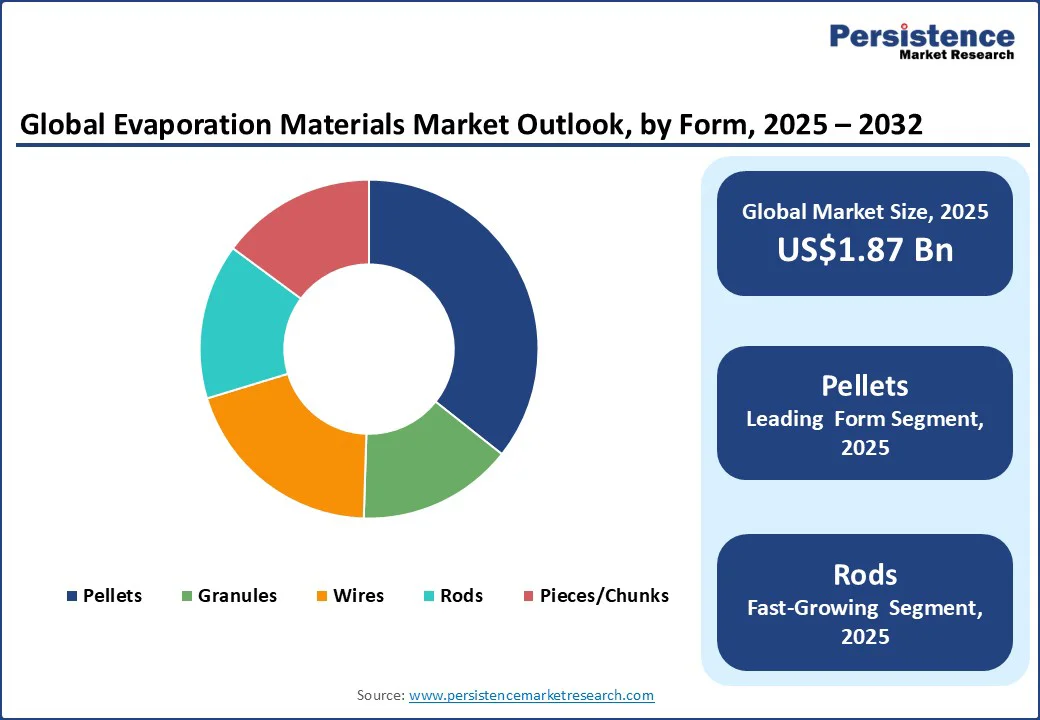

The global evaporation materials market size is likely to be valued at US$1.87 Bn in 2025 and is expected to reach US$2.88 Bn by 2032, growing at a CAGR of 6.9% during the forecast period from 2025 to 2032.

Key Industry Highlights:

| Global Market Attribute | Key Insights |

|---|---|

| Evaporation Materials Market Size (2025E) | US$1.87 Bn |

| Market Value Forecast (2032F) | US$2.88 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.9% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.1% |

The evaporation materials market is evolving rapidly, driven by surging demand in semiconductor manufacturing, thin-film coatings, and advanced display technologies such as OLED and AMOLED.

The demand for compound evaporation materials such as indium gallium zinc oxide (IGZO), quaternary alloys, and metal-ceramic composites is expanding rapidly in advanced optics, micro-LED, and photonic devices.

Manufacturers in East Asia are investing in new facilities to produce ultra-high-purity evaporation sources that enable precise thin-film deposition for specialized applications. This shift is steering the market away from conventional single-metal sources toward high-value, multi-element materials that deliver superior performance in reconfigurable photonics and next-generation display technologies.

Nanomaterial-infused evaporation materials are gaining traction as key enablers of miniaturized and flexible devices, particularly in sectors such as wearables, transparent displays, and flexible electronics.

Advanced solutions such as nanoparticle-infused oxides, metal-ceramic blends, and phase-change thin films allow smoother coatings, higher material utilization, and better electrical properties compared to traditional targets. These innovations are accelerating adoption among electronics manufacturers seeking improved device efficiency and reliability, making nanostructured evaporation materials a critical market driver.

The evaporation materials market faces risks due to its reliance on geographically concentrated sources of high-purity metals such as aluminum, silver, and specialty alloys. Any disruption in mining operations, export restrictions, or geopolitical tensions can directly affect the supply of these raw materials. Companies using vacuum-grade aluminum ingots or other sensitive inputs also require strict climate-controlled logistics, making transportation delays more likely. This dependence on fragile supply chains creates uncertainty for manufacturers and can extend lead times significantly.

Inconsistent coating density remains a technical challenge for evaporation materials, especially when compared with alternative deposition technologies. Variations in evaporation rates often lead to uneven crystallinity and lower-density coatings, which reduce performance in applications of micro-LEDs, advanced optics, and photonic devices. Thin-film manufacturers that rely on precise evaporation rate control struggle to maintain uniformity across larger substrates. These limitations can restrict adoption and push some end-users to explore more stable coating processes.

The market has a strong opportunity in scaling ultra-high-purity alloy evaporation sources, particularly ternary and quaternary compounds designed for ion-assisted deposition. Recent investments in East Asia have expanded capacity for producing specialty metals used in advanced photonics and display technologies.

Strategic partnerships between equipment manufacturers and material suppliers, along with venture funding for startups developing IGZO and phase-change alloys, are accelerating innovation in this space. This creates room for suppliers to position themselves in high-growth areas such as micro-LEDs, reconfigurable optics, and next-generation thin-film devices.

Emerging manufacturing hubs in Southeast Asia and Eastern Europe are presenting new opportunities for the adoption of compound evaporation materials. Planned installations of PVD systems in Vietnam and Poland are expected to create strong regional demand in the coming years.

At the same time, sustainability initiatives are driving interest in recycling technologies that can recover over 90% of spent evaporation materials, reducing both costs and waste. These trends open the door for companies to establish localized supply chains while also tapping into the growing push for circular economy solutions within the evaporation materials industry.

Metals are anticipated to be the largest segment in the evaporation materials market, accounting for nearly 40.3% of the total share in 2025. Aluminum, gold, and silver dominate this category due to their widespread use in semiconductors, photovoltaic cells, and optical coatings.

Their high conductivity, excellent film uniformity, and thermal stability make them essential for large-scale manufacturing. For instance, aluminum is a preferred material in integrated circuit fabrication and thin-film solar cells, making metals a core driver of overall market demand.

On the other hand, nanostructured materials are emerging as the fastest-growing segment. With an expected growth rate of around 15% annually, engineered nanopowders and nano-oxides are gaining traction in advanced electronics, flexible displays, and energy storage systems.

Their high surface area and ability to deliver superior thin-film properties are pushing adoption in next-generation applications. For instance, nano-enhanced IGZO films are increasingly used in micro-LEDs and transparent displays, signaling how nanomaterials are reshaping the market landscape.

Among the different physical forms, pellets are projected to dominate with a market share of 35.7% in 2025. These forms are preferred for their stability during evaporation and ease of handling in electron-beam and thermal evaporation systems.

Pellets provide consistent size and shape, ensuring uniform deposition, and are widely used in high-purity applications, where reliable material feeding is critical. Many suppliers offer aluminum and IGZO sources in pellet form, underlining their role as industry standards.

The fastest-growing form is rods, particularly specialty multi-component rods designed for high-throughput applications. Their ability to combine multiple alloys or compounds in a single source makes them ideal for advanced coating systems.

For example, ULVAC’s multi-zone rods have improved throughput by over 15%, while Nichia’s YSZ rods are valued in optics for producing smoother, defect-free coatings. These innovations make rods increasingly attractive for high-performance electronics and photonics manufacturing.

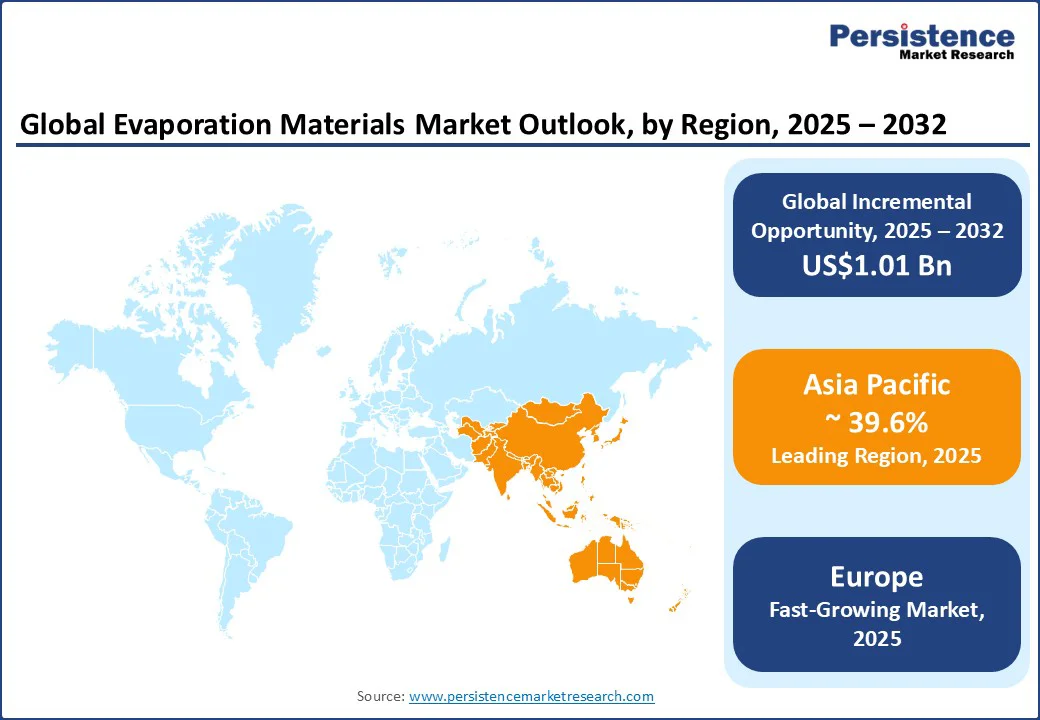

Asia Pacific is anticipated to lead the market, holding a market share of 39.6% in 2025. The region serves as the global center for electronics and semiconductor manufacturing, with China, South Korea, Japan, and Taiwan driving a growing need for ultra-high-purity evaporation sources.

Expanding solar power initiatives and aggressive investment in display technologies are further accelerating demand.

China accounts for over half the regional market, driven by its ongoing efforts to boost semiconductor self-sufficiency and accelerate the deployment of solar photovoltaics. Over US$120 Mn was invested in 2023 to expand production lines for ultra-pure metals used in thin-film deposition.

Companies such as BOE Technology and CSOT are ramping up in-house manufacturing capacity for OLED and quantum dot displays, while new facilities in Sichuan and Jiangsu are increasing monthly production of evaporation-grade materials such as indium and gallium.

South Korea is emerging as a key hub for advanced compound materials, with particular focus on micro-LEDs, photonics, and next-generation displays. Manufacturers such as Samsung SDI and SK Materials are developing evaporation sources such as indium-gallium-zinc oxide (IGZO), which enhance display performance and transistor efficiency.

Collaborative efforts between Korean universities and material suppliers are also helping introduce more sustainable production methods, including recyclable crucibles and waste-reducing deposition techniques.

Europe is expected to be the fastest-growing regional market for evaporation materials, with a high CAGR. The expansion is supported by the European Union’s renewable energy objectives, which are promoting extensive solar PV adoption, along with increasing demand across the automotive, aerospace, and healthcare industries. These industries increasingly rely on high-performance coatings for sensors, optics, and functional surfaces, which boost the demand for advanced evaporation materials.

Germany leads due to its innovation in sustainable production and composite materials. Its automotive and aerospace sectors are integrating thin-film coatings to improve fuel efficiency, reduce weight, and extend product lifespan.

Companies such as Heraeus and Umicore are focusing on recyclable and high-value materials that meet both technical and environmental standards. Research institutes such as the Fraunhofer Society are supporting this growth by developing composite materials suitable for extreme UV lithography and other cutting-edge applications.

In the U.K., a strong emphasis on R&D supports continued progress in medical devices, optics, and quantum technologies. Firms such as Oxford Instruments are producing customizable evaporation sources for use in quantum sensors and bio-compatible electronics. Collaborations with institutions such as the University of Cambridge are also pushing forward innovations in perovskite solar coatings, which are being refined using energy-efficient vacuum deposition methods.

North America remains an important market, supported by a strong foundation in electronics, semiconductors, aerospace, and renewable energy. The demand is largely shaped by ongoing investment in advanced manufacturing and research-led innovation, particularly in high-tech industries that rely on thin-film coatings.

The U.S. remains the dominant force in the region, with U.S.-based companies Materion, ULVAC Technologies, and Kurt J. Lesker Company developing high-purity and more efficient evaporation sources to meet evolving industry needs. For instance, Materion introduced a high-purity aluminum evaporation rod in 2023, which significantly improved deposition rates and minimized material waste, helping manufacturers align with sustainability goals.

Kurt J. Lesker has expanded its range of tailored alloy materials to support the rising demand for OLED displays and compound semiconductors. The country also benefits from strong collaboration between industry and academia. Leading institutions such as MIT and UC Berkeley are actively involved in developing next-generation materials for flexible electronics, quantum computing, and bio-integrated devices, broadening the scope of evaporation material applications.

The global evaporation materials market is moderately consolidated, with a mix of global leaders and regional specialists competing on purity levels, customized formulations, and application-specific solutions.

Established players such as Materion, ULVAC Technologies, and Kurt J. Lesker dominate with strong portfolios of metals, alloys, and nanostructured materials tailored for semiconductors, displays, and aerospace applications. Their strategies include R&D collaborations with end-use industries, long-term contracts, and investments in ultra-high purity grades to meet the stringent demands of advanced manufacturing.

Alongside these leaders, regional players in Asia Pacific and Europe are offering cost-effective materials and specialized compounds for solar PV and optical applications. Companies in China, South Korea, and Japan are scaling capacity for compound and nanostructured targets to capture growing semiconductor and renewable energy demand.

Differentiation is increasingly shifting from price to technological innovation, with partnerships, joint ventures, and acquisitions emerging as key strategies to strengthen market share and ensure secure supply chains.

The evaporation materials market size is estimated at US$1.87 Bn in 2025, driven by increasing demand from semiconductor, display, and optical coating applications.

By 2032, the evaporation materials market is projected to reach US$2.88 Bn.

Key trends include the adoption of nanostructured evaporation sources for uniform thin-film coatings, the rising use of compounds in advanced optoelectronics, and the growing demand for eco-efficient vacuum deposition processes.

Metals dominate the material type segment with over 40.3% share, while pellets lead in form with more than 35.7% share, due to their efficiency in uniform deposition and widespread use in display and semiconductor manufacturing.

The evaporation materials market is expected to grow at a CAGR of 6.9% from 2025 to 2032, supported by semiconductor expansion, thin-film solar developments, and innovations in high-purity alloys.

Prominent players include Materion Corporation, ULVAC Technologies, Kurt J. Lesker Company, and Nichia Corporation.

| Report Attribute | Details |

|---|---|

| Historical Data/Actuals | 2019 - 2024 |

| Forecast Period | 2025 - 2032 |

| Market Analysis | Value: US$ Bn |

| Geographical Coverage |

|

| Segmental Coverage |

|

| Competitive Analysis |

|

| Report Highlights |

|

By Material Type

By Form

By Application

By End-user

By Region

Delivery Timelines

For more information on this report and its delivery timelines please get in touch with our sales team.

About Author