- Advanced Materials

- Radiant Barrier Reflective Insulation Market

Radiant Barrier Reflective Insulation Market Size, Share, and Growth Forecast, 2025 - 2032

Radiant Barrier Reflective Insulation Market By Product Type (Foil-Based Radiant Barrier, Metalized Film Radiant Barrier, Others), by End-user (Residential, Commercial, and Industrial), and Regional Analysis for 2025 - 2032

Radiant Barrier Reflective Insulation Market Size and Trends Analysis

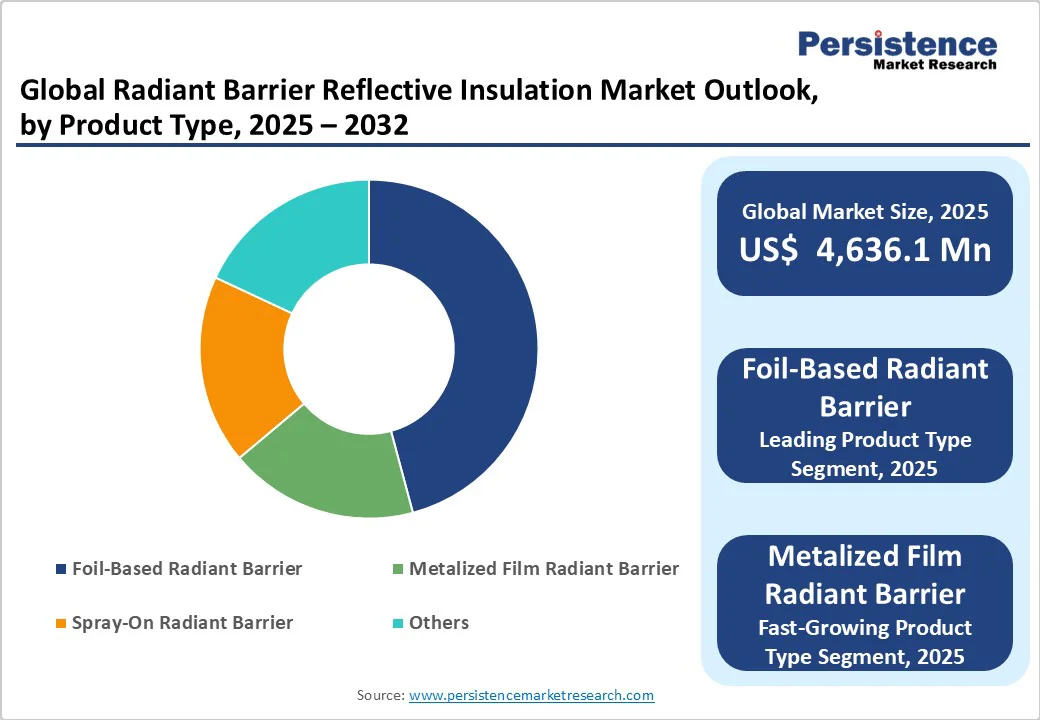

The global radiant barrier reflective insulation market size was valued at US$4,636.1 Million in 2025 and is projected to reach US$7,153.7 Million by 2032, growing at a CAGR of 6.4% between 2025 and 2032, driven by stringent energy conservation regulations and rising electricity costs.

Radiant barrier insulation is a thermal technology that reflects up to 97% of radiant heat using highly reflective surfaces, such as aluminum foil, reducing cooling loads and boosting energy efficiency in hot climates.

Key Industry Highlights

- Leading Product Type: Foil-based radiant barriers maintain 55.9% market leadership while metalized film barriers emerge as the fastest-growing segment with superior thermal performance.

- Leading Application: Residential applications dominate with 62.2% market share, supported by government incentives and DIY market trends, while the commercial segment shows the fastest growth.

- Regional Leadership: Asia Pacific leads with 38.8% regional market share driven by urbanization and infrastructure development, with North America representing the fastest-growing region.

- Strategic Developments: acquisitions by Kingspan Group in 2024 and Fi-Foil's Kennedy Insulation acquisition, indicating market consolidation trends.

- Government incentives and building codes create favorable market conditions, with potential 30-50% energy savings driving regulatory support and adoption acceleration.

- Technological innovations in metallization techniques and hybrid insulation systems enhance product performance and expand application opportunities in smart buildings.

| Key Insights | Details |

|---|---|

| Radiant Barrier Reflective Insulation Market Size (2025E) | US$4,636.1 Mn |

| Market Value Forecast (2032F) | US$7,153.7 Mn |

| Projected Growth (CAGR 2025 to 2032) | 6.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Energy Efficiency Regulations and Building Codes

Government mandates and building regulations aimed at reducing carbon emissions serve as primary catalysts for the radiant barrier market expansion. Countries including the U.S., Germany, China, and the UAE have introduced comprehensive energy codes that encourage or require energy-efficient building materials. The U.S. Department of Energy highlights that radiant barriers can reduce cooling costs by 5-10% when properly installed, directly supporting federal energy conservation goals.

In India, the Energy Conservation Building Code (ECBC) targets 30-50% energy savings in commercial buildings, with the potential to achieve 50% energy reduction by 2030. These regulatory frameworks create mandatory adoption environments, with compliance requirements driving approximately 40% of the market demand.

Rising Energy Costs and Environmental Sustainability Driving Market Growth

Rising global electricity costs and growing environmental awareness are driving the adoption of radiant barrier and reflective insulation systems. With energy accounting for 30-40% of building operational costs, these systems offer payback periods of just two to four years. Residential users can achieve 10-20% annual cooling savings, while commercial and industrial sectors leverage them for operational efficiency and sustainability goals.

Green building initiatives and certifications such as LEED, BREEAM, and GRIHA further promote reflective insulation for superior thermal performance. By reducing HVAC energy demand and greenhouse gas emissions, radiant barriers deliver both economic benefits and environmental value, supporting the shift toward net-zero energy buildings.

Barrier Analysis - High Installation Costs and Performance Sensitivity

Radiant barriers and reflective insulation systems, while offering significant energy-saving potential, face adoption challenges due to higher upfront costs and technical complexities. These materials are typically 15-25% more expensive than conventional insulation, such as fiberglass or foam, creating affordability concerns for price-sensitive homeowners and small-scale builders.

Retrofits in older buildings often require structural adjustments, increasing labor costs by 20-30%. Although energy savings and reduced HVAC loads usually offset costs within three to five years, the high initial investment deters immediate adoption.

Performance is highly installation-dependent; correct air-gap spacing, reflective surface orientation, and sealing are critical. Improper installation can reduce efficiency by 40-60%, resulting in inconsistent performance and dissatisfaction. Limited availability of trained contractors exacerbates this issue, particularly in regions without specialized expertise.

Moreover, radiant barriers are most effective in hot, sunny climates, limiting their applicability in colder regions. Standardized installation protocols, training programs, and material innovations, such as hybrid foils or nanocoatings, are essential to reduce costs, improve performance, and broaden market adoption.

Opportunity Analysis - Urbanization, Technological Innovation, and Policy Support

Rapid urbanization and infrastructure development across Asia-Pacific, Latin America, and the Middle East are fueling significant growth in the market, especially in rapidly developing economies, including China and India. Smart city initiatives and large-scale housing projects could push market potential beyond US$2 Billion by 2030. Technological innovations such as vacuum deposition, sputtering, and multi-layer hybrid systems are enhancing product efficiency, durability, and fire resistance.

Integration with IoT-based thermal monitoring and smart building automation is opening new avenues in energy-efficient architecture. Government incentives, subsidies, and tax rebates (ranging from 10-30%) are accelerating the adoption, supported by climate action policies and energy-efficiency mandates. The growing trend toward sustainable, retrofit-friendly solutions, including spray-on radiant barriers, further strengthens market outlook. Together, these dynamics highlight a future where reflective insulation becomes integral to modern, climate-responsive infrastructure worldwide.

Category-wise Analysis

Application Insights

Foil-based radiant barriers are anticipated to dominate the market with approximately 55.9% market share in 2025, attributed to superior heat reflection capabilities and established market presence. These products typically achieve 95-97% radiant heat reflection efficiency, making them highly effective in hot climates where solar heat gain is significant.

Manufacturing cost advantages and widespread installer familiarity contribute to sustained market leadership, with applications spanning residential attics, commercial roofing, and industrial facilities. The segment benefits from mature supply chains and standardized installation practices, reducing implementation barriers across multiple market segments.

The metalized film segment is experiencing notable growth driven by superior thermal performance, cost-effectiveness, and alignment with sustainable building practices. Advanced metallization techniques, including vacuum deposition and sputtering, have improved barrier properties and longevity, making these products preferred choices for modern insulation applications.

This segment attracts environmentally conscious consumers and commercial developers seeking high-performance solutions with reduced environmental impact. Growth rates of 7-8% CAGR exceed overall market expansion, indicating strong competitive positioning and market acceptance.

End-user Insights

The residential segment is projected to hold the largest market share at 62.2% in 2025, driven by increasing homeowner awareness of energy efficiency benefits and rising demand for sustainable building materials. Government incentives and building codes promoting energy-efficient housing significantly propel adoption, with relatively low installation costs and ease of retrofitting existing homes, making radiant barriers attractive investments.

Potential cooling cost savings of 10-20% in residential applications provide compelling value propositions for homeowners in hot climate regions. The segment benefits from growing DIY market trends and improved product accessibility through expanded distribution channels.

The commercial segment is experiencing robust growth, driven by increasing emphasis on energy efficiency and sustainability in commercial buildings. Large commercial structures face significant cooling demands, with radiant barriers helping reduce heat gain and lower operational costs.

Green building certification requirements and compliance with stringent energy codes encourage integration of radiant barriers in commercial construction projects. Long-term cost savings and improved occupant comfort make radiant barrier insulation appealing for commercial property owners and developers. Corporate sustainability targets and ESG compliance requirements further accelerate adoption in this segment.

Regional Insights

Asia Pacific Radiant Barrier Insulation Market Trends

Asia Pacific dominates the radiant barrier insulation market with approximately 38.8% market share in 2025, driven by extensive urbanization, infrastructure development, and rising energy costs. China emerges as a key market player due to aggressive energy-efficient urban development and massive residential and commercial construction activity. The government's emphasis on reducing carbon emissions and integrating energy-saving technologies accelerates adoption.

India's smart city initiatives and growing construction sector contribute significantly to regional growth, with favorable climate conditions making radiant barriers particularly effective. Japan and South Korea focus on sustainable construction practices and energy-efficient buildings, boosting regional demand. The region's hot and humid climate enhances radiant barrier effectiveness, especially in densely populated cities with high cooling demand.

North America Radiant Barrier Insulation Market Trends

North America, particularly the U.S., represents the fastest-growing regional market with strong demand driven by high energy consumption in residential and commercial buildings. The U.S. market benefits from a well-established DIY home improvement culture and Department of Energy recommendations for energy-efficient building materials. Southern states, including Texas, Florida, and California, drive substantial demand due to high air-conditioning usage and rising energy bills.

Federal tax incentives for energy-efficient retrofitting and stringent building energy codes support widespread adoption. The market is valued at approximately US$1.2 Billion in 2025 and projected to reach US$2.2 Billion by 2033, growing at a 7.3% CAGR. Commercial segments, including warehouses, schools, and retail chains, increasingly adopt radiant barriers to reduce operational costs.

Competitive Landscape

The global radiant barrier reflective insulation market exhibits a moderately fragmented competitive landscape with multiple established players holding significant market positions. Leading companies, including DuPont, Reflectix Inc., and Kingspan Group, maintain an estimated combined market share of 35-40%, while regional players and specialized manufacturers occupy the remaining market segments.

Market concentration is increasing through strategic acquisitions and partnerships, with larger companies expanding product portfolios and geographic reach. Competitive positioning emphasizes product innovation, manufacturing efficiency, and distribution network expansion as key differentiators.

Key Industry Developments

- Fi-Foil Company acquired Kennedy Insulation Group in 2023, significantly expanding its reflective insulation product line and market presence. Kingspan Group completed 19 acquisitions in 2024, including controlling stakes in Steico and Nordic Waterproofing, enhancing composite insulation capabilities.

- In December 2021, Balcan Innovations, the parent company of rFOIL, completed the acquisition of Reflectix Inc., a leading producer of reflective insulation and radiant barriers. This strategic move unified two of the industry’s foremost manufacturers under the Balcan Innovations umbrella, strengthening its market leadership and expanding its product portfolio in energy-efficient insulation solutions.

Companies Covered in Radiant Barrier Reflective Insulation Market

- DuPont

- Reflectix Inc.

- Innovative Insulation Inc.

- Dunmore Corporation

- Fi-Foil Company

- BMI Group

- LP Building Solutions

- Covertech Fabricating

- RadiantGUARD

- Kingspan Group

Frequently Asked Questions

The radiant barrier reflective insulation market is estimated to be valued at US$4,636.1 Million in 2025.

The key demand driver for the radiant barrier reflective insulation market is the rising global emphasis on energy efficiency and sustainable building practices.

In 2025, the Asia Pacific region will dominate the market with an estimated 38% revenue share in the radiant barrier reflective insulation market.

Among product types, foil-based radiant barrier holds the highest preference, capturing beyond 46.5% of the market revenue share in 2025, surpassing other applications.

Among end-users, residential holds the highest preference, capturing beyond 62.2% of the market revenue share in 2025, surpassing other applications.

The key players in the radiant barrier reflective insulation market include DuPont, Reflectix Inc., Innovative Insulation Inc., Dunmore Corporation, Fi-Foil Company, and BMI Group.