- Renewable Energy

- CIGS Thin-Film Solar Cells Market

CIGS Thin-Film Solar Cells Market Size, Share, and Growth Forecast, 2026 - 2033

CIGS Thin-Film Solar Cells Market By Product Type (Flexible CIGS Thin Film Solar Cells, Rigid CIGS Thin Film Solar Cells), Application (Residential, Commercial, Utility-Scale), End-user (Energy & Power, Building & Construction, Others), and Regional Analysis for 2026 - 2033

CIGS Thin-Film Solar Cells Market Size and Trends Analysis

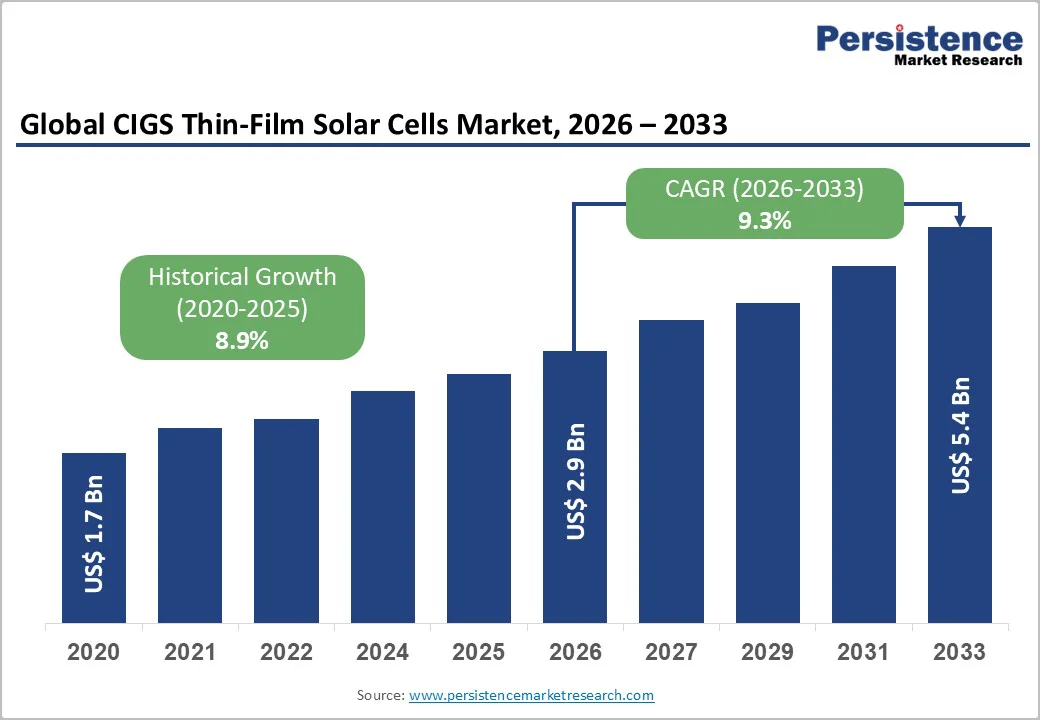

The global CIGS thin-film solar cells market size is likely to be valued at US$2.9 Billion in 2026 and is expected to reach US$5.4 Billion by 2033, growing at a CAGR of 9.3% during the forecast period from 2026 to 2033, driven by increasing demand for renewable energy, supportive government incentives, and CIGS technology's advantages in flexibility and low-light performance.

Expanding adoption of building-integrated photovoltaics (BIPV), such as solar façades, flexible rooftop membranes, and semi-transparent modules, is accelerating market penetration in both residential and commercial sectors.

Growing investments in BIPV, portable solar devices, and off-grid power solutions further accelerate adoption, as CIGS modules enable seamless integration into rooftops, facades, and infrastructure.

Key Industry Highlights:

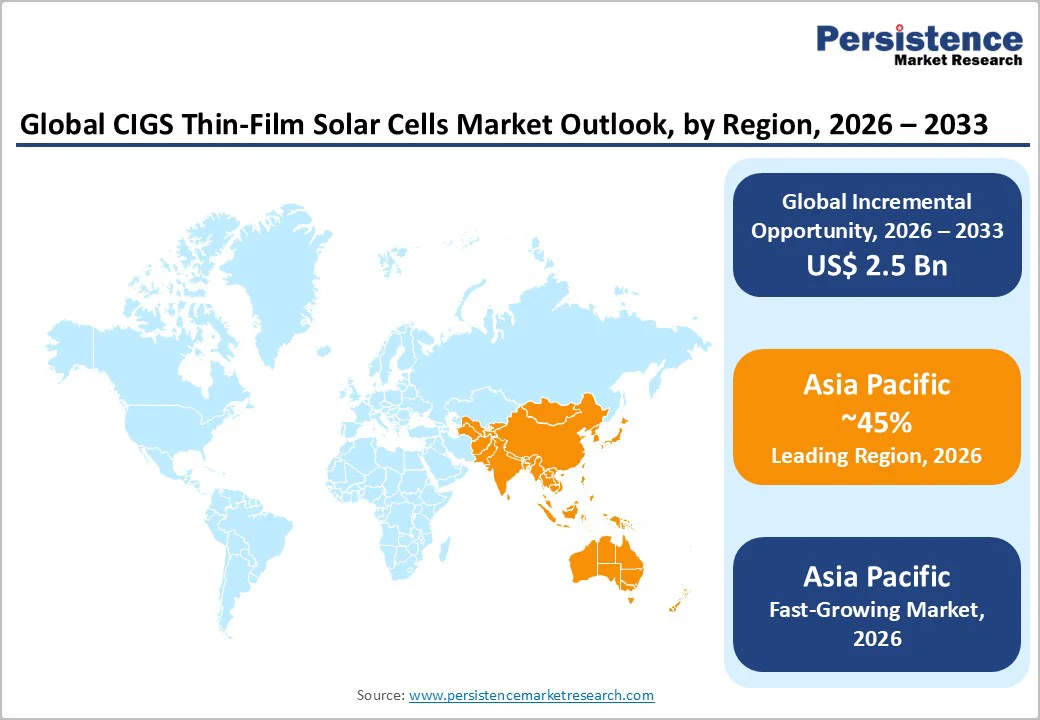

- Leading Region: Asia Pacific is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong deployment in China and Japan and large-scale manufacturing capacity.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by aggressive solar targets, rising investments, and cost-competitive manufacturing advantages.

- Leading Product Type: Rigid CIGS thin-film solar cells are expected to be the dominant product type in 2026, accounting for 60% of the market share, due to their durability and reliable performance in utility-scale and rooftop installations.

- Leading Application Type: Utility-scale is anticipated to be the leading application, accounting for over 45% of the revenue share in 2026, benefiting from economies of scale and the efficiency advantages of rigid CIGS modules.

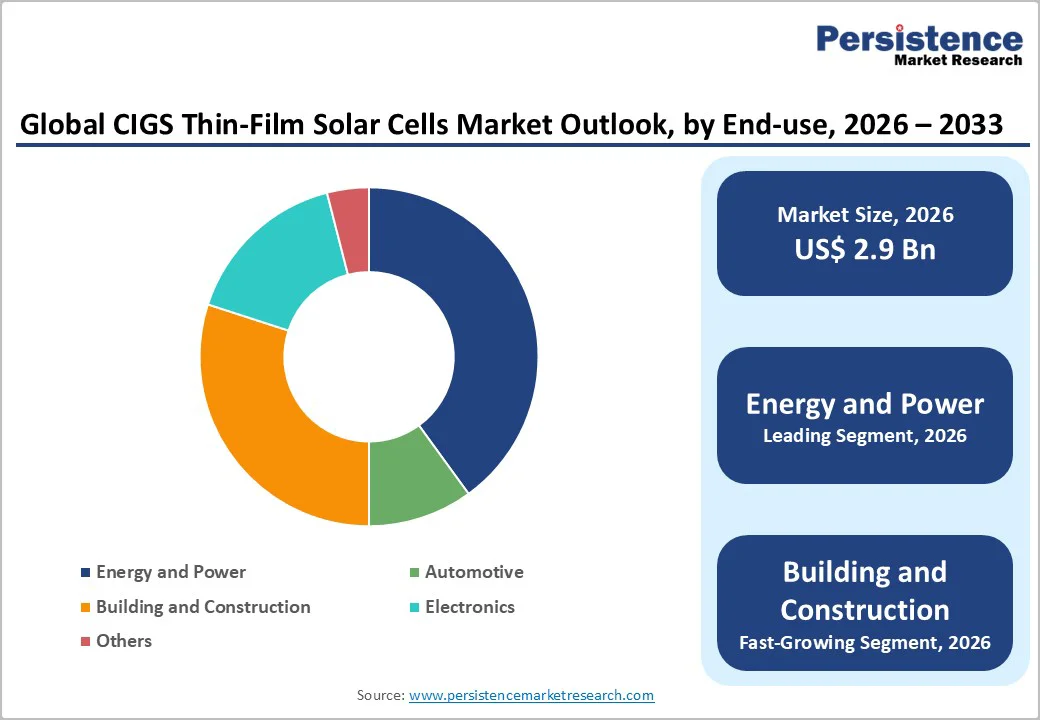

- Leading End-user: Energy and power is the leading end-user segment, contributing 58.3% of total revenue share, driven by large utility and distributed generation projects.

| Key Insights | Details |

|---|---|

| CIGS Thin-Film Solar Cells Market Size (2026E) | US$2.9 Bn |

| Market Value Forecast (2033F) | US$5.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Push for Renewable Energy Transition

The shift toward renewable energy is a major force accelerating the adoption of CIGS thin-film solar cells. Governments across developed and emerging economies are rapidly increasing clean-energy targets to lower carbon emissions and reduce dependence on fossil fuels.

This transition is supported by large-scale policy frameworks, which emphasize solar as a central pillar of decarbonization. Growing utility and commercial investments also create strong momentum for thin-film alternatives that offer superior performance in diverse environments.

The renewable-energy shift encourages widespread investment in advanced solar technologies, including lightweight and flexible modules that enable integration beyond traditional applications. This aligns directly with the strengths of CIGS, particularly for building-integrated photovoltaics (BIPV), portable solar, and next-generation power systems.

As countries prioritize sustainability and energy security, installation volumes continue to climb, supporting the requirement for efficient thin-film panels. CIGS modules are increasingly adopted in regions with land constraints or architectural restrictions, where their design flexibility offers a unique advantage.

Competition from Established Silicon Technologies

The CIGS thin-film solar cells market continues to face strong competitive pressure from conventional crystalline silicon (c-Si) technologies, which dominate global solar deployments due to their high efficiency, long-term reliability, and strong manufacturing ecosystem.

Silicon modules benefit from decades of technological maturity, streamlined manufacturing, and large-scale global production, making them cheaper and more widely adopted than CIGS alternatives. Their well-established supply chains further reduce procurement risks, making silicon a default choice for developers.

The continuous efficiency improvements are seen in mainstream silicon technologies, including PERC, TOPCon, and heterojunction (HJT) modules. These advancements raise the performance benchmark, widening the gap CIGS must overcome to strengthen its market position.

Silicon’s robust certification history and widespread bankability offer financiers greater confidence, creating additional hurdles for CIGS adoption in utility-scale and commercial projects. Silicon’s rapid integration into bifacial and high-power module formats enhances its competitiveness across diverse climatic conditions.

Flexible Electronics and Portable Applications

The rise of flexible electronics is opening significant opportunities for CIGS thin-film solar cell manufacturers. As consumer devices, wearables, and portable power solutions increasingly demand lightweight, bendable, and compact energy sources, CIGS technology fits these needs better than traditional rigid silicon modules.

Its high power-to-weight ratio and strong performance under bending or partial shading make it ideal for emerging applications such as foldable devices, smart textiles, e-paper, and ultra-thin portable power solutions.

Outdoor recreation, military equipment, emergency response kits, and systems are adopting portable solar chargers and rollable panels at a fast pace. CIGS cells perform well even under low-light, cloudy conditions, or variable angles, giving them a competitive advantage in real-world field use.

With growing demand for off-grid power, consumer convenience, and compact renewable solutions, flexible CIGS emerges as a high-growth opportunity area, encouraging manufacturers to scale flexible module lines and collaborate with electronics and wearable tech brands.

Category-wise Analysis

Product Type Insights

Rigid CIGS thin-film solar cells lead the CIGS thin-film solar cells market, capturing around 60% of the total revenue share, due to their proven durability, structural stability, and consistent long-term field performance. Their higher mechanical robustness and lower degradation rates make them a preferred choice for utility-scale solar farms and commercial rooftops, where longer operating life and reliability are paramount.

These modules integrate well with existing mounting systems and deliver stable efficiency across wide temperature fluctuations, reinforcing their suitability for large, grid-connected projects. For example, several large rooftop solar deployments in Europe have adopted rigid CIGS modules to enhance output under variable light conditions, demonstrating their reliability in mature solar markets.

Flexible CIGS thin-film solar cells are the fastest-growing product segment, fueled by rising demand for lightweight, versatile, and aesthetically adaptable solar solutions. Their ability to bend and conform to curved or irregular surfaces makes them particularly suitable for building-integrated photovoltaics (BIPV), electric vehicles, agricultural rooftops, temporary shelters, and emerging mobile power applications.

This flexibility enables deployment in locations where traditional rigid panels are impractical, broadening their use across modern architectural designs and portable energy solutions. For instance, flexible CIGS laminates are increasingly being incorporated into solar roof membranes for advanced BIPV projects, while companies in Japan and South Korea are applying these sheets to EV roofs to enhance driving range through auxiliary solar charging.

Application Type Insights

Utility-scale installations lead the CIGS thin-film solar cells market, capturing around 45% of the total revenue share. The segment benefits from economies of scale, where large land-based solar farms prioritize stable performance, long module life, and predictable energy output.

Rigid CIGS panels are particularly favored as they deliver reliable performance even under high-temperature and diffuse-light conditions common across utility projects. For example, several pilot utility farms in the U.S. Southwest have adopted rigid CIGS modules to enhance output reliability in high-heat regions, reinforcing their advantage in large-scale deployments.

The commercial application represents the fastest-growing application type, driven by the rising adoption of BIPV, energy-efficient buildings, and sustainability-driven corporate initiatives. Flexible CIGS modules are particularly well-suited for commercial rooftops, facades, skylights, and shading structures, due to their lightweight and aesthetic appeal.

Businesses increasingly prefer CIGS panels for installations where roof load constraints, architectural design, or limited structural support prevent the use of heavy silicon modules. For example, flexible CIGS films are being incorporated into solar façades and canopy structures in modern European office buildings, accelerating adoption in commercial environments.

End-user Insights

The energy and power sector is anticipated to lead, accounting for 58.3% share in 2026, driven by widespread deployment across utility-scale, grid-support, and distributed generation systems. Governments and power companies favor CIGS modules for their lower energy payback time, strong temperature resilience, and ability to maintain output under diffuse or low-light conditions.

These advantages make CIGS particularly effective in large-area installations across varied climates. For example, several Asian utility developers have integrated CIGS modules into mid-scale grid-support projects to optimize performance during monsoon-induced low-irradiance periods, demonstrating their value in climate-variable regions.

The building and construction segment is the fastest-growing end-user segment, due to the rapid adoption of BIPV (Building-Integrated Photovoltaics). Architects, real-estate developers, and infrastructure planners are turning to flexible and semi-transparent CIGS modules for facades, roofs, shading devices, canopies, parking structures, and aesthetic solar surfaces.

The lightweight, bendable nature of CIGS eliminates the structural reinforcement required by silicon panels, making it attractive for retrofits and modern green buildings. For example, flexible CIGS laminates are being incorporated into solar façade systems in next-generation commercial complexes across Europe, supporting energy-positive building design.

The ability to merge energy generation with modern architectural aesthetics is positioning CIGS as a preferred solution for environmentally conscious construction.

Regional Insights

North America CIGS Thin-Film Solar Cells Market Trends

North America is likely to be a significant market for CIGS thin-film solar cells in 2026, supported by favorable policy incentives and growing interest in versatile solar technologies. The region’s established solar infrastructure and ambitious clean-energy goals are encouraging manufacturers and developers to explore CIGS modules for applications where their advantages, such as performance under high temperatures and low-light conditions, are particularly valuable.

Increasing interest in BIPV solutions for modern commercial buildings supports regional demand as architects seek aesthetic, low-load photovoltaic materials. For example, U.S. commercial campuses have begun piloting CIGS BIPV façade panels to achieve higher energy output without altering building design parameters.

The North American CIGS market continues to face challenges that limit rapid growth. Production complexities, reliance on scarce materials such as indium and gallium, and higher per-watt costs compared to crystalline silicon PV modules remain key obstacles. These factors make broad adoption difficult, particularly for residential customers who prioritize affordability and short-term return on investment.

Additionally, limited awareness of CIGS advantages slows uptake, as installers often favor silicon modules for their established reliability and industry familiarity. For instance, utility developers in states such as Texas and Arizona still predominantly select silicon modules for large-scale projects due to their lower costs and stronger financial bankability.

Europe CIGS Thin-Film Solar Cells Market Trends

Europe is likely to be a significant market for CIGS thin-film solar cells in 2026, driven by the region’s strong commitment to sustainability, renewable-energy targets, and green-building initiatives. The European Union’s push for decarbonization and environmental compliance encourages the adoption of advanced solar technologies, particularly where aesthetics, flexibility, and building integration matter.

Countries such as Germany, France, Spain, and the Netherlands are increasingly adopting CIGS for BIPV, façades, rooftops, and urban sites, where conventional rigid panels are less suitable. Growing demand for architectural solar solutions is accelerating CIGS adoption, especially in energy-efficient commercial buildings and heritage-site renovations.

Europe is seeing renewed investment in improving CIGS performance and manufacturing efficiency. The consortium project aims to bring commercial-scale CIGS cells closer to 25% power conversion efficiency, bridging the gap with traditional silicon modules.

These efforts are complemented by increasing demand for semi-transparent, thin, and rooftop-compatible solar panels that work well with code-compliant buildings and low-impact installations. The expanding interest in solar façades and integrated mobility hubs is creating new avenues for next-generation CIGS deployment across Europe.

For example, German municipal buildings have installed CIGS façade laminates to meet energy-efficiency targets without compromising architectural design.

Asia Pacific CIGS Thin-Film Solar Cells Market Trends

The Asia Pacific region is anticipated to be the leading region in the CIGS thin-film solar cells market with 40% share, in 2026, driven by robust manufacturing capacity, strong government support for renewable energy, and rapidly increasing solar installations across countries such as China, India, Japan, and South Korea.

Growing energy demand, expanding industrialization, and national targets for solar deployment have spurred large-scale uptake of CIGS modules, both for utility-scale plants and decentralized energy generation.

Asia Pacific is also likely to be the fastest-growing market for CIGS thin-film solar cells in 2026. Asia Pacific is witnessing a marked shift toward flexible, lightweight, and building-integrated photovoltaic (BIPV) applications using CIGS technology. Flexible and thin-film CIGS modules are increasingly used for rooftop solar, commercial buildings, off-grid systems, and even portable/remote-area installation scenarios where traditional rigid modules may not be feasible.

Asia Pacific is consolidating its lead in the global CIGS market and is shaping the future of thin-film solar deployment. Countries, including Vietnam, Indonesia, and the Philippines, are increasingly exploring flexible and building-integrated photovoltaic (BIPV) solutions to support growing commercial infrastructure and rooftop solar potential.

Competitive Landscape

The global CIGS thin-film solar cells market exhibits a moderately fragmented structure, driven by diverse demand for flexible, lightweight modules (BIPV, rooftop, portable) and by regional manufacturing capabilities that support both rigid and flexible CIGS production.

Smaller specialist firms coexist with larger industrial players as CIGS finds niche adoption where aesthetics, low weight, and performance under diffuse light matter; ongoing R&D and improving production yields are steadily raising commercial viability.

With key leaders including Solar Frontier, Hanergy (and its Solibro arm), MiaSolé, Avancis, Solo Power, Siva Power, and Flisom, the competitive field combines legacy thin-film know-how with newer flexible-module specialists. These players compete through higher cell conversion efficiencies, scale-up of manufacturing, strategic partnerships for BIPV and rooftop integration, targeted product portfolios (rigid vs. flexible), and cost-reduction programs.

Key Industry Developments:

- In March 2025, the Korea Institute of Energy Research (KIER) reached a significant milestone in next-generation photovoltaics by developing ultra-lightweight, flexible perovskite/CIGS tandem solar cells, achieving a record power-conversion efficiency of 23.64%. Reported in the journal Joule, this breakthrough showcases substantial efficiency improvements over traditional thin-film devices while preserving exceptional mechanical flexibility.

- In January 2025, Swedish thin-film solar pioneer Midsummer was selected by Italy’s Ministry of University and Research to join a high-level consortium developing an advanced new class of tandem solar cells. The project, titled Quantum Dot Enhanced Lightweight Solar Cells (QDELS), aims to create next-generation Quantum Dot CIGS/Perovskite tandem modules capable of surpassing the performance of traditional silicon technologies.

Companies Covered in CIGS Thin-Film Solar Cells Market

- First Solar, Inc.

- Solar Frontier K.K.

- Avancis GmbH

- MiaSolé Hi-Tech Corp.

- Solibro GmbH

- Global Solar Energy, Inc.

- HelioVolt Corporation

- Stion Corporation

- Ascent Solar Technologies, Inc.

- Hanergy Thin Film Power Group Limited

- Flisom AG

Frequently Asked Questions

The global CIGS thin-film solar cells market is projected to reach US$2.9 billion in 2026.

Key drivers include growth in renewable policies, tech efficiency, incentives, and rapid industrialization in emerging markets.

The CIGS thin-film solar cells market is expected to grow at a CAGR of 9.3% from 2026 to 2033.

Opportunities lie in the rapid expansion of flexible and lightweight solar applications, especially for BIPV, mobility, and portable power solutions.

First Solar, Inc., Solar Frontier K.K., Avancis GmbH, MiaSolé Hi-Tech Corp., Solibro GmbH, and Global Solar Energy, Inc. are the leading players.