- Technology

- Zink Printing Market

Zink Printing Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Zink Printing Market by Component (ZINK-based Paper and ZINK-based Printer), by Functionality (Compact Photo Printers (Print only) and Camera with Printer (Camera and Print)), Connectivity (Bluetooth, NFC and Others), Application (Home/Individual and Commercial (Photography, Insurance, Photo Kiosks, Medical Labels, Commercial Signage) and Regional Analysis for 2026 - 2033

Zink Printing Market Size and Trends Analysis

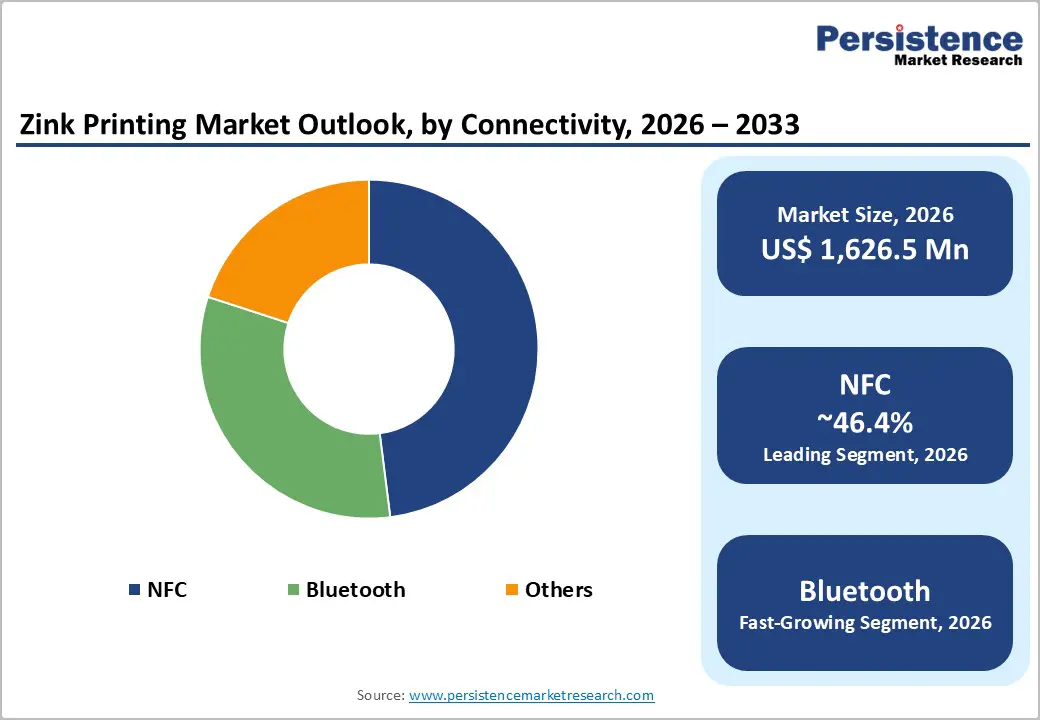

The global zink printing market size is likely to be valued at US$ 1,626.5 million in 2026 and is projected to reach US$ 2,126.0 million by 2033, growing at a CAGR of 3.9% between 2026 and 2033.

The market is driven by consumer preference for instant physical photo tangibility despite digital prevalence, expanding commercial use cases including insurance documentation and medical labeling, and improved printer affordability, enhancing market accessibility.

Key Industry Highlights:

- Leading Component Type: Zink based paper dominates with a 61.6% market share through a consumable, recurring-revenue model, while Printer hardware is the fastest-growing segment at an 8% CAGR, driven by form-factor innovation and affordability improvements.

- Dominant Connectivity Type: NFC connectivity commands 46.4% market share, reflecting seamless smartphone integration and standardized technology, while Bluetooth represents the fastest growing at 6% CAGR, driven by extended range and IoT integration capabilities.

- Primary Application Segment: Commercial applications establish 63.1% market share with photography studios, insurance, and medical labeling; Home/individual segment represents fastest-growing at 5% CAGR, driven by Gen Z retro-tech adoption momentum.

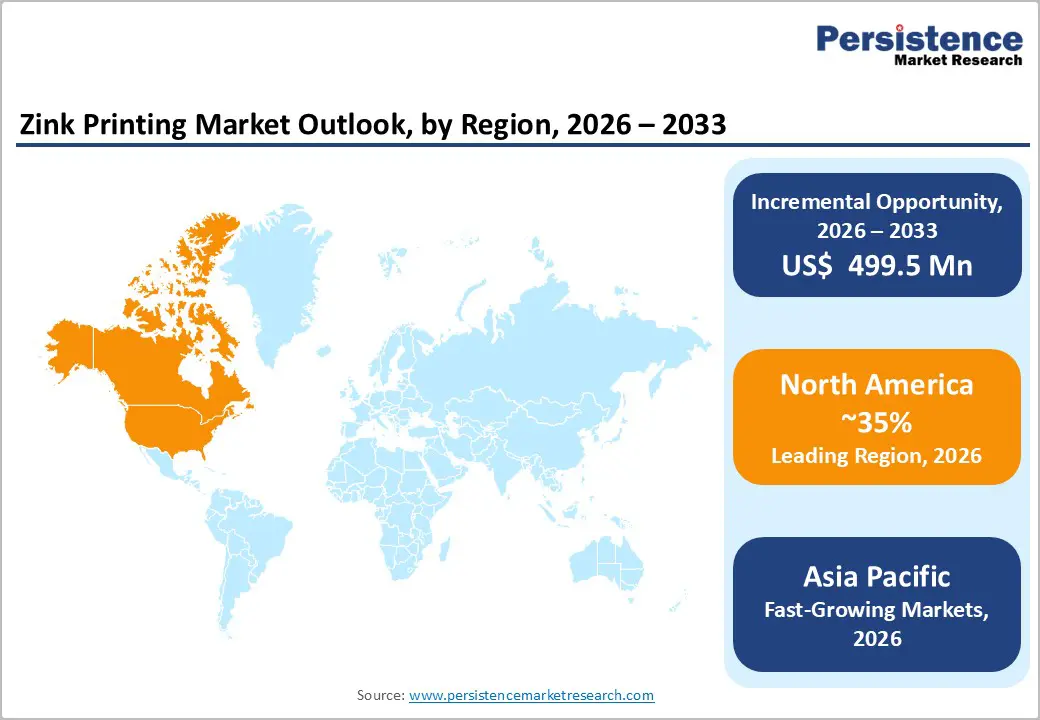

- Regional Market Leadership: North America maintains 35% global market share, driven by a shift in consumer sentiment toward tangible media; Europe commands 25% share, with photography's cultural heritage; Asia Pacific demonstrates the fastest regional growth at a 7% CAGR, expanding from a 22% current share to 30% by 2033.

- Consumer Retro-Tech Driver: 68% of North American millennials expressing desire for physical photo prints establishes a persistent demand foundation; 40% of 15-25-year-old consumers are interested in portable printing, creating substantial TAM expansion potential.

| Key Insights | Details |

|---|---|

| Zink Printing Market Size (2026E) | US$ 1,626.5 Mn |

| Market Value Forecast (2033F) | US$ 2,126.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 3.9% |

| Historical Market Growth (CAGR 2020 to 2024) | 3.2% |

Market Dynamics

Drivers - Revival of Analog Photo Culture and Tangible Memory Preservation Preferences

Consumer preferences, particularly among millennials and Generation Z demographics, demonstrate a pronounced shift toward tangible physical media despite digital prevalence, with survey data indicating 68% of young consumers desire physical photo prints. Zink printing technology, which enables instant photo materialization without elaborate darkroom processes, aligns with the emerging "retro-tech" consumer movement that values authentic analog experiences. Social media fatigue and digital oversaturation, with the average consumer generating 30+ photos daily but printing fewer than 2% annually, create a market opportunity for convenient physical photo production.

Zink printing economics, delivering a cost-per-print of US$ 0.50-1.50, comparable to smartphone data storage costs, establish price-competitive positioning versus traditional photo printing services. Event-based printing demand, including weddings, parties, and festivals, with instant photo-sharing capabilities, drives adoption of portable Zink printers at 20-25% annual growth. Environmental consciousness, with Zink technology producing zero hazardous waste compared to traditional ink-based printing, which requires cartridge disposal, appeals to sustainability-focused consumer segments.

Technological Advancement and Printer Affordability Improvements

Zink printer hardware costs have declined 35% over the past 5 years, with entry-level portable printers priced at US$ 100-300 compared to US$ 400-800 five years prior, expanding the consumer addressable market. Bluetooth and NFC connectivity integration, with 46.4% of devices supporting NFC and 35%+ supporting Bluetooth, enables seamless smartphone integration, eliminating complex setup requirements. Printer form factor miniaturization, with devices weighing 200-400 grams and pocket-sized dimensions, establishes portability advantages supporting adoption.

Battery technology advancement, enabling 8-12-hour continuous operation on single charge, establishes field deployment viability. Manufacturing efficiency improvements, with Zink paper production costs declining 20% through scale economies, establish improved unit economics supporting margin expansion. Competitive OEM licensing ecosystem, with HP, Lifeprint, Prynt, and C&A Global manufacturing Zink-compatible devices, establishes diverse product availability supporting broader market penetration.

Restraints -Digital Photo Dominance and Smartphone Display Proliferation

Digital photo prevalence remains entrenched, with consumers capturing 1.4+ trillion digital photos annually versus estimated 15-20 billion physical prints globally, establishing structural headwind against print-based solutions. Smartphone display technology advancement, with OLED/AMOLED screens delivering vibrant colors and always-on accessibility, reduces psychological motivation for physical photo printing. Cloud storage ubiquity, including Google Photos, iCloud, and Amazon Prime Photos offering unlimited digital storage, eliminates tangible media advantages for archival purposes.

Social media platform optimization for digital image sharing, including Instagram's algorithm prioritization of photo engagement, establishes preference for digital distribution versus physical prints. Digital printing alternatives, including inkjet and laser printing with higher quality and lower per-page costs for high-volume applications, constrain Zink positioning in traditional printing categories. Generational preferences, with older demographics (50+ years) preferring traditional inkjet solutions, limit growth potential in established consumer segments.

Zink Paper Supply Chain Concentration and Cost Economics

Zink paper production concentration, with Zink Holdings LLC controlling manufacturing and licensing arrangements, establishes supply chain dependency risk limiting competitive expansion. Paper cost structure, with Zink cartridges priced at US$ 0.75-1.50 per print, exceeds digital sharing costs approaching zero-marginal-cost, creating economic disadvantage. Zink patent portfolio, with continuing exclusive licensing arrangements and intellectual property protections extending through 2030+, prevents competitive entrants from developing alternative thermal printing substrates.

Thermal paper's environmental concerns, including potential BPA presence in earlier formulations, have created regulatory scrutiny, constraining certain applications. Paper durability limitations, with printed photos susceptible to fading under direct sunlight or extended storage periods without protective encasement, reduces value proposition versus digital archival. Printer compatibility ecosystem fragmentation, with proprietary OEM implementations preventing universal paper/printer interoperability, constrain consumer flexibility.

Opportunity - Healthcare and Pharmaceutical Labeling Market Expansion

Healthcare sector zink printing adoption, driven by regulatory requirements for medication labeling, patient identification, and diagnostic imaging documentation, represents a high-growth market opportunity. Pharmaceutical labeling applications, including blister pack printing, batch identification, and expiration date management, establish a specialized market segment valued at US$ 50-100 million with 12% annual growth. Medical imaging departments, incorporating zink printing for diagnostic hardcopy output, create proportionate equipment demand. Telemedicine expansion, requiring patient identification and secure documentation, drives Zink adoption in remote healthcare settings. Regulatory compliance drivers, including FDA labeling requirements and international pharmaceutical standards, mandate implementation.

IoT Integration and Autonomous Labeling Systems

Internet of Things (IoT) device integration, enabling automated label generation for inventory management, asset tracking, and logistics optimization, represents distinct market opportunity addressing unmet automation requirements. Smart retail applications, including dynamic price label generation and product information printing, drive proportionate demand for Zink printers. Warehouse automation, leveraging Zink printing for parcel labeling and shipment documentation, expands commercial deployment opportunities. Connected printer ecosystems, integrating Zink devices with enterprise resource planning (ERP) and warehouse management systems, establish comprehensive labeling automation platforms. Market projections indicate that IoT-integrated Zink solutions will represent 20-30% of commercial deployments by 2033, translating into a US$ 200-300 million incremental market opportunity. Manufacturing sector automation, including parts identification and quality control labeling, represents emerging high-value application segment.

Category-wise Analysis

Component Insights

Zink-based paper accounts for 61.6% market share due to its consumable nature, which generates recurring revenue beyond one-time printer purchases. Using embedded dye crystals activated by thermal printing, Zink paper relies on a proprietary supply chain controlled by Zink Holdings LLC. Standard 2×3-inch formats align with portable printers, enabling manufacturing efficiency and healthy margins, with retail prices of US$1.00-1.50 per print. Annual production of 300-400 million sheets highlight market maturity, while adhesive-backed options expand label and sticker applications.

Zink-based printers are the fastest-growing component, projected to grow at 8% CAGR through 2033. Advances in miniaturization, Bluetooth/NFC connectivity, falling hardware costs, and longer battery life are boosting adoption. A competitive OEM ecosystem and innovation-led differentiation continue to drive printer market expansion.

Connectivity Insights

NFC connectivity holds 46.4% market share due to its simplicity, security, and widespread smartphone integration. Single-tap pairing delivers a superior user experience with minimal setup, while compatibility across Android and iOS platforms ensures broad adoption. NFC’s short operating range of 4-10 cm enhances secure authentication for personal devices. Standardization under ISO 14443 enables multi-vendor interoperability, and low component costs support price-competitive product designs. A large existing NFC ecosystem across payments and retail further reinforces its dominance.

Bluetooth is the fastest-growing connectivity segment, expanding at 7% CAGR through 2033. Bluetooth 5.0 offers extended range, improved power efficiency, and multi-device connectivity, supporting commercial and IoT use cases. Falling module costs and growing ecosystem integration are accelerating adoption for remote printing and smart-device applications.

Application Insights

Commercial applications account for 63.1% market share, driven by business-oriented printing needs and favorable unit economics. Photography studios, including event, portrait, and festival operators, form the largest commercial user base. Insurance companies deploy portable printers extensively for on-site claims documentation, while healthcare facilities use Zink printing for patient identification and medication labeling. Retail photo kiosks and entertainment venues further expand commercial installations, alongside signage and promotional labeling applications. Higher price tolerance, with businesses accepting US$ 1.00-2.00 per print, supports strong profitability.

Home and individual applications are the fastest-growing segment, expanding at 6% CAGR through 2033. Adoption is rising rapidly among millennials and Gen Z, driven by event printing, social media-inspired keepsakes, scrapbooking, and crafting. Strong interest among younger consumers highlights significant long-term market expansion potential.

Regional Market Share and Insights

North America Zink Printing Market Analysis

North America commands approximately 35% of the global Zink printing market share, valued at approximately US$ 620 million in 2026, with projections approaching US$ 800 million by 2033. The U.S represents the dominant regional market contributor, accounting for 85% of North American market value, driven by consumer retro-tech adoption momentum and commercial printing infrastructure.

The shift in consumer sentiment toward tangible photo retention, with 72-78% of North American millennials expressing a desire for physical prints, is the primary market driver. Event and entertainment industry adoption, with music festivals, sporting events, and wedding venues deploying Zink printing solutions at 15-20% annual growth, drives commercial demand. Insurance industry deployment, with major carriers implementing field documentation systems, establishes a sustained procurement driver.

Europe Zink Printing Market Analysis

Europe represents approximately 25% of the global Zinc printing market share, valued at approximately US$ 410 million in 2026. Germany, the United Kingdom, France, and Spain collectively represent 75% of the European market value, reflecting an established photography culture and commercial printing infrastructure.

Photography heritage and cultural emphasis on photo preservation, particularly in Germany and France, represents the primary market driver. Commercial photography studio adoption, with established photo service industry integrating Zink solutions, drives market penetration. An emphasis on regulatory compliance, including environmental and chemical composition standards, influences supply chain decisions.

Asia Pacific Zink Printing Market Analysis

Asia Pacific demonstrates robust growth dynamics, commanding approximately 22% market share with projections increasing to 30% by 2033. The region valued at approximately US$ 325 million in 2026 is anticipated to reach US$ 800 million by 2033, representing the fastest-growing regional market with an estimated CAGR of 13%.

The smartphone adoption explosion, with 1.8+ billion users, creates a massive portable printing opportunity and is the primary regional differentiator. Emerging middle-class consumer segments, with growing discretionary spending enabling affordable Zink printer acquisition, establish rapid demand expansion. Government digitalization initiatives, including identity programs and public documentation systems, create proportionate demand.

Regional investment focuses on manufacturing capacity expansion and affordable pricing strategies, with manufacturers collectively allocating US$150-250 million annually to Asia Pacific market development through 2033.

Competitive Landscape

The global zink printing market demonstrates moderate consolidation with specialized printer manufacturers and diversified consumer electronics companies maintaining competitive positions through product innovation and distribution ecosystem development. The top 8 suppliers, including HP, Lifeprint, Prynt, C&A Global, Fujifilm, IDPRT, Hiti, and others, collectively control approximately 60% of global market share, reflecting incumbent advantages and distribution relationships.

Market structure reflects a bifurcation between consumer-focused portable printer developers (Lifeprint, Prynt), emphasizing style and affordability, and established imaging company OEMs (HP, Fujifilm), leveraging their heritage distribution networks.

Key Industry Developments

- In March 2024, Prynt announced Neon-colored printer models and expanded its lifestyle positioning to target younger demographics. Influencer partnership campaigns on TikTok and Instagram generated a 40% lift in awareness among the target demographic. Community printing events are establishing Prynt as a lifestyle brand rather than a peripheral device.

- In January 2023, Canon has launched the brand-new big format desktop printer from image Prograf. The ultra-low-volume market, comprising AEC offices, educational institutions, and the hospitality sector, is the target market for this printer.

- In October 2022, HP (Hewlett-Packard) Inc. announced that the HP PageWide Web Press T485 HD with HP Brilliant Ink is the latest inkjet web press for high-volume output.

Companies Covered in Zink Printing Market

- Hewlett-Packard Inc.

- Eastman Kodak Company

- Brother Industries, Ltd.

- L.G Electronics Inc.

- ZINK Holdings LLC

- Lifeprint

- PRYNT Corp.

- Dell Inc.

- Polaroid

- Others Key Players

Frequently Asked Questions

The Zink Printing market is estimated to be valued at US$ 1,626.5 Mn in 2026.

The primary demand driver for the Zink printing market is the growing need for instant, portable, and ink-free photo printing, driven by mobile-centric consumer behavior and on-the-go commercial use cases.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Zink Printing market.

Among the Connectivity, NFC holds the highest preference, capturing beyond 46.4% of the market revenue share in 2026, surpassing other Connectivity type.

The key players in Zink Printing are Hewlett-Packard Inc., Eastman Kodak Company, Brother Industries, Ltd. and L.G Electronics Inc.